|

市场调查报告书

商品编码

1940841

越南化肥:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Vietnam Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

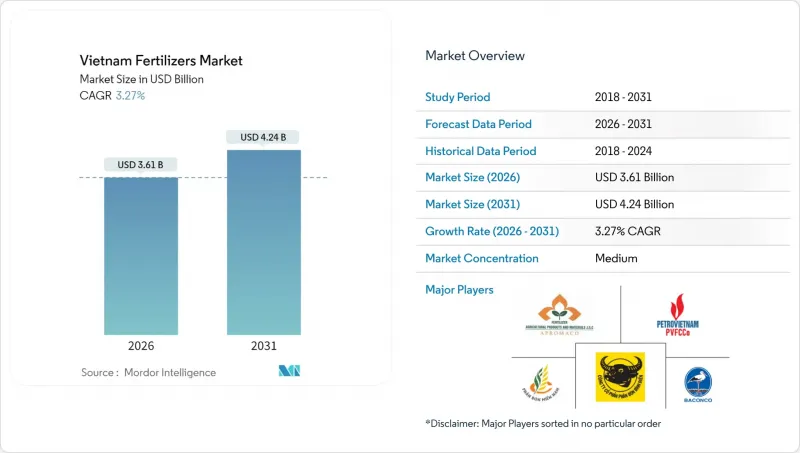

预计到 2026 年,越南化肥市场规模将达到 36.1 亿美元,高于 2025 年的 35 亿美元。

预计到 2031 年将达到 42.4 亿美元,2026 年至 2031 年的复合年增长率为 3.27%。

越南受益于国内尿素盈余、强有力的政府现代化计划以及对柬埔寨、韩国和菲律宾不断扩大的出口。物流成本上升以及因引入5%的新增值税而导致的成本结构变化带来了竞争压力,但税额扣抵抵免最终有利于国内生产商。对精准施肥系统和高价值出口作物专用肥料的需求推动了技术投资,而仿冒品进口产品以及对钾盐和磷酸二铵的依赖继续挤压利润空间。同时,主要企业积极扩张产能以及与全球经销商建立合作关係,正在巩固越南作为区域化肥中心的地位。

越南化肥市场趋势与分析

国内尿素过剩推动出口扩张

越南每年尿素盈余约120万吨,预计2024年出口量将达173万吨(价值7.0991亿美元),较2023年成长11.7%。柬埔寨占越南尿素出口总量的34.3%,韩国占12.7%,菲律宾占6.3%。富美和金瓯一体化天然气联合装置确保了原料价格的竞争力,从而带来成本优势。扩大出口分散了运输风险,提高了工厂运转率,即使国内需求放缓,也能支撑国内收入。

5%的增值税免税降低了国内生产成本

越南化肥市场实施5%的增值税(VAT)免税政策,将降低国内生产商的生产成本,并增强其相对于进口产品的竞争力。自2025年7月1日起,消费税免税政策将过渡到5%的课税制度,届时生产商可就天然气和设备申请税额扣抵。与全额课税的进口化肥相比,这项税制改革将降低净生产成本。虽然此举会增加营运资金需求,但也会提高国内企业的利润率,尤其是在磷酸二铵(DAP)和钾肥进口价格上涨的旺季。

向偏远地区运送液态肥料和控释肥料(CRF)的物流成本很高

在越南,向偏远地区运输液态和缓释肥料(CRF)的高昂物流成本限制了市场成长。这些成本推高了最终价格,降低了肥料的普及率,并阻碍了市场渗透。基础设施的限制、供应链效率低下以及对国际航运的依赖,使得越南的物流成本在农业企业收入中占据了相当大的比例。运输成本占越南肥料物流成本的60%,远高于30%的全球平均。疫情前,海运成本为每个货柜3000美元,到2024年预计将上涨至14,000美元。此外,通往西北部山区的公路交通仍然有限。液态和缓释肥料的温控运输要求进一步增加了运输成本,限制了Delta地区以外地区对特殊肥料的采用。

细分市场分析

2025年,单一成分肥料占越南肥料市场份额的76.65%,预计到2031年将以3.42%的复合年增长率快速增长,主要受水稻、玉米和甘蔗种植中对成本敏感的小规模的需求推动。在这一类别中,尿素受益于国内生产的经济效益,而磷酸二铵(DAP)和磷酸一铵(MAP)仍依赖进口,导致价格波动。复合肥料虽然市占率较小,但由于人工林主对添加硫和微量元素的均衡氮磷钾(NPK)肥料的需求,其成长速度更快。

尿素的供应支持传统的撒施方式,但氮素挥发造成的损失促使人们关注抑制剂和包膜技术。复合肥配方在以出口产量为目标的咖啡和水果种植者中越来越受欢迎。虽然微量元素配方尚处于发展初期,但它们正在解决红壤中常见的锌和硼缺乏问题,并有助于提高水果品质。预计到2030年,政府持续进行营养管理的教育将推动市场对均衡配方的需求成长。

截至2025年,传统颗粒肥料占越南肥料市场94.85%的份额,反映出越南完善的分销网络和对施肥设备的熟悉程度。受灌溉施肥和温室种植面积扩大的推动,特种肥料预计到2031年将以3.58%的复合年增长率成长。水溶性晶体和液体悬浮液在滴灌热带果园中吸收迅速,与颗粒肥料相比,养分利用率更高。

儘管缓效肥料价格较高,且运往偏远地区需要高昂的运输成本,但大型咖啡农场愿意支付更高的成本以降低人事费用。微生物接种剂和富含腐植酸的液体肥料能够解决土壤健康问题,并符合有机认证标准。数位化平台的扩展使特种肥料生产商能够有效率地满足小众市场需求,从而鼓励大型生产商实现产品系列多元化。

越南化肥市场按类型(复合肥和单质肥)、形态(常规型和特种型)、施用方法(灌溉施肥、叶面喷布、土壤施用)和作物类型(田间作物、园艺作物等)进行细分。市场预测以价值(美元)和数量(公吨)为单位。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

- 调查方法

第二章 报告

第三章执行摘要主要发现

第四章 主要产业趋势

- 主要农作物种植面积

- 田间作物

- 园艺作物

- 平均施肥量

- 微量营养素

- 田间作物

- 园艺作物

- 宏量营养素

- 田间作物

- 园艺作物

- 次发性大量营养素

- 田间作物

- 园艺作物

- 微量营养素

- 具有灌溉设施的农田

- 法律规范

- 价值炼和通路分析

- 市场驱动因素

- 国内尿素产能过剩推动出口扩张

- 增值税豁免将降低当地生产成本。

- 转向高价值出口作物的特殊等级

- 在湄公河和红河Delta地区引进精准施肥灌溉

- 政府有机肥目标(到2050年占种植面积的50%)

- 向小规模农户推广电子商务分销平台

- 市场限制

- 将液态肥料和控释肥运往偏远地区的物流成本很高

- 仿冒品伪劣进口商品损害了农民的信任。

- 对钾肥和磷酸二铵进口的依赖使该国容易受到价格波动的影响。

- 季节性库存过剩会对生产商的利润率带来压力。

第五章 市场规模及成长预测(数量与价值)

- 类型

- 复合肥

- 单一肥料

- 微量营养素

- 硼

- 铜

- 铁

- 锰

- 钼

- 锌

- 其他的

- 氮基

- 尿素

- 其他的

- 磷酸盐

- DAP

- MAP

- TSP

- 其他的

- 钾肥

- MoP

- SoP

- 其他的

- 次发性大量营养素

- 钙

- 镁

- 硫

- 微量营养素

- 形式

- 传统的

- 特殊肥料

- CRF

- 液体肥料

- SRF

- 水溶性

- 应用方法

- 施肥和灌溉

- 叶面喷布

- 土壤

- 作物类型

- 田间作物

- 园艺作物

- 草坪和观赏植物

第六章 竞争情势

- 关键策略倡议

- 市占率分析

- 公司概况

- 公司简介

- PetroVietnam Fertilizer and Chemical Corporation

- PetroVietnam Ca Mau Fertilizer Joint Stock Company

- Baconco Company Limited

- Binh Dien Fertilizer Joint Stock Company

- Duc Giang Chemical Group Joint Stock Company

- Southern Fertilizer Joint Stock Company

- Ninh Binh Phosphate Fertilizer Joint Stock Company

- Agricultural Products and Materials Joint Stock Company

- Haifa Chemicals Ltd.

- Yara International ASA

- Grupa Azoty SA

- Lam Thao Fertilizers and Chemicals Joint Stock Company

- Song Gianh Corporation

- Que Lam Group Joint Stock Company

- Israel Chemicals Ltd.

- Nutrien Ltd.

第七章:CEO们需要思考的关键策略问题

Vietnam fertilizers market size in 2026 is estimated at USD 3.61 billion, growing from 2025 value of USD 3.5 billion with 2031 projections showing USD 4.24 billion, growing at 3.27% CAGR over 2026-2031.

Vietnam benefits from surplus domestic urea, strong government modernization programs, and growing exports to Cambodia, South Korea, and the Philippines. Competitive pressure comes from logistics inflation and a new 5% VAT that changes cost dynamics, yet the tax credit mechanism ultimately favors local producers. Precision-fertigation systems and specialty fertilizer demand for high-value export crops are driving technology investment, while counterfeit imports and dependence on potash and DAP continue to weigh on margins. Meanwhile, aggressive capacity additions by domestic leaders and alliances with global distributors strengthen Vietnam's role as a regional fertilizer hub.

Vietnam Fertilizers Market Trends and Insights

Surplus Domestic Urea Driving Export Push

Vietnam produces a urea surplus of about 1.2 million metric tons annually, enabling 2024 exports of 1.73 million metric tons valued at USD 709.91 million, a 11.7% volume jump over 2023. Cambodia absorbed 34.3% of shipments, followed by South Korea at 12.7% and the Philippines at 6.3%. Cost advantages stem from integrated gas-based complexes in Phu My and Ca Mau that secure competitive feedstock pricing. The export momentum spreads freight risk and lifts plant utilization, thus buoying domestic earnings even when local demand moderates.

Pending 5% VAT Credit Lowers Local Production Cost

The implementation of 5% VAT credits in Vietnam's fertilizer market reduces production costs for domestic manufacturers, enhancing their competitiveness against imports. The transition from VAT exemption to a 5% VAT regime, effective July 1, 2025, enables producers to reclaim input VAT on natural gas and equipment. This tax adjustment decreases net production costs compared to imported fertilizers subject to full taxation. While the measure increases working capital requirements, it strengthens profit margins for domestic companies, particularly during peak seasons when diammonium phosphate (DAP) and potash import prices increase.

High Logistics Cost for Liquids and CRF to Remote Provinces

The high logistics costs associated with transporting liquid fertilizers and Controlled-Release Fertilizers (CRFs) to Vietnam's remote provinces constrain market growth. These costs increase final prices, reduce adoption rates, and restrict market penetration. Vietnam's logistics expenses constitute a significant portion of agricultural business revenue due to infrastructure limitations, supply chain inefficiencies, and dependence on international shipping. Transportation represents 60% of fertilizer logistics costs in Vietnam, compared to the global average of 30%. Ocean freight costs increased from USD 3,000 per container before the pandemic to USD 14,000 in 2024 . Additionally, road accessibility to the mountainous Northwest region remains restricted. The temperature-controlled shipping requirements for liquid and controlled-release fertilizers further increase delivery costs, limiting specialty fertilizer adoption beyond the delta regions.

Other drivers and restraints analyzed in the detailed report include:

- Precision-Fertigation Adoption in Mekong and Red River Deltas

- Government Organic Fertilizer Targets

- Potash and DAP Import Dependence - Exposed to Price Shocks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Straight fertilizers captured 76.65% of the Vietnam fertilizers market share in 2025 and show the fastest growth of CAGR 3.42% by 2031, driven by cost-sensitive smallholder practices in rice, corn, and sugarcane production. Within this group, urea benefits from strong domestic production economics, whereas DAP and MAP remain import-dependent, adding price volatility. Complex fertilizers account for a smaller slice yet expand faster as plantation operators seek balanced NPK blends with sulfur and micronutrients.

Urea's accessibility underpins traditional broadcast application, but nitrogen losses through volatilization spur interest in inhibitors and coating technologies. Complex blends find traction with coffee and fruit growers targeting export-grade yields. Micronutrient formulations, though nascent, address zinc and boron deficiencies common in lateritic soils, lifting fruit quality premiums. Continued government education on nutrient stewardship is anticipated to shift volumes toward balanced formulas by decade-end.

Conventional granules dominated 94.85% of the Vietnamese fertilizers market in 2025, reflecting entrenched distribution networks and familiarity with broadcasting tools. Specialty forms posted a 3.58% CAGR through 2031 due to fertigation and greenhouse growth. Water-soluble crystals and liquid suspensions generate rapid uptake in drip-irrigated tropical fruit orchards, improving nutrient efficiency relative to granular top-dressing.

Controlled-release fertilizers command premium pricing and face steep freight costs to remote provinces, but large coffee estates accept higher outlays to cut labor costs. Microbial inoculants and humic-enriched liquids address soil health concerns and meet organic certification criteria. As digital platforms expand, specialty suppliers can serve niche demand efficiently, encouraging portfolio diversification among major producers.

The Vietnam Fertilizers Market is Segmented by Type (Complex and Straight), Form (Conventional and Specialty), Application Mode (Fertigation, Foliar, and Soil), and Crop Type (Field Crops, Horticultural Crops, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

List of Companies Covered in this Report:

- PetroVietnam Fertilizer and Chemical Corporation

- PetroVietnam Ca Mau Fertilizer Joint Stock Company

- Baconco Company Limited

- Binh Dien Fertilizer Joint Stock Company

- Duc Giang Chemical Group Joint Stock Company

- Southern Fertilizer Joint Stock Company

- Ninh Binh Phosphate Fertilizer Joint Stock Company

- Agricultural Products and Materials Joint Stock Company

- Haifa Chemicals Ltd.

- Yara International ASA

- Grupa Azoty S.A.

- Lam Thao Fertilizers and Chemicals Joint Stock Company

- Song Gianh Corporation

- Que Lam Group Joint Stock Company

- Israel Chemicals Ltd.

- Nutrien Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY & KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.2 Primary Nutrients

- 4.2.2.1 Field Crops

- 4.2.2.2 Horticultural Crops

- 4.2.3 Secondary Macronutrients

- 4.2.3.1 Field Crops

- 4.2.3.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Surplus domestic urea driving export push

- 4.6.2 Pending 5 % VAT credit lowers local production cost

- 4.6.3 Shift to specialty grades for high-value export crops

- 4.6.4 Precision-fertigation adoption in Mekong & Red River deltas

- 4.6.5 Government organic-fertilizer targets (50 % area by 2050)

- 4.6.6 E-commerce distribution platforms reaching smallholders

- 4.7 Market Restraints

- 4.7.1 High logistics cost for liquids & CRF to remote provinces

- 4.7.2 Counterfeit & sub-standard imports eroding farmer trust

- 4.7.3 Potash & DAP import dependence exposed to price shocks

- 4.7.4 Seasonal inventory glut depressing producer margins

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Type

- 5.1.1 Complex

- 5.1.2 Straight

- 5.1.2.1 Micronutrients

- 5.1.2.1.1 Boron

- 5.1.2.1.2 Copper

- 5.1.2.1.3 Iron

- 5.1.2.1.4 Manganese

- 5.1.2.1.5 Molybdenum

- 5.1.2.1.6 Zinc

- 5.1.2.1.7 Others

- 5.1.2.2 Nitrogenous

- 5.1.2.2.1 Urea

- 5.1.2.2.2 Others

- 5.1.2.3 Phosphatic

- 5.1.2.3.1 DAP

- 5.1.2.3.2 MAP

- 5.1.2.3.3 TSP

- 5.1.2.3.4 Others

- 5.1.2.4 Potassic

- 5.1.2.4.1 MoP

- 5.1.2.4.2 SoP

- 5.1.2.4.3 Others

- 5.1.2.5 Secondary Macronutrients

- 5.1.2.5.1 Calcium

- 5.1.2.5.2 Magnesium

- 5.1.2.5.3 Sulfur

- 5.1.2.1 Micronutrients

- 5.2 Form

- 5.2.1 Conventional

- 5.2.2 Speciality

- 5.2.2.1 CRF

- 5.2.2.2 Liquid Fertilizer

- 5.2.2.3 SRF

- 5.2.2.4 Water Soluble

- 5.3 Application Mode

- 5.3.1 Fertigation

- 5.3.2 Foliar

- 5.3.3 Soil

- 5.4 Crop Type

- 5.4.1 Field Crops

- 5.4.2 Horticultural Crops

- 5.4.3 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments)

- 6.4.1 PetroVietnam Fertilizer and Chemical Corporation

- 6.4.2 PetroVietnam Ca Mau Fertilizer Joint Stock Company

- 6.4.3 Baconco Company Limited

- 6.4.4 Binh Dien Fertilizer Joint Stock Company

- 6.4.5 Duc Giang Chemical Group Joint Stock Company

- 6.4.6 Southern Fertilizer Joint Stock Company

- 6.4.7 Ninh Binh Phosphate Fertilizer Joint Stock Company

- 6.4.8 Agricultural Products and Materials Joint Stock Company

- 6.4.9 Haifa Chemicals Ltd.

- 6.4.10 Yara International ASA

- 6.4.11 Grupa Azoty S.A.

- 6.4.12 Lam Thao Fertilizers and Chemicals Joint Stock Company

- 6.4.13 Song Gianh Corporation

- 6.4.14 Que Lam Group Joint Stock Company

- 6.4.15 Israel Chemicals Ltd.

- 6.4.16 Nutrien Ltd.

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

缓释肥料市场:2026-2032年全球市场预测(以包膜类型、作物类型、释放週期、养分类型、施用方法、最终用途和销售管道)

缓释肥料市场:2026-2032年全球市场预测(以包膜类型、作物类型、释放週期、养分类型、施用方法、最终用途和销售管道) 2026年全球生物炭肥料市场报告几丁质肥料市场:2026-2032年全球市场预测(按应用、类型、原料、配方和分销管道划分)肥料包膜市场:2026-2032年全球市场预测(以包膜化学、释放机制、包膜养分类型、外形规格、製造流程、最终用途及通路划分)化肥市场:2026-2032年全球市场预测(依产品类型、作物类型、包装、施用方法、最终用户和分销管道划分)复合肥料市场:按产品类型、作物类型、物理形态和应用分類的全球市场预测,2026-2032年

2026年全球生物炭肥料市场报告几丁质肥料市场:2026-2032年全球市场预测(按应用、类型、原料、配方和分销管道划分)肥料包膜市场:2026-2032年全球市场预测(以包膜化学、释放机制、包膜养分类型、外形规格、製造流程、最终用途及通路划分)化肥市场:2026-2032年全球市场预测(依产品类型、作物类型、包装、施用方法、最终用户和分销管道划分)复合肥料市场:按产品类型、作物类型、物理形态和应用分類的全球市场预测,2026-2032年 海藻土壤改良剂市场预测至 2034 年—按产品类型、海藻种类、形态、应用、养殖方法、通路和地区进行全球分析。藻类肥料市场:2026-2032年全球市场预测(依原料、产品类型、通路及应用划分)

海藻土壤改良剂市场预测至 2034 年—按产品类型、海藻种类、形态、应用、养殖方法、通路和地区进行全球分析。藻类肥料市场:2026-2032年全球市场预测(依原料、产品类型、通路及应用划分) 全球缓释肥料市场规模、份额、趋势和成长分析报告(2026-2034)全球肥料造粒助剂市场规模、份额、趋势和成长分析报告(2026-2034年)

全球缓释肥料市场规模、份额、趋势和成长分析报告(2026-2034)全球肥料造粒助剂市场规模、份额、趋势和成长分析报告(2026-2034年)