|

市场调查报告书

商品编码

1831005

能源与永续发展追踪报告:网路规模与人工智慧运算(2025)-2024年能源消耗将成长22%,成长速度是营收成长的两倍多,而排放量将连续第二年下降。Energy & Sustainability Tracker - Webscale & AI Compute, 2025: Energy Consumption Grows 22% in 2024, Over 2x Faster than Revenues, but Emissions Fall for Second Straight Year |

|||||||

人工智慧革命已经到来,到2025年,其发展动能将扩展到主流市场。但这场革命需要前所未有的电力消耗。本报告全面分析了网路规模和人工智慧运算产业的能源使用情况,并对这场变革的核心参与者进行了评估。本报告利用专有的超大规模财务追踪器,扩展了现有的电信业者能源永续性分析,涵盖截至 2025 年 6 月的市场数据。

视觉

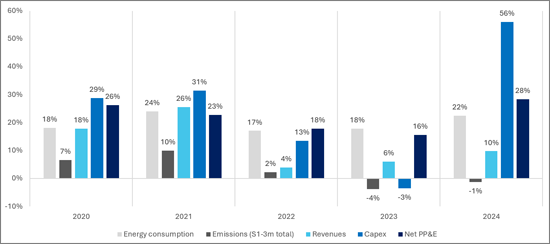

超大规模(全球):

能源、排放、收入、资本支出和净固定资产的年增长

超大规模产业定义

超大规模产业包括拥有并经营大型(超大规模)资料中心和海底光缆网路的互联网、软体和服务公司。MTN顾问公司于2017年开始进行分析时,这些公司建置超大规模资料中心的主要原因是支援庞大的客户群(例如腾讯的微信)、提供云端服务(例如亚马逊AWS)以及运作内部营运和研发。然而,在过去三年中,这些公司开始建造规模更大、更复杂的资料中心,专门用于人工智慧训练和推理。

范围和覆盖范围

本报告分析了全球20家领先的超大规模公司,并列出了财务指标(收入、资本支出、净固定资产及设备)和能源相关指标(能源和电力总消耗量、可再生能源占比和温室气体排放量)。数据涵盖2019年至2024年,分析采用了突显能源使用和永续发展趋势的衍生指标。

本研究仅限于已上市且拥有经审计财务报表及透明商业模式的公司。人工智慧投资热潮催生了许多新玩家,包括提供GPU租赁服务的新型云端服务供应商和专注于低成本电力的公司。然而,这些公司大多缺乏成熟的商业模式,其长期生存能力尚不明朗。一些重要的私人公司(例如马斯克的xAI)也不在本研究的范围内。

虽然本报告并未涵盖全球所有资料中心,但本研究中包含的上市超大规模资料中心公司占了全球超大规模容量的大部分,因此被认为是影响市场未来的关键参与者。虽然一些重要的私人运营商和中立运营商提供託管服务,许多小型设施也满足特定政府机构和企业的需求,但本研究重点关注主要的市场领导者。

人工智慧持续成长的能源需求

数据显示,该产业正在经历快速转型。光是2024年,网路规模化产业的能源消耗量就将达到190.8太瓦时(TWh),比前一年惊人地成长了22%。自2019年以来,能源消耗量的复合年增长率(CAGR)为19.9%,远超产业整体预期。这一增长与人工智慧(AI)的蓬勃发展密切相关。

数据清晰地表明,人工智慧投资正在显着增加网路规模化企业的能源消耗强度。 2019年,整个产业的能源消耗量为每百万美元收入51.7兆瓦时(MWh),到2024年底将上升至每百万美元收入71.5兆瓦时。 2024年,能源消耗强度将加速成长,能源消耗成长将是营收成长的两倍多。资料中心占能源消耗的85%至90%,而且这一比例还在上升。特别是Meta,其资料中心消耗的能源占总能源消耗的97%以上。

策略转型:电力保障-垂直整合

面对如此强劲的需求,该产业目前正经历结构性转型。能源已成为业务连续性的关键要素,促使人工智慧开发商和资料中心营运商投资建造自有发电设施,从而实现垂直整合。例如:

- 亚马逊:投资 5 亿美元建造小型模组化核反应堆,并收购了毗邻核电厂的资料中心用地。

- Fermi REIT:在德州启动了一个人工智慧资料中心和能源综合体,目标是发电量高达 11 吉瓦。

- Prologis:从物流地产转型,为人工智慧专用资料中心确保超过 3 吉瓦的电力供应。

儘管许多此类交易都优先考虑无碳能源,但本报告警告称,週期性投资结构和市场泡沫存在风险。报告特别指出,目前的情况与2000年代初期的网路泡沫有相似之处。

永续发展聚焦:两个指标所揭示的现实

儘管能源消耗正在快速增长,但该报告描绘了一幅更为复杂却也令人鼓舞的可持续发展图景。网路产业在再生能源应用方面处于领先地位,预计到2024年,其能源消耗的84.3%将来自再生能源。这比2019年的56.3%有了显着成长,并且远远超过电信业(约22-23%)。

这项努力已取得了显着的环境成效。温室气体排放量(范围 1、范围 2(市场型)、范围 3)连续第二年下降,从 2022 年的峰值 2.36 亿公吨(二氧化碳当量)降至 2024 年的 2.241 亿公吨。

然而,该报告提醒人们不要过于自信。虽然范围 1 和范围 2 的排放量通常备受关注,但它们仅仅反映了部分情况。范围 3(来自整个价值链的间接排放)更为重要。范围 3 的排放量占产业碳足迹的大部分。忽视这些排放的公司低估了其环境影响的真实程度。即使像苹果这样的公司完全使用再生能源运营,每年售出的数亿台设备仍然会消耗全球电网的电力。因此,全面了解排放情况至关重要,而本报告提供了全面的评估,以帮助企业做到这一点。

目标组织

|

|

|

目录

第1章 概要

第2章 分析

第3章 全球结果

第4章 企业业绩

第5章 排行榜

第6章 原始数据

第7章

The AI revolution is here, but its engine is running on an unprecedented amount of power. As artificial intelligence explodes into the mainstream in 2025, the focus intensifies on the energy-hungry data centers that power it. This report, "Energy & Sustainability Tracker: Webscale & AI Compute, 2025," from MTN Consulting, provides a comprehensive assessment of energy usage within the webscale and AI compute industry, analyzing the key operators at the heart of this transformation. Our analysis extends MTN Consulting's established research into network operator energy and sustainability, and leverages our proprietary webscale financial tracker covering market data through June 2025.

VISUALS

Webscale(global):

YoY% growth in energy, emissions, revenues, capex and net PP&E

The Webscale Sector Defined

The "webscale" sector comprises Internet, Software & Services companies that own and operate large (hyperscale) data centers and submarine cable networks. When we began coverage in 2017, these operators built hyperscale data centers for three primary purposes: supporting massive customer bases (Tencent's WeChat), delivering cloud services to end users (Amazon's AWS), and running internal operations and research. Over the past three years, webscale operators have increasingly built larger, more sophisticated data centers specifically for AI training and inference, what we term "AI Compute."

Scope and Coverage

This report analyzes 20 leading webscalers, presenting financial metrics (revenues, capex, and net PP&E) alongside energy-related indicators: total energy and electricity consumption, renewable energy share, and greenhouse gas emissions (Scopes 1, 2, both location- and market-based, and 3). Data cover 2019-2024, supplemented by derived metrics that illuminate energy use and sustainability trends.

Our focus is on publicly held companies with audited financial statements and transparent business models. The recent AI investment boom has produced a surge of new entrants: some renting GPU capacity ("neocloud" providers), others chasing low-cost energy or niche segments. Many of these firms lack proven business models and may not survive long. A few significant private players, such as Elon Musk's xAI, also fall outside this report's scope.

While we don't capture every data center worldwide, the public webscalers analyzed here account for the vast majority of global hyperscale capacity, and they are the players most likely to shape the market's future direction. Important private and carrier-neutral providers supply colocation services, and many smaller facilities serve specific government and corporate needs, but our coverage focuses on the dominant market leaders.

Data Quality and Methodology

Compiling a consistent dataset was a challenge. This is not the kind of exercise you can outsource to an AI. Financial reporting follows clear standards; energy and environmental disclosures do not. Companies vary widely in what they report, and ESG data are not always audited. MTN Consulting reviewed over 150 sustainability reports, relying on verified data whenever possible and estimating where necessary to create comparable, credible time series. We believe this is the most objective and comprehensive review of energy and sustainability practices in the webscale/hyperscale and AI Compute markets available today.

One important caveat: our focus on publicly traded companies introduces a reporting bias. Public companies face greater public pressure and are more likely to use renewable energy and commit to aggressive GHG emissions reduction programs. The "go green" push is not universal; private companies often take shortcuts and avoid disclosure. The companies we don't track likely have weaker environmental records than these public webscalers.

The Unstoppable Energy Demand of AI

The data reveals a sector in the throes of rapid transformation. In 2024 alone, the webscale sector consumed 190.8 TWh of energy, a staggering 22% year-over-year increase. Since 2019, energy use has grown at a compound annual growth rate (CAGR) of 19.9%, far outpacing broader industry estimates. This growth is intrinsically linked to the AI boom.

The evidence is clear that AI investment is making webscalers significantly more energy-intensive. In 2019, the sector consumed 51.7 megawatt-hours (MWh) per $1 million in revenue. By the end of 2024, that figure had risen to 71.5 MWh per $1 million. Growth in energy intensity accelerated in 2024, as energy consumption grew at over twice the speed of revenues. This energy is overwhelmingly consumed by data centers, which account for 85-90% of total webscale energy use. That figure continues to climb, driven by companies like Meta, which consumes over 97% of its total energy in data centers.

A Strategic Shift: Vertical Integration for Power Security

Faced with this demand, the industry is undergoing a fundamental shift. Energy has become so critical that we are witnessing vertical integration, with AI developers and data center owners investing directly in energy generation. A small sample of such moves:

- Amazon's $500M investment in small modular nuclear reactors and its strategic purchase of a data center site near a nuclear power plant.

- Fermi REIT's launch of a flagship AI data center and energy complex in Texas, designed to supply up to 11 GW.

- Prologis's pivot from logistics real estate to securing over 3 GW of power for specialized AI data centers.

While many of these deals prioritize carbon-free energy, the report sounds a note of caution on the circular investment dynamics and the potential risks of a market bubble, drawing parallels to the dot-com era.

Sustainability in the Spotlight: A Tale of Two Metrics

Despite soaring energy consumption, the report uncovers a more nuanced and promising story on sustainability. The webscale sector is leading the charge in renewable energy adoption. In 2024, a remarkable 84.3% of webscale energy came from renewable sources, a dramatic increase from 56.3% in 2019 and far exceeding other sectors like telecom (approx. 22-23%).

This commitment is driving tangible environmental progress. For the second consecutive year, total greenhouse gas emissions (Scopes 1, 2-market-based, and 3) have fallen, reaching 224.1 million metric tons of CO2-equivalent in 2024, down from a peak of 236.0 million in 2022.

However, the report issues a critical warning against complacency. It emphasizes that the commonly cited Scope 1 and 2 emissions tell only part of the story. The far more significant Scope 3 emissions, i.e. the indirect emissions from a company's value chain, comprise the vast majority of the sector's total carbon footprint. Companies that downplay these emissions are ignoring the true scale of their environmental impact. For instance, a company like Apple may run its operations on 100% renewables, but the hundreds of millions of devices it sells annually draw power from grids worldwide. A full accounting is essential, and this report provides it.

Who Leads and Who Lags? Exclusive Company Rankings

This tracker goes beyond sector-level analysis to deliver granular company rankings on key performance indicators, enabling you to benchmark players and identify leaders and laggards.

- Renewable Energy Adoption: Amazon, Microsoft, Meta, and Alphabet all achieved 98% or higher in 2024, while Chinese webscalers Alibaba, Tencent, and Baidu ranked lowest; some of these, however, are making rapid progress.

- Energy Intensity: Microsoft and Meta are among the most energy-intensive companies, a direct result of their massive AI compute investments. In contrast, device-centric companies like Xiaomi and Apple have the lowest intensity.

- Total Carbon Footprint: Amazon is the standout outlier, accounting for over 30% of the entire sector's emissions at over 68 million metric tons in 2024. While its renewable commitment is strong, its Scope 3 emissions are massive, and the report details its controversial departure from a UN-backed climate initiative.

Why You Need This Report

This report delivers actionable intelligence unavailable elsewhere. Investors can evaluate AI infrastructure opportunities with confidence. Policy makers can address energy grid capacity challenges with hard data. Industry participants can benchmark their sustainability performance against peers. The report provides detailed company-by-company metrics spanning six years, proprietary analysis of energy intensity trends, and clear rankings across renewable adoption and emissions. You'll gain the competitive advantage needed to make informed decisions in the rapidly evolving AI compute landscape. This is the definitive resource for understanding the intersection of artificial intelligence, energy consumption, and environmental impact.

Organizations covered:

|

|

|

Table of Contents

1. Overview

2. Analysis

3. Global results

4. Company results

5. Rankings

6. Raw data

7. About

List of Figures and Charts

Global, and for each of 20 companies:

- Revenues ($M) and YoY % growth

- Capex ($M) and Capex/Revenue ratio

- Net PP&E ($M) and YoY % growth

- Capex and Net PP&E growth

- YoY % growth in energy, emissions, revenues, capex and net PP&E

- Correlation between financial, energy input, and emissions output metrics, 2019-24

- Energy consumption in GWh and electricity's share of total energy, 2019-24

- YoY growth rates in electric use vs. total energy consumption

- Energy intensity vs. electric intensity (MWh per $1M in revenues), 2019-24

- Energy intensity, Net PP&E basis

- Renewable energy consumption in GWh and % total

- Carbon footprint by emissions type (market-based), millions of metric tons of CO2-equivalent

- Market-based vs. location-based carbon footprint (S1-2-3 total), millions of metric tons of CO2-equivalent

- Scope 3 emissions as % of S1-2-3 total, market-based vs. location-based

- Emissions intensity in MT CO2-equivalent per $M of revenue

- Emissions intensity in MT CO2-equivalent per $M of Net PP&E

Additional charts for each company:

- Company vs. global average: Energy intensity in MWh per $M of revenue

- Company vs. global average: Energy intensity in MWh per $M of revenue

- Company vs. global average: S1-S3m emissions intensity in MT CO2-equivalent per $M of revenue

- Company vs. global average: Renewable energy as % total consumption

Individual charts ranking all webscalers by the following key metrics that we track:

- Capex ($M)

- Net PP&E ($M)

- Revenues ($M)

- Electricity consumption

- Energy consumption

- Renewable energy consumption (MWh)

- % renewable energy

- Capex/Revenue

- Electric as % total energy

- Scope 3 as % of total S1-3 emissions

- YoY % change in energy consumption

- Electricity intensity (MWh per $M in revenue)

- Energy intensity (MWh per $M in revenue)

- Energy intensity of fixed asset base (MWh per $1M in Net PP&E)

- Revenue from 1MWh electricity used ($)

- Revenue from 1MWh energy used ($)

- Emissions intensity: S1-2m per $M in Net PP&E

- Emissions intensity: S1-2m per $M in revenue

- Emissions intensity: S1-3m per $M in Net PP&E

- Emissions intensity: S1-3m per $M in revenue

- S1

- S2l

- S2m

- S1-2l

- S1-2m

- S3

- S1-3m

永续性和能源管理软体市场(按软体类型、技术、部署模型、应用、公司规模和最终用户划分)—全球预测 2025-2032

永续性和能源管理软体市场(按软体类型、技术、部署模型、应用、公司规模和最终用户划分)—全球预测 2025-2032 2025年永续性与能源管理软体全球市场报告

2025年永续性与能源管理软体全球市场报告 按设备类型、安全类型和地区分類的能源网路安全市场

按设备类型、安全类型和地区分類的能源网路安全市场 能源管理软体市场(2025-2029)永续能源管理软体市场预测至 2032 年:按组件、部署类型、组织规模、模组、最终用户和地区进行的全球分析能源管理软体市场(按组件、应用、部署模式和最终用户产业)—2025 年至 2030 年全球预测

能源管理软体市场(2025-2029)永续能源管理软体市场预测至 2032 年:按组件、部署类型、组织规模、模组、最终用户和地区进行的全球分析能源管理软体市场(按组件、应用、部署模式和最终用户产业)—2025 年至 2030 年全球预测 商业大楼用HVAC最佳化能源管理软体的全球市场 - 市场规模,竞争情形(2024年~2029年)

商业大楼用HVAC最佳化能源管理软体的全球市场 - 市场规模,竞争情形(2024年~2029年) 全球永续性与能源管理软体市场

全球永续性与能源管理软体市场 全球永续能源管理软体市场 - 全球产业分析、规模、份额、成长、趋势、预测 (2031) - 按软体、按最终用途、按模组、按地区

全球永续能源管理软体市场 - 全球产业分析、规模、份额、成长、趋势、预测 (2031) - 按软体、按最终用途、按模组、按地区