|

市场调查报告书

商品编码

1940857

步进马达:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Stepper Motor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

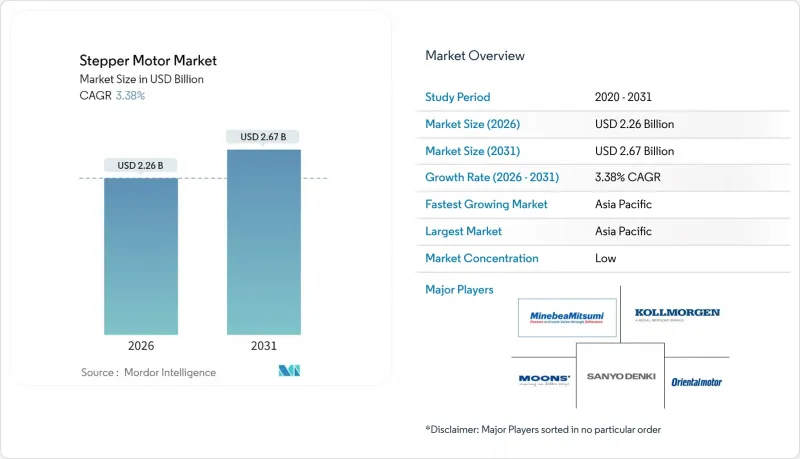

步进马达市场预计将从 2025 年的 21.9 亿美元成长到 2026 年的 22.6 亿美元,预计到 2031 年将达到 26.7 亿美元,2026 年至 2031 年的复合年增长率为 3.38%。

由于机器人、医疗设备和半导体製造设备製造商持续选择步进马达技术来实现精确的开放回路定位,从而避免使用高成本的伺服平台,因此市场需求保持稳定。协作机器人越来越多地应用于组装单元,加速了紧凑型、符合NEMA标准的机器人的普及,这些机器人能够提供可预测的扭矩和简化的编程。半导体产业的资本投资,尤其是在封装和微影术线方面的投资,支撑了对可在无尘室环境中可靠运作的混合型和线性产品的订单。对低维护、高重复性致动器的需求也推动了实验室自动化、桌上型3D列印机和电池生产线的成长。儘管库存调整导致2024年整体运动控制市场出现萎缩,但2025年工厂自动化投资的恢復预示着市场将回归稳定的采购週期。

全球步进马达市场趋势与洞察

机器人和协作机器人的日益普及

製造工厂在部署协作机器人时,倾向于选择步进马达驱动,因为其可预测的步进增量提供了固有的扭矩限制,从而提高了人机安全性。美国的製造业回流计画和欧洲的生产力提升计画正在推动模组化运动平台的标准化,这些平台支援低压两相混合马达和微步控制器。配备编码器的封闭回路型模型可提供类似伺服的平滑度,从而扩展取放系统的工作范围。以乙太网路为基础的通讯协定将马达整合到工厂网路中,实现状态监测并最大限度地减少非计划性停机时间。随着小批量生产在契约製造占据主导地位,易于切换和快速编程的特性使步进马达解决方案成为系统整合商的理想选择。

医疗设备对精密运动控制的需求日益增长

手术机器人、血液分析仪和输液帮浦需要在紧凑的面积内实现亚微米级的精确度。现代混合式步进马达与高解析度编码器相结合,能够满足这项要求。设计人员会选择具有可重复保持扭矩的电机,即使断电也能保持仪器位置—这是保障患者安全的关键措施。透过阻尼演算法将共振频率移出人耳可听频宽,从而实现静音运行,符合医院噪音标准。 FDA 和 CE 法规强调可追溯性,并优先选择拥有 ISO 13485 认证和检验的设计历史文件的供应商。医疗产业较长的更换週期意味着零件供应商能够获得可预测的收入。

与伺服/无刷直流马达的性能比较

儘管步进马达组的性能有所提升,但其扭矩在转速超过 1000 RPM 后会急剧下降,这限制了它们在高速拾取放置和输送机驱动中的应用。入门级伺服的价格下降缩小了以往步进马达在中等精度任务的优势成本。整合伺服系统现在标配自动调谐和现场汇流排选项,简化了部署,并缩小了总安装成本的差距。因此,负责人正在重点宣传那些静态位置保持扭矩比动态要求更重要的应用场景,例如阀门驱动和微孔盘分度。

细分市场分析

混合式步进马达兼具高扭力密度和1.8度步进分辨率,预计到2025年将占据步进马达市场54.65%的份额。其复合年增长率预计将达到3.95%,超过永磁马达和可变磁阻马达。这项优势正推动着精密磁路研发的持续投入,以在不增加机架尺寸的情况下提高磁通密度。目前,供应商正采用高填充率绕组来降低I²R损耗,实现低电流运行,从而减少发热并延长轴承寿命。

混合技术的改进也有助于提高能源效率,以满足IEC 60034-30-1等级标准的要求。钕铁硼磁体坯料采用雷射加工,最大限度地减少组装后的变形,并提高微步线性度,这对于光学元件测试平台至关重要。永久磁铁马达在对成本敏感的自动贩卖机中仍然很受欢迎,而可变磁阻马达则在极端温度下的泵浦应用中保持着一定的市场份额,因为在这些应用中,磁铁劣化是一个需要考虑的问题。总体而言,步进马达市场正受益于以混合技术改进为中心的技术蓝图,该路线图在不牺牲成本优势的前提下,缩小了与更便宜的伺服之间的性能差距。

区域分析

亚太地区将继续保持其在营收方面的领先地位,预计到2025年将占据35.74%的市场份额。这主要得益于中国完善的零件生态系统,该系统能够简化磁铁、轴和驱动器的采购流程。像MOONS' Electric这样的区域领导企业利用规模经济优势,年产量超过百万台,并透过极具竞争力的价格支持全球出口通路。日本凭藉其大规模生产能力和技术实力,包括专利封闭回路型韧体和高真空设计,引领该地区的半导体设备出口。韩国和东南亚已发展成为契约製造中心,透过将进口的混合产品整合到印表机和机器人的成品子组件中,加强了区域价值链。

北美预计将以3.76%的复合年增长率成长,这得益于联邦政府对自动化升级的支持以及美国本土半导体製造厂的位置。美国系统整合商在建造新的电动车电池工厂时,越来越多地选择符合NEMA标准的标准化机架,而非定制伺服,以缩短前置作业时间。加拿大生命科学和食品包装企业对耐冲洗的IP65防护等级组件的需求不断增长,而墨西哥的汽车线束生产线则需要成本优化的开放回路步进马达来支援。

受节能指令(例如2019/1781号法规)的推动,欧洲市场正稳步成长,该法规旨在促进工厂的封闭回路型改造。德国原始设备製造商(OEM)正利用其本地精密加工技术,为全球晶圆加工设备市场提供高真空规格的产品。同时,中东和非洲的新兴经济体也开始在海水淡化、纺织和包装计划采用步进马达驱动器,儘管其应用量仍远低于成熟地区。整体而言,地域多元化保护了步进马达市场免受局部衰退的影响,从而支撑起一个具有韧性的多区域需求基础。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 机器人技术和协作自动化技术的日益普及

- 医疗设备对精密运动控制的需求日益增长

- 扩展 3D 列印和桌面製造生态系统

- 对半导体封装设备的投资激增

- 转向节能型闭合迴路马达解决方案

- 政府对国内运动部件生产的激励措施

- 市场限制

- 伺服/无刷直流马达的性能极限及比较

- 来自亚洲低成本製造商的价格压力

- 整合式智慧致动器将蚕食独立马达的市场份额。

- 紧凑型设计中的温度控管挑战

- 产业供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 宏观经济因素的影响

第五章 市场规模与成长预测

- 依马达类型

- 杂交种

- 永久磁铁

- 可变磁阻

- 透过驱动系统

- 开放回路

- 闭合迴路

- 透过使用

- 工业设备

- 机器人技术与协作机器人

- 医疗设备和检测设备

- 电脑/3D列印

- 其他用途

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 东南亚

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- AMETEK, Inc.

- Anaheim Automation, Inc.

- Arcus Technology Inc.

- Changzhou Fulling Motor Co., Ltd.

- Changzhou Leili Intelligent Drive Systems Co., Ltd.

- ElectroCraft, Inc.

- Faulhaber Group

- JVL Industri Elektronik A/S

- Kollmorgen(Regal Rexnord Corp.)

- Lin Engineering, Inc.

- MinebeaMitsumi Inc.

- MOONS'Electric Co., Ltd.

- Nanotec Electronic GmbH & Co. KG

- Nidec Servo Corporation

- Nippon Pulse America, Inc.

- Oriental Motor Co., Ltd.

- Parker-Hannifin Corp.

- Performance Motion Devices, Inc.

- Phytron GmbH

- Schneider Electric SE

- Sanyo Denki Co., Ltd.

- Sonceboz SA

- STMicroelectronics NV

- Tamagawa Seiki Co., Ltd.

- Texas Instruments Inc.

第七章 市场机会与未来展望

The stepper motor market is expected to grow from USD 2.19 billion in 2025 to USD 2.26 billion in 2026 and is forecast to reach USD 2.67 billion by 2031 at 3.38% CAGR over 2026-2031.

Demand holds steady as manufacturers in robotics, medical devices, and semiconductor equipment continue choosing stepper technology for precise open-loop positioning that avoids the higher system cost of servo platforms. Collaborative robots are gaining traction in assembly cells and are accelerating the adoption of compact NEMA-frame units that deliver predictable torque and simplified programming.Semiconductor capital spending, particularly in packaging and lithography lines, sustains orders for hybrid and linear variants that operate reliably in clean-room environments. Growth also stems from laboratory automation, desktop 3-D printers, and battery-manufacturing lines seeking low-maintenance actuators with tight repeatability. While the overall motion-control sector contracted in 2024 because of inventory corrections, renewed factory-automation investment in 2025 signals a return to steady purchasing cycles.

Global Stepper Motor Market Trends and Insights

Growing adoption of robotics and collaborative automation

Manufacturing plants deploying collaborative robots favor stepper drives because predictable step increments allow intrinsic torque limiting that enhances human-machine safety. U.S. reshoring programs and European productivity upgrades are standardizing on modular motion platforms that accept low-voltage, two-phase hybrids with microstepping controllers. Encoder-equipped closed-loop models are now achieving near-servo smoothness, broadening the feasible working envelope for pick-and-place systems. Ethernet-based protocols integrate the motors into plant networks, enabling condition monitoring that minimizes unplanned downtime. As small-lot production dominates contract manufacturing, easy changeover and fast programming keep stepper solutions attractive for integrators.

Rising demand for precision motion control in medical devices

Surgical robots, hematology analyzers, and drug-delivery pumps require sub-micron accuracy within compact footprints, a specification matched by modern hybrid steppers coupled to high-resolution encoders. Designers select the motors for repeatable holding torque that maintains instrument position even when power is cut, a critical patient-safety safeguard. Quiet operation is delivered by damping algorithms that shift resonance away from audible frequencies, meeting hospital noise norms. FDA and CE rules highlight traceability, favoring vendors with ISO 13485 certificates and validated design-history files. Long replacement cycles in healthcare extend revenue visibility for component suppliers.

Performance limits versus servo / BLDC motors

Despite incremental gains, torque in stepper stacks declines sharply above 1,000 RPM, capping suitability in high-speed pick-and-place or conveyor drives. Price erosion in entry-level servos reduces the historical cost gap that once favored steppers for medium-precision work. Integrated servo packages now include automatic tuning and fieldbus options, simplifying commissioning and reducing the total installed cost delta. Marketers, therefore, emphasize use cases where positional holding torque at standstill outweighs dynamic requirements, such as valve actuation or microplate indexing.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of 3-D printing and desktop manufacturing ecosystems

- Surge in semiconductor packaging-equipment investments

- Integrated smart-actuators cannibalizing discrete motors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid variants commanded 54.65% stepper motor market share in 2025 due to their balance of torque density and 1.8-degree step resolution, and they are forecast to expand at a 3.95% CAGR, outpacing permanent-magnet and variable-reluctance formats. This dominance translates into sustained research and development allocations for finer magnetic circuits that raise flux density without enlarging frame size. Vendors now deploy high-fill-factor windings that shave I2R losses and allow operation at reduced current, extending bearing life through lower heat generation.

Hybrid improvements also underpin energy-efficiency upgrades needed to comply with IEC 60034-30-1 classes. Neodymium-iron-boron magnet blanks are laser-machined to minimize post-assembly skew, improving microstep linearity essential for photonics test stages. Permanent-magnet units still serve cost-sensitive vending machines, while variable-reluctance designs retain niches in extreme-temperature pumps where magnet decay is a concern. Overall, the stepper motor market benefits from a technology roadmap centered on hybrid refinements that close the performance gap with inexpensive servos without surrendering the cost advantage.

The Stepper Motor Market Report is Segmented by Motor Type (Hybrid, Permanent Magnet, and Variable Reluctance), Drive Technique (Open-Loop, and Closed-Loop), Application (Industrial Equipment, Robotics and Cobots, Medical and Laboratory Devices, Computing / 3-D Printing, and More), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific remained the 2025 revenue leader with a 35.74% share, anchored by Chinese component ecosystems that streamline magnet, shaft, and driver sourcing. Regional titans such as MOONS' Electric leverage scale economies above 1 million units per year, supporting aggressive pricing that feeds global export channels. Japan complements volume with technology, patented closed-loop firmware, and high-vacuum designs that power the region's semiconductor equipment exports. South Korea and Southeast Asia have emerged as contract-manufacturing hubs that integrate imported hybrids into finished printer and robot sub-assemblies, reinforcing intra-regional value chains.

North America, projected at a 3.76% CAGR, benefits from federal incentives that reimburse automation upgrades and onshore semiconductor fabs. U.S. integrators increasingly specify standardized NEMA frames over custom servos to shorten lead times during green-field EV battery-plant construction. Canadian facilities in life sciences and food packaging drive demand for wash-down IP65 variants, while Mexico supports automotive harness production lines using cost-optimized open-loop steppers.

Europe experiences steady gains under energy-efficiency directives such as Regulation 2019/1781 that push factories toward closed-loop retrofits. German OEMs exploit local precision-machining expertise to supply high-vacuum variants to the global wafer-tool sector. Meanwhile, emerging Middle-East and African economies begin specifying stepper drives in desalination, textile, and packaging projects, though volumes remain a fraction of mature regions. Altogether, geographic diversification shields the stepper motor market from isolated downturns and underscores a resilient multi-regional demand base.

- AMETEK, Inc.

- Anaheim Automation, Inc.

- Arcus Technology Inc.

- Changzhou Fulling Motor Co., Ltd.

- Changzhou Leili Intelligent Drive Systems Co., Ltd.

- ElectroCraft, Inc.

- Faulhaber Group

- JVL Industri Elektronik A/S

- Kollmorgen (Regal Rexnord Corp.)

- Lin Engineering, Inc.

- MinebeaMitsumi Inc.

- MOONS' Electric Co., Ltd.

- Nanotec Electronic GmbH & Co. KG

- Nidec Servo Corporation

- Nippon Pulse America, Inc.

- Oriental Motor Co., Ltd.

- Parker-Hannifin Corp.

- Performance Motion Devices, Inc.

- Phytron GmbH

- Schneider Electric SE

- Sanyo Denki Co., Ltd.

- Sonceboz SA

- STMicroelectronics N.V.

- Tamagawa Seiki Co., Ltd.

- Texas Instruments Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing adoption of robotics and collaborative automation

- 4.2.2 Rising demand for precision motion control in medical devices

- 4.2.3 Expansion of 3-D printing and desktop manufacturing ecosystems

- 4.2.4 Surge in semiconductor packaging-equipment investments

- 4.2.5 Shift to energy-efficient closed-loop stepper solutions

- 4.2.6 Government incentives for localised motion-component production

- 4.3 Market Restraints

- 4.3.1 Performance limits versus servo / BLDC motors

- 4.3.2 Price pressure from low-cost Asian manufacturers

- 4.3.3 Integrated smart-actuators cannibalising discrete motors

- 4.3.4 Thermal-management challenges in compact designs

- 4.4 Industry Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Motor Type

- 5.1.1 Hybrid

- 5.1.2 Permanent Magnet

- 5.1.3 Variable Reluctance

- 5.2 By Drive Technique

- 5.2.1 Open-Loop

- 5.2.2 Closed-Loop

- 5.3 By Application

- 5.3.1 Industrial Equipment

- 5.3.2 Robotics and Cobots

- 5.3.3 Medical and Laboratory Devices

- 5.3.4 Computing / 3-D Printing

- 5.3.5 Other Applications

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 South-East Asia

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Egypt

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AMETEK, Inc.

- 6.4.2 Anaheim Automation, Inc.

- 6.4.3 Arcus Technology Inc.

- 6.4.4 Changzhou Fulling Motor Co., Ltd.

- 6.4.5 Changzhou Leili Intelligent Drive Systems Co., Ltd.

- 6.4.6 ElectroCraft, Inc.

- 6.4.7 Faulhaber Group

- 6.4.8 JVL Industri Elektronik A/S

- 6.4.9 Kollmorgen (Regal Rexnord Corp.)

- 6.4.10 Lin Engineering, Inc.

- 6.4.11 MinebeaMitsumi Inc.

- 6.4.12 MOONS' Electric Co., Ltd.

- 6.4.13 Nanotec Electronic GmbH & Co. KG

- 6.4.14 Nidec Servo Corporation

- 6.4.15 Nippon Pulse America, Inc.

- 6.4.16 Oriental Motor Co., Ltd.

- 6.4.17 Parker-Hannifin Corp.

- 6.4.18 Performance Motion Devices, Inc.

- 6.4.19 Phytron GmbH

- 6.4.20 Schneider Electric SE

- 6.4.21 Sanyo Denki Co., Ltd.

- 6.4.22 Sonceboz SA

- 6.4.23 STMicroelectronics N.V.

- 6.4.24 Tamagawa Seiki Co., Ltd.

- 6.4.25 Texas Instruments Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

汽车步进马达市场:按类型、转子设计、技术、应用、车辆类型和销售管道划分-2026-2032年全球市场预测工业混合步进马达市场:依马达类型、机架尺寸、维持转矩和应用划分-2026-2032年全球市场预测步进马达市场:按类型、技术、扭力、功率、控制机制、控制器介面和应用划分-全球预测,2026-2032年五相开放回路马达市场:按马达类型、机架尺寸、扭力范围、应用和最终用户分類的全球预测(2026-2032年)

汽车步进马达市场:按类型、转子设计、技术、应用、车辆类型和销售管道划分-2026-2032年全球市场预测工业混合步进马达市场:依马达类型、机架尺寸、维持转矩和应用划分-2026-2032年全球市场预测步进马达市场:按类型、技术、扭力、功率、控制机制、控制器介面和应用划分-全球预测,2026-2032年五相开放回路马达市场:按马达类型、机架尺寸、扭力范围、应用和最终用户分類的全球预测(2026-2032年) 2025年全球混合伺服马达电缆市场

2025年全球混合伺服马达电缆市场 步进系统市场规模、份额、趋势及预测(按组件类型、最终用途和地区),2025 年至 2033 年

步进系统市场规模、份额、趋势及预测(按组件类型、最终用途和地区),2025 年至 2033 年 步进马达市场:2025年至2030年预测

步进马达市场:2025年至2030年预测 全球步进马达市场:2032 年预测 - 按类型、轴类型、功率范围、安装配置、运动控制、应用、最终用户和地区进行分析

全球步进马达市场:2032 年预测 - 按类型、轴类型、功率范围、安装配置、运动控制、应用、最终用户和地区进行分析 整合步进马达市场(2025-2029)

整合步进马达市场(2025-2029) 高扭力步进马达市场(类型 - 永磁步进马达、变磁阻步进马达、混合式步进马达);功率-低、中、高; - 2025 年至 2035 年全球产业分析、规模、份额、成长、趋势和预测

高扭力步进马达市场(类型 - 永磁步进马达、变磁阻步进马达、混合式步进马达);功率-低、中、高; - 2025 年至 2035 年全球产业分析、规模、份额、成长、趋势和预测