|

市场调查报告书

商品编码

1940812

美国网路安全:市场份额分析、行业趋势和统计数据以及成长预测(2026-2031 年)US Cybersecurity - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

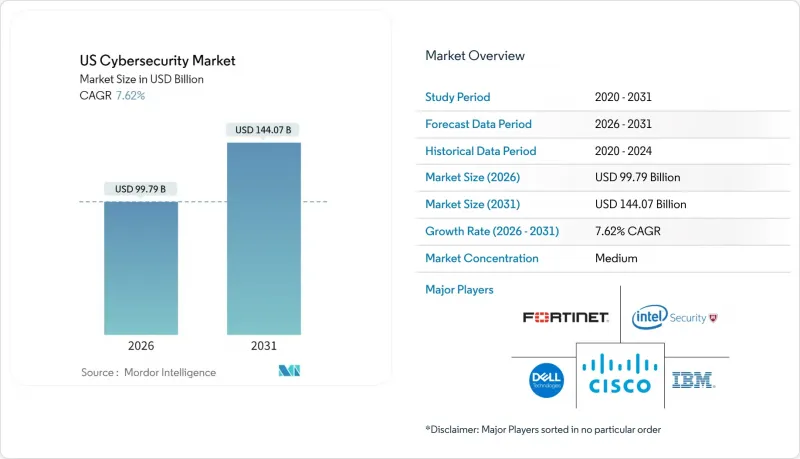

美国网路安全市场预计将从 2025 年的 927.3 亿美元成长到 2026 年的 997.9 亿美元,到 2031 年达到 1,440.7 亿美元,2026 年至 2031 年的复合年增长率为 7.62%。

这项成长主要受联邦政府零信任指令、针对关键基础设施的勒索软体攻击激增以及云端迁移加速推动,目前已有94%的组织采用多重云端环境。儘管如此,本地部署架构仍然占据最大份额,因为国防、金融服务和医疗保健行业的企业仍在维护必须保持本地控制的旧有系统。然而,随着企业寻求可扩展的保护和即时威胁情报,云端交付的安全解决方案正以15%的复合年增长率持续成长。创投持续推动创业投资,预计到2024年,美国网路安全Start-Ups将获得116亿美元的投资,其中大部分将用于开发能够减轻分析师工作量的AI驱动型威胁侦测平台。美国证券交易委员会(SEC)强制性的资料外洩揭露规则、不断上涨的网路保险费以及持续的人才短缺等因素共同作用,强化了长期需求,使美国网路安全市场成为公共和私营部门的战略重点。

美国网路安全市场趋势与洞察

联邦零信任指令加速各机构安全现代化进程

第14028号行政命令强制所有民事机构采用零信任架构,启动了一项为期多年的现代化计划,该项目的影响也将波及州和地方政府。国防安全保障部近期向ASRC Federal公司授予1700万美元,用于美国公民及移民服务局(USCIS)的整合服务;财政部新推出的200亿美元PROTECTS计画也展现了联邦政府的强大采购能力。已有23个州发布了零信任蓝图,其中加州累计5000万美元,旨在到2026年实现所有机构以身分为中心的管理。承包商也必须效仿,将零信任要求深入国防和金融服务供应链的各个环节。这种连锁反应使美国网路安全市场成为持续公共部门支出的最大受益者。

针对中型医疗和教育机构的勒索软体攻击激增

2024年2月,Change Healthcare的资料外洩事件导致6.7万家药局的处方笺处理系统瘫痪,联合健康集团(UnitedHealth Group)为此支付了23亿美元的补救费用。三个月后,Ascension Health也遭遇了类似的危机,勒索软体攻击瘫痪了旗下140家医院的电子健康记录系统。美国卫生与公众服务部证实,去年有1亿份病患纪录遭洩露,增加了联邦政府对医院升级防御系统的压力。教育机构同样面临风险,联邦调查局(FBI)报告称,由于勒索软体攻击导致学生服务资料库被清除,多所学校被迫关闭。这些事件加剧了网路安全投入的迫切性,预计网路安全领域的复合年增长率将达到14.6%,远超美国整体网路安全市场的成长速度。

各州隐私法规的碎片化使供应商合规性变得复杂。

加州的《加州消费者隐私法案》(CCPA)、维吉尼亚的《消费者资料保护法案》(CDPA) 和康乃狄克州的《消费者资料保护和揭露法案》(CTDPA) 各自对资料外洩通知和消费者权益提出了不同的要求,迫使供应商必须遵守各州的合规规定。美国证券交易委员会 (SEC) 修订后的《SP条例》要求金融机构在资料外洩发生后 30 天内通知个人,这与各州更为严格的期限有所重迭。中型安全服务提供商报告称,其每年平均合规成本高达 230 万美元,这挤压了利润空间并阻碍了市场准入。监管碎片化减缓了产品部署速度,使产品上市计划更加复杂,预计将使美国网路安全市场的复合年增长率 (CAGR) 下降约 1.2 个百分点。

细分市场分析

解决方案是主要的收入驱动力,预计到2025年将占美国网路安全市场份额的67.30%,而託管服务预计到2031年将以15.1%的复合年增长率增长。在联邦政府推行零信任政策后,身分和存取管理(IAM)的采用率激增,而随着容器化开发平臺的普及,应用安全支出也随之成长。网路安全设备正被软体定义替代方案所取代,而终端保护正在演变为XDR套件,该套件可从笔记型电脑、伺服器和行动装置收集遥测资料。云端安全子类别,尤其是云端原生应用程式保护平台(CNAPP),正经历最快的成长,这反映了传统工具无法应对的多重云端环境的复杂性。专业服务在合规性审核和事件回应方面保持着强大的市场地位,但人才短缺正在限制其服务能力并推高计费成本。

託管服务的成长主要受人才严重短缺和监管压力的驱动,迫使即使是资源雄厚的公司也寻求外部专业知识。资安管理服务供应商 (MSSP) 越来越多地以订阅形式提供安全营运中心 (SOC) 功能,降低了中型企业的准入门槛。工具疲劳也影响产品组合:90% 的大型企业运行功能重迭的漏洞扫描器,并正在整合到一个统一的平台上。供应商透过整合人工智慧分析和编配功能来应对这项挑战,从而增强解决方案的采用率并提高每位客户的平均收入。因此,解决方案保持了规模,而服务则推动了美国网路安全市场更高的成长率。

到2025年,本地部署环境将占总收入的57.20%,这主要受国防、金融服务和医疗保健产业维护资料主权和传统系统整合的迫切需求所驱动。联邦机构继续在空气间隙环境中维护机密网络,但分析层正越来越多地迁移到商业云。摩根大通等金融机构正在投资混合架构,将本地金钥管理与云端原生侦测功能结合,以确保合规性,同时又不牺牲灵活性。

受资本支出减少、弹性扩展和软体即服务 (SaaS) 部署速度加快的推动,云端交付安全解决方案以 14.4% 的复合年增长率 (CAGR) 实现成长。与基于设备的替代方案相比,采用 SECaaS 的企业实施週期缩短了 40%,从而加快了风险缓解速度。供应商整合威胁情报来源和行为分析,提供持续更新的控制平面,以适应不断演变的攻击者技术。随着时间的推移,这种成长差距扩大了收入差距,导致儘管高度监管行业的绝对支出趋于稳定,但本地部署方案在美国网路安全市场的份额仍然相对下降。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 联邦零信任指令加速各机构安全现代化进程

- 针对中型医疗和教育机构的勒索软体攻击激增

- 5G和边缘运算的采用扩大了关键基础设施的威胁面

- 快速向SaaS和多重云端转型推动了对云端原生安全平台的需求。

- 创业投资的涌入推动了基于人工智慧的威胁侦测Start-Ups的创新

- 网路保险保费上涨推动了对主动防御的投资

- 市场限制

- 各州之间分散的隐私法规使供应商的合规工作变得更加复杂。

- 严重的劳动力短缺导致人事费用上升和计划延期

- 采购部门因抵製多家供应商工具的激增而出现整合疲劳

- 中小企业面临预算压力,导致安保支出减少。

- 关键法规结构评估

- 价值链分析

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 关键相关人员影响评估

- 主要用例和案例研究

- 宏观经济因素对市场的影响

- 投资分析

第五章 市场规模与成长预测

- 报价

- 解决方案

- 应用程式安全

- 云端安全

- 资料安全

- 身分和存取管理

- 基础设施保护

- 综合风险管理

- 网路安全设备

- 端点安全

- 其他解决方案

- 服务

- 专业服务

- 託管服务

- 解决方案

- 透过部署模式

- 本地部署

- 云

- 按组织规模

- 小型企业

- 大公司

- 按最终用户行业划分

- BFSI

- 卫生保健

- 资讯科技和电信

- 工业与国防

- 零售

- 能源与公共产业

- 製造业

- 其他的

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Cisco Systems, Inc.

- Palo Alto Networks, Inc.

- Microsoft Corporation(Security BU)

- Fortinet, Inc.

- IBM Corporation

- CrowdStrike Holdings, Inc.

- Check Point Software Technologies Ltd.

- Zscaler, Inc.

- Okta, Inc.

- Trend Micro Incorporated

- Splunk Inc.

- Proofpoint, Inc.

- Cloudflare, Inc.

- Mandiant(A Google Cloud Company)

- Rapid7, Inc.

- SentinelOne, Inc.

- Sophos Ltd.

- Darktrace plc

- Akamai Technologies, Inc.

- Netskope, Inc.

- Arctic Wolf Networks, Inc.

第七章 市场机会与未来展望

The US cybersecurity market is expected to grow from USD 92.73 billion in 2025 to USD 99.79 billion in 2026 and is forecast to reach USD 144.07 billion by 2031 at 7.62% CAGR over 2026-2031.

This expansion is fueled by federal zero-trust mandates, a sharp increase in ransomware attacks on critical infrastructure, and accelerated cloud migration that now places 94% of organizations in multi-cloud settings . On-premise architectures still hold the largest deployment footprint because defense, financial services, and healthcare operators retain legacy systems that must remain behind local controls; however, cloud-delivered security is advancing at a 15% CAGR as enterprises seek scalable protection and real-time threat intelligence. Venture capital continues to stimulate innovation, with USD 11.6 billion invested in US cyber start-ups during 2024, much of it channeled into AI-driven threat-detection platforms that reduce analyst workload. Mandatory SEC breach-disclosure rules, rising cyber-insurance premiums, and a persistent talent shortage collectively reinforce long-term demand, positioning the US cybersecurity market as a strategic priority for both public and private sectors.

US Cybersecurity Market Trends and Insights

Federal Zero-Trust Mandates Accelerating Security Modernization Across Agencies

Executive Order 14028 obliges every civilian agency to adopt zero-trust architecture, triggering multi-year modernization projects that ripple through state and local governments. The Department of Homeland Security recently awarded USD 17 million to ASRC Federal for USCIS integration services, and the Treasury's new USD 20 billion PROTECTS vehicle underscores federal buying power. Twenty-three states have published their zero-trust roadmaps, with California allocating USD 50 million for identity-centric controls across all agencies by 2026. Contractors must follow suit, extending zero-trust requirements deep into defense and financial services supply chains. The cascade effect positions the US cybersecurity market as the primary beneficiary of sustained public-sector spending.

Surge in Ransomware Attacks Targeting Mid-Market Healthcare and Education Institutions

Change Healthcare's February 2024 breach halted prescription processing for 67,000 pharmacies and cost UnitedHealth Group USD 2.3 billion in remediation. Ascension Health faced a similar disruption three months later when a ransomware attack paralyzed electronic health-record systems across 140 hospitals. The Department of Health and Human Services confirmed that 100 million patient records were exposed last year, fueling federal pressure on hospitals to modernize defenses. Educational institutions are equally vulnerable; the FBI attributes multiple campus closures to ransomware that erased student-services databases. These events amplify spending urgency, pushing healthcare security outlays to an expected 14.6% CAGR, well above the overall US cybersecurity market trajectory.

Fragmented State-Level Privacy Regulations Creating Compliance Complexity for Vendors

CCPA in California, CDPA in Virginia, and CTDPA in Connecticut impose divergent breach-notification and consumer-rights requirements that force vendors to maintain state-specific compliance frameworks. The SEC's amended Regulation S-P now obliges financial institutions to notify individuals within 30 days of a data compromise, overlapping with stricter state deadlines. Mid-market security providers report average annual compliance costs of USD 2.3 million, eroding margins, and deterring market entry. Fragmentation slows product rollouts and complicates go-to-market planning, shaving an estimated 1.2 percentage points from the US cybersecurity market CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of 5G and Edge Computing Expanding the Threat Surface for Critical Infrastructure

- Rapid Migration to SaaS and Multi-Cloud Driving Demand for Cloud-Native Security Platforms

- Acute Talent Shortage Elevating Labour Costs and Project Timelines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions remain the primary revenue driver, holding 67.30% of the US cybersecurity market share in 2025, while managed services are forecast to grow at a 15.1% CAGR through 2031. Identity and access management adoption surged after federal zero-trust directives, and application security spending expanded alongside containerized development pipelines. Network security appliances face displacement from software-defined alternatives, whereas endpoint protection evolves toward XDR suites that ingest telemetry from laptops, servers and mobile devices. Cloud-security subcategories-particularly cloud-native application protection platforms (CNAPP)-post the fastest acceleration, reflecting multi-cloud complexity that legacy tools cannot address. Professional services hold a resilient niche in compliance audits and incident response, though the labor shortage constrains capacity and pushes billable rates higher.

Managed services growth stems from acute talent constraints and regulatory pressures that force even resource-rich enterprises to seek external expertise. MSSPs increasingly deliver security-operations-centre (SOC) functions via subscription, lowering entry thresholds for mid-market businesses. The offering mix is also shaped by tool-sprawl fatigue: 90% of large organizations run overlapping vulnerability scanners that they now seek to consolidate into integrated platforms. Vendors respond by embedding AI analytics and orchestration features, reinforcing solution stickiness and expanding average revenue per customer. Consequently, solutions retain scale, while services inject higher growth velocity into the overall US cybersecurity market.

On-premises setups accounted for 57.20% of revenue in 2025, largely because defence, financial-services and healthcare sectors must preserve data sovereignty and legacy integrations. Federal agencies continue to maintain classified networks behind air-gapped environments, although analytics layers increasingly migrate to commercial clouds. Financial institutions such as JPMorgan Chase invest in hybrid architecture that combines on-premises key-management with cloud-native detection, ensuring regulatory compliance without sacrificing agility.

Cloud-delivered security solutions expanded at a 14.4% CAGR, buoyed by reduced capital spending, elastic scaling and the speed of software-as-a-service rollouts. Organizations deploying SECaaS report implementation cycles 40% shorter than appliance-based alternatives, accelerating time to risk reduction. Providers integrate threat-intelligence feeds and behavioral analytics, delivering a continuously updated control plane that adapts to evolving attacker techniques. The growth differential widens the revenue gap over time, causing the on-premises slice of the US cybersecurity market to contract in relative terms, even as absolute spending remains stable in compliance-heavy industries.

The US Cybersecurity Market Report Segments the Industry Into Offering (Solutions, Services), by Deployment Mode (Cloud, and On-Premise), by Organization Size (SMEs, and Large Enterprises), by End User (BFSI, Healthcare, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Cisco Systems, Inc.

- Palo Alto Networks, Inc.

- Microsoft Corporation (Security BU)

- Fortinet, Inc.

- IBM Corporation

- CrowdStrike Holdings, Inc.

- Check Point Software Technologies Ltd.

- Zscaler, Inc.

- Okta, Inc.

- Trend Micro Incorporated

- Splunk Inc.

- Proofpoint, Inc.

- Cloudflare, Inc.

- Mandiant (A Google Cloud Company)

- Rapid7, Inc.

- SentinelOne, Inc.

- Sophos Ltd.

- Darktrace plc

- Akamai Technologies, Inc.

- Netskope, Inc.

- Arctic Wolf Networks, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Federal Zero-Trust Mandates Accelerating Security Modernization Across Agencies

- 4.2.2 Surge in Ransomware Attacks Targeting Mid-Market Healthcare and Education Institutions

- 4.2.3 Adoption of 5G and Edge Computing Expanding the Threat Surface for Critical Infrastructure

- 4.2.4 Rapid Migration to SaaS and Multi-Cloud Driving Demand for Cloud-Native Security Platforms

- 4.2.5 Venture-Capital Influx Spurring Innovation in AI-Based Threat Detection Start-ups

- 4.2.6 Escalating Cyber-Insurance Premiums Incentivizing Proactive Defense Investments

- 4.3 Market Restraints

- 4.3.1 Fragmented State-Level Privacy Regulations Creating Compliance Complexity for Vendors

- 4.3.2 Acute Talent Shortage Elevating Labor Costs and Project Timelines

- 4.3.3 Consolidation Fatigue as Buyers Resist Multi-Vendor Tool Sprawl

- 4.3.4 Budget Pressure on SMBs Curtailing Security Spend

- 4.4 Evaluation of Critical Regulatory Framework

- 4.5 Value Chain Analysis

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact Assessment of Key Stakeholders

- 4.9 Key Use Cases and Case Studies

- 4.10 Impact on Macroeconomic Factors of the Market

- 4.11 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Solutions

- 5.1.1.1 Application Security

- 5.1.1.2 Cloud Security

- 5.1.1.3 Data Security

- 5.1.1.4 Identity and Access Management

- 5.1.1.5 Infrastructure Protection

- 5.1.1.6 Integrated Risk Management

- 5.1.1.7 Network Security Equipment

- 5.1.1.8 Endpoint Security

- 5.1.1.9 Other Solutions

- 5.1.2 Services

- 5.1.2.1 Professional Services

- 5.1.2.2 Managed Services

- 5.1.1 Solutions

- 5.2 By Deployment Mode

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.3 By Organization Size

- 5.3.1 SMEs

- 5.3.2 Large Enterprises

- 5.4 By End-User Vertical

- 5.4.1 BFSI

- 5.4.2 Healthcare

- 5.4.3 IT and Telecom

- 5.4.4 Industrial and Defense

- 5.4.5 Retail

- 5.4.6 Energy and Utilities

- 5.4.7 Manufacturing

- 5.4.8 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Cisco Systems, Inc.

- 6.4.2 Palo Alto Networks, Inc.

- 6.4.3 Microsoft Corporation (Security BU)

- 6.4.4 Fortinet, Inc.

- 6.4.5 IBM Corporation

- 6.4.6 CrowdStrike Holdings, Inc.

- 6.4.7 Check Point Software Technologies Ltd.

- 6.4.8 Zscaler, Inc.

- 6.4.9 Okta, Inc.

- 6.4.10 Trend Micro Incorporated

- 6.4.11 Splunk Inc.

- 6.4.12 Proofpoint, Inc.

- 6.4.13 Cloudflare, Inc.

- 6.4.14 Mandiant (A Google Cloud Company)

- 6.4.15 Rapid7, Inc.

- 6.4.16 SentinelOne, Inc.

- 6.4.17 Sophos Ltd.

- 6.4.18 Darktrace plc

- 6.4.19 Akamai Technologies, Inc.

- 6.4.20 Netskope, Inc.

- 6.4.21 Arctic Wolf Networks, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

网路安全市场:按组件、安全类型、组织规模、部署模式和产业划分-2026-2032年全球市场预测

网路安全市场:按组件、安全类型、组织规模、部署模式和产业划分-2026-2032年全球市场预测 人工智慧网路安全市场预测至2034年—按交付方式、安全类型、部署方式、技术、应用、最终用户和地区分類的全球分析金融科技网路安全解决方案市场预测至2034年-按组件、安全类型、部署模式、组织规模、应用、最终用户和地区分類的全球分析

人工智慧网路安全市场预测至2034年—按交付方式、安全类型、部署方式、技术、应用、最终用户和地区分類的全球分析金融科技网路安全解决方案市场预测至2034年-按组件、安全类型、部署模式、组织规模、应用、最终用户和地区分類的全球分析 2026-2030年全球智慧体与自主人工智慧系统网路安全解决方案市场

2026-2030年全球智慧体与自主人工智慧系统网路安全解决方案市场 网路安全市场规模、份额、趋势和预测:按组件、部署类型、用户类型、行业和地区划分,2026-2034 年

网路安全市场规模、份额、趋势和预测:按组件、部署类型、用户类型、行业和地区划分,2026-2034 年 2026年全球建筑网路安全市场报告2026年全球电网网路安全市场报告2026年全球旅游安全市场报告

2026年全球建筑网路安全市场报告2026年全球电网网路安全市场报告2026年全球旅游安全市场报告 全球网路靶场市场报告:实际结果与预测(2021-2032)2026年全球Web3安全市场报告

全球网路靶场市场报告:实际结果与预测(2021-2032)2026年全球Web3安全市场报告