|

市场调查报告书

商品编码

1940883

非洲聚对苯二甲酸乙二醇酯(PET):市场占有率分析、产业趋势与统计、成长预测(2026-2031)Africa Polyethylene Terephthalate (PET) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

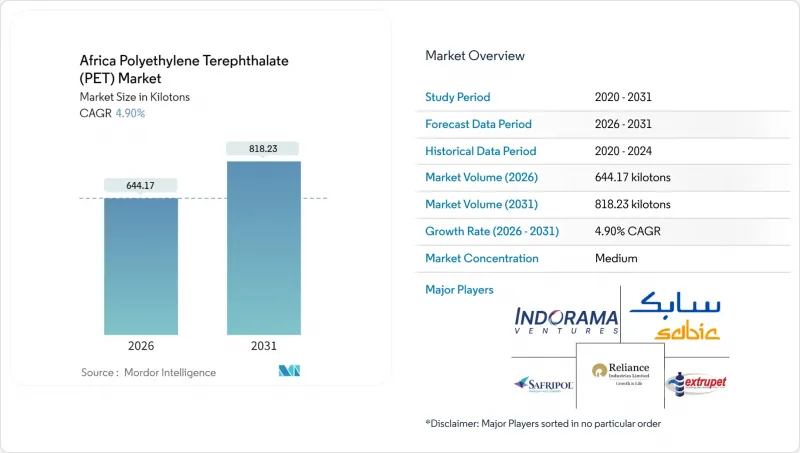

预计到 2026 年,非洲聚对苯二甲酸乙二醇酯 (PET) 市场规模将达到 644.17 千吨。

预计该数值将从 2025 年的 614.08 千吨增长到 2031 年的 818.23 千吨,2026 年至 2031 年的复合年增长率为 4.9%。

中产阶级的持续成长、非洲大陆自由贸易区(AfCFTA)下的关税协调以及本地瓶装产能的扩张是推动需求成长的关键因素。品牌所有者青睐PET材质,因为它具有透明度高、强度重量比好以及与现有灌装线亲和性等优点;同时,由于生产者责任法规的加强,对再生PET的需求也在增长。跨国快速消费品(FMCG)公司不断建造本地生产基地,将供应重心从依赖进口转向依赖区域树脂工厂。公共部门贷款与循环经济目标相契合,将大规模蓝色贷款和绿色债券用于建造综合收集和回收基础设施。然而,原油价格波动以及消费者对生物基替代品的兴趣带来了策略上的不确定性,这需要灵活的筹资策略和产品创新。

非洲聚对苯二甲酸乙二醇酯(PET)市场趋势与洞察

该地区不断壮大的中产阶级的饮料消费量增加

都市区收入的快速增长推动了对碳酸软性饮料、瓶装水和机能饮料的需求。可口可乐HBC公司正投资10亿美元扩大在奈及利亚的产能,而可口可乐饮料非洲公司将于2024年在纳米比亚开设一条价值5,000万美元的瓶装生产线。产量的增加带来了瓶坯和瓶盖的大宗订单,确保了对原生树脂的稳定需求。不断增长的消费给不发达的废弃物处理系统带来了压力,拉各斯和阿克拉等城市正在试点生产者费用押金返还计划。饮料製造商正在整合封盖、拉伸吹塑成型和填充生产线,以降低运输成本并前置作业时间。灌装量的增加降低了单位包装成本,使PET包装在价格上能与玻璃和铝包装竞争。

政府设定的再生包装含量目标

肯亚2024年实施的「生产者延伸责任制」(EPR)法规透过对每件进口产品附加税150肯亚先令的税款并要求品牌註册,为使用再生材料提供了明确的奖励。南非的EPR框架(自2021年起生效)要求每年报告回收和处理量。尼日利亚监管机构正在製定类似的规则,并计划在基础设施到位后逐步实施最低再生材料含量标准。百事可乐撒哈拉以南非洲地区目前的目标是在其饮料产品线中实现20%的再生聚酯(rPET)含量,并已为区域采购协议奠定了基础。 rPET含量较高的公司可以透过新兴的生态标章计画获得更高的商店可见度。然而,有效实施这些措施需要将非正式的回收商正规化,并将清洁和固态缩聚(SSP)设备升级到食品级标准。

加速消费者向生物基/可堆肥替代品的转变

2019年至2024年间,全球采用生物基包装的新型食品和饮料产品年均成长60%。欧盟法规将某些可生物降解聚合物指定为可回收物,此监管先例可供非洲政策制定者效法。各大品牌正在试行可堆肥咖啡胶囊和淀粉基咖啡壶,这给小众市场对PET的使用带来了压力。再生PET的价格通常比原生材料高出每吨150美元,因此实现长期成本平衡有助于推广生物基解决方案。然而,由于原料物流、专用挤出设备以及工业堆肥设施的缺乏,扩大非洲生物聚合物的供应仍面临许多挑战。

细分市场分析

2025年,原生PET在非洲聚对苯二甲酸乙二醇酯(PET)市场占有82.78%的份额,加工商看重其稳定的特性黏度和广泛的食品级认证。该细分市场受益于成熟的进口管道、原材料的优惠关税待遇以及充足的瓶坯加工能力。瓶装回收PET(rPET)的供应仍然受限,因为目前只有少数工厂运作专门的高温洗涤和固相聚合(SSP)生产线来生产高品质的片状PET。

到2031年,再生PET市场将以7.85%的复合年增长率增长,这主要得益于生产者责任延伸(EPR)法规以及饮料巨头将经营团队薪酬与循环包装目标挂钩的自愿承诺。国际金融公司(IFC)的融资支持了新的清洗生产线和SSP(固相萃取)瓶颈的消除,而链延长添加剂则使得在不影响透明度的前提下恢復IVI(内部体积指数)成为可能。随着这些投资的成长,到本十年末,非洲再生级聚对苯二甲酸乙二醇酯(PET)的市占率可望达到两位数。然而,在打包供应、监管一致性和信贷市场到位之前,原生树脂可能仍将占据主导地位,从而降低大规模再生PET(rPET)整合的风险。

非洲聚对苯二甲酸乙二醇酯(PET)市场报告按原料类型(原生PET、再生PET)、终端用户产业(汽车、建筑、电气电子、工业机械、包装及其他终端用户产业)和地区(奈及利亚、南非、非洲其他地区)进行细分。市场预测以数量(吨)和价值(美元)为单位。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 随着该地区中产阶级的壮大,饮料消费量也不断增加。

- 政府对再生包装含量设定的目标

- 跨国消费品製造商扩大本地灌装产能

- 根据非洲大陆自由贸易区(AfCFTA)进行的关税调整将降低PET进口成本。

- 新兴发展金融机构/国际金融公司为PET回收基础设施提供融资

- 市场限制

- 原物料价格波动与原油价格相关

- 消费者越来越倾向选择生物基/可堆肥替代品

- 小规模再生聚乙烯(rPET)原料收集网络

- 价值链分析

- 波特五力模型

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 进出口趋势

- 价格趋势

- 形态趋势

- 回收利用概述

- 法律规范

- 终端用户产业趋势

- 航太(航太零件生产收入)

- 汽车(汽车产量)

- 建筑与施工(新建建筑占地面积)

- 电气电子设备(电气电子设备生产收入)

- 包装(塑胶包装量)

第五章 市场规模和成长预测(价值和数量)

- 依原料类型

- 处女宠物

- 再生PET(rPET)

- 按最终用户行业划分

- 车

- 建筑/施工

- 电气和电子设备

- 工业和机械

- 包装

- 其他终端用户产业

- 按地区

- 奈及利亚

- 南非

- 其他非洲地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Alpek SAB de CV

- ALPLA

- Extrupet(Pty)Ltd.

- Far Eastern New Century Co., Ltd.

- Indorama Ventures Public Company Limited.

- Mohinani Group

- Mpact Group Limited

- PETCO

- Reliance Industries Limited

- SABIC

- Safripol Pty Ltd

- Sumilon Eco Pet Sarl

第七章 市场机会与未来展望

第八章:执行长面临的关键策略挑战

Africa Polyethylene Terephthalate (PET) market size in 2026 is estimated at 644.17 kilotons, growing from 2025 value of 614.08 kilotons with 2031 projections showing 818.23 kilotons, growing at 4.9% CAGR over 2026-2031.

Sustained middle-class growth, tariff harmonization under the African Continental Free Trade Area (AfCFTA), and expanding local bottling capacity are the primary forces lifting demand. Brand owners favor PET for its clarity, strength-to-weight ratio, and familiarity in existing filling lines, while recycled grades gain momentum as producer responsibility rules tighten. Multinational fast-moving consumer goods (FMCG) players continue to build localized production hubs, shifting the supply balance away from imports and toward regional resin plants. Public-sector lending taps into circular economy objectives, directing large-scale blue-loans and green-bonds toward integrated collection and recycling infrastructure. Nonetheless, oil-linked feedstock swings and consumer interest in bio-based alternatives create strategic uncertainty that requires agile sourcing strategies and product innovation.

Africa Polyethylene Terephthalate (PET) Market Trends and Insights

Rising Beverage Consumption by the Region's Growing Middle Class

Rapid income gains across urban hubs propel demand for carbonated drinks, bottled water, and functional beverages. Coca-Cola HBC has earmarked USD 1 billion for Nigerian capacity additions, while Coca-Cola Beverages Africa opened a USD 50 million bottling line in Namibia in 2024. Higher throughput translates into larger off-take contracts for preforms and caps, locking in steady offtake for virgin resin. Growing consumption stresses underdeveloped waste systems, prompting cities such as Lagos and Accra to pilot deposit-return schemes funded by producer levies. Beverage converters respond by co-locating closure injection, stretch-blow, and filling lines, reducing freight cost and cutting lead times. Rising fill volumes compress per-unit packaging costs, preserving PET's price competitiveness against glass and aluminum.

Government Targets for Recycled-Content Packaging

Kenya's 2024 Extended Producer Responsibility (EPR) regulations impose KES 150 per imported item and require brand registration, creating explicit incentives for recycled content. South Africa's EPR framework, live since 2021, demands annual reporting on collected and processed volumes. Nigeria's regulator is drafting similar rules that will phase in minimum recycled content thresholds once infrastructure matures. PepsiCo Sub-Saharan Africa now targets 20% rPET inclusion across its beverage lines, setting an anchor for regional offtake contracts. Firms that certify higher rPET ratios gain shelf visibility advantages under emerging eco-labeling schemes. Effective enforcement, however, hinges on formalizing informal collectors and upgrading washing and solid-state polycondensation (SSP) units to food-grade standards.

Rising Consumer Shift to Bio-Based/Compostable Alternatives

Global food and beverage launches featuring bio-based packaging rose 60% annually between 2019 and 2024. European Union rules recognize certain biodegradable polymers as recyclable, creating a regulatory precedent that African policymakers may emulate. Brands test compostable coffee-capsules and starch-based pots, pressuring PET volumes in niche segments. Recycled PET often trades USD 150 per tonne above virgin, widening the motivation to test bio-based solutions if long-run cost parity can be achieved. Scaling biopolymer supply in Africa remains complex because feedstock logistics, specialized extrusion equipment, and industrial composting sites are still limited.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Local Bottling Capacity by Multinational FMCGs

- AfCFTA-Driven Tariff Alignment Lowering PET Import Costs

- Sub-Scale Collection Networks for rPET Feedstock

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Virgin PET secured 82.78% of the Africa Polyethylene Terephthalate (PET) market share in 2025 because converters prize its consistent intrinsic viscosity and broad food-grade approvals. The segment benefits from mature import corridors, duty concessions on raw materials, and plentiful preform conversion capacity. Bottle-to-bottle rPET remains supply-constrained as high-grade flake requires specialized hot-wash and SSP lines that only a handful of plants operate today.

Recycled PET is advancing at an 7.85% CAGR to 2031, propelled by EPR regulations and voluntary pledges from beverage majors that link executive remuneration to circular-packaging milestones. International Finance Corporation loans underwrite new wash lines and SSP debottlenecking, while chain-extension additives now restore intrinsic viscosity without compromising clarity. As these investments scale, the Africa Polyethylene Terephthalate (PET) market size for recycled grades could reach meaningful double-digit share by the end of the decade. Still, virgin resin will dominate until bale supply, regulatory coherence, and credit markets align to de-risk full-scale rPET integration.

The Africa Polyethylene Terephthalate (PET) Market Report is Segmented by Source Type (Virgin PET, Recycled PET), End-User Industry (Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging, Other End-User Industries), and Geography (Nigeria, South Africa, Rest of Africa). The Market Forecasts are Provided in Terms of Volume (Tons) and Value (USD).

List of Companies Covered in this Report:

- Alpek S.A.B. de C.V.

- ALPLA

- Extrupet (Pty) Ltd.

- Far Eastern New Century Co., Ltd.

- Indorama Ventures Public Company Limited.

- Mohinani Group

- Mpact Group Limited

- PETCO

- Reliance Industries Limited

- SABIC

- Safripol Pty Ltd

- Sumilon Eco Pet Sarl

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising beverage consumption by the region's growing middle-class

- 4.2.2 Government targets for recycled-content packaging

- 4.2.3 Expansion of local bottling capacity by multinational FMCGs

- 4.2.4 AfCFTA-driven tariff alignment lowering PET import costs

- 4.2.5 Emerging DFI/IFC financing for PET recycling infrastructure

- 4.3 Market Restraints

- 4.3.1 Volatile crude-oil-linked feedstock prices

- 4.3.2 Rising consumer shift to bio-based/compostable alternatives

- 4.3.3 Sub-scale collection networks for rPET feedstock

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Import And Export Trends

- 4.7 Price Trends

- 4.8 Form Trends

- 4.9 Recycling Overview

- 4.10 Regulatory Framework

- 4.11 End-use Sector Trends

- 4.11.1 Aerospace (Aerospace Component Production Revenue)

- 4.11.2 Automotive (Automobile Production)

- 4.11.3 Building and Construction (New Construction Floor Area)

- 4.11.4 Electrical and Electronics (Electrical and Electronics Production Revenue)

- 4.11.5 Packaging(Plastic Packaging Volume)

5 Market Size & Growth Forecasts (Value and Volume)

- 5.1 By Source Type

- 5.1.1 Virgin PET

- 5.1.2 Recycled PET (rPET)

- 5.2 By End-User Industry

- 5.2.1 Automotive

- 5.2.2 Building and Construction

- 5.2.3 Electrical and Electronics

- 5.2.4 Industrial and Machinery

- 5.2.5 Packaging

- 5.2.6 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Nigeria

- 5.3.2 South Africa

- 5.3.3 Rest of Africa

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)**/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Alpek S.A.B. de C.V.

- 6.4.2 ALPLA

- 6.4.3 Extrupet (Pty) Ltd.

- 6.4.4 Far Eastern New Century Co., Ltd.

- 6.4.5 Indorama Ventures Public Company Limited.

- 6.4.6 Mohinani Group

- 6.4.7 Mpact Group Limited

- 6.4.8 PETCO

- 6.4.9 Reliance Industries Limited

- 6.4.10 SABIC

- 6.4.11 Safripol Pty Ltd

- 6.4.12 Sumilon Eco Pet Sarl

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

8 Key Strategic Questions for CEOs

再生聚对苯二甲酸乙二醇酯市场:2026-2032年全球市场预测(依原料种类、形态、等级、製造流程、颜色及应用划分)

再生聚对苯二甲酸乙二醇酯市场:2026-2032年全球市场预测(依原料种类、形态、等级、製造流程、颜色及应用划分) 2026年全球聚对苯二甲酸乙二醇酯(PET)杯市场报告

2026年全球聚对苯二甲酸乙二醇酯(PET)杯市场报告 全球聚对苯二甲酸乙二醇酯(PET)市场规模、份额、趋势和成长分析报告(2026-2034年)

全球聚对苯二甲酸乙二醇酯(PET)市场规模、份额、趋势和成长分析报告(2026-2034年) 聚对苯二甲酸乙二醇酯(PET)杯市场规模、份额和成长分析:按杯子设计与应用、原料、製造技术、最终用途和地区划分-2026-2033年产业预测

聚对苯二甲酸乙二醇酯(PET)杯市场规模、份额和成长分析:按杯子设计与应用、原料、製造技术、最终用途和地区划分-2026-2033年产业预测 生物基聚对苯二甲酸丙二醇酯(BioPTT)市场:市场规模-按地区、应用和预测至2034年

生物基聚对苯二甲酸丙二醇酯(BioPTT)市场:市场规模-按地区、应用和预测至2034年 聚对苯二甲酸乙二醇酯市场分析及预测(至2035年):类型、产品类型、应用、形态、材料类型、製程、最终用户、功能、安装类型

聚对苯二甲酸乙二醇酯市场分析及预测(至2035年):类型、产品类型、应用、形态、材料类型、製程、最终用户、功能、安装类型 南美洲聚对苯二甲酸乙二酯(PET):市场占有率分析、产业趋势与统计、成长预测(2026-2031)全球再生聚对苯二甲酸乙二醇酯市场规模、份额、趋势和成长分析报告(2026-2034年)2026年全球再生聚对苯二甲酸乙二酯市场报告2026年全球聚对苯二甲酸乙二醇酯(PET)及聚聚丁烯对苯二甲酸酯(PBT)树脂市场报告

南美洲聚对苯二甲酸乙二酯(PET):市场占有率分析、产业趋势与统计、成长预测(2026-2031)全球再生聚对苯二甲酸乙二醇酯市场规模、份额、趋势和成长分析报告(2026-2034年)2026年全球再生聚对苯二甲酸乙二酯市场报告2026年全球聚对苯二甲酸乙二醇酯(PET)及聚聚丁烯对苯二甲酸酯(PBT)树脂市场报告