|

市场调查报告书

商品编码

1940858

交流/直流电源适配器:市场占有率分析、产业趋势与统计、成长预测(2026-2031)AC DC Power Adapters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

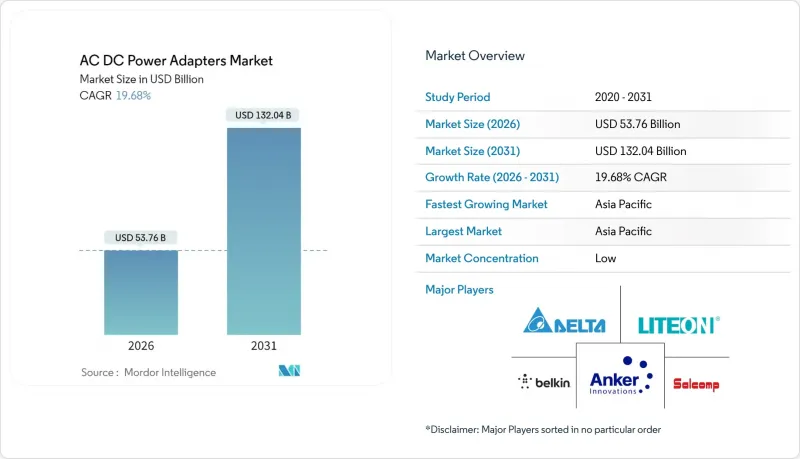

2025年,AC/DC电源供应器市值为449.2亿美元,预计2031年将达到1,320.4亿美元,而2026年为537.6亿美元。

预测期(2026-2031 年)的复合年增长率预计为 19.68%。

USB-C 电源传输标准的製定、GaN 技术的快速普及以及对监管效率的需求,共同推动了这一成长趋势。製造商受益于更高的功率/重量比,从而能够实现紧凑的多设备充电设计。随着企业硬体和电动车基础设施对扩充性解决方案的需求不断增长,高功率(>100W)市场将扩大其收入基础。永续性目标正在加速模组化适配器和回收计划的推广,将合规成本转化为在 AC-DC 电源适配器市场关键全部区域实现品牌差异化的手段。

全球AC-DC电源供应器市场趋势与洞察

USB-C 电源传输 (PD) 标准的日益普及

USB-C PD 3.1 支援高达 240W 的功率,可实现高性能笔记型电脑和工业设备的单线充电。欧盟 USB-C 强制法规将于 2024 年 12 月生效,届时将促使原始设备製造商 (OEM) 实现连接埠标准化,从而推动售后市场对独立充电器的需求。同时,IEC 62368-1 等安全标准也不断发展完善,确保即使功率提升也能维持低故障率。线缆整合使企业能够受益于更整洁的工作空间和更低的库存成本。这一趋势也正在扩展到工业控制设备、销售终端和医疗推车等领域,从而将 AC-DC 电源适配器市场纳入跨产业的电源生态系统。

家用电子电器的普及

十年前,一般家庭平均拥有7-10台需要充电的设备,现在只有3-4台。混合办公环境需要桌面电源转接器,能够为笔记型电脑提供100W或更高的功率,同时还能支援平板电脑和穿戴式装置。苹果在iPhone 15和16系列中采用USB-C接口,开启了配件更新换代的周期,使AC/DC电源转接器市场的所有厂商都从中受益。人工智慧笔记型电脑的出现提高了其稳定电力消耗,使得140W适配器从小众产品变成了主流选择。厂商们随即推出了GaN充电器,兼顾了散热和便携性,延长了产品寿命,并缓解了电子废弃物问题。

严格的全球安全和EMI/EMC认证成本

EN61204-3 和 FCC B 类认证要求高达 30kW 的辐射和传导发射测试,这会占用中小企业高达 25% 的研发预算。医疗适配器还必须符合 IEC/EN60601-1 的漏电流和绝缘要求,这将使每个产品系列的成本增加超过 5 万美元。在供应中断期间频繁更换零件需要进行完整的重新测试,从而造成库存风险。知名品牌正在建立自己的实验室以加快研发进度,这进一步加剧了 AC-DC 电源供应器市场的资源缺口。

细分市场分析

到2025年,行动装置和平板电脑细分市场将贡献30.78%的最大收入,这主要得益于智慧型手机和平板电脑普及率的不断提高。然而,预计到2031年,电动车充电适配器细分市场的复合年增长率将达到22.50%,在所有行业中位居榜首。这一快速增长反映了全球范围内的充电桩安装补贴以及汽车製造商之间互通性倡议。铁路车辆段采用800V架构,需要配备碳化硅整流器的高功率直流-直流适配器,这在交流-直流电源适配器市场催生了一个高端价格区间。升级到人工智慧笔记型电脑的需求也将推动收入成长,但成长要素是单一设备功率的提升,而非个人电脑流通数量的增加。

汽车和消费品设计的相互影响正在加速车载资讯娱乐主机采用 USB-C PD 介面。随着里程焦虑的缓解,驾驶者希望能够同时为车载设备、笔记型电脑、 VR头戴装置和车载冰箱等设备充电,从而推动了对多连接埠转接器的需求。虽然工业自动化领域目前规模仍然小规模,但全天候运作技术正在为可靠的 24V 适配器带来稳定的售后服务收入。能够使其产品蓝图检验週期与汽车製造商认证计划保持一致的供应商,将能够在 AC-DC 电源适配器市场获得可持续的份额。

预计到2025年,16-45W功率等级的电源转接器将占总收入的26.39%,主要得益于智慧型手机和平板电脑的出货量成长。然而,101-240W功率等级的电源转接器预计将以21.95%的复合年增长率成长,主要由工作站笔记型电脑、桌上型电脑替代充电器和掌上游戏机等产品推动。氮化镓(GaN)开关元件带来的250%功率密度提升,不仅缩小了面积,还提供了高效的散热性能,使厂商能够在不增加尺寸的情况下收取更高的价格。随着功率预算的增加,优化电感设计和闸极驱动将成为AC-DC电源供应器市场的关键差异化因素。

由于无线充电的普及和高效SoC的广泛应用,15W以下功率的电源适配器市场营收成长放缓。 46-100W功率的电源适配器仍然是主流笔记型电脑生态系统的核心,但其市场份额正受到能够同时为智慧型手机、平板电脑和笔记型电脑充电的高功率适配器的蚕食。企业IT负责人越来越倾向于选择整合式240W扩充坞,这种扩充座可以减少桌面杂乱,并简化多年的装置更新週期。这使得宽能带隙晶片从尖端创新转变为AC-DC电源适配器市场的基本配置。

区域分析

预计到2025年,亚太地区将占全球营收份额的44.80%,并在2031年之前以22.35%的复合年增长率成长。中国垂直整合的供应链有效降低了零件成本,而台湾晶圆代工厂则供应为全球创新提供动力的氮化镓外延晶圆。韩国智慧型手机OEM製造商和日本精密设备製造商构成了强大的价值链,巩固了主导地位。

北美市场的发展动力主要来自企业对100W以上桌上型充电器日益增长的需求,以及加州和东北部各州积极推动的电动车基础设施建设。美国能源局(DoE)的六级能源效率标准正在推动节能型拓朴结构的早期应用,并影响财富500强企业的采购政策。这使得北美成为AC-DC电源供应器市场中高价值、高利润设计方案的试验场。

在欧洲,严格的监管与对永续性的重视相结合。通用充电器指令加速了USB-C介面在整个地区的普及,并刺激了对符合PD标准的充电器的售后市场需求。二级CoC能源效率标准正在推动向宽能带隙的过渡,而循环经济法案则鼓励模组化适配器和回收计划的实施。东欧契约製造凭藉其具有成本竞争力的产品,正在赢得市场份额,成为亚洲产品的有力竞争者,从而分散了全球AC-DC电源适配器市场的风险。

儘管绝对收入较低,但中东、非洲和南美洲的新兴经济体仍实现了两位数的成长率。巴西和阿根廷透过家用电子电器进口和可再生能源併网,为南美洲的经济成长提供支持,而这离不开工业级适配器。波湾合作理事会(GCC)的基础设施建设以及非洲以行动优先的技术生态系统,都需要能够承受电网不稳定的可靠充电器。供应商根据当地电压标准和价格敏感度客製化产品,正在推动交流/直流电源适配器市场的新需求。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- USB-C 电源传输 (PD) 标准的广泛应用

- 消费性电子设备(智慧型手机、笔记型电脑、平板电脑)的普及

- 汽车配件和售后电动汽车适配器的快速电气化

- 加强能源效率法规(美国能源局第六级,欧盟碳排放交易体系第五版)

- 整合氮化镓和碳化硅半导体以提高每瓦效率

- OEM厂商对模组化适配器以适应循环经济的兴趣日益浓厚。

- 市场限制

- 严格的全球安全标准和EMI/EMC认证成本

- 原料(铜、铁氧体磁芯)价格波动

- 消费者越来越多地转向无线充电板

- OEM厂商将适配器整合到设备定价中

- 产业价值链分析

- 监管环境

- 技术展望

- 宏观经济因素如何影响市场

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按最终用户行业划分

- 消费者

- 个人电脑

- 笔记型电脑

- 行动装置

- 其他消费品

- 车

- 电动车充电适配器

- 车载资讯娱乐系统及配件

- 产业

- 消费者

- 额定功率

- ≤15 瓦

- 16-45 W

- 46-100 W

- 101-240 W

- 按连接埠类型

- 单埠

- 多埠(2至4个连接埠)

- 超多埠(5 个或更多连接埠/GaN 扩充座)

- 按外形规格

- 墙壁插座(固定插销)

- 可拆式插头(可更换)

- 桌上型电脑(Brick)

- 嵌入式/基板安装

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 东南亚

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Delta Electronics, Inc.

- Lite-On Technology Corporation

- Belkin International, Inc.(a Foxconn subsidiary)

- Anker Innovations Technology Co., Ltd.

- Shenzhen Huntkey Electric Co., Ltd.

- Salcomp PLC

- Flex Ltd.

- Mean Well Enterprises Co., Ltd.

- Phihong Technology Co., Ltd.

- TDK-Lambda Corporation

- Chicony Power Technology Co., Ltd.

- FSP Group

- Guangzhou Shengyang Electronics Co., Ltd.

- Momax Technology(HK)Ltd.

- Alphatec, Inc.(Aukey)

- RAVPower(Shenzhen Sunvalley)

- Mophie LLC(ZAGG Inc.)

- Ugreen Group Ltd.

- PNY Technologies, Inc.

- Samsung Electronics Co., Ltd.(Power Adapter Division)

- Apple Inc.(Power Adapter Engineering Group)

- Xiaomi Inc.(Accessory Business Unit)

- Oppo Electronics Corp.(SuperVOOC Chargers)

第七章 市场机会与未来展望

The AC DC power adapters market was valued at USD 44.92 billion in 2025 and estimated to grow from USD 53.76 billion in 2026 to reach USD 132.04 billion by 2031, at a CAGR of 19.68% during the forecast period (2026-2031).

Standardization around USB-C Power Delivery, rapid GaN adoption, and regulatory efficiency mandates collectively drive this trajectory. Manufacturers benefit from higher watt-per-gram ratios that allow compact, multi-device charging designs. High-power segments above 100 W widen profit pools as enterprise hardware and EV infrastructure demand scalable solutions. Sustainability targets accelerate modular adapters and take-back programs, turning compliance costs into brand differentiation levers across every major region of the AC-DC power adapters market.

Global AC DC Power Adapters Market Trends and Insights

Growing Adoption of USB-C Power Delivery (PD) Standards

USB-C PD 3.1 now supports up to 240 W, enabling single-cable charging for high-performance laptops and industrial equipment. Mandatory USB-C rules in the EU, effective since December 2024, compel OEMs to unify ports, which widens aftermarket demand for standalone chargers. Safety frameworks, such as IEC 62368-1, evolve in parallel, keeping failure rates low even as wattage increases. Enterprises benefit from cable consolidation that reduces workspace clutter and lowers inventory costs. The trend permeates industrial controls, point-of-sale kiosks, and medical carts, entrenching the AC DC power adapters market in cross-sector power-delivery ecosystems.

Proliferation of Consumer Electronics

Households now manage 7-10 charge-dependent devices, up from 3-4 a decade ago. Hybrid work environments require desktop hubs that allocate 100 W or more to laptops while sustaining tablets and wearables. Apple's transition to USB-C across the iPhone 15 and 16 families unlocked accessory refresh cycles that benefit every vendor in the AC DC power adapters market. AI-capable laptops increase steady-state power draw, making 140 W bricks a mainstream option instead of a niche one. Manufacturers respond by releasing GaN chargers that balance thermal load and portability, thereby extending product life and alleviating electronic waste concerns.

Stringent Global Safety and EMI/EMC Certification Costs

EN61204-3 and FCC Class B compliance demand exhaustive radiated and conducted emission tests up to 30 kW, absorbing as much as 25% of engineering budgets for smaller firms. Medical adapters must also satisfy IEC/EN60601-1 leakage and isolation clauses, adding USD 50,000 or more per product family. Component substitutions common during supply disruptions trigger full retest cycles, creating inventory risk. Larger brands internalize labs to shorten schedules, widening the resource gap in the AC-DC power adapters market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Electrification of Automotive Accessories and Aftermarket EV Adapters

- Rising Energy-Efficiency Regulations

- Volatility in Raw-Material Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The mobile devices and tablets segment generated the largest revenue in 2025, at 30.78%, driven by the ubiquity of smartphones and rising tablet penetration. Still, the EV charging-adapter category is forecast to register a 22.50% CAGR to 2031, the highest among all industries. This leap mirrors global charger-installation subsidies and automaker interoperability initiatives. Fleet depots adopt 800 V architectures that require robust DC-to-DC adapters with SiC rectifiers, creating premium price tiers within the AC DC power adapters market size. Consumers upgrading to AI-ready laptops also add revenue, yet growth stems more from higher wattage per unit than from additional PCs entering circulation.

Cross-pollination between automotive and consumer designs accelerates the deployment of USB-C PD in in-vehicle infotainment consoles. As range anxiety diminishes, drivers expect cabin devices, laptops, VR headsets, and refrigeration units to charge concurrently, elevating multi-port demand. Industrial automation remains a smaller slice, but round-the-clock robotics creates sticky after-sales revenue for high-reliability 24 V adapters. Vendors that align road-map validation cycles with automaker qualification timelines gain a durable share in the AC-DC power adapters market.

The 16-45 W class held 26.39% of 2025 revenue, supported by smartphone and tablet shipments. However, the 101-240 W bracket is projected to clock a 21.95% CAGR, propelled by workstation laptops, desktop replacement chargers, and portable gaming consoles. The 250% power-density gain from GaN switching elements compresses the footprint while dissipating heat effectively, allowing vendors to charge price premiums without incurring size penalties. As power budgets increase, inductor design and gate-drive optimization become key differentiation points in the AC-DC power adapter market.

Below 15 W, wireless substitution and power-efficient SoCs slow revenue expansion. The 46-100 W segment remains core to mainstream laptop ecosystems but faces cannibalization from high-power bricks that simultaneously support phones, tablets, and laptops. Enterprise IT buyers tend to gravitate toward unified 240 W docks, which reduce desk clutter and spark multi-year refresh cycles. Wide-bandgap chips thus transition from a flagship novelty to a baseline requirement in the AC-DC power adapter market.

The AC DC Power Adapters Market Report is Segmented by End-User Industry (Consumer Personal Computers, Laptops, Mobile Devices, and More), Output Power Rating (<=15W, 16-45W, 46-100W, and More), Port Type (Single-Port, and More), Form Factor (Wall Plug Fixed-Pin, Detachable Plug Interchangeable, and More), and Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held a 44.80% revenue share in 2025 and is forecast to post a 22.35% CAGR through 2031. China's vertically integrated supply chain keeps component costs low, while Taiwan's foundries supply GaN epi-wafers that underpin global innovation. South Korea's smartphone OEMs and Japan's precision engineering firms round out a robust value chain that anchors leadership in the AC-DC power adapter market.

North America follows with strong enterprise uptake of 100 W-plus desktop chargers and aggressive EV infrastructure rollouts in California and northeastern states. DoE Level VI rules push early adoption of energy-efficient topologies that ripple through the procurement policies of Fortune 500 firms. The region thus serves as a proving ground for premium, high-margin designs inside the AC-DC power adapters market.

Europe combines regulatory heft with sustainability orientation. The common-charger directive accelerated the ubiquity of USB-C across the bloc and catalyzed aftermarket demand for PD-compliant chargers. Tier 2 CoC efficiency regulations stimulate wide-bandgap migration, while circular-economy legislation rewards modular adapters and take-back schemes. Eastern European contract manufacturers are gaining market share as cost-competitive alternatives to Asian sources, thereby diversifying risk across the global AC-DC power adapters market.

Emerging economies in the Middle East, Africa, and South America contribute smaller absolute revenue but deliver double-digit growth. Brazil and Argentina anchor South American expansion through consumer electronics imports and renewable energy integrations that rely on industrial-grade adapters. Gulf Cooperation Council infrastructure upgrades and Africa's mobile-first tech ecosystems require ruggedized chargers that withstand grid instability. Vendors tailoring products to local voltage norms and price sensitivities add incremental volume to the AC-DC power adapters market.

- Delta Electronics, Inc.

- Lite-On Technology Corporation

- Belkin International, Inc. (a Foxconn subsidiary)

- Anker Innovations Technology Co., Ltd.

- Shenzhen Huntkey Electric Co., Ltd.

- Salcomp PLC

- Flex Ltd.

- Mean Well Enterprises Co., Ltd.

- Phihong Technology Co., Ltd.

- TDK-Lambda Corporation

- Chicony Power Technology Co., Ltd.

- FSP Group

- Guangzhou Shengyang Electronics Co., Ltd.

- Momax Technology (HK) Ltd.

- Alphatec, Inc. (Aukey)

- RAVPower (Shenzhen Sunvalley)

- Mophie LLC (ZAGG Inc.)

- Ugreen Group Ltd.

- PNY Technologies, Inc.

- Samsung Electronics Co., Ltd. (Power Adapter Division)

- Apple Inc. (Power Adapter Engineering Group)

- Xiaomi Inc. (Accessory Business Unit)

- Oppo Electronics Corp. (SuperVOOC Chargers)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing adoption of USB-C Power Delivery (PD) standards

- 4.2.2 Proliferation of consumer electronics (smartphones, laptops, tablets)

- 4.2.3 Rapid electrification of automotive accessories and aftermarket EV adapters

- 4.2.4 Rising energy-efficiency regulations (DoE Level VI, EU CoC V5)

- 4.2.5 Integration of GaN and SiC semiconductors boosting watt-per-gram ratio

- 4.2.6 OEM interest in adapter modularity for circular-economy compliance

- 4.3 Market Restraints

- 4.3.1 Stringent global safety and EMI/EMC certification costs

- 4.3.2 Volatility in raw-material (copper, ferrite core) prices

- 4.3.3 Growing consumer shift toward wireless charging pads

- 4.3.4 OEM consolidation of adapters into device price

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By End-user Industry

- 5.1.1 Consumer

- 5.1.1.1 Personal Computers

- 5.1.1.2 Laptops

- 5.1.1.3 Mobile Devices

- 5.1.1.4 Other Consumer

- 5.1.2 Automotive

- 5.1.2.1 EV Charging Adapters

- 5.1.2.2 In-vehicle Infotainment and Accessories

- 5.1.3 Industrial

- 5.1.1 Consumer

- 5.2 By Output Power Rating

- 5.2.1 <= 15 W

- 5.2.2 16-45 W

- 5.2.3 46-100 W

- 5.2.4 101-240 W

- 5.3 By Port Type

- 5.3.1 Single-Port

- 5.3.2 Multi-Port (2-4 Ports)

- 5.3.3 Ultra-Multi-Port (>= 5 Ports / GaN Docks)

- 5.4 By Form Factor

- 5.4.1 Wall Plug (Fixed-Pin)

- 5.4.2 Detachable Plug (Interchangeable)

- 5.4.3 Desktop (Brick)

- 5.4.4 Embedded / Board-Mount

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Russia

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 South-East Asia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Delta Electronics, Inc.

- 6.4.2 Lite-On Technology Corporation

- 6.4.3 Belkin International, Inc. (a Foxconn subsidiary)

- 6.4.4 Anker Innovations Technology Co., Ltd.

- 6.4.5 Shenzhen Huntkey Electric Co., Ltd.

- 6.4.6 Salcomp PLC

- 6.4.7 Flex Ltd.

- 6.4.8 Mean Well Enterprises Co., Ltd.

- 6.4.9 Phihong Technology Co., Ltd.

- 6.4.10 TDK-Lambda Corporation

- 6.4.11 Chicony Power Technology Co., Ltd.

- 6.4.12 FSP Group

- 6.4.13 Guangzhou Shengyang Electronics Co., Ltd.

- 6.4.14 Momax Technology (HK) Ltd.

- 6.4.15 Alphatec, Inc. (Aukey)

- 6.4.16 RAVPower (Shenzhen Sunvalley)

- 6.4.17 Mophie LLC (ZAGG Inc.)

- 6.4.18 Ugreen Group Ltd.

- 6.4.19 PNY Technologies, Inc.

- 6.4.20 Samsung Electronics Co., Ltd. (Power Adapter Division)

- 6.4.21 Apple Inc. (Power Adapter Engineering Group)

- 6.4.22 Xiaomi Inc. (Accessory Business Unit)

- 6.4.23 Oppo Electronics Corp. (SuperVOOC Chargers)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

AC-DC电源市场:依输出功率、输出电压、输入方式、安装类型、冷却方式及最终用户产业划分-2026-2032年全球市场预测双向可程式设计直流测试电源市场(按功率等级、输出电压、应用、最终用户、分销管道和功能划分),全球预测,2026-2032年

AC-DC电源市场:依输出功率、输出电压、输入方式、安装类型、冷却方式及最终用户产业划分-2026-2032年全球市场预测双向可程式设计直流测试电源市场(按功率等级、输出电压、应用、最终用户、分销管道和功能划分),全球预测,2026-2032年 返驰式转换器市场 - 2026-2031 年预测三相模组化不间断电源 (UPS) 市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测 (2024-2032)

返驰式转换器市场 - 2026-2031 年预测三相模组化不间断电源 (UPS) 市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测 (2024-2032) 2025-2029年全球ACDC电源市场

2025-2029年全球ACDC电源市场 实验室级和桌上型直流电源市场报告:2031 年趋势、预测和竞争分析

实验室级和桌上型直流电源市场报告:2031 年趋势、预测和竞争分析 2030 年桌上型电源市场预测:按类型、输出类型、电流类型、应用、最终用户和地区进行全球分析返驰式转换器市场报告:2030 年趋势、预测与竞争分析

2030 年桌上型电源市场预测:按类型、输出类型、电流类型、应用、最终用户和地区进行全球分析返驰式转换器市场报告:2030 年趋势、预测与竞争分析 AC-DC 电源供应器:市场占有率分析、产业趋势/统计、成长预测 (2024-2029)

AC-DC 电源供应器:市场占有率分析、产业趋势/统计、成长预测 (2024-2029)