|

市场调查报告书

商品编码

1246781

海上互联互通(第 11 版)Maritime Connectivity, 11th Edition |

||||||

即使 COVID-19 的影响从市场上消失,数字化和吞吐量需求仍然存在。 客船将经历连接需求激增,对石油和天然气的需求以及离岸设施将逐船持续,这可能是船员福利成为需求的主要驱动力的时候。 总体而言,对海事卫星连接的需求持续增长,到 2032 年,新的终端外形和价格点预计将向小型船舶开放,新的商业模式将获得边际用例。

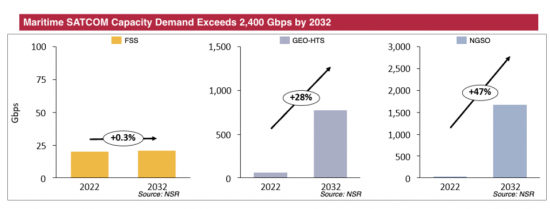

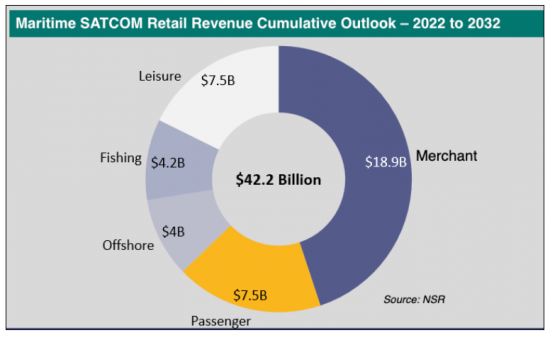

预测期内的累计收入预计为 422 亿美元,复合年增长率为 9.5%。

分析总结

本报告分析了全球海事连接(海事卫星通信)的最新发展、市场动态和增长机会、GEO(对地静止)和 NGEO(非对地静止)连接在海事卫星通信中的作用,以及整个市场规模 - 运行中的卫星数量、零售额、容量需求、收入等 - 趋势展望(未来 10 年),按地区和细分市场(商船、客船、海上设施、渔船、休閒船)我们将汇总并发布行业参与者未来应采取的详细趋势和策略等信息。

主要特点

本报告分析的内容:

- NGSO(非固定)公司的努力及其影响:Starlink/OneWeb

- 按地区划分的趋势:8 个地区(北美、拉丁美洲、欧洲、中东/非洲、亚洲、AOR(大西洋)、IOR(印度洋)、POR(太平洋)、ARC(南极洲))

- 按船舶类型预测:总共 5 种类型(商业、客运、海上设施、渔业、休閒船)

- 每个船舶市场的 VSAT 需求摘要

本报告中分析的公司

SpaceX Starlink、OneWeb、Telesat Lightspeed、AWS Kuiper、Inmarsat、Intellian、Speedcast、Marlink、Anuvu、SES

内容

第 1 章海上卫星通信:执行摘要

- 概览

- 420 亿美元的市场机会

- 短期内每月 ARPU 上升

- 正在向非 GEO HTS 迁移

- 主要分析结果

第2章主要分析结果

- 卫星通信船市场的 LEO+MEO 枢轴

- VSAT:历史比较

- 区域展望

- 有效市场 (TAM)

- 服务提供商层的状态

- 商船的前景

- 客船前景

- 海上设施的前景

- 渔船的前景

- 休閒船的前景

第 3 章问题与建议

- 超越“连通性”的货币化

- NGEO 是否会改善连接并减少服务提供商提供的 VAS 的作用?

- 海上卫星通信的三大增长机会

第四章数据附录

Report Summary:

NSR's “ Maritime Connectivity, 11th Edition” report offers valuable insights and analysis, helping industry stakeholders understand market dynamics and capitalize on growth opportunities in maritime SatCom markets.

Focusing on the impacts from Non-GEO systems such as the 'new entrants' of Starlink, OneWeb, and mPower this edition explores the role of GEO vs. Non-GEO (NGSO) connectivity in the maritime SATCOM markets. Building from a regional and segment level view, the report is broken down into 5 vessel types - Merchant, Passenger, Offshore, Fishing, and Leisure. Each segmentation provides insight into In-service units, retail revenues, capacity demand and revenue. Overall, as more capacity choices come online over the next ten years Maritime SATCOM players will need to have a carefully crafted capacity strategy in place to optimize revenues and meet customer demands.

As the impacts of COVID-19 fall away from the market, digitalization and throughput requirements remain. Passenger vessels are seeing a surge in connectivity requirements, oil and gas / Offshore demand persist on a per-vessel basis, and now might be the time for crew welfare provisioning to become a key driver of demand. Towards 2032, new terminal form factors and price points will unlock smaller and smaller vessels, new business models will help capture marginal use-cases, and overall, the demand for maritime satellite connectivity continues to expand.

Bottom line, NSR's “ Maritime Connectivity, 11th Edition” helps industry stakeholders make informed decisions about their business strategies and investments in this important evolving market.

Key questions are answered in this report?

- What are the major satellite connectivity architectures?

- Which region holds the most opportunity?

- What is the revenue outlook of the Maritime SATCOM Market?

- What is the growth rate of the Maritime SATCOM market?

- Which vessel market is in transition towards NGSO market?

Who Should Purchase this Report:

- SATCOM service providers

- Business Strategy mangers

- Maritime end-users

- Maritime Satellite Equipment manufacturers

- Satellite Operators

- Financial services and other investor community members

Key Features:

Covered in this Report:

- NEW in this Edition - Focus on the uptake and impact of NGSO Players such as Starlink and OneWeb

- 8 Regions - NAM, LAM, EU, MEA, ASIA, AOR, IOR, POR, ARC

- Forecasts for 5 vessel markets - Merchant, Passenger, Offshore, Fishing, Leisure.

- Overview of VSAT demand for each vessel market.

Key Findings:

- Merchant Vessels - VSAT adoption increasing across merchant market. IoT and Cloud-to-Vessel adoption is occurring across fleets, including more SD-WAN installations.

- Passenger Vessels - Cruise liners trialing NGSO connectivity e.g., SpaceX Starlink. Passenger vessels are optimizing their fleets network to automate data processing.

- Offshore Vessels - A market that is filled with VSAT architecture. Early trials of NGSO low latency connectivity taking place in Q1 of 2023 e.g., SpaceX Starlink.

- Fishing Vessels - Vessel optimization for HTS architecture is occurring and is a given with new builds. VSAT adoption is on the rise across the fishing market.

- Leisure Vessels - NGSO adoption is occurring across both small and super yachts. VSAT adoption is happening on small yachts due to affordable price tag.

Overall cumulative revenue for the forecast period is USD$42.2 billion and a CAGR of 9.5%.

Companies included in this Report:

SpaceX Starlink, OneWeb, Telesat Lightspeed, AWS Kuiper, Inmarsat, Intellian, Speedcast, Marlink, Anuvu, SES.

Table of Contents

1. Maritime SATCOM Executive Summary

- 1.1. Overview

- 1.2. A $42 Billion Opportunity

- 1.3. A near-term Increase for Monthly ARPUs

- 1.4. The Non-GEO HTS Migration Underway

- 1.5. Major Findings

2. Key Findings

- 2.1. A LEO + MEO Pivot for SATCOM vessel markets

- 2.2. VSAT Historical Comparisons

- 2.3. Regional Outlook

- 2.4. Total Addressable Market (TAM)

- 2.5. State of Service Provider Layer

- 2.6. Merchant Outlook

- 2.7. Passenger Outlook

- 2.8. Offshore Outlook

- 2.9. Fishing Outlook

- 2.10. Leisure Outlook

3. Challenges and Recommendations

- 3.1. Monetizing beyond "Connectivity"

- 3.2. Non-GEO Improving Connectivity and Decreasing Role of SP-provided VAS?

- 3.3. Three Big Growth Opportunities in Maritime SATCOM.

4. Data Appendix

- 4.1. Global Forecast At-a-glance

- 4.2. Merchant Forecast

- 4.3. Passenger Forecast

- 4.4. Offshore Forecast

- 4.5. Fishing Forecast

- 4.6. Leisure Forecast

- 4.7. Key Definitions

- 4.8. Changelog

List of Exhibits

1. Maritime SATCOM Executive Summary

- 1.1. Maritime SATCOM Retail Revenue Cumulative Outlook - 2022 to 2032

- 1.2. Global Maritime SATCOM Market Retail Revenue ($M)

- 1.3. Global Maritime SATCOM Average BB $Month 2022-2027

- 1.4. Maritime SATCOM Capacity Demand, FSS vs. GEO-HTS vs. NGSO

- 1.5. Maritime SATCOM Capacity Revenues

2. Key Findings

- 2.1. Maritime SATCOM Retail Revenues by Capacity Type (USD $M)

- 2.2. VSAT Vessel Comparison

- 2.3. VSAT No. of Vessels

- 2.4. Broadband SATCOM Addressable Vessels

- 2.5. Broadband Connected Vessels

- 2.6. Top Maritime Service Provider by Service Revenues (2022)

- 2.7. Top Maritime Service Provider by Connected Vessels (2022)

- 2.8. Merchant Retail ARPU 2022-2032 (USD$ per Month)

- 2.9. Merchant Service Revenues ($M) - GEO-HTS vs NGSO

- 2.10. Percentage of Addressable Merchant vessels

- 2.11. Passenger Retail ARPU 2022-2032 (USD$ per Month)

- 2.12. Passenger Service Revenues ($M) - GEO-HTS vs NGSO

- 2.13. Percentage of Addressable Passenger vessels

- 2.14. Offshore Retail ARPU 2022-2032 (USD$ per Month)

- 2.15. Offshore Service Revenues ($M) - GEO-HTS vs NGSO

- 2.16. Percentage of Addressable Offshore vessels

- 2.17. Fishing Retail ARPU 2022-2032 (USD$ per Month)

- 2.18. Fishing Service Revenues ($M) - GEO-HTS vs NGSO

- 2.19. Percentage of Addressable Fishing vessels

- 2.20. Leisure Retail ARPU 2022-2032 (USD$ per Month)

- 2.21. Leisure Service Revenues ($M) - GEO-HTS vs NGSO

- 2.22. Percentage of Addressable Leisure vessels

3. Challenges and Recommendations

- 3.1. Average VSAT Mbps Demand Per Vessel by Market

- 3.2. NGSO Maritime SATCOM Market Breakdown

- 3.3. Global Maritime SATCOM NGSO Capacity Revenues ($M)

- 3.4. Global Maritime SATCOM NGSO Capacity Demand Breakdown

4. Appendix

- 4.1. Global

- 4.1.1. Global Maritime Market Retail Revenues (USD Billions)

- 4.1.2. Global Maritime Market In-Service Units

- 4.1.3. Global Maritime Market Capacity Demand

- 4.2. Merchant Forecast

- 4.2.1. In-Service Units, 2022 to 2032

- 4.2.2. Retail Revenues (USD Million), 2022 to 2032

- 4.2.3. Capacity Demand (FSS, GEO-HTS & NGSO)

- 4.2.4. Cumulative Capacity Revenues (USD Billions), '22 to '32

- 4.2.5. Capacity Revenues (USD Millions)

- 4.2.6. Regional In-Service Units

- 4.2.7. Regional Retail Revenues (USD Billions)

- 4.2.8. Regional Capacity Demand (FSS, GEO-HTS & NGSO)

- 4.3. Passenger Forecast

- 4.3.1. In-Service Units, 2022 to 2032

- 4.3.2. Retail Revenues (USD Million), 2022 to 2032

- 4.3.3. Capacity Demand (FSS, GEO-HTS & NGSO)

- 4.3.4. Cumulative Capacity Revenues (USD Billions), '22 to '32

- 4.3.5. Capacity Revenues (USD Millions)

- 4.3.6. Regional In-Service Units

- 4.3.7. Regional Retail Revenues (USD Billions)

- 4.3.8. Regional Capacity Demand (FSS, GEO-HTS & NGSO)

- 4.4. Offshore Forecast

- 4.4.1. In-Service Units, 2022 to 2032

- 4.4.2. Retail Revenues (USD Million), 2022 to 2032

- 4.4.3. Capacity Demand (FSS, GEO-HTS & NGSO)

- 4.4.4. Cumulative Capacity Revenues (USD Billions), '22 to '32

- 4.4.5. Capacity Revenues (USD Millions)

- 4.4.6. Regional In-Service Units

- 4.4.7. Regional Retail Revenues (USD Billions)

- 4.4.8. Regional Capacity Demand (FSS, GEO-HTS & NGSO)

- 4.5. Fishing Forecast

- 4.5.1. In-Service Units, 2022 to 2032

- 4.5.2. Retail Revenues (USD Million), 2022 to 2032

- 4.5.3. Capacity Demand (FSS, GEO-HTS & NGSO)

- 4.5.4. Cumulative Capacity Revenues (USD Billions), '22 to '32

- 4.5.5. Capacity Revenues (USD Millions)

- 4.5.6. Regional In-Service Units

- 4.5.7. Regional Retail Revenues (USD Billions)

- 4.5.8. Regional Capacity Demand (FSS, GEO-HTS & NGSO)

- 4.6. Leisure Forecast

- 4.6.1. In-Service Units, 2022 to 2032

- 4.6.2. Retail Revenues (USD Million), 2022 to 2032

- 4.6.3. Capacity Demand (FSS, GEO-HTS & NGSO)

- 4.6.4. Cumulative Capacity Revenues (USD Billions), '22 to '32

- 4.6.5. Capacity Revenues (USD Millions)

- 4.6.6. Regional In-Service Units

- 4.6.7. Regional Retail Revenues (USD Billions)

- 4.6.8. Regional Capacity Demand (FSS, GEO-HTS & NGSO)

亚太海事卫星市场:按国家分類的最终用户、服务、解决方案、分析和预测(2023-2033)

亚太海事卫星市场:按国家分類的最终用户、服务、解决方案、分析和预测(2023-2033) 欧洲海事卫星市场:按最终用户、按服务、按解决方案、按国家 - 分析和预测(2023-2033)

欧洲海事卫星市场:按最终用户、按服务、按解决方案、按国家 - 分析和预测(2023-2033) 海上卫星通讯的全球市场:趋势与预测 (2023~2033年)

海上卫星通讯的全球市场:趋势与预测 (2023~2033年) 2024年全球海事卫星通讯市场报告

2024年全球海事卫星通讯市场报告 全球海事卫星市场:全球和区域分析 - 按最终用户、按服务、按解决方案、按国家 - 分析和预测(2023-2033)

全球海事卫星市场:全球和区域分析 - 按最终用户、按服务、按解决方案、按国家 - 分析和预测(2023-2033) 海事卫星通讯市场 - 按类型(行动卫星服务、甚小孔径终端)、按产品、按应用、按最终用户、预测 2024 - 2032 年

海事卫星通讯市场 - 按类型(行动卫星服务、甚小孔径终端)、按产品、按应用、按最终用户、预测 2024 - 2032 年 全球海事卫星通讯市场:份额、规模、趋势、行业分析报告-按类型、按收入来源、按最终用途、按地区、细分市场预测,2023-2032年

全球海事卫星通讯市场:份额、规模、趋势、行业分析报告-按类型、按收入来源、按最终用途、按地区、细分市场预测,2023-2032年 海事卫星通讯市场 - 2018-2028 年全球产业规模、份额、趋势、机会和预测,按类型、产品、最终用户垂直、地区和竞争细分

海事卫星通讯市场 - 2018-2028 年全球产业规模、份额、趋势、机会和预测,按类型、产品、最终用户垂直、地区和竞争细分![海事卫星通讯市场:趋势、机会与竞争分析 [2023-2028]](/sample/img/cover/42/1342014.png) 海事卫星通讯市场:趋势、机会与竞争分析 [2023-2028]

海事卫星通讯市场:趋势、机会与竞争分析 [2023-2028]