|

市场调查报告书

商品编码

1940839

美国化肥:市场占有率分析、产业趋势与统计、成长预测(2026-2031)United States Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

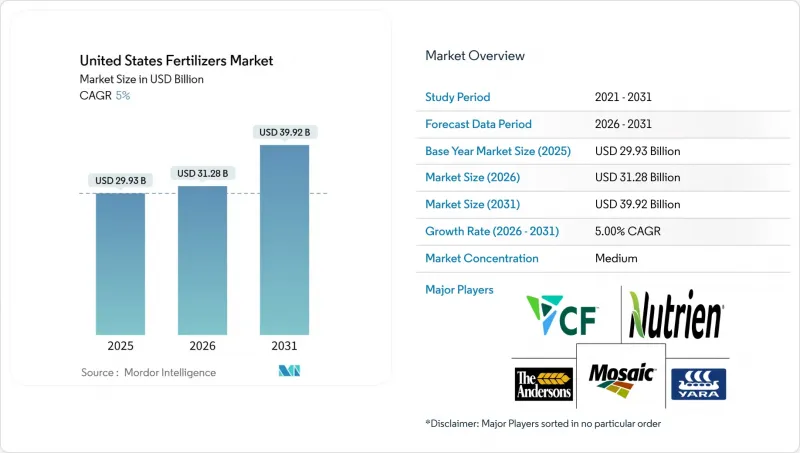

美国化肥市场预计将从 2025 年的 299.2 亿美元成长到 2026 年的 313 亿美元,到 2031 年达到 392.3 亿美元,2026 年至 2031 年的复合年增长率为 4.62%。

在监管压力日益增大的情况下,对作物营养的强劲需求、精密农业的日益普及以及鼓励使用高效肥料的政策奖励,共同支撑了收入增长。生产商正投资美国墨西哥湾沿岸沿岸的清洁氨产能,以对冲天然气价格波动风险并满足新的永续性标准。同时,密西西比河沿岸多式联运物流网络的加强降低了中西部农民的运输成本,并提高了市场应对原料价格波动的能力。日益激烈的竞争正促使前五大供应商进一步推动垂直整合,拓展数位化农业平台,并调整产品组合,转向特种肥料和控释肥料。

美国化肥市场趋势与洞察

精密农业的现状

目前,变数施肥系统已应用于70%的玉米和大豆种植面积,在确保产量的同时,可减少15%至20%的氮肥用量。在爱荷华州和伊利诺州,该系统的采用率超过85%,卫星影像、土壤感测器和产量测绘技术协同工作,提供切实可行的处方笺。 Nutrien公司每年投资2亿美元,开发将感测器数据与产品推荐结合的数位化农艺平台。此模式提高了养分利用效率,并将咨询服务与销售连结起来。随着越来越多的生产者实现成本节约和生产力提升,这项技术正将采购决策从“数量”转向“价值”,从而促进了控释产品的推广应用,使养分输送与作物需求相匹配。美国政府审核局(GAO)的一项模型估计,全产业推广应用该技术可在不牺牲产量的前提下,将全国化肥用量减少高达12%。因此,向数据驱动型管理的转变是美国化肥市场结构性成长的关键。

向高效肥料过渡

美国国税局2024-37号公告将永续航空燃料积分(每加仑1.75美元)与已证实的氮肥利用效率挂钩,显着提升了对缓释尿素、硝化抑制剂和脲酶抑制剂的需求。种植者正透过扩大产能来应对这项需求。 CF Industries已累计1.5亿美元用于维修其位于唐纳森维尔的工厂,使其能够生产缓释尿素;拜耳的碳排放项目已发放超过12.5万个与这些产品相关的积分,证明其能够直接减少农场温室气体排放。随着碳市场和税收政策的融合,需求正从小众园艺领域转向大型农业面积,推动了特种配方供应商基本客群的扩大和销售成长。

天然气价格波动

2024年,亨利港价格在每百万英热单位(MMBtu)2.10美元至6.80美元之间波动,波动幅度高达224%。由于原料成本占氨生产成本的80%之多,这种波动几乎直接影响氮肥生产成本。据CF工业公司称,价格每变动1美元,年度利润可能变动高达5,500万美元。 2024年第三季度,当现货天然气价格超过每百万英热单位6美元时,没有避险合约的小规模生产商减少了产量。这导致供应紧张,并抑制了对价格敏感的生产商的需求。伊利诺大学的一项分析发现,天然气价格持续高于每百万英热单位5美元时,由于农民寻求成本更低的替代方案,施用量减少了高达12%。因此,这种波动在短期内会抑制养分总消耗量。

细分市场分析

2025年,与精准可变施肥配方相容的单一肥料(可针对土壤特定养分缺乏进行精准施肥)占美国肥料市场收入的77.35%。受玉米和大豆种植面积强劲成长的推动,预计到2031年,美国单一肥料市场将以4.74%的复合年增长率成长。预计到2024年,玉米面积将达到9,410万英亩,并且由于持续依赖高氮肥用量,市场需求将保持稳定。然而,复合肥料由于其养分比例单一,往往无法满足田间具体处方笺,因此成长受到限制。随着网格土壤取样辨识出集约化作物轮作中限制产量的养分缺乏情况,锌和硼等微量元素的用量正以每年15-20%的速度成长。自 1990 年以来,工业硫沉降量急剧下降,导致许多土壤的硫含量低于其充足阈值,因此对次要营养物质(特别是硫)的需求正在恢復。

规模较大的农场出于田间经济效益的考虑,仍然倾向于使用单一营养元素肥料,以便零售商在销售点配製精确的配方。然而,小规模的农场和肥料供应有限的地区则出于便利性考虑,继续使用复合肥料。随着越来越多的州发现普遍存在的微量元素缺乏问题,预计美国肥料市场中微量元素添加剂的份额将会增加。在明尼苏达州和北达科他州,有针对性地施用铁肥使大豆产量每英亩提高了多达12蒲式耳,证明了投资回报。因此,种植者正在将微量元素混合包装成散装的氮磷钾复合肥,以获取新的高收益收入来源。单一营养元素产品仍将维持最大的市场份额,而补充营养元素产品将实现逐步成长。

由于成熟的供应链、低廉的单位成本以及与现有喷雾器的兼容性,预计到2025年,传统颗粒状和球状肥料将占总销售额的76.10%。然而,随着种植者越来越重视环境合规性和养分利用效率,特种配方肥料正以5.18%的复合年增长率快速成长。缓释肥料,例如聚合物包膜尿素,能够根据植物吸收时间稳定释放氮肥,促使玉米带地区的玉米种植系统采用率提高了25%。美国特种配方肥料市场主要由可与喷雾器系统整合以实现变数施肥的液体肥料所驱动。水溶性肥料在温室和水耕种植中越来越受欢迎,因为精准的养分输送可以减少废弃物并提高作物品质。

美国环保署(EPA)的工人保护标准鼓励使用能够减少粉尘和施肥人员暴露的产品,从而推动了对液体肥料和包衣颗粒的需求。 Nutrien公司报告称,其特种肥料部门在2024年实现了显着的收入成长,这主要得益于其用于精密农业的控释和液体肥料产品的强劲订单。随着特种肥料在监管更加严格的环境下,凭藉其多功能性,以及符合碳排放计划和税收优惠政策(这些政策要求肥料能够证明其养分利用效率的提升),预计这一增长势头将进一步加快。

美国化肥市场按类型(复合肥、单质肥)、形态(常规肥、特种肥)、施用方法(叶面喷布、土培)和作物类型(田间作物、园艺作物、草坪和观赏植物)进行细分。市场预测以价值(美元)和数量(公吨)为单位。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

- 调查方法

第二章 报告

第三章执行摘要主要发现

第四章 主要产业趋势

- 主要农作物种植面积

- 田间作物

- 园艺作物

- 平均养分施用率

- 微量营养素

- 田间作物

- 园艺作物

- 宏量营养素

- 田间作物

- 园艺作物

- 次要大量营养素

- 田间作物

- 园艺作物

- 微量营养素

- 法律规范

- 价值炼和通路分析

- 市场驱动因素

- 精密农业及技术整合的介绍

- 高效能肥料的研发与政策支持

- 农产品价格对农民购买力的影响

- 再生农业和排碳权

- 扩大墨西哥湾沿岸地区绿色氨的生产能力

- 密西西比州多式联运化肥走廊

- 市场限制

- 天然气价格波动对氮气成本的影响

- 加强对营养物质径流的监管

- 特种作物中的生物营养替代品

- 老化的氨气管道网路所带来的风险

第五章 市场规模及成长预测(数量与价值)

- 类型

- 复合肥

- 单一成分肥料

- 微量营养素

- 硼

- 铜

- 铁

- 锰

- 钼

- 锌

- 其他的

- 氮基

- 硝酸铵

- 无水氨

- 尿素

- 其他的

- 磷酸盐

- DAP

- MAP

- SSP

- TSP

- 钾肥

- MoP

- 硫酸钾

- 其他的

- 中等元素

- 钙

- 镁

- 硫

- 微量营养素

- 形式

- 传统的

- 特殊用途

- CRF

- 液体肥料

- SRF

- 水溶性

- 目的

- 土壤

- 叶面喷布

- 施肥和灌溉

- 作物类型

- 田间作物

- 园艺作物

- 草坪和观赏植物

第六章 竞争情势

- 关键策略倡议

- 市占率分析

- 公司简介

- 公司简介

- CF Industries Holdings, Inc.

- Nutrien Ltd.

- The Mosaic Company

- The Andersons Inc.

- Yara International ASA

- Haifa Group

- ICL Group Ltd

- Koch Industries Inc.

- Sociedad Quimica y Minera de Chile SA

- Wilbur-Ellis Company LLC(Wilbur-Ellis Holdings Inc.)

- Intrepid Potash Inc.

- Compass Minerals International Inc.

- JR Simplot Company

- Growmark Inc.

- CHS Inc.

第七章:CEO们需要思考的关键策略问题

The United States fertilizers market is expected to grow from USD 29.92 billion in 2025 to USD 31.3 billion in 2026 and is forecast to reach USD 39.23 billion by 2031 at 4.62% CAGR over 2026-2031.

Strong demand for crop nutrients, growing adoption of precision agriculture, and policy incentives that reward enhanced-efficiency fertilizer use are sustaining revenue growth even as regulatory pressures tighten. Producers are investing in clean-ammonia capacity on the Gulf Coast to hedge natural gas volatility and meet emerging sustainability criteria. Meanwhile, intermodal logistics upgrades along the Mississippi River corridor are lowering delivered costs for Midwestern growers and helping the market absorb feedstock price shocks. Competitive intensity is rising as the five largest suppliers pursue vertical integration, expand digital agriculture platforms, and reposition portfolios toward specialty and controlled-release formulations.

United States Fertilizers Market Trends and Insights

Precision Agriculture Uptake

Variable-rate systems now guide fertilizer placement on 70% of corn and soybean acres, trimming nitrogen use by 15-20% while safeguarding yields . Adoption exceeds 85% in Iowa and Illinois, where satellite imagery, soil sensors, and yield mapping converge to deliver actionable prescriptions. Nutrien invests USD 200 million annually in digital agronomy platforms that integrate sensor data with product recommendations, a model that links advisory services to sales while improving nutrient use efficiency. As more growers verify savings and productivity gains, the technology is shifting purchasing decisions from volume to value, encouraging uptake of controlled-release products that match nutrient delivery to crop demand. Government Accountability Office modeling suggests industry-wide implementation could trim nationwide fertilizer use by as much as 12% without sacrificing output. This pivot toward data-driven management is therefore a structural growth lever for the United States fertilizers market.

Enhanced-Efficiency Fertilizers Shift

IRS Notice 2024-37 links a USD 1.75 per gallon sustainable aviation fuel credit to proof of enhanced-efficiency nitrogen use, creating an outsize pull for controlled-release urea, nitrification inhibitors, and urease inhibitors. Producers are scaling capacity in response; CF Industries earmarked USD 150 million to retrofit its Donaldsonville complex for controlled-release urea, while Bayer's Carbon Program has issued more than 125,000 credits tied to such products, confirming direct greenhouse-gas reductions on the farm. As carbon markets converge with tax policy, demand is migrating from niche horticulture into core commodity acreage, widening the customer base and accelerating top-line growth for suppliers of specialty formulations.

Natural Gas Price Volatility

Henry Hub prices oscillated between USD 2.10 and USD 6.80 per MMBtu in 2024, driving a 224% range that translates almost directly into nitrogen production costs because feedstock accounts for up to 80% of ammonia expenditure. CF Industries notes that every USD 1.00 swing moves annual margins by as much as USD 55 million. Small producers without hedged contracts curtailed output during the third quarter of 2024 when spot gas breached USD 6.00, tightening supply while curbing demand among price-sensitive growers. University of Illinois analysis indicates that sustained gas over USD 5.00 reduces application rates by up to 12% as farmers seek lower-cost alternatives. The volatility, therefore, acts as a near-term drag on total nutrient consumption.

Other drivers and restraints analyzed in the detailed report include:

- High Corn and Soybean Commodity Prices

- Regenerative Farming Carbon-Credit Programs

- Tighter Nutrient-Runoff Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Straight fertilizers captured 77.35% of 2025 revenue in the United States fertilizers market because their single-nutrient formulations align neatly with precision variable-rate prescriptions that target soil-specific deficiencies. The United States fertilizers market size for straight formulations is projected to expand at a 4.74% CAGR through 2031 as corn and soybean acreage remains robust. Corn plantings reached 94.1 million acres in 2024 and continue to rely on high nitrogen rates, driving stable demand. For complex fertilizers, their blanket nutrient ratios often fail to align with site-specific prescriptions, thereby limiting growth. Micronutrients such as zinc and boron are increasing by 15-20% annually, as grid soil sampling identifies yield-limiting deficiencies in intensive rotations. Secondary nutrient demand, especially sulfur, is rebounding because industrial sulfur deposition has fallen sharply since 1990, pushing many soils below sufficiency thresholds.

Field-level economics still favor straight nutrients for large operations because retailers can blend to precise formulas at the point of sale. However, smaller farms and areas with limited custom application services continue to use complex grades for convenience. The United States fertilizers market share for micronutrient additives is likely to rise as more states document widespread deficiencies. Targeted iron applications in Minnesota and North Dakota lifted soybean yields by up to 12 bushels per acre, demonstrating the return on investment. Producers are therefore packaging micronutrients with bulk NPK blends to capture emerging high-margin revenue streams. Straight products will keep commanding the largest share, yet supplementary nutrients will provide incremental growth.

Conventional granular and prilled fertilizers delivered 76.10% of sales in 2025 owing to established supply chains, low per-unit cost, and compatibility with existing spreader equipment. Nevertheless, specialty formulations are expanding at a 5.18% CAGR as growers increasingly weigh environmental compliance and nutrient use efficiency. Controlled-release fertilizers such as polymer-coated urea allow steady nitrogen availability that synchronizes with crop uptake, leading to an adoption growth of 25% in Corn Belt corn systems. The United States fertilizers market size for specialty forms is bolstered by liquid solutions that integrate with sprayer fleets for variable-rate placement. Water-soluble formulations command high premiums in greenhouse and hydroponic operations where precise nutrient dosing curbs waste and boosts quality.

EPA Worker Protection Standards favor products that limit dust and applicator exposure, nudging demand toward liquids and coated granules. Nutrien reported significant revenue growth in its specialty division in 2024, citing strong orders for controlled-release and liquid products used in precision agriculture. The growth trajectory is expected to accelerate because specialty blends qualify for carbon programs and tax rebates that require demonstrated increases in nutrient efficiency, positioning them as multipurpose solutions in a tightening regulatory environment.

The United States Fertilizers Market is Segmented by Type (Complex, Straight), Form (Conventional, Specialty), Application Mode (Fertigation, Foliar, Soil), and Crop Type (Field Crops, Horticultural Crops, Turf & Ornamental). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

List of Companies Covered in this Report:

- CF Industries Holdings, Inc.

- Nutrien Ltd.

- The Mosaic Company

- The Andersons Inc.

- Yara International ASA

- Haifa Group

- ICL Group Ltd

- Koch Industries Inc.

- Sociedad Quimica y Minera de Chile SA

- Wilbur-Ellis Company LLC (Wilbur-Ellis Holdings Inc.)

- Intrepid Potash Inc.

- Compass Minerals International Inc.

- J.R. Simplot Company

- Growmark Inc.

- CHS Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY & KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.2 Primary Nutrients

- 4.2.2.1 Field Crops

- 4.2.2.2 Horticultural Crops

- 4.2.3 Secondary Macronutrients

- 4.2.3.1 Field Crops

- 4.2.3.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Precision agriculture adoption and technology integration

- 4.5.2 Enhanced-efficiency fertilizer development and policy support

- 4.5.3 Commodity price impacts on farmer purchasing power

- 4.5.4 Regenerative farming and carbon-credit programs

- 4.5.5 Gulf Coast green-ammonia capacity build-out

- 4.5.6 Mississippi intermodal fertilizer corridors

- 4.6 Market Restraints

- 4.6.1 Natural gas price volatility effects on nitrogen costs

- 4.6.2 Tighter nutrient-runoff regulations

- 4.6.3 Biologic nutrition substitutes in specialty crops

- 4.6.4 Aging ammonia pipeline network risks

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Type

- 5.1.1 Complex

- 5.1.2 Straight

- 5.1.2.1 Micronutrients

- 5.1.2.1.1 Boron

- 5.1.2.1.2 Copper

- 5.1.2.1.3 Iron

- 5.1.2.1.4 Manganese

- 5.1.2.1.5 Molybdenum

- 5.1.2.1.6 Zinc

- 5.1.2.1.7 Others

- 5.1.2.2 Nitrogenous

- 5.1.2.2.1 Ammonium Nitrate

- 5.1.2.2.2 Anhydrous Ammonia

- 5.1.2.2.3 Urea

- 5.1.2.2.4 Others

- 5.1.2.3 Phosphatic

- 5.1.2.3.1 DAP

- 5.1.2.3.2 MAP

- 5.1.2.3.3 SSP

- 5.1.2.3.4 TSP

- 5.1.2.4 Potassic

- 5.1.2.4.1 MoP

- 5.1.2.4.2 SoP

- 5.1.2.4.3 Others

- 5.1.2.5 Secondary Macronutrients

- 5.1.2.5.1 Calcium

- 5.1.2.5.2 Magnesium

- 5.1.2.5.3 Sulfur

- 5.1.2.1 Micronutrients

- 5.2 Form

- 5.2.1 Conventional

- 5.2.2 Speciality

- 5.2.2.1 CRF

- 5.2.2.2 Liquid Fertilizer

- 5.2.2.3 SRF

- 5.2.2.4 Water Soluble

- 5.3 Application

- 5.3.1 Soil

- 5.3.2 Foliar

- 5.3.3 Fertigation

- 5.4 Crop Type

- 5.4.1 Field Crops

- 5.4.2 Horticultural Crops

- 5.4.3 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 CF Industries Holdings, Inc.

- 6.4.2 Nutrien Ltd.

- 6.4.3 The Mosaic Company

- 6.4.4 The Andersons Inc.

- 6.4.5 Yara International ASA

- 6.4.6 Haifa Group

- 6.4.7 ICL Group Ltd

- 6.4.8 Koch Industries Inc.

- 6.4.9 Sociedad Quimica y Minera de Chile SA

- 6.4.10 Wilbur-Ellis Company LLC (Wilbur-Ellis Holdings Inc.)

- 6.4.11 Intrepid Potash Inc.

- 6.4.12 Compass Minerals International Inc.

- 6.4.13 J.R. Simplot Company

- 6.4.14 Growmark Inc.

- 6.4.15 CHS Inc.

7 KEY STRATEGIC QUESTIONS FOR FERTILIZERS CEOS

缓释肥料市场:2026-2032年全球市场预测(以包膜类型、作物类型、释放週期、养分类型、施用方法、最终用途和销售管道)

缓释肥料市场:2026-2032年全球市场预测(以包膜类型、作物类型、释放週期、养分类型、施用方法、最终用途和销售管道) 2026年全球生物炭肥料市场报告几丁质肥料市场:2026-2032年全球市场预测(按应用、类型、原料、配方和分销管道划分)肥料包膜市场:2026-2032年全球市场预测(以包膜化学、释放机制、包膜养分类型、外形规格、製造流程、最终用途及通路划分)化肥市场:2026-2032年全球市场预测(依产品类型、作物类型、包装、施用方法、最终用户和分销管道划分)复合肥料市场:按产品类型、作物类型、物理形态和应用分類的全球市场预测,2026-2032年

2026年全球生物炭肥料市场报告几丁质肥料市场:2026-2032年全球市场预测(按应用、类型、原料、配方和分销管道划分)肥料包膜市场:2026-2032年全球市场预测(以包膜化学、释放机制、包膜养分类型、外形规格、製造流程、最终用途及通路划分)化肥市场:2026-2032年全球市场预测(依产品类型、作物类型、包装、施用方法、最终用户和分销管道划分)复合肥料市场:按产品类型、作物类型、物理形态和应用分類的全球市场预测,2026-2032年 海藻土壤改良剂市场预测至 2034 年—按产品类型、海藻种类、形态、应用、养殖方法、通路和地区进行全球分析。藻类肥料市场:2026-2032年全球市场预测(依原料、产品类型、通路及应用划分)

海藻土壤改良剂市场预测至 2034 年—按产品类型、海藻种类、形态、应用、养殖方法、通路和地区进行全球分析。藻类肥料市场:2026-2032年全球市场预测(依原料、产品类型、通路及应用划分) 全球缓释肥料市场规模、份额、趋势和成长分析报告(2026-2034)全球肥料造粒助剂市场规模、份额、趋势和成长分析报告(2026-2034年)

全球缓释肥料市场规模、份额、趋势和成长分析报告(2026-2034)全球肥料造粒助剂市场规模、份额、趋势和成长分析报告(2026-2034年)