|

市场调查报告书

商品编码

1940804

新加坡网路安全:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Singapore Cybersecurity - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

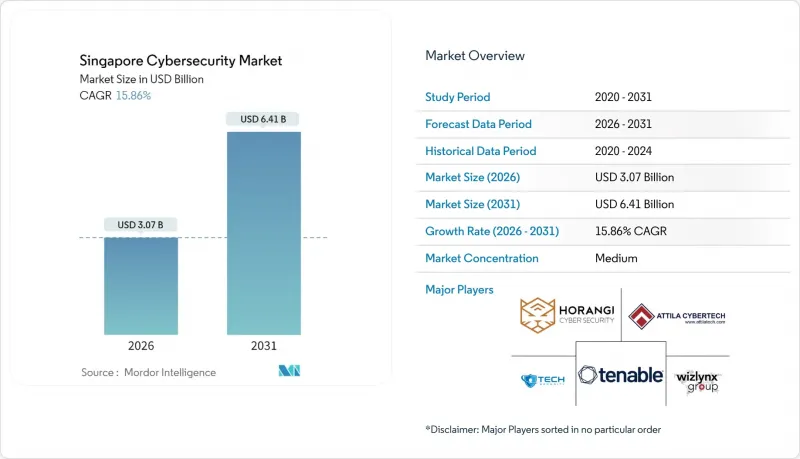

预计到 2026 年,新加坡网路安全市场规模将达到 30.7 亿美元。

这意味着从 2025 年的 26.5 亿美元成长到 2031 年的 64.1 亿美元,2026 年至 2031 年的复合年增长率为 15.86%,巩固了该城邦作为东南亚数位指挥中心的地位。

经营团队成长要素于威胁数量的上升(网路犯罪将在2023年占所有已记录犯罪的49.2%)以及超大规模资料中心投资密度的不断增加(到2024年中期,运作中或已签约的IT负载将超过1.4吉瓦)。采购部门现在评估产品的标准不再是功能数量,而是其提供的风险降低能力,67%的大型企业要求在2024年的合约中明确关键风险指标。 IT和OT防御的显着转变反映了自动化港口码头和智慧工厂倾向于采用单一安全控制平面而非孤立的系统架构的趋势。自2023年中期以来,在关键基础设施中强制实施的零信任策略已使银行的未经授权特权存取事件减少了42%。

新加坡网路安全市场趋势与洞察

政府强制推行全国零信任架构

监管机构现要求所有关键资讯基础设施所有者提交零信任蓝图,截至2024年11月,已有96%的所有者提交了计画。金融机构实施了流量微隔离,并在实施的第一年内,未经授权的权限事件减少了42%。在预算週期中,高达28%的安全支出被分配给了身分分析,这显示市场对情境察觉存取控制的需求十分旺盛。多机构设计审查流程的简化将策略核准时间缩短至34天,使传统的审批延迟减少了一半,从而帮助供应商加快了收入确认。这些趋势共同推动零信任实施成为主要竞标机会的核心,使支持自适应信任评分的供应商获得了决定性的优势。

加速数位银行牌照发放,推动下一代银行、金融服务和保险(BFSI)安全支出

预计2024年底,取得数位牌照的银行将吸收18亿新元的存款,相当于新加坡零售储蓄总额的4%。新进业者在第一年将约22%的营运支出用于网路安全,现有银行也采取了类似的投入,到2024年,它们将网路安全方面的投资增加36%,达到4.91亿新元。后量子密码技术的试点部署已经保障了12%的国内银行间交易安全。如今,竞争格局的关键在于快速收集威胁情报和自动化合规认证,预算正从独立设备转向託管式侦测和回应平台。银行业早期采用这些技术的趋势正在蔓延至支付、资产管理和资本市场系统,扩大了新加坡网路安全市场的潜在需求。

CREST认证人员短缺推高了服务成本。

截至2024年,新加坡本地仅有530名CREST认证专业人员,与1,200人的需求相比,缺口高达56%。高级分析师的薪资中位数已上涨14%至11.7万新元,挤压了资安管理服务提供者(MSSP)的利润空间。儘管MSSP已透过自动化将一级安全工单量减少了35%,但许多公司仍透过提高授权授权价格来承担薪资上涨的成本。持续的人才短缺正在延缓大规模部署,延长上运作时间,并阻碍近期收入成长。除非人才储备得到显着扩充,否则人才供不应求将继续限制新加坡网路安全市场实现预期成长的能力。

细分市场分析

到2025年,服务业将占据新加坡网路安全市场份额的59.60%,其中託管保全服务收入将达到23亿新元。平均检测时间(MTDI)将从2022年的8小时缩短至2024年的2小时,充分体现了全天候监控的投资回报。整合跨国威胁情报的供应商续约率高达92%,远超过84%的产业中位数。客户越来越多地将监控服务与保险仲介和事件回应合约结合,为资安管理服务提供者(MSSP)创造了类似年金的收入来源。这些因素正推动新加坡网路安全市场持续保持两位数的强劲成长。

预计到2031年,云端安全市场将维持15.52%的复合年增长率,主要得益于企业云端工作负载84%的渗透率。新加坡金融管理局(MAS)修订的法规将强制控制目标的数量从8个增加到11个,在加强实质审查週期的同时,也扩大了可用支出规模。目前,结合了态势管理和自动化修復功能的供应商每月平均为每位客户执行37次策略更新,是2022年的三倍。付费使用制使得在电子商务高峰期能够快速扩展。因此,预计在新加坡的网路安全市场,云端原生解决方案的成长速度将持续超过设备更新。

即使到了2025年,本地部署仍将占据新加坡网路安全市场份额的54.30%,其中71%的金融业资料库託管在可信任的资料中心。四级资料中心的机房面积达66万平方公尺,为各大银行和支付网路提供延迟可控的环境。混合取证工作流程已将证据处理时间缩短了27%,展现了受监管工作负载分阶段迁移的路径。因此,许多现有企业在试点云端优先应用的同时,也不断更新其边界硬体。

预计在2025年至2027年间新增300兆瓦超大规模IT负载的推动下,云端采用率将以16.93%的复合年增长率成长。符合绿色资料中心标准的营运商可实现低于1.3的PUE值,进而释放能源预算用于机架内安全加速器。新的批量授权定价收费系统(按CPU秒收费)已将月度帐单波动性降低了18%,减轻了财务长的担忧。更快的配置速度使Start-Ups能够在数小时内而非数週内运作SOC基础设施。这些优势将使云端采用率继续保持在新加坡网路安全市场的前沿地位。

新加坡网路安全市场报告按产品类型(解决方案、服务)、部署模式(云端、本地部署)、最终用户垂直产业(银行、金融服务和保险、医疗保健、IT 和电信、工业和国防、製造业、零售和电子商务、能源和公共产业、其他)以及最终用户公司规模(中小企业、大型企业)对产业进行细分。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 新加坡政府强制推行全国零信任架构

- 加速数位银行牌照发放,推动下一代银行、金融服务和保险(BFSI)安全支出

- 新加坡交易所上市公司的强制性网路安全事件揭露规则

- 由于大士港和裕廊岛重建项目,对OT安全的需求增加。

- 5G SA 网路部署需要云端原生安全功能

- 研发税收优惠(针对国内网路安全智慧财产权的创造)

- 市场限制

- CREST认证人员短缺导致服务成本上升。

- 分散的中小企业市场仍将传统防毒产品视为价格优势。

- 资料主权条款限制外国託管服务提供者 (MSSP) 的资料湖託管

- 合规性重迭度高(CSA CCOP 与 MAS TRM),导致销售週期过长

- 关键法规结构评估

- 价值链分析

- 技术展望

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 主要用例和案例研究

- 宏观经济因素对市场的影响

- 投资分析

第五章 市场区隔

- 报价

- 解决方案

- 应用程式安全

- 云端安全

- 资料安全

- 身分和存取管理

- 基础设施保护

- 综合风险管理

- 网路安全设备

- 端点安全

- 其他服务

- 服务

- 专业服务

- 託管服务

- 解决方案

- 透过部署模式

- 本地部署

- 云

- 按最终用户行业划分

- BFSI

- 卫生保健

- 资讯科技和电信

- 工业与国防

- 製造业

- 零售与电子商务

- 能源与公共产业

- 其他的

- 按最终用户公司规模划分

- 小型企业

- 大公司

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Ensign InfoSecurity

- ST Engineering(Digital Systems)

- Horangi Cyber Security

- Palo Alto Networks(Singapore)

- Cisco Systems(Singapore)

- IBM Security Singapore

- Check Point Software Technologies(SG)

- Fortinet Singapore

- FireEye Mandiant(Singapore)

- Trend Micro Singapore

- CrowdStrike Singapore

- Darktrace Singapore

- Splunk Singapore

- SecureAge Technology

- Quann(Subsidiary of Certis)

- Group-IB Singapore

- V-Key

- Wizlynx Pte Ltd

- InsiderSecurity

- WebOrion

- GROUP8

- Blackpanda

第七章 市场机会与未来展望

Singapore Cybersecurity market size in 2026 is estimated at USD 3.07 billion, growing from 2025 value of USD 2.65 billion with 2031 projections showing USD 6.41 billion, growing at 15.86% CAGR over 2026-2031 and confirming the city-state's status as Southeast Asia's digital command center.

Corporate boards attribute the growth to elevated threat volumes-cybercrime already formed 49.2% of all offences logged in 2023-and to the rising density of hyperscale data-center investments that surpassed 1.4 GW of active or committed IT load by mid-2024. Procurement teams now judge offerings on delivered risk reduction rather than feature counts, with 67% of large enterprises insisting on key-risk indicators in 2024 contracts. A pronounced shift toward converged IT-OT defence reflects automated port terminals and smart factories that prefer one security control plane over siloed stacks. Zero-trust policies, mandated across critical infrastructure, have already trimmed unauthorized-privilege cases at banks by 42% since mid-2023.

Singapore Cybersecurity Market Trends and Insights

Nationwide Zero-Trust Architecture Mandates from Government

Regulators now compel every critical information-infrastructure owner to file a zero-trust roadmap, and 96% had submitted plans by November 2024. Financial institutions responded by micro-segmenting traffic, cutting unauthorized-privilege cases by 42% within one year of go-live. Budget cycles allocate up to 28% of security outlays to identity analytics, underscoring demand for context-aware access controls. Streamlined multi-agency design reviews compressed policy-approval windows to 34 days, halving historical delays and allowing vendors to accelerate revenue recognition. Together, these moves place zero-trust enforcement at the heart of every major tender, giving suppliers that support adaptive trust scoring a decisive edge.

Accelerated Digital-Bank Licences Driving Next-Gen BFSI Security Spend

Digital full-bank licensees accumulated SGD 1.8 billion in deposits by end-2024, equal to 4% of Singapore's retail savings pool. Each new entrant channelled roughly 22% of operating expenditure into cybersecurity during its first year, an intensity mirrored by incumbents whose resilience investments grew 36% to SGD 491 million in 2024. Pilot deployments of post-quantum cryptography already protect 12% of domestic interbank traffic. Competitive parity now hinges on rapid threat-intelligence ingestion and automated compliance evidence, redirecting budgets toward managed detection and response platforms rather than standalone appliances. The banking cluster's early adoption curves ripple through payments, wealth management and capital-markets systems, magnifying total addressable demand for the Singapore Cybersecurity market.

Scarce Pool of CREST-Certified Talent Inflates Service Costs

Only 530 CREST-certified professionals operated locally in 2024 against demand for 1,200, equating to a 56% gap. Median senior-analyst pay climbed 14% to SGD 117,000, compressing margins for managed security service providers. MSSPs used automation to trim Tier-1 ticket volumes by 35%, yet many still absorb wage inflation by passing through higher seat-licence prices. Persistent scarcity delays large rollouts, elongating go-live timelines and dampening short-term revenue conversion. Unless training pipelines expand materially, talent supply will continue to limit the Singapore Cybersecurity market's ability to scale at the forecast rate.

Other drivers and restraints analyzed in the detailed report include:

- SGX-Listed Firms' Mandatory Cyber-Incident Disclosure Rules

- Heightened OT-Security Demand from Tuas Mega-Port and Jurong Island Revamp

- Fragmented SME Market Still Anchored on Legacy Antivirus

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services contributed 59.60% to the Singapore Cybersecurity market share in 2025, helped by managed security service revenues of SGD 2.3 billion. Average mean-time-to-detect dropped from eight hours in 2022 to two hours in 2024, proving the return on 24/7 monitoring investments. Providers that integrate cross-border threat-intelligence achieved 92% renewal, outpacing the sector median of 84%. Clients increasingly bundle insurance broking and incident-response retainers with monitoring, creating annuity-like revenue for MSSPs. These factors sustain robust double-digit expansion for the Singapore Cybersecurity market.

Cloud security is on track for a 15.52% CAGR through 2031, riding on 84% enterprise cloud-workload penetration. Updated MAS rules expanded mandatory control objectives from eight to 11, intensifying due-diligence cycles yet enlarging addressable spend. Vendors that pair posture management with auto-remediation now execute 37 policy updates per client each month, triple 2022 volumes. Consumption-based pricing fits well with rapid scale-out during peak e-commerce seasons. As a result, cloud-native solutions will continue to outpace appliance refreshes inside the Singapore Cybersecurity market.

On-premise installations still held 54.30% of the Singapore Cybersecurity market share in 2025, with 71% of financial-sector databases co-located in trusted facilities. Tier-4 floor space reached 660,000 m2, providing large banks and payment networks with latency-controlled environments. Hybrid forensics workflows lowered evidence-processing time by 27%, validating a staged migration path for regulated workloads. Accordingly, most incumbents continue to refresh perimeter hardware even while piloting cloud-first applications.

Cloud deployments promise a 16.93% CAGR, buoyed by an extra 300 MW of hyperscale IT load planned for 2025-2027. Operators meeting the Green Data Centre standard report PUE below 1.3, releasing energy budgets for in-rack security accelerators. New bulk-licence tariffs priced per CPU-second reduced monthly invoice volatility by 18%, easing CFO concerns. Faster provisioning times allow startups to activate SOC infrastructure in hours rather than weeks. These advantages will keep cloud adoption at the forefront of the Singapore Cybersecurity market.

The Singapore Cybersecurity Market Report Segments the Industry Into by Offering (Solutions, and Services), Deployment Mode (Cloud, and On-Premise), End-User Vertical (BFSI, Healthcare, IT and Telecom, Industrial and Defense, Manufacturing, Retail and E-Commerce, Energy and Utilities, Others), and End-User Enterprise Size (Small and Medium Enterprises (SMEs), and Large Enterprises)

List of Companies Covered in this Report:

- Ensign InfoSecurity

- ST Engineering (Digital Systems)

- Horangi Cyber Security

- Palo Alto Networks (Singapore)

- Cisco Systems (Singapore)

- IBM Security Singapore

- Check Point Software Technologies (SG)

- Fortinet Singapore

- FireEye Mandiant (Singapore)

- Trend Micro Singapore

- CrowdStrike Singapore

- Darktrace Singapore

- Splunk Singapore

- SecureAge Technology

- Quann (Subsidiary of Certis)

- Group-IB Singapore

- V-Key

- Wizlynx Pte Ltd

- InsiderSecurity

- WebOrion

- GROUP8

- Blackpanda

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Nationwide zero-trust architecture mandates from Singapore Government

- 4.2.2 Accelerated digital-bank licences driving next-gen BFSI security spend

- 4.2.3 SGX-listed firms' mandatory cyber-incident disclosure rules

- 4.2.4 Heightened OT-security demand from Tuas mega-port & Jurong Island revamp

- 4.2.5 Roll-out of 5G SA networks necessitating cloud-native security functions

- 4.2.6 R&D tax-incentives for local cybersecurity IP creation

- 4.3 Market Restraints

- 4.3.1 Scarce pool of CREST-certified talent inflates service costs

- 4.3.2 Fragmented SME market still price-anchored on legacy antivirus

- 4.3.3 Data-sovereignty clauses limiting foreign MSSP data-lake hosting

- 4.3.4 High compliance overlap (CSA CCOP vs. MAS TRM) elongates sales cycles

- 4.4 Evaluation of Critical Regulatory Framework

- 4.5 Value Chain Analysis

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Key Use Cases and Case Studies

- 4.9 Impact on Macroeconomic Factors of the Market

- 4.10 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By Offering

- 5.1.1 Solutions

- 5.1.1.1 Application Security

- 5.1.1.2 Cloud Security

- 5.1.1.3 Data Security

- 5.1.1.4 Identity and Access Management

- 5.1.1.5 Infrastructure Protection

- 5.1.1.6 Integrated Risk Management

- 5.1.1.7 Network Security Equipment

- 5.1.1.8 Endpoint Security

- 5.1.1.9 Other Services

- 5.1.2 Services

- 5.1.2.1 Professional Services

- 5.1.2.2 Managed Services

- 5.1.1 Solutions

- 5.2 By Deployment Mode

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.3 By End-User Vertical

- 5.3.1 BFSI

- 5.3.2 Healthcare

- 5.3.3 IT and Telecom

- 5.3.4 Industrial and Defense

- 5.3.5 Manufacturing

- 5.3.6 Retail and E-commerce

- 5.3.7 Energy and Utilities

- 5.3.8 Others

- 5.4 By End-User Enterprise Size

- 5.4.1 Small and Medium Enterprises (SMEs)

- 5.4.2 Large Enterprises

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Ensign InfoSecurity

- 6.4.2 ST Engineering (Digital Systems)

- 6.4.3 Horangi Cyber Security

- 6.4.4 Palo Alto Networks (Singapore)

- 6.4.5 Cisco Systems (Singapore)

- 6.4.6 IBM Security Singapore

- 6.4.7 Check Point Software Technologies (SG)

- 6.4.8 Fortinet Singapore

- 6.4.9 FireEye Mandiant (Singapore)

- 6.4.10 Trend Micro Singapore

- 6.4.11 CrowdStrike Singapore

- 6.4.12 Darktrace Singapore

- 6.4.13 Splunk Singapore

- 6.4.14 SecureAge Technology

- 6.4.15 Quann (Subsidiary of Certis)

- 6.4.16 Group-IB Singapore

- 6.4.17 V-Key

- 6.4.18 Wizlynx Pte Ltd

- 6.4.19 InsiderSecurity

- 6.4.20 WebOrion

- 6.4.21 GROUP8

- 6.4.22 Blackpanda

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

网路安全市场:按组件、安全类型、组织规模、部署模式和产业划分-2026-2032年全球市场预测

网路安全市场:按组件、安全类型、组织规模、部署模式和产业划分-2026-2032年全球市场预测 人工智慧网路安全市场预测至2034年—按交付方式、安全类型、部署方式、技术、应用、最终用户和地区分類的全球分析金融科技网路安全解决方案市场预测至2034年-按组件、安全类型、部署模式、组织规模、应用、最终用户和地区分類的全球分析

人工智慧网路安全市场预测至2034年—按交付方式、安全类型、部署方式、技术、应用、最终用户和地区分類的全球分析金融科技网路安全解决方案市场预测至2034年-按组件、安全类型、部署模式、组织规模、应用、最终用户和地区分類的全球分析 2026-2030年全球智慧体与自主人工智慧系统网路安全解决方案市场

2026-2030年全球智慧体与自主人工智慧系统网路安全解决方案市场 网路安全市场规模、份额、趋势和预测:按组件、部署类型、用户类型、行业和地区划分,2026-2034 年

网路安全市场规模、份额、趋势和预测:按组件、部署类型、用户类型、行业和地区划分,2026-2034 年 2026年全球建筑网路安全市场报告2026年全球电网网路安全市场报告2026年全球旅游安全市场报告

2026年全球建筑网路安全市场报告2026年全球电网网路安全市场报告2026年全球旅游安全市场报告 全球网路靶场市场报告:实际结果与预测(2021-2032)2026年全球Web3安全市场报告

全球网路靶场市场报告:实际结果与预测(2021-2032)2026年全球Web3安全市场报告