|

市场调查报告书

商品编码

1721384

云端运算市场 (~2035年):部署模型·服务模式·解决方案·产业·主要各地区的产业趋势与全球预测Cloud Computing Market, Till 2035: Distribution by Type of Deployment Model, by Type of Service Model, by Type of Solution, by Type of Industry Vertical and Key Geographical Regions : Industry Trends and Global Forecasts |

||||||

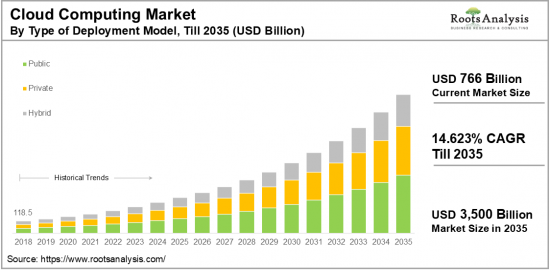

预计到 2035 年,全球云端运算市场规模将从目前的 7,660 亿美元成长至 3.5 兆美元,预测期内复合年增长率为 14.623%。

云端运算的市场机会:各市场区隔

按部署模型

- 混合云端

- 公共云端

- 私有云端

按服务模式

- Infrastructure as a Service (IaaS)

- Platform as a Service (PaaS)

- Software as a Service (SaaS)

各解决方案

- 云端备用

- 云端转移

- 云端协作

- 云端保全

- 云端储存

- 灾难復原

各业界

- BFSI (银行,金融服务,保险)

- 教育

- 政府机关

- 医疗保健

- IT·通讯

- 製造

- 媒体&娱乐

- 零售

- 其他

各服务供应商

- 世界的云端供应商

- 地区的云端供应商

各用途

- 商务流程管理

- 资料管理·分析

- 基础架构管理

- 保全·遵守

- 其他

各终端用户

- 企业

- 政府机关

- 个人

- 其他

按定价模式

- 计量型

- 订阅型

各技术

- AI

- 容器化

- 边缘运算

- 机器学习 (ML) 的整合

- 伺服器无运算

- 虚拟化

不同企业规模

- 大企业

- 中小企业

不同商业模式

- B2B

- B2C

- B2B2C

各地区

- 北美

- 美国

- 加拿大

- 墨西哥

- 其他的北美各国

- 欧洲

- 奥地利

- 比利时

- 丹麦

- 法国

- 德国

- 爱尔兰

- 义大利

- 荷兰

- 挪威

- 俄罗斯

- 西班牙

- 瑞典

- 瑞士

- 英国

- 其他欧洲各国

- 亚洲

- 中国

- 印度

- 日本

- 新加坡

- 韩国

- 其他亚洲各国

- 南美

- 巴西

- 智利

- 哥伦比亚

- 委内瑞拉

- 其他的南美各国

- 中东·北非

- 埃及

- 伊朗

- 伊拉克

- 以色列

- 科威特

- 沙乌地阿拉伯

- UAE

- 其他的中东·北非各国

- 全球其他地区

- 澳洲

- 纽西兰

- 其他的国家

云端运算市场:成长与趋势

云端运算产业是一个快速发展的领域,它透过采用尖端技术来改造传统的IT基础设施。该行业在提高各行各业的业务效率、营运改善和财务绩效方面发挥关键作用。

对灵活且经济的IT解决方案日益增长的需求,推动着企业从传统的本地部署系统转向基于云端的服务,以提高效率并降低营运成本。这种转变减少了对大规模实体硬体和维护的需求,使企业能够灵活地调整营运。此外,随着对数据驱动洞察和高品质数位服务的需求不断增长,企业正在积极采用云端运算解决方案,以帮助保持营运一致性并确保合规性。

本报告提供全球云端运算的市场调查、 市场概要,背景,市场影响因素的分析,市场规模的转变·预测,各种区分·各地区的详细分析,竞争情形,主要企业简介等资讯。

目录

第1章 序文

第2章 调查手法

第3章 经济以及其他的计划特有的考虑事项

第4章 宏观经济指标

第5章 摘要整理

第6章 简介

第7章 竞争情形

第8章 企业简介

- 章概要

- Adobe

- Alibaba

- Amazon

- Amazon

- Epicor

- Fujitsu

- IBM

- Cisco

- IFS

- Salesforce

- SAP

- Cloudflex

第9章 价值链分析

第10章 SWOT分析

第11章 全球云端运算市场

第12章 各部署模型的市场机会

第13章 各服务模式的市场机会

第14章 各解决方案的市场机会

第15章 各业界的市场机会

第16章 各服务供应商的市场机会

第17章 应用各领域的市场机会

第18章 各终端用户的市场机会

第19章 各价格设定模式的市场机会

第20章 各技术的市场机会

第21章 不同企业规模的市场机会

第22章 不同商业模式的市场机会

第23章 北美云端运算的市场机会

第24章 欧洲的云端运算的市场机会

第25章 亚洲的云端运算的市场机会

第26章 中东·北非的云端运算的市场机会

第27章 南美的云端运算的市场机会

第28章 全球其他地区的云端运算的市场机会

第29章 表格形式资料

第30章 企业·团体一览

第31章 客制化的机会

第32章 ROOTS订阅服务

第33章 着者详细内容

GLOBAL CLOUD COMPUTING MARKET: OVERVIEW

As per Roots Analysis, the global cloud computing market size is estimated to grow from USD 766 billion in the current year to USD 3,500 billion by 2035, at a CAGR of 14.623% during the forecast period, till 2035.

The opportunity for cloud computing market has been distributed across the following segments:

Type of Deployment Model

- Hybrid Cloud

- Public Cloud

- Private Cloud

Type of Service Model

- Infrastructure as a Service (IaaS)

- Platform as a Service (PaaS)

- Software as a Service (SaaS)

Type of Solution

- Cloud Backup

- Cloud Migration

- Cloud Orchestration

- Cloud Security

- Cloud Storage

- Disaster Recovery

Type of Industry Vertical

- BFSI (Banking, Financial Services, and Insurance)

- Education

- Government

- Healthcare

- IT & Telecommunications

- Manufacturing

- Media & Entertainment

- Retail

- Others

Type of Service Providers

- Global Cloud Providers

- Regional Cloud Providers

Area of Application

- Business Process Management

- Data Management and Analytics

- Infrastructure Management

- Security and Compliance

- Others

End User

- Enterprises

- Government Organizations

- Individual Users

- Others

Type of Pricing Model

- Pay-As-You-Go

- Subscription-Based

Type of Technology

- Artificial Intelligence (AI)

- Containerization

- Edge Computing

- Machine Learning (ML) Integration

- Serverless Computing

- Virtualization

Company Size

- Large Enterprises

- Small and Medium-sized Enterprises (SMEs)

Business Model

- B2B

- B2C

- B2B2C

Geographical Regions

- North America

- US

- Canada

- Mexico

- Other North American countries

- Europe

- Austria

- Belgium

- Denmark

- France

- Germany

- Ireland

- Italy

- Netherlands

- Norway

- Russia

- Spain

- Sweden

- Switzerland

- UK

- Other European countries

- Asia

- China

- India

- Japan

- Singapore

- South Korea

- Other Asian countries

- Latin America

- Brazil

- Chile

- Colombia

- Venezuela

- Other Latin American countries

- Middle East and North Africa

- Egypt

- Iran

- Iraq

- Israel

- Kuwait

- Saudi Arabia

- UAE

- Other MENA countries

- Rest of the World

- Australia

- New Zealand

- Other countries

CLOUD COMPUTING MARKET: GROWTH AND TRENDS

The cloud computing industry is a rapidly evolving field that transforms traditional IT frameworks by incorporating state-of-the-art technologies. This industry plays a crucial role in improving operations, efficiency, and financial performance for various business sectors. It includes a broad array of cloud offerings, such as infrastructure as a service (IaaS), platform as a service (PaaS), and software as a service (SaaS), all designed to enhance effectiveness and scalability while ensuring data protection and accessibility.

The growing need for adaptable and economical IT solutions has prompted a transition from conventional on-site systems to cloud-based services, boosting efficiency and reducing operational expenses. This transition reduces the necessity for substantial physical hardware and upkeep, enabling companies to adjust their operations flexibly. Additionally, the rising demand for data-driven insights and high-quality digital services encourages organizations to embrace cloud computing solutions, which aid in maintaining operational consistency and compliance with regulations.

Various firms are investing into the cloud computing sector, creating numerous opportunities; for example, in October 2023, Microsoft revealed a A$5 billion investment in computing capacity and capability to aid Australia in harnessing the AI era. However, the escalating costs of cloud services and potential security risks present challenges, especially for small and medium-sized enterprises (SMEs).Despite these obstacles, the market is experiencing remarkable growth due to opportunities for innovation and the emergence of advanced technologies, including Artificial General Intelligence (AGI) and the Internet of Things (IoT).

These advancements provide further opportunities for predictive analytics, improved security measures, and better decision-making abilities, suggesting that the global cloud computing market would grow at a healthy pace during the forecast period.

CLOUD COMPUTING MARKET: KEY SEGMENTS

Market Share by Type of Deployment Model

Based on the type of deployment model, the global cloud computing market is segmented into public cloud, private cloud, and hybrid cloud deployment models. According to our estimates, currently, public cloud segment captures the majority share of the market. Businesses can take advantage of lower infrastructure expenses and the capability to swiftly adjust resources according to demand, making it appealing for organizations of all sizes.

Moreover, the widespread usage of software-as-a-service (SaaS) and infrastructure-as-a-service (IaaS) offerings further accelerates the expansion of the public cloud sector. However, hybrid cloud segment is anticipated to grow at a higher CAGR during the forecast period.

Market Share by Type of Service Model

Based on the type of service model, the cloud computing market is segmented into service (IaaS), platform as a service (PaaS), and software as a service (SaaS). According to our estimates, currently, software as a service (SaaS) segment captures the majority share of the market. This can be attributed to its widespread use across different sectors, offering cost-effectiveness, scalability, and easy access. Organizations prefer SaaS for its easy deployment and limited requirement for IT infrastructure, making it suitable for applications such as CRM, ERP, and collaborative tools.

Market Share by Type of Solution

Based on the type of solution, the cloud computing market is segmented into cloud backup, cloud migration, cloud orchestration, cloud security, cloud storage, and disaster recovery. According to our estimates, currently, cloud storage segment captures the majority share of the market. This can be attributed to the rapid increase in data and the demand for scalable, economical storage options.

Both businesses and individuals are increasingly turning to cloud storage for its ease of access, versatility, and capacity to manage large data volumes without substantial infrastructure costs. Moreover, cloud storage services play a pivotal role in enabling other cloud solutions, assisting with backup, disaster recovery, and migration tasks.

Market Share by Type of Industry Vertical

Based on the type of industry vertical, the cloud computing market is segmented into industry verticals, including BFSI (Banking, Financial Services, and Insurance), education, government, healthcare, IT & telecommunications, manufacturing, media & entertainment, retail, and others. According to our estimates, currently, IT & telecommunications segment captures the majority share of the market further, this segment is anticipated to grow at a higher CAGR in the future.

This can be attributed its critical requirement for adaptable and scalable infrastructure capable of handling large amounts of data processing, storage, and intricate applications. The early adoption of cloud technologies in this sector to enhance operational efficiency, lower costs, and improve service delivery reinforces its top status.

Market Share by Type of Service Providers

Based on type of service providers, the cloud computing market is segmented into global cloud providers and regional cloud providers. According to our estimates, currently, global cloud segment captures the majority share of the market. Major players like Amazon Web Services (AWS), Microsoft Azure, and Google Cloud hold a leading position in this sector. Their dominance stems from their vast infrastructure, wide-ranging service offerings, and capacity to cater to a global clientele. Their substantial investments in data centers, cutting-edge technology, and customer support enhance reliability, scalability, and performance, making them the top choice for businesses in need of strong and flexible cloud solutions.

Market Share by Area of Application

Based on area of application, the cloud computing market is segmented into business process management, data management and analytics, infrastructure management, security and compliance, and others. According to our estimates, currently, Data management and analytics segment captures the majority share of the market. This can be attributed to the increasing demand for actionable insights from large data sets. This is followed by the market share captured by security and compliance segment, owing to the need for strong data protection and adherence to regulations.

Market Share by End User

Based on end user, the cloud computing market is segmented into enterprises, government organizations, individual users, and others. According to our estimates, currently, enterprise segment captures the majority share of the market. This can be attributed to their demand for scalable solutions that boost productivity, collaboration, and data management. Government entities come in next, motivated by the need for secure, compliant, and effective infrastructure. This is followed by the market share captured by government organizations segment.

Market Share by Type of Pricing Model

Based on type of pricing model, the cloud computing market is segmented into pay-as-you-go and subscription-based models. According to our estimates, currently, pay-as-you-go model captures the majority share of the market. This can be attributed to its flexibility and cost efficiency, enabling businesses to pay solely for the resources they utilize, which is particularly appealing for variable workloads.

Market Share by Type of Technology

Based on type of technology, the cloud computing market is segmented into artificial intelligence, containerization, edge computing, machine learning integration, serverless computing, and virtualization. According to our estimates, currently, artificial intelligent segment captures the majority share of the market. This can be attributed to its capacity to enhance decision-making and automate processes across diverse industries, leading to a notable demand for cloud-based AI solutions.

Market Share by Company Size

Based on the company, the cloud computing market is segmented into large size companies and small and mid-size companies. According to our estimates, currently, large companies captures the majority share of the market. This can be attributed to necessary resources and capabilities to invest significantly in research and development, manufacturing infrastructure, and marketing, allowing them to offer cloud computing services at a lower cost per unit in comparison to smaller rivals. Moreover, there are cost-effective and high-quality cloud computing options available for medium and small enterprises.

Market Share by Business Model

Based on the business model, the cloud computing market is segmented into B2B, B2C and B2B2C. According to our estimates, currently, B2B segment captures the majority share of the market. This can be attributed to the growing use of cloud computing technology across various industries, including aerospace, manufacturing, healthcare, finance, and more. Additionally, the B2C model is predicted to experience significant growth at a robust CAGR during this forecast period as cloud computing technologies become increasingly user-friendly, and consumers are adopting these solutions for personalized applications, smartphone integration, and enhanced user experiences.

Market Share by Geographical Regions

Based on the geographical regions, the cloud computing market is segmented into North America, Europe, Asia, Latin America, Middle East and North Africa, and Rest of the World. According to our estimates, currently, North America captures the majority share of the market. This can be attributed to the presence of major technology companies that have created a strong ecosystem for innovation and development. This region is marked by significant advancements in cloud technologies, including artificial intelligence, machine learning, and big data analytics, which fuel demand for cloud services across diverse sectors. Moreover, considerable investments from both governmental and private entities in digital infrastructure and security enhance the cloud computing environment.

Example Players in Cloud Computing Market

- Adobe

- Alibaba Cloud

- Amazon Web Services

- App Maisters

- Box

- CenturyLink

- Cisco

- Citrix

- Cloudflex

- Cloudways

- DigitalOcean

- DXC Technology

- Epicor

- Fujitsu

- IBM

- Infor

- Intuit

- IFS

- JDV Technologies

- Joyent

- Microsoft

- Navisite

- NEC

- OpenText

- Oracle

- OVH

- pCloud

- Rackspace

- Sage

- Salesforce

- SAP

- ServiceNow

- Skytap

- Tencent Cloud

- Tudip Technologies

- Upland Software

- Visartech

- VMware

- Vultr

- Workday

- Zoho

- Zymr

CLOUD COMPUTING MARKET: RESEARCH COVERAGE

The report on the cloud computing market features insights on various sections, including:

- Market Sizing and Opportunity Analysis: An in-depth analysis of the cloud computing market, focusing on key market segments, including [A] type of deployment model, [B] type of service model, [C] type of solution, [D] type of industry vertical, [E] type of service providers, [F] area of application, [G] end user, [H] type of pricing mode [I] type of technology, [J] company size, [K] business model and [L] geographical regions

- Competitive Landscape: A comprehensive analysis of the companies engaged in the Cloud computing market, based on several relevant parameters, such as [A] year of establishment, [B] company size, [C] location of headquarters, [D] ownership structure.

- Company Profiles: Elaborate profiles of prominent players engaged in the Cloud computing market, providing details on [A] location of headquarters, [B]company size, [C] company mission, [D] company footprint, [E] management team, [F] contact details, [G] financial information, [H] operating business segments, [I] Cloud computing portfolio, [J] moat analysis, [K] recent developments, and an informed future outlook.

- SWOT Analysis: An insightful SWOT framework, highlighting the strengths, weaknesses, opportunities and threats in the domain. Additionally, it provides Harvey ball analysis, highlighting the relative impact of each SWOT parameter.

KEY QUESTIONS ANSWERED IN THIS REPORT

- How many companies are currently engaged in cloud computing market?

- Which are the leading companies in this market?

- What is the significance of edge AI in the cloud computing market?

- What factors are likely to influence the evolution of this market?

- What is the current and future market size?

- What is the CAGR of this market?

- How is the current and future market opportunity likely to be distributed across key market segments?

- Which type of cloud computing is expected to dominate the market?

REASONS TO BUY THIS REPORT

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. By analyzing the competitive landscape, businesses can make informed decisions to optimize their market positioning and develop effective go-to-market strategies.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

ADDITIONAL BENEFITS

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 10% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

1. PREFACE

- 1.1. Introduction

- 1.2. Market Share Insights

- 1.3. Key Market Insights

- 1.4. Report Coverage

- 1.5. Key Questions Answered

- 1.6. Chapter Outlines

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Introduction

- 2.4.2.2. Types

- 2.4.2.2.1. Qualitative

- 2.4.2.2.2. Quantitative

- 2.4.2.3. Advantages

- 2.4.2.4. Techniques

- 2.4.2.4.1. Interviews

- 2.4.2.4.2. Surveys

- 2.4.2.4.3. Focus Groups

- 2.4.2.4.4. Observational Research

- 2.4.2.4.5. Social Media Interactions

- 2.4.2.5. Stakeholders

- 2.4.2.5.1. Company Executives (CXOs)

- 2.4.2.5.2. Board of Directors

- 2.4.2.5.3. Company Presidents and Vice Presidents

- 2.4.2.5.4. Key Opinion Leaders

- 2.4.2.5.5. Research and Development Heads

- 2.4.2.5.6. Technical Experts

- 2.4.2.5.7. Subject Matter Experts

- 2.4.2.5.8. Scientists

- 2.4.2.5.9. Doctors and Other Healthcare Providers

- 2.4.2.6. Ethics and Integrity

- 2.4.2.6.1. Research Ethics

- 2.4.2.6.2. Data Integrity

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

3. ECONOMIC AND OTHER PROJECT SPECIFIC CONSIDERATIONS

- 3.1. Forecast Methodology

- 3.1.1. Top-Down Approach

- 3.1.2. Bottom-Up Approach

- 3.1.3. Hybrid Approach

- 3.2. Market Assessment Framework

- 3.2.1. Total Addressable Market (TAM)

- 3.2.2. Serviceable Addressable Market (SAM)

- 3.2.3. Serviceable Obtainable Market (SOM)

- 3.2.4. Currently Acquired Market (CAM)

- 3.3. Forecasting Tools and Techniques

- 3.3.1. Qualitative Forecasting

- 3.3.2. Correlation

- 3.3.3. Regression

- 3.3.4. Time Series Analysis

- 3.3.5. Extrapolation

- 3.3.6. Convergence

- 3.3.7. Forecast Error Analysis

- 3.3.8. Data Visualization

- 3.3.9. Scenario Planning

- 3.3.10. Sensitivity Analysis

- 3.4. Key Considerations

- 3.4.1. Demographics

- 3.4.2. Market Access

- 3.4.3. Reimbursement Scenarios

- 3.4.4. Industry Consolidation

- 3.5. Robust Quality Control

- 3.6. Key Market Segmentations

- 3.7. Limitations

4. MACRO-ECONOMIC INDICATORS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Overview of Major Currencies Affecting the Market

- 4.2.2.2. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Exchange Impact

- 4.2.3.1. Evaluation of Foreign Exchange Rates and Their Impact on Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.4.2. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.6. Interest Rates

- 4.2.6.1. Overview of Interest Rates and Their Impact on the Market

- 4.2.6.2. Strategies for Managing Interest Rate Risk

- 4.2.7. Commodity Flow Analysis

- 4.2.7.1. Type of Commodity

- 4.2.7.2. Origins and Destinations

- 4.2.7.3. Values and Weights

- 4.2.7.4. Modes of Transportation

- 4.2.8. Global Trade Dynamics

- 4.2.8.1. Import Scenario

- 4.2.8.2. Export Scenario

- 4.2.9. War Impact Analysis

- 4.2.9.1. Russian-Ukraine War

- 4.2.9.2. Israel-Hamas War

- 4.2.10. COVID Impact / Related Factors

- 4.2.10.1. Global Economic Impact

- 4.2.10.2. Industry-specific Impact

- 4.2.10.3. Government Response and Stimulus Measures

- 4.2.10.4. Future Outlook and Adaptation Strategies

- 4.2.11. Other Indicators

- 4.2.11.1. Fiscal Policy

- 4.2.11.2. Consumer Spending

- 4.2.11.3. Gross Domestic Product (GDP)

- 4.2.11.4. Employment

- 4.2.11.5. Taxes

- 4.2.11.6. R&D Innovation

- 4.2.11.7. Stock Market Performance

- 4.2.11.8. Supply Chain

- 4.2.11.9. Cross-Border Dynamics

- 4.2.1. Time Period

5. EXECUTIVE SUMMARY

6. INTRODUCTION

- 6.1. Chapter Overview

- 6.2. Overview of Cloud Computing Market

- 6.2.1. Key Characteristics of Cloud Computing Market

- 6.2.2. Type of Deployment Mode

- 6.2.3. Type of Cloud Computing

- 6.2.4. Type of Component

- 6.2.5. Type of Provider

- 6.2.6. Stage of Deployment

- 6.2.7. Type of Offering

- 6.2.8. Area of Application

- 6.2.9. Type of Platform

- 6.2.10. Type of End User

- 6.3. Future Perspective

7. COMPETITIVE LANDSCAPE

- 7.1. Chapter Overview

- 7.2. Cloud Computing: Overall Market Landscape

- 7.2.1. Analysis by Year of Establishment

- 7.2.2. Analysis by Company Size

- 7.2.3. Analysis by Location of Headquarters

- 7.2.4. Analysis by Ownership Structure

8. COMPANY PROFILES

- 8.1. Chapter Overview

- 8.2. Adobe

- 8.2.1. Company Overview

- 8.2.2. Company Mission

- 8.2.3. Company Footprint

- 8.2.4. Management Team

- 8.2.5. Contact Details

- 8.2.6. Financial Performance

- 8.2.7. Operating Business Segments

- 8.2.8. Service / Product Portfolio (project specific)

- 8.2.9. MOAT Analysis

- 8.2.10. Recent Developments and Future Outlook

- Similar detail is presented for other below mentioned companies based on information in the public domain

- 8.3. Alibaba

- 8.4. Amazon

- 8.5. Amazon

- 8.6. Epicor

- 8.7. Fujitsu

- 8.8. IBM

- 8.9. Google

- 8.10. Cisco

- 8.11. IFS

- 8.12. Salesforce

- 8.13. SAP

- 8.14. Cloudflex

9. VALUE CHAIN ANALYSIS

10. SWOT ANALYSIS

11. GLOBAL CLOUD COMPUTING MARKET

- 11.1. Chapter Overview

- 11.2. Key Assumptions and Methodology

- 11.3. Trends Disruption Impacting Market

- 11.4. Global Cloud Computing Market, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 11.5. Multivariate Scenario Analysis

- 11.5.1. Conservative Scenario

- 11.5.2. Optimistic Scenario

- 11.6. Key Market Segmentations

12. MARKET OPPORTUNITIES BASED ON TYPE OF DEPLOYMENT MODE

- 12.1. Chapter Overview

- 12.2. Key Assumptions and Methodology

- 12.3. Revenue Shift Analysis

- 12.4. Market Movement Analysis

- 12.5. Penetration-Growth (P-G) Matrix

- 12.6. Cloud Computing Market for Hybrid Cloud: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 12.7. Cloud Computing Market for Private Cloud: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 12.8. Cloud Computing Market for Public Cloud: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 12.9. Data Triangulation and Validation

13. MARKET OPPORTUNITIES BASED ON TYPE OF SERVICE MODEL

- 13.1. Chapter Overview

- 13.2. Key Assumptions and Methodology

- 13.3. Revenue Shift Analysis

- 13.4. Market Movement Analysis

- 13.5. Penetration-Growth (P-G) Matrix

- 13.6. Cloud Computing Market for IaaS: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 13.7. Cloud Computing Market for PaaS: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 13.8. Cloud Computing Market for SaaS: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 13.9. Data Triangulation and Validation

14. MARKET OPPORTUNITIES BASED ON TYPE OF SOLUTION

- 14.1. Chapter Overview

- 14.2. Key Assumptions and Methodology

- 14.3. Revenue Shift Analysis

- 14.4. Market Movement Analysis

- 14.5. Penetration-Growth (P-G) Matrix

- 14.6. Cloud Computing Market for Cloud Backup: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 14.7. Cloud Computing Market for Cloud Migration: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 14.8. Cloud Computing Market for Cloud Orchestration: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 14.9. Cloud Computing Market for Cloud Security: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 14.10. Cloud Computing Market for Cloud Storage: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 14.11. Cloud Computing Market for Disaster Recovery: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 14.12. Data Triangulation and Validation

15. MARKET OPPORTUNITIES BASED ON TYPE OF INDUSTRY VERTICAL

- 15.1. Chapter Overview

- 15.2. Key Assumptions and Methodology

- 15.3. Revenue Shift Analysis

- 15.4. Market Movement Analysis

- 15.5. Penetration-Growth (P-G) Matrix

- 15.6. Cloud Computing Market for BFSI: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 15.7. Cloud Computing Market for Education: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 15.8. Cloud Computing Market for Government: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 15.9. Cloud Computing Market for Healthcare: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 15.10. Cloud Computing Market for IT & Telecommunications: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 15.11. Cloud Computing Market for Manufacturing: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 15.12. Cloud Computing Market for Media & Entertainment: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 15.13. Cloud Computing Market for Retail: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 15.14. Cloud Computing Market for Others: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 15.15. Data Triangulation and Validation

16. MARKET OPPORTUNITIES BASED ON TYPE OF SERVICE PROVIDERS

- 16.1. Chapter Overview

- 16.2. Key Assumptions and Methodology

- 16.3. Revenue Shift Analysis

- 16.4. Market Movement Analysis

- 16.5. Penetration-Growth (P-G) Matrix

- 16.6. Cloud Computing Market for Global Cloud Providers: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 16.7. Cloud Computing Market for Regional Cloud Providers: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 16.8. Data Triangulation and Validation

17. MARKET OPPORTUNITIES BASED ON AREA OF APPLICATION

- 17.1. Chapter Overview

- 17.2. Key Assumptions and Methodology

- 17.3. Revenue Shift Analysis

- 17.4. Market Movement Analysis

- 17.5. Penetration-Growth (P-G) Matrix

- 17.6. Cloud Computing Market for Business Process Management: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 17.7. Cloud Computing Market for Data Management and Analytics: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 17.8. Cloud Computing Market for Infrastructure Management: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 17.9. Cloud Computing Market for Security and Compliance: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 17.10. Cloud Computing Market for Others: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 17.11. Data Triangulation and Validation

18. MARKET OPPORTUNITIES BASED ON END USER

- 18.1. Chapter Overview

- 18.2. Key Assumptions and Methodology

- 18.3. Revenue Shift Analysis

- 18.4. Market Movement Analysis

- 18.5. Penetration-Growth (P-G) Matrix

- 18.6. Cloud Computing Market for Enterprises: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 18.7. Cloud Computing Market for Government Organizations: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 18.8. Cloud Computing Market for Individual Users: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 18.9. Cloud Computing Market for Others: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 18.10. Data Triangulation and Validation

19. MARKET OPPORTUNITIES BASED ON TYPE OF PRICING MODEL

- 19.1. Chapter Overview

- 19.2. Key Assumptions and Methodology

- 19.3. Revenue Shift Analysis

- 19.4. Market Movement Analysis

- 19.5. Penetration-Growth (P-G) Matrix

- 19.6. Cloud Computing Market for Pay-As-You-Go: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.7. Cloud Computing Market for Subscription-Based: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.8. Data Triangulation and Validation

20. MARKET OPPORTUNITIES BASED ON TYPE OF TECHNOLOGY

- 20.1. Chapter Overview

- 20.2. Key Assumptions and Methodology

- 20.3. Revenue Shift Analysis

- 20.4. Market Movement Analysis

- 20.5. Penetration-Growth (P-G) Matrix

- 20.6. Cloud Computing Market for Artificial Intelligence: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 20.7. Cloud Computing Market for Containerization: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 20.8. Cloud Computing Market for Edge Computing: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 20.9. Cloud Computing Market for Machine Learning Integration: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 20.10. Cloud Computing Market for Serverless Computing: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 20.11. Cloud Computing Market for Virtualization: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 20.12. Data Triangulation and Validation

21. MARKET OPPORTUNITIES BASED ON COMPANY SIZE

- 21.1. Chapter Overview

- 21.2. Key Assumptions and Methodology

- 21.3. Revenue Shift Analysis

- 21.4. Market Movement Analysis

- 21.5. Penetration-Growth (P-G) Matrix

- 21.6. Cloud Computing Market for Large Enterprises: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.7. Cloud Computing Market for Small and Medium-sized Enterprises (SMEs): Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.8. Data Triangulation and Validation

22. MARKET OPPORTUNITIES BASED ON BUSINESS MODEL

- 22.1. Chapter Overview

- 22.2. Key Assumptions and Methodology

- 22.3. Revenue Shift Analysis

- 22.4. Market Movement Analysis

- 22.5. Penetration-Growth (P-G) Matrix

- 22.6. Cloud Computing Market for B2B: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.7. Cloud Computing Market for B2C: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.8. Cloud Computing Market for B2B2C: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.9. Data Triangulation and Validation

23. MARKET OPPORTUNITIES FOR CLOUD COMPUTING IN NORTH AMERICA

- 23.1. Chapter Overview

- 23.2. Key Assumptions and Methodology

- 23.3. Revenue Shift Analysis

- 23.4. Market Movement Analysis

- 23.5. Penetration-Growth (P-G) Matrix

- 23.6. Cloud Computing Market in North America: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.1. Cloud Computing Market in the US: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.2. Cloud Computing Market in Canada: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.3. Cloud Computing Market in Mexico: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.4. Cloud Computing Market in Other North American Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.7. Data Triangulation and Validation

24. MARKET OPPORTUNITIES FOR CLOUD COMPUTING IN EUROPE

- 24.1. Chapter Overview

- 24.2. Key Assumptions and Methodology

- 24.3. Revenue Shift Analysis

- 24.4. Market Movement Analysis

- 24.5. Penetration-Growth (P-G) Matrix

- 24.6. Cloud Computing Market in Europe: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.1. Cloud Computing Market in the Austria: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.2. Cloud Computing Market in Belgium: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.3. Cloud Computing Market in Denmark: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.4. Cloud Computing Market in France: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.5. Cloud Computing Market in Germany: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.6. Cloud Computing Market in Ireland: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.7. Cloud Computing Market in Italy: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.8. Cloud Computing Market in Netherlands: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.9. Cloud Computing Market in Norway: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.10. Cloud Computing Market in Russia: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.11. Cloud Computing Market in Spain: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.12. Cloud Computing Market in Sweden: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.13. Cloud Computing Market in Switzerland: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.14. Cloud Computing Market in the UK: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.15. Cloud Computing Market in Other European Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.7. Data Triangulation and Validation

25. MARKET OPPORTUNITIES FOR CLOUD COMPUTING IN ASIA

- 25.1. Chapter Overview

- 25.2. Key Assumptions and Methodology

- 25.3. Revenue Shift Analysis

- 25.4. Market Movement Analysis

- 25.5. Penetration-Growth (P-G) Matrix

- 25.6. Cloud Computing Market in Asia: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.1. Cloud Computing Market in China: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.2. Cloud Computing Market in India: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.3. Cloud Computing Market in Japan: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.4. Cloud Computing Market in Singapore: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.5. Cloud Computing Market in South Korea: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.6. Cloud Computing Market in Other Asian Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.7. Data Triangulation and Validation

26. MARKET OPPORTUNITIES FOR CLOUD COMPUTING IN MIDDLE EAST AND NORTH AFRICA (MENA)

- 26.1. Chapter Overview

- 26.2. Key Assumptions and Methodology

- 26.3. Revenue Shift Analysis

- 26.4. Market Movement Analysis

- 26.5. Penetration-Growth (P-G) Matrix

- 26.6. Cloud Computing Market in Middle East and North Africa (MENA): Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.1. Cloud Computing Market in Egypt: Historical Trends (Since 2019) and Forecasted Estimates (Till 205)

- 26.6.2. Cloud Computing Market in Iran: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.3. Cloud Computing Market in Iraq: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.4. Cloud Computing Market in Israel: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.5. Cloud Computing Market in Kuwait: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.6. Cloud Computing Market in Saudi Arabia: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.7. Cloud Computing Market in United Arab Emirates (UAE): Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.8. Cloud Computing Market in Other MENA Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.7. Data Triangulation and Validation

27. MARKET OPPORTUNITIES FOR CLOUD COMPUTING IN LATIN AMERICA

- 27.1. Chapter Overview

- 27.2. Key Assumptions and Methodology

- 27.3. Revenue Shift Analysis

- 27.4. Market Movement Analysis

- 27.5. Penetration-Growth (P-G) Matrix

- 27.6. Cloud Computing Market in Latin America: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.6.1. Cloud Computing Market in Argentina: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.6.2. Cloud Computing Market in Brazil: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.6.3. Cloud Computing Market in Chile: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.6.4. Cloud Computing Market in Colombia Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.6.5. Cloud Computing Market in Venezuela: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.6.6. Cloud Computing Market in Other Latin American Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.7. Data Triangulation and Validation

28. MARKET OPPORTUNITIES FOR CLOUD COMPUTING IN REST OF THE WORLD

- 28.1. Chapter Overview

- 28.2. Key Assumptions and Methodology

- 28.3. Revenue Shift Analysis

- 28.4. Market Movement Analysis

- 28.5. Penetration-Growth (P-G) Matrix

- 28.6. Cloud Computing Market in Rest of the World: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 28.6.1. Cloud Computing Market in Australia: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 28.6.2. Cloud Computing Market in New Zealand: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 28.6.3. Cloud Computing Market in Other Countries

- 28.7. Data Triangulation and Validation

29. TABULATED DATA

30. LIST OF COMPANIES AND ORGANIZATIONS

31. CUSTOMIZATION OPPORTUNITIES

32. ROOTS SUBSCRIPTION SERVICES

33. AUTHOR DETAIL

2026-2030年全球政府部门云端运算市场

2026-2030年全球政府部门云端运算市场 日本云端运算市场,2026-2030年

日本云端运算市场,2026-2030年 2025年全球自託管云端平台市场报告

2025年全球自託管云端平台市场报告 云端运算市场规模、份额和趋势分析:按服务、部署类型、工作负载、企业规模、最终用途、地区和细分市场预测(2026-2033 年)

云端运算市场规模、份额和趋势分析:按服务、部署类型、工作负载、企业规模、最终用途、地区和细分市场预测(2026-2033 年) 云端运算市场-全球产业规模、份额、趋势、机会和预测,按服务、部署方式、应用程式类型、最终用户、地区和竞争格局划分,2020-2030 年预测

云端运算市场-全球产业规模、份额、趋势、机会和预测,按服务、部署方式、应用程式类型、最终用户、地区和竞争格局划分,2020-2030 年预测 云端运算市场:按服务、部署方式、企业规模、工作负载、最终用途、技术类型、国家划分 - 全球产业分析、市场规模、市场份额及2025-2032年预测

云端运算市场:按服务、部署方式、企业规模、工作负载、最终用途、技术类型、国家划分 - 全球产业分析、市场规模、市场份额及2025-2032年预测 云端运算:全球市场份额和排名、总收入和需求预测(2025-2031 年)

云端运算:全球市场份额和排名、总收入和需求预测(2025-2031 年) 云端运算和储存市场按服务类型、云端服务组件、部署模式、组织规模和最终用户行业划分 - 全球预测 2025-2032云端运算市场:2025-2032 年全球预测(按服务模式、部署模式、组织规模、产业和应用)工业IoT市场中的云端运算(按服务模式、部署模式、连接类型、应用程式和最终用户产业)-全球预测,2025-2032

云端运算和储存市场按服务类型、云端服务组件、部署模式、组织规模和最终用户行业划分 - 全球预测 2025-2032云端运算市场:2025-2032 年全球预测(按服务模式、部署模式、组织规模、产业和应用)工业IoT市场中的云端运算(按服务模式、部署模式、连接类型、应用程式和最终用户产业)-全球预测,2025-2032