|

市场调查报告书

商品编码

1940905

美国农药:市场占有率分析、产业趋势与统计、成长预测(2026-2031)US Insecticide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

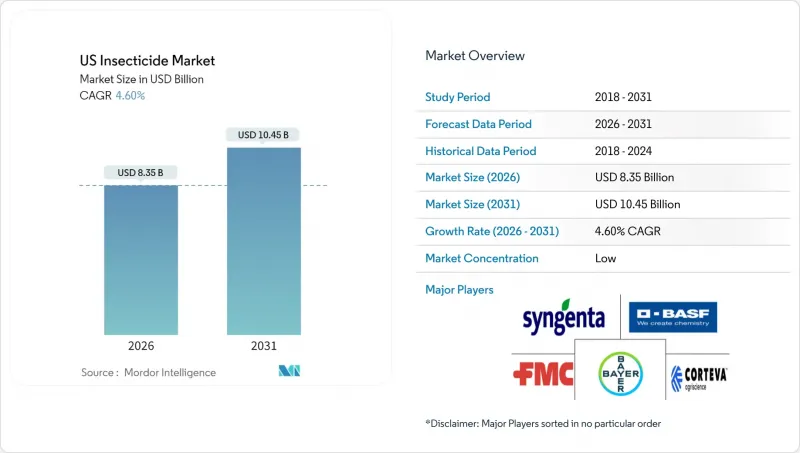

2025年美国杀虫剂市值为79.8亿美元,预计到2031年将达到104.5亿美元,高于2026年的83.5亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 4.60%。

特种作物种植面积的扩大、精密农业的日益普及以及持续存在的抗药性问题,在监管审查日益严格的情况下,支撑了市场需求。成长要素包括:专注于透过种子处理进行早期保护;对低剂量活性成分(可减少环境影响)的需求日益增长;以及人事费用的上升推动了自动化或单次施用技术的普及。儘管叶面喷布仍占据主导地位,但美国杀虫剂市场正稳步向技术主导方法转型,以减少工人接触并提高投资回报率。目前的竞争策略着重于产品系列的广度、监管适应性以及与支持变数施药决策的资料平台的整合。

美国农药市场趋势与洞察

扩大特色作物种植面积

预计2020年至2024年间,杏仁、柑橘和酿酒葡萄的每英亩盈利将显着增长,这将促使种植者加大对符合出口残留标准的高品质杀虫剂的投资。在同一时期,加州的杏仁面积增加了12%,而佛罗里达州则扩大了杀虫剂使用范围,以控制亚洲柑橘叶蝇,作为柑橘復育工作的一部分。由于特种作物的毛利率通常是谷物的三到五倍,种植者们正在积极采用成本更高、风险更低的配方,以保障产量和品质。同时,气候变迁正在开闢新的产区,并扩大太平洋西北地区的面积。因此,美国杀虫剂市场中,高端产品的销售量保持稳定,这些产品能够承受价格上涨而不会大幅降低需求。

抗药性管理的必要性

监管机构目前强制要求轮调使用不同作用机制的杀虫剂来防治玉米根虫和棉花小菜蛾等害虫。大学推广服务中心的数据显示,到2024年,67%的玉米种植者已製定正式的抗性管理方案,较2020年的23%显着成长。这种转变导致对新型活性成分的需求出现可预测的高峰,同时也加速了旧化合物的淘汰。因此,更丰富的产品系列能够提供收入保障,使供应商能够规划整个种植季节并占据更高的市场份额。系统性的轮换也有助于开发多效合一的活性成分配方,这种配方可以在一次处理中同时提供杀虫剂和杀菌剂的保护,从而在满足监管要求的同时减少人工成本。

由环保署主导的废除

监管机构撤回已上市的杀虫剂活性成分,造成了市场混乱,迫使人们迅速采用替代化学品,这通常会导致每英亩成本上升,加剧种植户的经济压力,而拥有强大替代产品系列的公司则从中获益。美国环保署(EPA)于2024年限制在吸引授粉昆虫的作物上使用新烟碱类杀虫剂,每年造成约3.4亿美元的市场损失,并即时催生了对替代化学品的需求,而由于供应受限,这些替代化学品的价格更高。随着可供选择的化学品种类日益减少,中小企业难以维持永续的产品系列,这些措施正在加速产业整合。

细分市场分析

儘管叶面喷布在2025年占据了美国杀虫剂市场55.87%的份额,但由于种子处理剂在各种作物系统中的通用性,预计到2031年,其复合年增长率将达到4.78%,成为成长最快的市场。以目前的普及速度,到2031年,种子处理剂在美国杀虫剂市场的份额预计将超过叶面喷布。推动种子处理剂普及的因素包括:单次包覆即可提供4-6週的保护,与同等规模的叶面喷布喷洒方案相比,总成本最多可降低40%。处理过的种子只需一次施用于土壤,无需额外的处理步骤,从而显着节省了人力成本。此外,监管压力也支持使用封闭式种子披衣设备,从而减少了工人的接触风险。

在灌溉基础设施发达的地区,尤其是在水资源有限的地区,人们对化学灌溉和滴灌的需求日益增长,以便同时控制病虫害和调节土壤湿度。熏蒸处理在草莓苗圃和苗圃生产仍占有一席之地,但成长有限。土壤处理在多年生果园中仍然十分重要,因为根系保护至关重要。目前,产品研发的重点是包埋颗粒剂和生物接种剂,它们与系统性活性成分配合使用,可在根系生长期间持续释放药效。这些趋势表明,美国杀虫剂市场可以透过多种途径来满足不断变化的农业和工业需求。

美国农药市场报告按施用方法(化学灌溉、叶面喷布、熏蒸、种子处理等)和作物类型(经济作物、水果和蔬菜、谷物、豆类和油籽等)进行细分。市场预测以价值(美元)和数量(公吨)为单位。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

- 调查方法

第二章 报告

第三章执行摘要主要发现

第四章:主要产业趋势

- 每公顷农药用量

- 活性成分价格分析

- 法规结构

- 我们

- 价值炼和通路分析

- 市场驱动因素

- 扩大特色作物种植面积

- 抗药性管理的必要性

- 种子处理技术的广泛应用

- 低剂量活性成分的核准

- 对保护性农业的需求

- 无人机精准喷洒

- 市场限制

- 美国环保署主导的召回产品

- 对授粉昆虫健康的担忧

- 基因改造昆虫抗性状

- 喷雾器人手不足

第五章 市场规模和成长预测(价值和数量)

- 应用方法

- 化学灌溉

- 叶面喷布

- 熏蒸

- 种子处理

- 土壤处理

- 作物类型

- 经济作物

- 水果和蔬菜

- 谷类和杂粮

- 豆类和油籽

- 草坪和观赏植物

第六章 竞争情势

- 关键策略倡议

- 市占率分析

- 公司概况

- 公司简介

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Nufarm Ltd

- Syngenta Group

- UPL Limited

- PI Industries

- Sumitomo Chemical Co.

- American Vanguard Corporation

- Envu US LLC(Cinven)

- Helena Agri-Enterprises(Marubeni Corporation)

- Nutrien Ltd

- Gowan Company

- Atticus LLC

第七章:CEO们需要思考的关键策略问题

The US insecticide market was valued at USD 7.98 billion in 2025 and estimated to grow from USD 8.35 billion in 2026 to reach USD 10.45 billion by 2031, at a CAGR of 4.60% during the forecast period (2026-2031).

Rising specialty-crop acreage, wider precision-agriculture deployment, and persistent resistance issues are sustaining demand even as regulatory scrutiny tightens. Growth also reflects the drive for earlier-stage protection through seed treatment, the premium assigned to low-rate active ingredients that lighten environmental loading, and escalating labor costs that favor automated or one-pass application tactics. While foliar sprays still dominate, the US insecticide market is steadily tilting toward technology-enabled approaches that reduce operator exposure and improve return on investment. Competitive strategies now center on portfolio breadth, regulatory adaptability, and integration with data platforms that support variable-rate decisions.

US Insecticide Market Trends and Insights

Specialty-Crop Acreage Expansion

Revenue potential per acre for almonds, citrus, and wine grapes grew markedly between 2020 and 2024, encouraging heavier investment in premium chemistry that meets export residue rules. In California, almond plantings rose 12% over the period, while Florida citrus recovery efforts enlarged insecticide programs aimed at Asian citrus psyllid suppression. Specialty crops often deliver three-to-five-fold higher gross returns relative to grains, so growers willingly adopt high-priced, reduced-risk formulations that protect both yield and quality. Climate shifts are simultaneously opening new production zones in the Pacific Northwest, widening the addressable acreage. As a result, the US insecticide market gains reliable volume from premium categories that absorb price increases without material demand destruction.

Resistance management needs

Regulatory mandates now codify rotation of modes of action for pests such as corn rootworm and cotton bollworm. University extension data show 67% of corn growers implemented formal resistance programs in 2024 versus 23% in 2020, a shift that creates predictable peaks for newer actives while hastening obsolescence of aging compounds. Portfolio depth, therefore, becomes a revenue hedge, with suppliers able to fill entire seasonal plans, enjoying greater share security. Structured rotation also stimulates development of formulations that blend multiple actives, bundling insecticidal and fungicidal protection in single passes to ensure compliance and labor savings.

EPA-Driven Withdrawals

Regulatory withdrawals of established insecticide active ingredients are creating market disruptions that force rapid adoption of alternative chemistries, often at higher per-acre costs that strain grower economics while benefiting companies with robust replacement product portfolios. The EPA's 2024 decision to restrict neonicotinoid applications on pollinator-attractive crops eliminated approximately USD 340 million in annual market value, creating immediate demand for alternative chemistries that command premium pricing due to limited supply. These regulatory actions are accelerating industry consolidation as smaller companies struggle to maintain viable product portfolios amid shrinking chemistry options.

Other drivers and restraints analyzed in the detailed report include:

- Growth in seed-treatment adoption

- Approvals of low-rate AIs (Active Ingredients)

- Pollinator-Health Pressures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Foliar sprays led with 55.87% of the US insecticide market share in 2025, whereas seed treatment posted the fastest growth at a 4.78% CAGR through 2031, anchored by their versatility across crop systems. The US insecticide market size for seed treatment is poised to eclipse by 2031 if current penetration continues. Adoption is supported by evidence that a single coating delivers four-to-six-week protection at up to 40% lower total cost than comparable foliar-only programs. Labor savings are significant because treated seed enters the soil in one operation, eliminating additional passes. Regulatory pressure also favors closed-system seed coaters that reduce applicator exposure.

Demand for chemigation and drip injection rises where irrigation infrastructure permits, especially in water-limited regions aiming for simultaneous pest and moisture management. Fumigation retains a niche in strawberry beds and nursery stock but exhibits minimal growth. Soil treatments remain important in perennial orchards where root-zone protection is critical. Product development now focuses on encapsulated microgranules and biological inoculants that complement systemic actives, offering sustained release throughout root flushes. Together, these trends illustrate the diversified pathway through which the US insecticide market accommodates evolving agronomic and labor realities.

The US Insecticide Market Report is Segmented by Application Mode (Chemigation, Foliar, Fumigation, Seed Treatment, and More), and Crop Type (Commercial Crops, Fruits and Vegetables, Grains and Cereals, Pulses and Oilseeds, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

List of Companies Covered in this Report:

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Nufarm Ltd

- Syngenta Group

- UPL Limited

- PI Industries

- Sumitomo Chemical Co.

- American Vanguard Corporation

- Envu US LLC (Cinven)

- Helena Agri-Enterprises (Marubeni Corporation)

- Nutrien Ltd

- Gowan Company

- Atticus LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY & KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 United States

- 4.4 Value Chain & Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Specialty-crop acreage expansion

- 4.5.2 Resistance management needs

- 4.5.3 Growth in seed-treatment adoption

- 4.5.4 Approvals of low-rate AIs (Active Ingredients)

- 4.5.5 Protected agriculture demand

- 4.5.6 Drone-based precision spraying

- 4.6 Market Restraints

- 4.6.1 EPA-driven withdrawals

- 4.6.2 Pollinator-health pressures

- 4.6.3 GM insect-resistant traits

- 4.6.4 Applicator labor shortage

5 MARKET SIZE AND GROWTH FORECAST (VALUE AND VOLUME)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Seed Treatment

- 5.1.5 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Bayer AG

- 6.4.3 Corteva Agriscience

- 6.4.4 FMC Corporation

- 6.4.5 Nufarm Ltd

- 6.4.6 Syngenta Group

- 6.4.7 UPL Limited

- 6.4.8 PI Industries

- 6.4.9 Sumitomo Chemical Co.

- 6.4.10 American Vanguard Corporation

- 6.4.11 Envu US LLC (Cinven)

- 6.4.12 Helena Agri-Enterprises (Marubeni Corporation)

- 6.4.13 Nutrien Ltd

- 6.4.14 Gowan Company

- 6.4.15 Atticus LLC

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

储粮杀虫剂市场报告:按产品类型、应用和地区划分(2026-2034年)

储粮杀虫剂市场报告:按产品类型、应用和地区划分(2026-2034年) Buprofezin市场:2026-2032年全球市场预测(按剂型、作物、应用方法、最终用户和销售管道)Chlorantraniliprole市场:全球市场按作物类型、剂型、应用方法和最终用户分類的预测-2026-2032年克百威市场:按剂型、作物类型、最终用户、分销管道和应用划分-2026-2032年全球预测高效能Cypermethrin市场:按製剂类型、销售管道和应用划分-2026-2032年全球预测二唑唑市场:依作物类型、剂型、应用方法、最终用户和分销管道划分-2026-2032年全球预测

Buprofezin市场:2026-2032年全球市场预测(按剂型、作物、应用方法、最终用户和销售管道)Chlorantraniliprole市场:全球市场按作物类型、剂型、应用方法和最终用户分類的预测-2026-2032年克百威市场:按剂型、作物类型、最终用户、分销管道和应用划分-2026-2032年全球预测高效能Cypermethrin市场:按製剂类型、销售管道和应用划分-2026-2032年全球预测二唑唑市场:依作物类型、剂型、应用方法、最终用户和分销管道划分-2026-2032年全球预测 农药市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年全球农药市场规模、份额、趋势和成长分析报告(2026-2034年)

农药市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年全球农药市场规模、份额、趋势和成长分析报告(2026-2034年) 全球农药市场报告(2026 年)

全球农药市场报告(2026 年) 农药市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、地区和竞争格局划分,2021-2031年

农药市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、地区和竞争格局划分,2021-2031年