|

市场调查报告书

商品编码

1940871

非洲资料中心:市场占有率分析、产业趋势与统计资料、成长预测(2026-2031 年)Africa Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

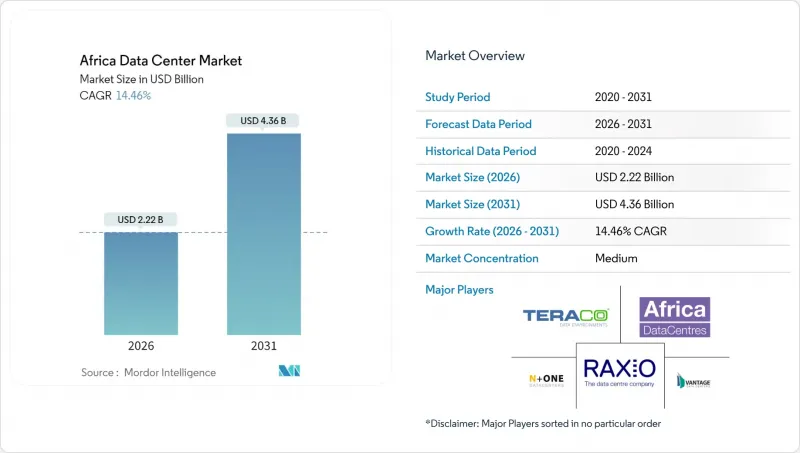

2025年非洲资料中心市场价值19.4亿美元,预计到2031年将达到43.6亿美元,高于2026年的22.2亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 14.46%。

就IT负载容量而言,市场规模预计将从2025年的1,170兆瓦成长到2030年的3,460兆瓦,在预测期(2025-2030年)内复合年增长率(CAGR)为24.29%。市场占有率和估计值均以兆瓦(MW)为单位计算和报告。这一快速成长反映了企业和政府向自主託管策略的转变,这得益于海底电缆部署的增加、5G网路的推广以及严格的资料居住规则,所有这些都转化为更低的延迟和更佳的合规经济效益,从而惠及非洲的市场领先。随着电网限制(曾经的障碍)如今有利于能够将可再生能源与合规专业知识结合的营运商,这种良性投资循环正在加速。此外,云端优先政策、不断发展的金融科技生态系统以及降低整体拥有成本的可再生能源园区也推动了需求成长。竞争正从简单的占地面积转向能源供应、熟练劳动力和监管合规,从而导致合併和联盟,将分散的本地能力整合到覆盖整个非洲数据中心市场的跨区域平台中。

非洲资料中心市场趋势与洞察

快速扩展的云端优先数位转型

非洲企业云端支出正以每年 25-30% 的速度成长,这推动了对国际超大规模容量和本地託管相结合的需求,以支援低延迟工作负载。政府 IT 法规强制规定最低在地采购,例如尼日利亚 40% 的标准,正在加速从本地部署环境转向中立运营商设施的转变。金融机构超过 60% 的交易使用云端原生核心进行处理,但监管对离岸储存的限制要求企业使用国内基础设施以满足合规性要求。这种混合部署的需求凸显了高度互联的资料中心的重要性,这些资料中心能够连接公共云端节点和企业机房,而无需透过欧洲或北美的环路连接。由此产生的需求激增有利于那些拥有配备暗纤连接到多个云端入口点的园区,以及符合银行、金融服务和保险 (BFSI) 客户要求的审核资料保护控制措施的营运商。

政府资料主权法律法规

尼日利亚2023年《资料保护法》、南非《个人资讯保护法》和肯亚《资料保护法》共同规定,敏感资料必须储存在国内。跨国公司作为关键资料控制者,必须在本地处理个人记录,否则将面临高达年收入2%的罚款,这使得位置标准从电力价格转向了法律合规性。金融监管机构强制要求客户银行资料储存在国内,从而保证了三级和四级资料中心的最低运转率。跨境传输限制正在瓦解传统的集中式架构,迫使云端服务供应商在多个非洲市场复製资料区域。随着资料居住变得日益复杂,拥有强大运转率以及法律、网路安全和审核专业知识的营运商正成为首选合作伙伴。

长期电网不稳定

在南非以外,电网可靠性低于60%迫使各设施将石油发电机设计为持续运作,而非仅作为备用电源。尼日利亚的设施需要为柴油燃料预留预算,以应对长达数週的停电,能源成本占营运支出的55%至65%(成熟市场这一比例为35%至45%)。发电机频繁跳闸会增加维护成本和排放,使永续性声明受到质疑,并限制超大规模企业的进入,直到可再生普及为止。南非的轮流停电计画虽然可预测,但仍需要电网和备用电源1:1冗余,使得电力基础设施的资本支出翻了一番。随着电池储能成本的下降,拥有太阳能、风能和地热资产的营运商享有结构性的成本优势。

细分市场分析

截至2025年,大型资料中心将占非洲资料中心市场30.92%的份额,显示客户明显偏好能够简化合规性审核和互连设计的整合式机房。规模经济效应能够显着提高电力利用效率,实现高弹性的电气拓扑结构,并整合现场可再生能源,从而降低每个机架的总拥有成本。面临严格资料保护审查的企业更倾向于将关键工作负载託管在能够证明符合ISO 27001标准并具备多层实体安全防护的园区内,从而缩短实质审查週期。此外,基础设施基金筹集的资金使大型营运商能够预先建造机房主体结构,并在主要租户签约后再进行内部建设,从而可以根据非洲数据中心市场需求的激增情况调整运转率。

成长动能依然强劲,年复合成长率高达24.12%,这主要得益于约翰尼斯堡、拉哥斯和内罗毕正在兴建的兆瓦级新设施直接连接大型机房。中型机房对寻求客製化办公空间但无需兆瓦级容量投入的区域企业仍然具有吸引力。小规模机房对于地方政府电子政府和分店的工作负载仍然适用,但由于监管部门提高了运作和安全性的标准,它们面临升级的压力。大型和超大型建设项目(主要位于南非)将分流来自跨国云端服务和内容提供商的流量,并成为洲际互联基础设施的接入点。

截至2025年,三级资料中心将占非洲资料中心市场57.92%的份额,在冗余性和资本密集度之间取得了切实可行的平衡。 99.982%的可用性标准满足了大多数银行、金融和保险(BFSI)、电信和政府采购的要求,同时也在当地投资者的计划预算范围内。三级认证也符合电力品质的实际情况,因为在许多非洲都市区,双电源和多样化的变电站并不现实。这促使营运商采用N+1拓扑结构和模组化电源模组,为随着电网弹性的提高而升级到四级预留了空间。

然而,受超大规模扩张的推动,Tier 4 的采用率正以 24.05% 的复合年增长率加速成长。这些设施需要可同时维护的系统和容错电源路径。它们正成为区域云端可用区的核心,吸引需要低延迟和本地处理的金融科技和电子商务平台。 Tier 1 和 Tier 2 网站仍然用于内容快取和灾害復原应用场景,但正面临日益严格的监管审查,促使所有者进行冗余改造。因此,随着非洲数位经济的成熟,这种分级结构反映了客户期望的逐步提高。

非洲资料中心市场报告按资料中心规模(大型、超大型、中型、巨型、小规模)、等级标准(Tier 1 & 2、Tier 3、Tier 4)、资料中心类型(超大规模/自建、企业/边缘、託管)、最终用户行业(银行、金融服务和保险 (BFSI)、IT 和 ITES、电子商务、媒体和娱乐等国家/地区细分(南非等地区)以及国家/地区细分。市场预测以 IT 负载容量(兆瓦)为单位。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 快速部署5G与国家骨干光纤计划

- 非洲企业正迅速向云端优先的数位转型迈进。

- 更多海底电缆登陆站将提升国际频宽供应。

- 政府资料主权法规推动国内託管

- 创业投资和基础设施资金正迅速流入非洲资料中心。

- 绿氢能和可再生运作校园的兴起

- 市场限制

- 电力系统长期不稳定且依赖柴油发电机

- 缺乏操作重要设施所需的熟练国内劳动力

- 关键设备的高进口关税和物流成本

- 主要成长走廊的政治和安全风险

- 市场展望

- IT负载能力

- 高架楼层面积

- 託管收入

- 预装机架

- 机架空间利用率

- 海底电缆

- 主要行业趋势

- 智慧型手机用户数量

- 每部智慧型手机的数据流量

- 行动资料通讯速度

- 宽频资料传输速度

- 光纤连接网路

- 法律规范

- 南非

- 以色列

- 奈及利亚

- 其他非洲地区

- 价值炼和通路分析

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模及成长预测(兆瓦)

- 按资料中心规模

- 大规模

- 巨大的

- 中号

- 百万

- 小规模

- 按层级标准

- 一级和二级

- 三级

- 第四级

- 依资料中心类型

- 超大规模/内部建设

- 企业/边缘运算

- 搭配

- 未使用的

- 使用

- 零售共址

- 批发託管

- 按最终用户行业划分

- BFSI

- 资讯科技与资讯科技服务

- 电子商务

- 政府

- 製造业

- 媒体与娱乐

- 沟通

- 其他最终用户

- 按国家/地区

- 南非

- 以色列

- 奈及利亚

- 其他非洲地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Teraco Data Environments Proprietary Limited

- Medallion Communications Limited

- Africa Data Centers

- Paratus Group Holdings Limited

- Vantage Data Centers LLC

- Telecom Egypt

- Agility Logistics Parks(Agility Public Warehousing Company KSCP)

- N+ONE Data Centers

- Open Access Data Centres Limited

- ONIX Data Centre Limited

- Icolo Data Centres Kenya Limited

- Interxion Holding NV(a Digital Realty company)

- Wana Corporate SA(INWI Business)

- Raxio Data Centre Holdings Pte. Ltd.

- MainOne Cable Company Limited(an Equinix company)

第七章 市场机会与未来展望

The Africa Data Center Market was valued at USD 1.94 billion in 2025 and estimated to grow from USD 2.22 billion in 2026 to reach USD 4.36 billion by 2031, at a CAGR of 14.46% during the forecast period (2026-2031).

In terms of IT load capacity, the market is expected to grow from 1.17 thousand megawatt in 2025 to 3.46 thousand megawatt by 2030, at a CAGR of 24.29% during the forecast period (2025-2030). The market segment shares and estimates are calculated and reported in terms of MW. The surge reflects a strategic pivot by enterprises and governments toward sovereign hosting, backed by subsea cable additions, 5G rollouts, and assertive data-residency rules, all of which lower latency and improve compliance economics for early movers in the Africa data center market. The investment up-cycle accelerates because grid constraints, once a deterrent, now favor operators that can bundle renewable power and compliance expertise. Demand also benefits from cloud-first mandates, growing fintech ecosystems, and renewable-powered campuses that lower total cost of ownership. Competition centers on energy sourcing, skilled labor, and regulatory navigation rather than sheer floor space, driving mergers and partnerships that consolidate fragmented local capacity into region-spanning platforms across the Africa data center market.

Africa Data Center Market Trends and Insights

Spiralling Cloud-First Digital Transformation

Corporate cloud spending in Africa is growing 25-30% each year, forcing enterprises to blend international hyperscale capacity with local colocation for low-latency workloads. Government IT mandates that stipulate minimum local sourcing, such as Nigeria's 40% threshold, accelerate migrations from on-premise rooms to carrier-neutral facilities. Financial institutions process more than 60% of transactions via cloud-native cores, yet regulatory ceilings on offshore storage require compliant in-country infrastructure. This hybrid imperative elevates interconnection rich data centers that can knit public cloud nodes to enterprise cages without hair-pinning traffic through Europe or North America. The resulting demand spike benefits operators whose campuses incorporate dark fiber to multiple cloud on-ramps and who can offer audited data-protection controls sought by BFSI clients.

Government Data-Sovereignty Legislation

Nigeria's Data Protection Act 2023, South Africa's Protection of Personal Information Act, and Kenya's Data Protection Act collectively obligate sensitive data to remain within national borders. Multinationals categorised as Data Controllers of Major Importance must process personal records locally or risk penalties up to 2% of annual turnover, reshaping site-selection criteria from power price to legal compliance. Financial regulators stipulate that customer banking data reside domestically, guaranteeing a baseline load for Tier 3 and Tier 4 halls. Cross-border transfer restrictions fragment previously centralised architectures, compelling cloud providers to replicate zones across multiple African markets. Operators that can marshal legal, cybersecurity, and audit expertise alongside robust uptime become preferred partners as data-residency complexity deepens.

Chronic Grid Instability

Outside South Africa, grid reliability hovers below 60%, compelling facilities to size diesel plants for continuous rather than standby use. Nigerian sites budget diesel for weeks-long power gaps, elevating energy to 55-65% of operating expense compared with 35-45% in mature markets. Frequent genset cycling escalates maintenance and emissions, challenging sustainability narratives and limiting hyperscale commitment until renewables scale. South Africa's load-shedding schedule, although predictable, still obliges a 1:1 redundancy between grid and backup sources, doubling capital outlay for electrical infrastructure. Operators with captive solar, wind, or geothermal assets gain a structural cost edge as battery storage costs decline.

Other drivers and restraints analyzed in the detailed report include:

- Rapid 5G and National Backbone Fibre Projects

- Rising Subsea Cable Landings

- Limited Skilled Workforce

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Large facilities commanded 30.92% of the Africa data center market size in 2025, evidencing customer preference for consolidated halls that streamline compliance audits and interconnection design. Economies of scale allow superior power usage efficiency, more fault-tolerant electrical topologies, and onsite renewable integration, lowering per-rack total cost of ownership. Enterprises facing stringent data-protection reviews prefer hosting critical workloads in campuses that can demonstrate ISO 27001 adherence and layered physical security, reducing due-diligence cycles. Moreover, capital availability from infrastructure funds enables large operators to pre-fit shells and delay internal build until anchor tenants sign, keeping utilisation aligned with demand spikes in the Africa data center market.

The growth trajectory remains steep, 24.12% CAGR, because greenfield megawatts under construction in Johannesburg, Lagos, and Nairobi pipeline directly into large-format halls. Medium-sized sites continue to appeal to regional enterprises that desire customised suites without megawatt-scale commitments. Small footprints, though still relevant for municipal e-government and branch office workloads, face upgrade pressure as regulations tighten uptime and security benchmarks. Massive and mega-scale builds, predominantly in South Africa, serve spill-over traffic from multinational cloud and content providers and act as landing pads for cross-continent interconnection fabrics.

Tier 3 halls made up 57.92% of the Africa data center market size in 2025, striking a pragmatic balance between redundancy and capital intensity. The 99.982% availability threshold satisfies most BFSI, telecom, and government procurement checklists while keeping project budgets within reach for local investors. Tier 3 certification also aligns with power-quality realities, as dual utility feeds or diverse substations remain impractical in many African metros. As a result, operators deploy N+1 topologies with modular power blocks that can evolve toward Tier 4 if grid resilience improves.

Tier 4 adoption is nevertheless accelerating at 24.05% CAGR, predominantly through hyperscale expansions that require concurrently maintainable systems and fault-tolerant electrical paths. Such facilities anchor regional cloud availability zones, attracting fintech and e-commerce platforms that need low-latency, in-country processing. Tier 1 and Tier 2 sites persist for content caching and disaster-recovery use cases but increasingly attract scrutiny from regulators, nudging owners to retrofit additional redundancy. The tier mix therefore mirrors a gradual up-shift in customer expectations as African digital economies mature.

The Africa Data Center Market Report is Segmented by Data Center Size (Large, Massive, Medium, Mega, and Small), Tier Standard (Tier 1 and 2, Tier 3, and Tier 4), Data Center Type (Hyperscale/Self-Built, Enterprise/Edge, and Colocation), End User Industry (BFSI, IT and ITES, E-Commerce, Media and Entertainment, and More), and Country (South Africa and More). The Market Forecasts are Provided in Terms of IT Load Capacity (MW).

List of Companies Covered in this Report:

- Teraco Data Environments Proprietary Limited

- Medallion Communications Limited

- Africa Data Centers

- Paratus Group Holdings Limited

- Vantage Data Centers LLC

- Telecom Egypt

- Agility Logistics Parks (Agility Public Warehousing Company KSCP)

- N+ONE Data Centers

- Open Access Data Centres Limited

- ONIX Data Centre Limited

- Icolo Data Centres Kenya Limited

- Interxion Holding N.V. (a Digital Realty company)

- Wana Corporate S.A. (INWI Business)

- Raxio Data Centre Holdings Pte. Ltd.

- MainOne Cable Company Limited (an Equinix company)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid rollout of 5G and national backbone fibre projects

- 4.2.2 Spiralling cloud-first digital transformation among African enterprises

- 4.2.3 Rising subsea cable landings boosting international bandwidth supply

- 4.2.4 Government data-sovereignty legislation driving in-country hosting

- 4.2.5 Surging venture capital and infrastructure fund inflows into African data centers

- 4.2.6 Emergence of green hydrogen and renewable-powered campuses

- 4.3 Market Restraints

- 4.3.1 Chronic grid instability and reliance on diesel generators

- 4.3.2 Limited domestic skilled workforce for critical facility operations

- 4.3.3 High import tariffs and logistics costs for mission-critical equipment

- 4.3.4 Political and security risks in key growth corridors

- 4.4 Market Outlook

- 4.4.1 IT Load Capacity

- 4.4.2 Raised Floor Space

- 4.4.3 Colocation Revenue

- 4.4.4 Installed Racks

- 4.4.5 Rack Space Utilization

- 4.4.6 Submarine Cable

- 4.5 Key Industry Trends

- 4.5.1 Smartphone Users

- 4.5.2 Data Traffic Per Smartphone

- 4.5.3 Mobile Data Speed

- 4.5.4 Broadband Data Speed

- 4.5.5 Fiber Connectivity Network

- 4.5.6 Regulatory Framework

- 4.5.6.1 South Africa

- 4.5.6.2 Israel

- 4.5.6.3 Nigeria

- 4.5.6.4 Rest of Africa

- 4.6 Value Chain and Distribution Channel Analysis

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (MW)

- 5.1 By Data Center Size

- 5.1.1 Large

- 5.1.2 Massive

- 5.1.3 Medium

- 5.1.4 Mega

- 5.1.5 Small

- 5.2 By Tier Standard

- 5.2.1 Tier 1 and 2

- 5.2.2 Tier 3

- 5.2.3 Tier 4

- 5.3 By Data Center Type

- 5.3.1 Hyperscale/Self-built

- 5.3.2 Enterprise/Edge

- 5.3.3 Colocation

- 5.3.3.1 Non-Utilized

- 5.3.3.2 Utilized

- 5.3.3.2.1 Retail Colocation

- 5.3.3.2.2 Wholesale Colocation

- 5.4 By End-User Industry

- 5.4.1 BFSI

- 5.4.2 IT and ITES

- 5.4.3 E-Commerce

- 5.4.4 Government

- 5.4.5 Manufacturing

- 5.4.6 Media and Entertainment

- 5.4.7 Telecom

- 5.4.8 Other End Users

- 5.5 By Country

- 5.5.1 South Africa

- 5.5.2 Israel

- 5.5.3 Nigeria

- 5.5.4 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Teraco Data Environments Proprietary Limited

- 6.4.2 Medallion Communications Limited

- 6.4.3 Africa Data Centers

- 6.4.4 Paratus Group Holdings Limited

- 6.4.5 Vantage Data Centers LLC

- 6.4.6 Telecom Egypt

- 6.4.7 Agility Logistics Parks (Agility Public Warehousing Company KSCP)

- 6.4.8 N+ONE Data Centers

- 6.4.9 Open Access Data Centres Limited

- 6.4.10 ONIX Data Centre Limited

- 6.4.11 Icolo Data Centres Kenya Limited

- 6.4.12 Interxion Holding N.V. (a Digital Realty company)

- 6.4.13 Wana Corporate S.A. (INWI Business)

- 6.4.14 Raxio Data Centre Holdings Pte. Ltd.

- 6.4.15 MainOne Cable Company Limited (an Equinix company)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment

2026年全球智慧客户资料中心市场报告2026年全球网路资料中心(IDC)市场报告2026年全球资料中心房地产市场报告

2026年全球智慧客户资料中心市场报告2026年全球网路资料中心(IDC)市场报告2026年全球资料中心房地产市场报告 资料中心市场:按组件、资料中心类型、层级、冷却方式、电源、最终用户和组织规模划分-2026年至2032年全球市场预测

资料中心市场:按组件、资料中心类型、层级、冷却方式、电源、最终用户和组织规模划分-2026年至2032年全球市场预测 全球在轨资料中心市场预测(至2034年)-按平台、组件、系统、连接类型、应用、最终用户和地区分類的分析

全球在轨资料中心市场预测(至2034年)-按平台、组件、系统、连接类型、应用、最终用户和地区分類的分析 资料中心汇流排市场规模、份额和成长分析:按导体材料、绝缘类型、额定功率、安装/整合方法、资料中心类型和地区划分-2026-2033年产业预测2026年全球客製化资料中心市场报告

资料中心汇流排市场规模、份额和成长分析:按导体材料、绝缘类型、额定功率、安装/整合方法、资料中心类型和地区划分-2026-2033年产业预测2026年全球客製化资料中心市场报告 资料中心能源概况 - Oracle:自 2019 年以来,能源使用量以 24% 的复合年增长率成长,由于可再生能源的使用,排放保持稳定,但 Stargate 专案可能会大幅增加碳足迹。

资料中心能源概况 - Oracle:自 2019 年以来,能源使用量以 24% 的复合年增长率成长,由于可再生能源的使用,排放保持稳定,但 Stargate 专案可能会大幅增加碳足迹。 氢动力资料中心市场分析及预测(至2035年):类型、产品类型、服务、技术、组件、应用、部署模式、最终用户、功能、安装模式资料中心市场分析及预测(至2035年):类型、产品类型、服务、技术、组件、应用、部署模式、最终用户、解决方案

氢动力资料中心市场分析及预测(至2035年):类型、产品类型、服务、技术、组件、应用、部署模式、最终用户、功能、安装模式资料中心市场分析及预测(至2035年):类型、产品类型、服务、技术、组件、应用、部署模式、最终用户、解决方案