|

市场调查报告书

商品编码

1723656

基因编辑市场 - 各技术,治疗类别,遗传基因编辑方法,各基因转移方法,各基因转移种模式,各应用领域,终端用户类别,主要加入企业:2035年前的产业趋势与全球预测Genome Editing Market - Focus on Technology, Type of Therapy, Gene Editing Approach, Type of Gene Delivery Method, Gene Delivery Modality, Application Area, Type of End-User and Leading Industry Players: Industry Trends and Global Forecasts, till 2035 |

||||||

基因组编辑市场:概览

2024 年全球基因组编辑市场规模为 34.1 亿美元。预计在预测期内,该市场将以 12.1% 的复合年增长率成长,从目前的 42.5 亿美元增至 2035 年的 133.6 亿美元。

基因组编辑市场机会分布在以下几个领域:

采用的付款方式

- 契约退职金

- 里程金

遗传基因编辑技术类型

- CRISPR-Cas系统

- TALENs

- Meganucleases

- ZFN系

- 其他技术

遗传基因编辑方法

- 遗传基因基因剔除

- 遗传基因敲门界内

基因转移法

- 生物外

- 体内

基因转移方法

- 病毒载体

- 非病毒性媒介

治疗类型

- 细胞治疗

- 基因治疗

- 其他的治疗方法

应用领域

- 药物研发与开发

- 诊断药

终端用户

- 製药公司及生物科技企业

- 学术·研究机关

主要地区

- 北美(美国,加拿大)

- 欧洲(德国,法国,爱尔兰)

- 亚太地区(韩国,中国,日本)

基因组编辑市场:成长与趋势

人类基因组由约 30 亿个碱基对组成,包含 20,000-25,000 个蛋白质编码基因。这些基因充当密码子,调控蛋白质的合成,进而影响基因表现。生物技术领域的不断进步使得各种医学研究人员能够透过称为基因组编辑或基因组工程的专门技术来修改人类基因组的表达。基因组编辑,也称为基因编辑,是一种透过插入、删除或替换单一基因或一组基因来修改生物体基因组的技术,从而改变核苷酸组成。由于对特定位点进行基因组编辑的需求日益增长,参与该领域的公司开发了各种基因组编辑工具。主要技术包括锌指核酸酶 (ZFN)、转录活化因子样效应核酸酶 (TALEN) 和 CRISPR 技术。值得注意的是,ZFN 是 1895 年发现的第一个基因组工程技术,随后 TALEN(2011 年)和 CRISPR 成为基因组编辑领域的里程碑式突破。这些基因编辑工具已广泛应用于治疗由基因异常引起的各种临床疾病,例如镰状细胞疾病、帕金森氏症、週边动脉疾病、脊髓性肌肉萎缩症、自体免疫疾病和其他遗传性疾病。

此外,基因治疗已成为一种有前景的治疗方法,透过将治疗基因导入细胞或替换突变基因来解决潜在的基因异常问题。截至 2024 年 4 月,有超过 1,100 项正在进行的临床试验,研究处于不同开发阶段的基因疗法。根据世界卫生组织统计,全球每1,000人中就有10人患有遗传性疾病,影响超过7,000万人。此外,全球超过40%的婴儿死亡与各种遗传性疾病有关。儘管重组药物潜力巨大,但其开发需要在药物发现、开发和生产方面投入大量资金。因此,为了确保这些药物的高效、精准和安全地给药,製药公司扩大采用先进的基因组编辑技术。因此,人们越来越重视整合尖端技术,透过精准的基因改造来改善临床疗效。

基因组编辑领域持续的技术创新,加上细胞和基因治疗领域令人鼓舞的临床试验结果,正在推动该行业向前发展。此外,基因编辑在农业和粮食安全领域的应用不断扩展,进一步推动了市场成长。

基因组编辑市场:关键洞察

本报告深入探讨了基因组编辑市场的现状,并识别了行业内的潜在成长机会。报告的主要内容包括:

近85%的技术使用CRISPR-Cas技术,其中近30%能够将CRISPR工具直接递送到细胞中,主要用于药物研发和再生医学。

近年来,合作伙伴关係稳定成长,技术授权协议成为最主要的合作模式。

各种技术开发者已提交并授予超过 2,400 项与基因组编辑相关的专利,以保护该领域产生的智慧财产权。

- 为了获得丰厚的回报,许多公私投资者自 2018 年以来已投资相当于 141 亿美元的资金,该领域的融资活动遍布不同地区。

- 预计未来十年基因组编辑技术市场将以每年 12.1% 的速度成长。

- 基因治疗领域预计将在治疗类型方面实现显着成长,因为製药和生物技术公司正在开发的技术预计将带来最大的市场机会。

基因组编辑市场:关键细分市场

根据采用的付款方式,全球基因组编辑市场分为预付款和里程碑付款。目前,该细分市场在整个市场中占据最高占有率。然而,值得注意的是,里程碑付款细分市场预计在预测期内将显着增长。

根据基因编辑技术类型,全球基因组编辑市场细分为 CRISPR-Cas 系统、TALEN、大范围核酸酶、ZFN 等。目前,CRISPR-Cas 系统在基因组编辑市场中占据主导地位。值得一提的是,这一趋势在未来不太可能改变。这一趋势的出现归因于下一代 CRISPR 技术,它透过提供更客製化和精准的结果,克服了传统基因编辑技术的局限性。

根据基因编辑方法,全球基因组编辑市场细分为基因敲入和基因敲除。目前,基因敲除方法的收入占据市场主导地位。这可以归因于与基因敲入方法相比,这种方法更具可行性和可及性,因为基因敲入方法需要复杂的最佳化过程。

根据基因转移方法,全球基因组编辑市场细分为体外和体内。目前,体外基因编辑占据基因组编辑市场的最大占有率。这是因为在体外基因转移中,细胞从患者体内取出,在实验室中进行修饰,然后再重新导入体内。这使得在实验室中精确控制基因修饰,同时最大限度地减少相关的脱靶效应。然而,在预测期内,体内基因编辑市场可能会以相对更高的复合年增长率成长。

以基因转殖方式划分,全球基因组编辑市场分为病毒载体与非病毒载体。目前,病毒载体在基因组编辑市场中占有最高占有率。然而,由于使用病毒载体作为基因转移方式存在各种课题(例如细胞毒性、免疫原性和规模化问题),预计未来几年这一趋势将发生变化,非病毒载体在整个市场中将占据几乎相同的占有率。

依治疗类型划分,全球基因组编辑市场分为细胞治疗、基因治疗和其他治疗。目前,细胞治疗领域占据最大的市场占有率。此外,鑑于其在多种疾病治疗中的广泛应用,这一趋势未来不太可能改变。

按应用细分,全球基因组编辑市场分为药物发现和市场开发以及诊断。目前,药物发现和开发领域占据了大部分市场占有率。

按最终用户细分,全球基因组编辑市场分布在製药和生技公司、学术和研究机构之间。值得注意的是,製药和生物技术领域占据了基因组编辑市场的大部分占有率。这是因为製药和生物技术公司在该领域签订了最多的技术许可/整合协议,因此贡献了行业参与者的大部分收入。

依主要地区细分,市场分为北美、欧洲和亚太地区。目前,北美占据最大的市场占有率。此外,值得注意的是,预计欧洲在预测期内将以相对较高的复合年增长率成长。

报告中解答的关键问题

- 目前有多少家公司进入该市场?

- 谁是该市场的主要参与者?

- 哪些因素可能影响该市场的发展?

- 目前和未来的市场规模是多少?

- 该市场的复合年增长率是多少?

- 当前和未来的市场机会在主要细分市场中如何分配?

为什么要购买此报告?

- 本报告提供全面的市场分析,并针对整体市场和特定细分市场提供详细的收入预测。这些资讯对于成熟的市场领导者和新进入者都极具价值。

- 利害关係人可以利用本报告更深入了解市场中的竞争动态。透过分析竞争格局,企业可以优化市场定位并制定有效的市场进入策略。为了帮助利害关係人做出明智的决策,本报告提供了全面的市场概览,包括关键推动因素、阻碍因素和课题。这些资讯使利害关係人能够掌握市场趋势,并做出基于数据的决策,从而掌握成长前景。

更多优势

- PPT 洞察包

- 报告所有分析模组免费提供 Excel 资料包

- 10% 免费内容客製化

- 由我们的研究团队提供详细的报告讲解

- 如果报告发布时间超过 6-12 个月,可免费更新报告

本报告提供全球基因编辑市场相关调查,提供市场概要,以及各技术,治疗类别,遗传基因编辑方法,各基因转移方法,各基因转移种模式,各应用领域,终端用户类别,按主要加入企业趋势,及加入此市场的主要企业简介等资讯。

目录

章节I:报告概要

第1章 背景

第2章 调查手法

第3章 市场动态

第4章 宏观经济指标

章节II:定性性的洞察

第5章 摘要整理

第6章 简介

- 章概要

- 遗传基因编辑简介

- 基因编辑技术的应用

- 其他的新兴技术

- 结论

章节III:竞争情形

第7章 市场形势基因编辑技术

- 章概要

- 基因编辑:技术形势

- 基因编辑:技术供应商的形势

第8章 技术竞争力分析

- 章概要

- 前提/主要参数

- 调查手法

- 技术竞争力分析

章节IV: 企业简介

第9章 基因编辑市场:北美为据点的企业简介

- 章概要

- Arcturus Therapeutics

- Arsenal Bio

- Beam Therapeutics

- Caribou Biosciences

- Century Therapeutics

- CRISPR Therapeutics

- Editas Medicine

- Intellia Therapeutics

- Prime Medicine

- Vor Biopharma

第10章 基因编辑市场:欧洲为据点的企业简介

- 章概要

- Avectas

- Bio-Sourcing

- Flash Therapeutics

- Ntrans Technologies

- OXGENE(Acquired by WuXi AppTec)

- Revvity(formerly known as Horizon Discovery)

第11章 基因编辑市场:亚太地区及其他地区为据点的企业简介

- 章概要

- Edigene

- Fortgen

- G+FLAS Life Sciences

- TargetGene Biotechnologies

章节V: 市场趋势

第12章 伙伴关係和合作

- 章概要

- 伙伴关係模式

- 基因编辑技术:伙伴关係和合作

第13章 专利分析

- 章概要

- 范围调查手法

- 基因编辑领域:专利分析

- 基因编辑领域:专利基准分析

- 专利评估分析

第14章 资金筹措与投资分析

- 章概要

- 资金筹措模式

- 基因编辑市场:资金筹措与投资分析

- 结论

章节VI:市场机会分析

第15章 市场影响分析:促进因素,阻碍因素,机会,课题

- 章概要

- 市场促进因素

- 市场阻碍因素

- 市场机会

- 市场课题

- 结论

第16章 基因编辑技术市场

- 章概要

- 前提调查手法

- 基因编辑技术市场:2035年前的预测

- 主要的市场区隔

第17章 基因编辑技术市场(付款方式)

第18章 基因编辑技术市场(遗传基因编辑各技术类型)

第19章 基因编辑技术市场(遗传基因编辑方法)

第20章 基因编辑技术市场(各基因转移方法)

第21章 基因编辑技术市场(各基因转移种模式)

第22章 基因编辑技术市场(治疗类别)

第23章 基因编辑技术市场(各应用领域)

第24章 基因编辑技术市场(各终端用户)

第25章 基因编辑技术市场(主要各地区)

第26章 基因编辑技术市场:主要产业的参与企业

章节VII:其他的垄断的洞察

第27章 结论

第28章 执行洞察

章节VIII: 附录

第29章 附录1表格形式资料

第30章 附录2企业·团体一览

GENOME EDITING MARKET: OVERVIEW

As per Roots Analysis, the global genome editing market size is currently valued at USD 3.41 billion in 2024, is projected to reach USD 4.25 billion in the current year and USD 13.36 billion by 2035, growing at a CAGR of 12.1% during the forecast period.

The opportunity for genome editing market has been distributed across the following segments:

Payment Method Employed

- Upfront Payments

- Milestone Payments

Type of Gene Editing Technique

- CRISPR-Cas System

- TALENs

- Meganucleases

- ZFNs

- Other Techniques

Gene Editing Approach

- Gene Knock-out

- Gene Knock-in

Gene Delivery Methods

- Ex vivo

- In vivo

Gene Delivery Modality

- Viral Vectors

- Non-Viral Vectors

Type of Therapy

- Cell Therapies

- Gene Therapies

- Other Therapies

Application Area

- Drug Discovery and Development

- Diagnostics

Type of End-User

- Pharmaceutical and Biotechnology Companies

- Academic and Research Institutes

Key Geographical Regions

- North America (US, Canada)

- Europe (Germany, France and Ireland)

- Asia-Pacific (South Korea, China and Japan)

GENOME EDITING MARKET: GROWTH AND TRENDS

The human genome comprises nearly three billion nucleotide base pairs, which contain ~20,000-25,000 protein-coding genes. These genes act as a code that regulates and controls protein synthesis, thereby influencing gene expression. The ongoing advancements in the biotechnology domain have enabled various medical researchers to modify human genome expression through specialized techniques called genome editing or genome engineering. Genome editing, also known as gene editing, is a technique that allows genome modification by inserting, deleting or replacing a single gene or a set of genes in an organism, thereby altering the nucleotide composition. The growing need for genome editing at the desired site has led to the development of various genome editing tools by companies engaged in this domain. Key technologies include zinc finger nucleases (ZFNs), transcription activator-like effector nucleases (TALENs) and CRISPR technology. Notably, ZFN was the first genome engineering technique discovered in 1895, followed by TALENs (in 2011) and CRISPR, which emerged as a transformative breakthrough in the genome editing domain. These gene editing tools have been widely used for the treatment of various clinical conditions developed as a result of genetic abnormalities, such as sickle cell disease, Parkinson's disease, peripheral artery disease, spinal muscular atrophy, autoimmune diseases, and other genetic disorders.

Moreover, gene therapies have gained prominence as a promising approach to addressing the underlying genetic abnormalities by introducing therapeutic genes into the cells or by replacing mutated genes. As of April 2024, over 1,100 active clinical trials are investigating gene therapies at various stages of development. According to the WHO, 10 out of every 1,000 individuals suffer from genetic disorders, affecting more than 70 million people worldwide. Further, more than 40% of infant mortality globally is associated with various genetic disorders. Despite its potential, gene edited drug development requires substantial investment in drug discovery, development, and manufacturing. Therefore, in order to ensure the efficiency, precision and safe delivery of these drugs, pharmaceutical companies are increasingly adopting advanced genome editing technologies. As a result, there is a growing emphasis on integrating cutting-edge technologies to enhance clinical outcomes through precise genetic modifications.

The ongoing pace of innovation in the genome editing domain, coupled with the promising clinical trial results in cell and gene therapies are driving the industry forward. Additionally, the expanding applications of gene editing in agriculture and food security are further propelling the market growth.

GENOME EDITING MARKET: KEY INSIGHTS

The report delves into the current state of the genome editing market and identifies potential growth opportunities within the industry. The key takeaways of the report are:

Close to 85% of technologies use CRISPR-Cas technique; of these, nearly 30% enable the delivery of the CRISPR tool directly into the cells, primarily utilized for drug discovery and regenerative medicine.

A steady growth in partnership activity has been observed in recent years; technology licensing agreements have emerged as the most prominent type of partnership model.

Over 2,400 patents related to genome editing have been filed by / granted to various technology developers in order to protect the intellectual property generated within this field.

- Foreseeing lucrative returns, many public and private investors have made investments worth USD 14.1 billion since 2018; the funding activity in this domain is well distributed across different geographical regions.

- The genome editing technologies market is anticipated to witness an annualized growth rate of 12.1% over the next decade.

- The market opportunity for technologies being developed for pharmaceutical and biotechnology companies is likely to be the highest; in terms of type of therapy, gene therapy segment is anticipated to grow substantially.

GENOME EDITING MARKET: KEY SEGMENTS

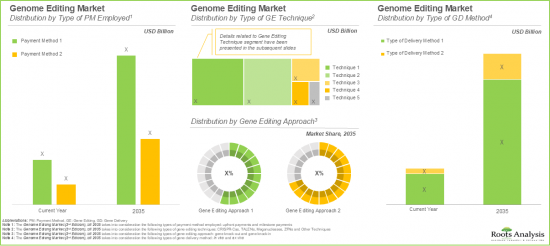

Based on the type of Payment Mode Employed, Upfront Payments Captures the Majority of the Current Market Share

Based on the type of payment method employed, the global genome editing market is segmented into upfront payments and milestone payments. Presently, the upfront payment segment occupies the highest share of the overall market. However, it is important to note that the milestone payment segment is anticipated to witness significant growth during the forecast period.

CRISPR-Cas System is Likely to Hold the Largest Share in the Genome Editing Market During the Forecast Period

Based on the type of gene editing techniques, the global genome editing market is segmented into CRISPR-Cas Systems, TALENs, Meganucleases, ZFNs, and others. Currently, CRISP-Case systems segment leads the genome editing market. Further, it is important to highlight that this trend is unlikely to change in the future as well. This trend can be attributed to the fact that next-generation CRISPR technologies have emerged as a promising technique to overcome the limitations associated with conventional gene editing techniques, by offering more customized and precise results.

Genome Editing Market for Gene Knock-out is Likely to Grow at a Relatively Faster Pace During the Forecast Period

Based on the type of gene editing approach, the global genome editing market is segmented across gene knock-in and gene knock-out approaches. Presently, the market is dominated by the revenues generated through gene knock-out approach. This can be attributed to the greater feasibility and accessibility of this approach, in comparison to knock-in approach, since knock-in approaches require a complex optimization process.

Genome Editing Market for In-vivo is Likely to Grow at a Higher CAGR During the Forecast Period

Based on the gene delivery method, the global genome editing market is segmented into ex-vivo and in-vivo. Currently, the ex-vivo segment captures the maximum share of the genome editing market. This can be attributed to the fact that in ex vivo gene delivery, cells are taken from the patient, modified in the lab and then reintroduced into the body. This allows precise control over the genetic modification in a lab setting, while minimizing the associated off-target effects. However, the in-vivo segment is likely to grow at a relatively higher CAGR during the forecast period.

Viral Vectors are Likely to Dominate the Genome Editing Market During the Forecast Period

Based on the gene delivery modality, the global genome editing market is distributed across viral vectors and non-viral vectors. Presently, the viral vector segment occupies the highest share of the genome editing market. However, due to various challenges associated with the use of viral vectors as gene modality (such as cytotoxicity, immunogenicity and scale-up issues), this trend is anticipated to change in the coming years, with non-viral vectors occupying an approximately equal market share in the overall market.

Cell Therapies Hold the Largest Share in the Genome Editing Market

Based on the type of therapy, the global genome editing market is segmented into cell therapies, gene therapies, and others. Presently, the cell therapies segment accounts for the largest market share. Additionally, owing to its wider applicability in treating a wide array of diseases this trend is unlikely to change in the future as well.

Drug Discovery and Development Hold the Largest Share in the Genome Editing Market

Based on the application area, the global genome editing market is segmented into drug discovery and development, and diagnostics. Currently, drug discovery and development segment capture the majority of the market share.

Revenues Generated from Pharmaceutical and Biotechnology Companies are Likely to Dominate the Genome Editing Market During the Forecast Period

Based on the end-user, the global genome editing market is distributed across pharmaceutical and biotechnology companies, and academic and research institutions. Notably, the pharmaceutical and biotechnology segment captures the majority of the genome editing market. This is due to the fact that pharmaceutical and biotechnology companies have signed maximum technology licensing / integration agreements in this domain, thus contributing to the majority of the revenue generated by industry players.

North America Accounts for the Largest Share in the Market

Based on key geographical regions, the market is segmented into North America, Europe, and Asia Pacific. In the current scenario, North America is likely to capture the largest market share. Further, it is worth highlighting that Europe is expected to grow at a relatively high CAGR during the forecast period.

Example Players in the Genome Editing Market

- Arcturus Therapeutics

- ArsenalBio

- Avectas

- Beam Therapeutics

- Bio-Sourcing

- Caribou Biosciences

- Century Therapeutics

- CRISPR Therapeutics

- Editas Medicine

- Flash Biosolutions

- Graphite Bio

- Intellia Therapeutics

- NTrans Technologies

- OXGENE

- Prime Medicine

- Revvity

- Vor Biopharma

GENOME EDITING MARKET: RESEARCH COVERAGE

The report on the genome editing market features insights into various sections, including:

- Market Sizing and Opportunity Analysis: An in-depth analysis of current market opportunity and the future growth potential of genome editing market, focusing on key market segments, including [A] payment method employed, [B] type of gene editing technique, [C] gene editing approach, [D] gene delivery methods, [E] gene delivery modality, [F] type of therapy, [G] application area, [H] type of end-user, [I] key geographical regions, and [J] leading industry players.

- Market Impact Analysis: A thorough analysis of various factors, such as [A] drivers, [B] restraints, [C] opportunities, and [D] existing challenges that are likely to impact market growth.

- Market Landscape: A comprehensive evaluation of genome editing technologies, based on several relevant parameters, such as [A] type of gene editing technique, [B] type of gene editing approach, [C] type of gene delivery method, [D] type of gene delivery modality, [E] highest phase of drug development supported, [F] therapeutic area, and [G] application area.

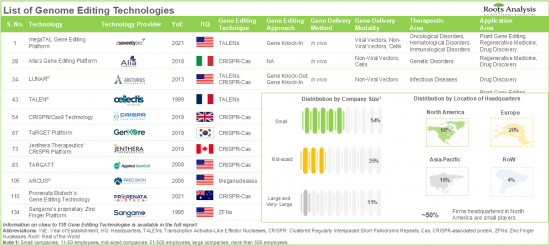

- Genome Editing Technology Providers Landscape: The report features a list of technology providers engaged in the genome editing domain, along with analyses based on [A] year of establishment, [B] company size, and [C] location of headquarters, [D] most active players, and [E] operational model.

- Technology Competitiveness Analysis: An insightful competitiveness analysis of the genome technologies in this domain, based on various relevant parameters, such as [A] company strength, and [B] technology strength.

- Company Profiles: Comprehensive profiles of key industry players in the genome editing domain based in regions, such as North America, Europe, and Asia-Pacific and rest of the world, featuring information on [A] company overview, [B] financial information (if available), [C] technology portfolio, [D] recent developments, and [E] future outlook statements.

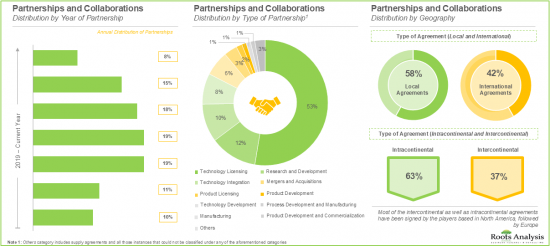

- Partnerships and Collaborations: A detailed analysis of partnerships inked between stakeholders in the genome editing market, since 2018, based on several relevant parameters, such as [A] year of partnership, [B] type of partnership, [C] purpose of partnership, [D] type of partner, [E] location of headquarters of partner, [F] most active players (in terms of number of partnerships), and [G] geography.

- Patent Analysis: An in-depth analysis of various patents that have been filed / granted by various technology providers related to genome editing, since 2018, based on various relevant parameters, such as [A] type of patent, [B] publication year, [C] geography, [D] CPC symbols, [E] leading industry players (in terms of number of patents), [F] patent benchmarking, [G] patent characteristics, [H] leading industry players, and [I] patent valuation.

- Funding and Investments Analysis: A detailed analysis of the various funding and investments raised in the genome editing domain, based on several relevant parameters, such as [A] year of funding, [B] amount of funding, [C] type of funding, [D] geography, [E] most active players (in terms of number of funding instances), and [F] leading investors.

KEY QUESTIONS ANSWERED IN THIS REPORT

- How many companies are currently engaged in this market?

- Which are the leading companies in this market?

- What factors are likely to influence the evolution of this market?

- What is the current and future market size?

- What is the CAGR of this market?

- How is the current and future market opportunity likely to be distributed across key market segments?

REASONS TO BUY THIS REPORT

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. By analyzing the competitive landscape, businesses can make informed decisions to optimize their market positioning and develop effective go-to-market strategies.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

ADDITIONAL BENEFITS

- Complimentary PPT Insights Packs

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 10% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

SECTION I: REPORT OVERVIEW

1. BACKGROUND

- 1.1. Context

- 1.2. Project Objectives

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.2.1. Market Landscape and Market Trends

- 2.2.2. Market Forecast and Opportunity Analysis

- 2.2.3. Comparative Analysis

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Types of Primary Research

- 2.4.2.1.1. Qualitative Research

- 2.4.2.1.2. Quantitative Research

- 2.4.2.1.3. Hybrid Approach

- 2.4.2.2. Advantages of Primary Research

- 2.4.2.3. Techniques for Primary Research

- 2.4.2.3.1. Interviews

- 2.4.2.3.2. Surveys

- 2.4.2.3.3. Focus Groups

- 2.4.2.3.4. Observational Research

- 2.4.2.3.5. Social Media Interactions

- 2.4.2.4. Key Opinion Leaders Considered in Primary Research

- 2.4.2.4.1. Company Executives (CXOs)

- 2.4.2.4.2. Board of Directors

- 2.4.2.4.3. Company Presidents and Vice Presidents

- 2.4.2.4.4. Research and Development Heads

- 2.4.2.4.5. Technical Experts

- 2.4.2.4.6. Subject Matter Experts

- 2.4.2.4.7. Scientists

- 2.4.2.4.8. Doctors and Other Healthcare Providers

- 2.4.2.5. Ethics and Integrity

- 2.4.2.5.1. Research Ethics

- 2.4.2.5.2. Data Integrity

- 2.4.2.1. Types of Primary Research

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

- 2.5. Robust Quality Control

3. MARKET DYNAMICS

- 3.1. Chapter Overview

- 3.2. Forecast Methodology

- 3.2.1. Top-down Approach

- 3.2.2. Bottom-up Approach

- 3.2.3. Hybrid Approach

- 3.3. Market Assessment Framework

- 3.3.1. Total Addressable Market (TAM)

- 3.3.2. Serviceable Addressable Market (SAM)

- 3.3.3. Serviceable Obtainable Market (SOM)

- 3.3.4. Currently Acquired Market (CAM)

- 3.4. Forecasting Tools and Techniques

- 3.4.1. Qualitative Forecasting

- 3.4.2. Correlation

- 3.4.3. Regression

- 3.4.4. Extrapolation

- 3.4.5. Convergence

- 3.4.6. Sensitivity Analysis

- 3.4.7. Scenario Planning

- 3.4.8. Data Visualization

- 3.4.9. Time Series Analysis

- 3.4.10. Forecast Error Analysis

- 3.5. Key Considerations

- 3.5.1. Demographics

- 3.5.2. Government Regulations

- 3.5.3. Reimbursement Scenarios

- 3.5.4. Market Access

- 3.5.5. Supply Chain

- 3.5.6. Industry Consolidation

- 3.5.7. Pandemic / Unforeseen Disruptions Impact

- 3.6. Limitations

4. MACRO-ECONOMIC INDICATORS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Major Currencies Affecting the Market

- 4.2.2.2. Factors Affecting Currency Fluctuations on the Industry

- 4.2.2.3. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Currency Exchange Rate

- 4.2.3.1. Impact of Foreign Exchange Rate Volatility on the Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.4.2. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.6. Interest Rates

- 4.2.6.1. Interest Rates and Their Impact on the Market

- 4.2.6.2. Strategies for Managing Interest Rate Risk

- 4.2.7. Commodity Flow Analysis

- 4.2.7.1. Type of Commodity

- 4.2.7.2. Origins and Destinations

- 4.2.7.3. Values and Weights

- 4.2.7.4. Modes of Transportation

- 4.2.8. Global Trade Dynamics

- 4.2.8.1. Import Scenario

- 4.2.8.2. Export Scenario

- 4.2.8.3. Trade Policies

- 4.2.8.4. Strategies for Mitigating the Risks Associated with Trade Barriers

- 4.2.8.5. Impact of Trade Barriers on the Market

- 4.2.9. War Impact Analysis

- 4.2.9.1. Russian-Ukraine War

- 4.2.9.2. Israel-Hamas War

- 4.2.10. COVID Impact / Related Factors

- 4.2.10.1. Global Economic Impact

- 4.2.10.2. Industry-specific Impact

- 4.2.10.3. Government Response and Stimulus Measures

- 4.2.10.4. Future Outlook and Adaptation Strategies

- 4.2.11. Other Indicators

- 4.2.11.1. Fiscal Policy

- 4.2.11.2. Consumer Spending

- 4.2.11.3. Gross Domestic Product

- 4.2.11.4. Employment

- 4.2.11.5. Taxes

- 4.2.11.6. Stock Market Performance

- 4.2.11.7. Cross Border Dynamics

- 4.2.1. Time Period

- 4.3. Conclusion

SECTION II: QUALITATIVE INSIGHTS

5. EXECUTIVE SUMMARY

6. INTRODUCTION

- 6.1. Chapter Overview

- 6.2. Introduction to Gene Editing

- 6.2.1. Evolution of Gene Editing

- 6.2.2. Gene Editing Technologies

- 6.2.2.1. CRISPR - CAS System

- 6.2.2.2. Transcription Activator-Like Effector Nucleases (TALENs)

- 6.2.2.3. Zinc Finger Nucleases (ZFNs)

- 6.2.2.4. Meganucleases / Homing Endonucleases

- 6.3. Applications of Genome Editing Technologies

- 6.4. Other Emerging Technologies

- 6.5. Concluding Remarks

SECTION III: COMPETITIVE LANDSCAPE

7. MARKET LANDSCAPE: GENOME EDITING TECHNOLOGIES

- 7.1. Chapter Overview

- 7.2. Genome Editing: Technology Landscape

- 7.2.1. Analysis by Type of Gene Editing Technique

- 7.2.2. Analysis by Type of Gene Editing Approach

- 7.2.3. Analysis by Type of Gene Delivery Method

- 7.2.4. Analysis by Type of Gene Delivery Modality

- 7.2.5. Analysis by Highest Phase of Drug Development Supported

- 7.2.6. Analysis by Therapeutic Area

- 7.2.7. Analysis by Application Area

- 7.3. Genome Editing: Technology Providers Landscape

- 7.3.1. Analysis by Year of Establishment

- 7.3.2. Analysis by Company Size

- 7.3.3. Analysis by Location of Headquarters

- 7.3.4. Analysis by Company Size and Location of Headquarters

- 7.3.5. Most Active Players: Analysis by Number of Technologies

- 7.3.6. Analysis by Operational Model

8. TECHNOLOGY COMPETITIVENESS ANALYSIS

- 8.1. Chapter Overview

- 8.2. Assumptions / Key Parameters

- 8.3. Methodology

- 8.4. Technology Competitiveness Analysis

- 8.4.1. Genome Editing Technologies Offered by Players Headquartered in North America

- 8.4.2. Genome Editing Technologies Offered by Players Headquartered in Europe

- 8.4.3. Genome Editing Technologies Offered by Players Headquartered in Asia-Pacific, Middle East and North Africa, and Latin America

SECTION IV: COMPANY PROFILES

9. GENOME EDITING MARKET: COMPANY PROFILES OF PLAYERS BASED IN NORTH AMERICA

- 9.1. Chapter Overview

- 9.2. Arcturus Therapeutics

- 9.2.1. Company Overview

- 9.2.2. Financial Information

- 9.2.3. Technology Portfolio

- 9.2.4. Recent Developments and Future Outlook

- 9.3. Arsenal Bio

- 9.3.1. Company Overview

- 9.3.2. Technology Portfolio

- 9.3.3. Recent Developments and Future Outlook

- 9.4. Beam Therapeutics

- 9.4.1. Company Overview

- 9.4.2. Financial Information

- 9.4.3. Technology Portfolio

- 9.4.4. Recent Developments and Future Outlook

- 9.5. Caribou Biosciences

- 9.5.1. Company Overview

- 9.5.2. Financial Information

- 9.5.3. Technology Portfolio

- 9.5.4. Recent Developments and Future Outlook

- 9.6. Century Therapeutics

- 9.6.1. Company Overview

- 9.6.2. Financial Information

- 9.6.3. Technology Portfolio

- 9.6.4. Recent Developments and Future Outlook

- 9.7. CRISPR Therapeutics

- 9.7.1. Company Overview

- 9.7.2. Financial Information

- 9.7.3. Technology Portfolio

- 9.7.4. Recent Developments and Future Outlook

- 9.8. Editas Medicine

- 9.8.1. Company Overview

- 9.8.2. Financial Information

- 9.8.3. Technology Portfolio

- 9.8.4. Recent Developments and Future Outlook

- 9.9. Intellia Therapeutics

- 9.9.1. Company Overview

- 9.9.2. Financial Information

- 9.9.3. Technology Portfolio

- 9.9.4. Recent Developments and Future Outlook

- 9.10. Prime Medicine

- 9.10.1. Company Overview

- 9.10.2. Technology Portfolio

- 9.10.3. Recent Developments and Future Outlook

- 9.11. Vor Biopharma

- 9.11.1. Company Overview

- 9.11.2. Technology Portfolio

- 9.11.3. Recent Developments and Future Outlook

10. GENOME EDITING MARKET: COMPANY PROFILES OF PLAYERS BASED IN EUROPE

- 10.1. Chapter Overview

- 10.2. Avectas

- 10.2.1. Company Overview

- 10.2.2. Technology Portfolio

- 10.3. Bio-Sourcing

- 10.3.1. Company Overview

- 10.3.2. Technology Portfolio

- 10.4. Flash Therapeutics

- 10.4.1. Company Overview

- 10.4.2. Technology Portfolio

- 10.5. Ntrans Technologies

- 10.5.1. Company Overview

- 10.5.2. Technology Portfolio

- 10.6. OXGENE (Acquired by WuXi AppTec)

- 10.6.1. Company Overview

- 10.6.2. Technology Portfolio

- 10.7. Revvity (formerly known as Horizon Discovery)

- 10.7.1. Company Overview

- 10.7.2. Technology Portfolio

11. GENOME EDITING MARKET: COMPANY PROFILES OF PLAYERS BASED IN ASIA-PACIFIC AND REST OF THE WORLD

- 11.1. Chapter Overview

- 11.2. Edigene

- 11.2.1. Company Overview

- 11.2.2. Technology Portfolio

- 11.3. Fortgen

- 11.3.1. Company Overview

- 11.3.2. Technology Portfolio

- 11.4. G+FLAS Life Sciences

- 11.4.1. Company Overview

- 11.4.2. Technology Portfolio

- 11.5. TargetGene Biotechnologies

- 11.5.1. Company Overview

- 11.5.2. Technology Portfolio

SECTION V: MARKET TRENDS

12. PARTNERSHIPS AND COLLABORATIONS

- 12.1. Chapter Overview

- 12.2. Partnership Models

- 12.3. Genome Editing Technologies: Partnerships and Collaborations

- 12.3.1. Analysis by Year of Partnership

- 12.3.2. Analysis by Type of Partnership

- 12.3.3. Analysis by Year and Type of Partnership

- 12.3.4. Analysis by Purpose of Partnership

- 12.3.5. Analysis by Type of Partner

- 12.3.6. Analysis by Location of Headquarters of Partner

- 12.3.7. Most Active Players: Analysis by Number of Partnerships

- 12.3.8. Analysis by Geography

- 12.3.8.1. Local and International Agreements

- 12.3.8.2. Intercontinental and Intracontinental Agreements

13. PATENT ANALYSIS

- 13.1. Chapter Overview

- 13.2. Scope and Methodology

- 13.3. Genome Editing Domain: Patent Analysis

- 13.3.1. Analysis by Publication Year

- 13.3.2. Analysis by Type of Patent and Publication Year

- 13.3.3. Analysis by Geography

- 13.3.4. Analysis by CPC Symbols

- 13.3.5. Leading Industry Players: Analysis by Number of Patents

- 13.4. Genome Editing Domain: Patent Benchmarking Analysis

- 13.4.1. Analysis by Patent Characteristics

- 13.4.2. Analysis by Leading Industry Players

- 13.5. Patent Valuation Analysis

14. FUNDING AND INVESTMENT ANALYSIS

- 14.1. Chapter Overview

- 14.2. Funding Models

- 14.3. Genome Editing Market: Funding and Investment Analysis

- 14.3.1. Analysis by Year of Funding

- 14.3.1.1. Cumulative Year-wise Trend of Funding Instances

- 14.3.1.2. Cumulative Year-wise Trend of Amount Invested

- 14.3.2. Analysis by Type of Funding

- 14.3.2.1. Analysis by Funding Instances

- 14.3.2.2. Analysis by Amount Invested

- 14.3.3. Analysis by Year and Type of Funding

- 14.3.4. Analysis by Geography

- 14.3.5. Most Active Players: Analysis by Amount Invested and Number of Funding Instances

- 14.3.6. Leading Investors: Analysis by Number of Funding Instances

- 14.3.1. Analysis by Year of Funding

- 14.4. Concluding Remarks

SECTION VI: MARKET OPPORTUNITY ANALYSIS

15. MARKET IMPACT ANALYSIS: DRIVERS, RESTRAINTS, OPPORTUNITIES AND CHALLENGES

- 15.1. Chapter Overview

- 15.2. Market Drivers

- 15.3. Market Restraints

- 15.4. Market Opportunities

- 15.5. Market Challenges

- 15.6. Conclusion

16. GENOME EDITING TECHNOLOGIES MARKET

- 16.1. Chapter Overview

- 16.2. Assumptions and Methodology

- 16.3. Genome Editing Technologies Market: Forecasted Estimates, till 2035

- 16.3.1. Scenario Analysis

- 16.3.1.1. Conservative Scenario

- 16.3.1.2. Optimistic Scenario

- 16.3.1. Scenario Analysis

- 16.4. Key Market Segmentations

17. GENOME EDITING TECHNOLOGIES MARKET, BY TYPE OF PAYMENT METHOD EMPLOYED

- 17.1. Chapter Overview

- 17.2. Key Assumptions and Methodology

- 17.3. Genome Editing Technologies Market: Distribution by Type of Payment Method Employed

- 17.3.1. Genome Editing Technologies Market for Milestone Payments: Forecasted Estimates, till 2035

- 17.3.2. Genome Editing Technologies Market for Upfront Payments: Forecasted Estimates, till 2035

- 17.4. Data Triangulation

18. GENOME EDITING TECHNOLOGIES MARKET, BY TYPE OF GENE EDITING TECHNIQUE

- 18.1. Chapter Overview

- 18.2. Key Assumptions and Methodology

- 18.3. Genome Editing Technologies Market: Distribution by Type of Gene Editing Technique

- 18.3.1. Genome Editing Technologies Market for CRISPR-Cas System: Forecasted Estimates, till 2035

- 18.3.2. Genome Editing Technologies Market for TALENs: Forecasted Estimates, till 2035

- 18.3.3. Genome Editing Technologies Market for Meganucleases: Forecasted Estimates, till 2035

- 18.3.4. Genome Editing Technologies Market for ZFNs: Forecasted Estimates, till 2035

- 18.3.5. Genome Editing Technologies Market for Other Techniques: Forecasted Estimates, till 2035

- 18.4. Data Triangulation

19. GENOME EDITING TECHNOLOGIES MARKET, BY GENE EDITING APPROACH

- 19.1. Chapter Overview

- 19.2. Key Assumptions and Methodology

- 19.3. Genome Editing Technologies Market: Distribution by Gene Editing Approach

- 19.3.1. Genome Editing Technologies Market for Gene Knock-Out Approaches: Forecasted Estimates, till 2035

- 19.3.2. Genome Editing Technologies Market for Gene Knock-In Approaches: Forecasted Estimates, till 2035

- 19.4. Data Triangulation

20. GENOME EDITING TECHNOLOGIES MARKET, BY GENE DELIVERY METHOD

- 20.1. Chapter Overview

- 20.2. Key Assumptions and Methodology

- 20.3. Genome Editing Technologies Market: Distribution by Gene Delivery Method

- 20.3.1. Genome Editing Technologies Market for Ex Vivo Delivery Methods: Forecasted Estimates, till 2035

- 20.3.2. Genome Editing Technologies Market for In Vivo Delivery Methods: Forecasted Estimates, till 2035

- 20.4. Data Triangulation

21. GENOME EDITING TECHNOLOGIES MARKET, BY GENE DELIVERY MODALITY

- 21.1. Chapter Overview

- 21.2. Key Assumptions and Methodology

- 21.3. Genome Editing Technologies Market: Distribution by Gene Delivery Modality

- 21.3.1. Genome Editing Technologies Market for Viral Vectors: Forecasted Estimates, till 2035

- 21.3.2. Genome Editing Technologies Market for Non-Viral Vectors: Forecasted Estimates, till 2035

- 21.4. Data Triangulation

22. GENOME EDITING TECHNOLOGIES MARKET, BY TYPE OF THERAPY

- 22.1. Chapter Overview

- 22.2. Key Assumptions and Methodology

- 22.3. Genome Editing Technologies Market: Distribution by Type of Therapy

- 22.3.1. Genome Editing Technologies Market for Cell Therapies: Forecasted Estimates, till 2035

- 22.3.2. Genome Editing Technologies Market for Gene Therapies: Forecasted Estimates, till 2035

- 22.3.3. Genome Editing Technologies Market for Other Therapies: Forecasted Estimates, till 2035

- 22.4. Data Triangulation

23. GENOME EDITING TECHNOLOGIES MARKET, BY APPLICATION AREA

- 23.1. Chapter Overview

- 23.2. Key Assumptions and Methodology

- 23.3. Genome Editing Technologies Market: Distribution by Application Area

- 23.3.1. Genome Editing Technologies Market for Drug Discovery and Development: Forecasted Estimates, till 2035

- 23.3.2. Genome Editing Technologies Market for Diagnostics: Forecasted Estimates, till 2035

- 23.4. Data Triangulation

24. GENOME EDITING TECHNOLOGIES MARKET, BY TYPE OF END USER

- 24.1. Chapter Overview

- 24.2. Key Assumptions and Methodology

- 24.3. Genome Editing Technologies Market: Distribution by Type of End User

- 24.3.1. Genome Editing Technologies Market for Pharmaceutical and Biotechnology Companies: Forecasted Estimates, till 2035

- 24.3.2. Genome Editing Technologies Market for Academic and Research Institutes: Forecasted Estimates, till 2035

- 24.4. Data Triangulation

25. GENOME EDITING TECHNOLOGIES MARKET, BY KEY GEOGRAPHICAL REGIONS

- 25.1. Chapter Overview

- 25.2. Key Assumptions and Methodology

- 25.3. Genome Editing Technologies Market: Distribution by Key Geographical Regions

- 25.3.1. Genome Editing Technologies Market in North America: Forecasted Estimates, till 2035

- 25.3.1.1. Genome Editing Technologies Market in the US: Forecasted Estimates, till 2035

- 25.3.1.2. Genome Editing Technologies Market in Canada: Forecasted Estimates, till 2035

- 25.3.2. Genome Editing Technologies Market in Europe: Forecasted Estimates, till 2035

- 25.3.2.1. Genome Editing Technologies Market in Germany: Forecasted Estimates, till 2035

- 25.3.2.2. Genome Editing Technologies Market in France: Forecasted Estimates, till 2035

- 25.3.2.3. Genome Editing Technologies Market in Ireland: Forecasted Estimates, till 2035

- 25.3.3. Genome Editing Technologies Market in Asia-Pacific: Forecasted Estimates, till 2035

- 25.3.3.1. Genome Editing Technologies Market in South Korea: Forecasted Estimates, till 2035

- 25.3.3.2. Genome Editing Technologies Market in China: Forecasted Estimates, till 2035

- 25.3.3.3. Genome Editing Technologies Market in Japan: Forecasted Estimates, till 2035

- 25.3.1. Genome Editing Technologies Market in North America: Forecasted Estimates, till 2035

- 25.4. Market Dynamics Assessment

- 25.4.1. Penetration Growth (P-G) Matrix

- 25.5. Data Triangulation

26. GENOME EDITING TECHNOLOGIES MARKET: LEADING INDUSTRY PLAYERS

- 26.1. Chapter Overview

- 26.2. Leading Industry Players

SECTION VII: OTHER EXCLUSIVE INSIGHTS

27. CONCLUDING INSIGHTS

28. EXECUTIVE INSIGHTS

SECTION VIII: APPENDICES

29. APPENDIX 1: TABULATED DATA

30. APPENDIX 2: LIST OF COMPANIES AND ORGANIZATIONS

List of Tables

- Table 7.1 List of Genome Editing Technologies

- Table 7.2 Genome Editing Technologies: Information on Type of Gene Editing Technique

- Table 7.3 Genome Editing Technologies: Information on Type of Gene Editing Approach

- Table 7.4 Genome Editing Technologies: Information on Type of Gene Delivery Method

- Table 7.5 Genome Editing Technologies: Information on Type of Gene Delivery Modality

- Table 7.6 Genome Editing Technologies: Information on Highest Phase of Drug Development Supported

- Table 7.7 Genome Editing Technologies: Information on Therapeutic Area

- Table 7.8 Genome Editing Technologies: Information on Application Area

- Table 7.9 Genome Editing Technologies: List of Technology Providers

- Table 7.10 Genome Editing Technology Providers: Information on Operational Model

- Table 7.11 Genome Editing Technology Providers: Information on Product Centric Model and Technology Centric Model

- Table 8.1 Genome Editing Technologies Provided by Players Headquartered in North America

- Table 8.2 Genome Editing Technologies Provided by Players Headquartered in Europe

- Table 8.3 Genome Editing Technologies Provided by Players Headquartered in Asia-Pacific, Middle East and North Africa, and Latin America

- Table 9.1 Genome Editing Technology Providers: List of Companies Profiled

- Table 9.2 Arcturus Therapeutics: Company Overview

- Table 9.3 Arcturus Therapeutics: Technology Portfolio

- Table 9.4 Arcturus Therapeutics: Recent Developments and Future Outlook

- Table 9.5 Arsenal Bio: Company Overview

- Table 9.6 Arsenal Bio: Technology Portfolio

- Table 9.7 Arsenal Bio: Recent Developments and Future Outlook

- Table 9.8 Beam Therapeutics: Company Overview

- Table 9.9 Beam Therapeutics: Technology Portfolio

- Table 9.10 Beam Therapeutics: Recent Developments and Future Outlook

- Table 9.11 Caribou Biosciences: Company Overview

- Table 9.12 Caribou Biosciences: Technology Portfolio

- Table 9.13 Caribou Biosciences: Recent Developments and Future Outlook

- Table 9.14 Century Therapeutics: Company Overview

- Table 9.15 Century Therapeutics: Technology Portfolio

- Table 9.16 Century Therapeutics: Recent Developments and Future Outlook

- Table 9.17 CRISPR Therapeutics: Company Overview

- Table 9.18 CRISPR Therapeutics: Technology Portfolio

- Table 9.19 CRISPR Therapeutics: Recent Developments and Future Outlook

- Table 9.20 Editas Medicine: Company Overview

- Table 9.21 Editas Medicine: Technology Portfolio

- Table 9.22 Editas Medicine: Recent Developments and Future Outlook

- Table 9.23 Intellia Therapeutics: Company Overview

- Table 9.24 Intellia Therapeutics: Technology Portfolio

- Table 9.25 Intellia Therapeutics: Recent Developments and Future Outlook

- Table 9.26 Prime Medicine: Company Overview

- Table 9.27 Prime Medicine: Technology Portfolio

- Table 9.28 Prime Medicine: Recent Developments and Future Outlook

- Table 9.29 Vor Biopharma: Company Overview

- Table 9.30 Vor Biopharma: Technology Portfolio

- Table 9.31 Vor Biopharma: Recent Developments and Future Outlook

- Table 10.1 Genome Editing Technology Providers: List of Companies Profiled

- Table 10.2 Avectas: Company Overview

- Table 10.3 Avectas: Technology Portfolio

- Table 10.4 Bio-Sourcing: Company Overview

- Table 10.5 Bio-Sourcing: Technology Portfolio

- Table 10.6 Flash BioSolutions: Company Overview

- Table 10.7 Flash BioSolutions: Technology Portfolio

- Table 10.8 Ntrans Technologies: Company Overview

- Table 10.9 Ntrans Technologies: Technology Portfolio

- Table 10.10 OXGENE: Company Overview

- Table 10.11 OXGENE: Technology Portfolio

- Table 10.12 Revvity: Company Overview

- Table 10.13 Revvity: Technology Portfolio

- Table 11.1 Genome Editing Technology Providers: List of Companies Profiled

- Table 11.2 Edigene: Company Overview

- Table 11.3 Edigene: Technology Portfolio

- Table 11.4 Fortgen: Company Overview

- Table 11.5 Fortgen: Technology Portfolio

- Table 11.6 G+FLAS Life Sciences: Company Overview

- Table 11.7 G+FLAS Life Sciences: Technology Portfolio

- Table 11.8 TargetGene Biotechnologies: Company Overview

- Table 11.9 TargetGene Biotechnologies: Technology Portfolio

- Table 12.1 Genome Editing Market: List of Partnerships and Collaborations

- Table 12.2 Technology Licensing / Integration Agreements: Information on Purpose of Partnership

- Table 12.3 Partnerships and Collaborations: Information on Type of Agreement

- Table 13.1 Patent Analysis: Top CPC Sections

- Table 13.2 Patent Analysis: Top CPC Symbols

- Table 13.3 Patent Analysis: Top CPC Codes

- Table 13.4 Patent Analysis: Summary of Benchmarking Analysis

- Table 13.5 Patent Analysis: Categorization based on Weighted Valuation Scores

- Table 13.6 Patent Portfolio: List of Leading Patents (by Highest Relative Valuation)

- Table 14.1 Genome Editing Market: List of Funding and Investments

- Table 16.1 Genome Editing Technologies: Average Upfront Payment and Average Milestone Payment, 2018-2024 (USD Million)

- Table 16.2 Licensing Deals: Tranches of Milestone Payments

- Table 26.1 Leading Industry Players: Based on General Market Understanding

- Table 26.2 Leading Industry Players: Based on Funding Amount Invested (USD Million)

- Table 26.3 Leading Industry Players: Based on Number of Technology Licensing / Integration Deals

- Table 28.1 Prorenata Biotech: Company Snapshot

- Table 29.1 Genome Editing Technologies: Distribution by Type of Gene Editing Technique

- Table 29.2 Genome Editing Technologies: Distribution by Type of Gene Editing Approach

- Table 29.3 Genome Editing Technologies: Distribution by Type of Gene Delivery Method

- Table 29.4 Genome Editing Technologies: Distribution by Type of Gene Delivery Modality

- Table 29.5 Genome Editing Technologies: Distribution by Highest Phase of Drug Development Supported

- Table 29.6 Genome Editing Technologies: Distribution by Therapeutic Area

- Table 29.7 Genome Editing Technologies: Distribution by Application Area

- Table 29.8 Genome Editing Technology Providers: Distribution by Year of Establishment

- Table 29.9 Genome Editing Technology Providers: Distribution by Company Size

- Table 29.10 Genome Editing Technology Providers: Distribution by Location of Headquarters

- Table 29.11 Genome Editing Technology Providers: Distribution by Company Size and Location of Headquarters

- Table 29.12 Most Active Players: Distribution by Number of Technologies

- Table 29.13 Genome Editing Technology Providers: Distribution by Operational Model

- Table 29.14 Genome Editing Technology Providers: Distribution by Product Centric Model

- Table 29.15 Genome Editing Technology Providers: Distribution by Technology Centric Model

- Table 29.16 Arcturus Therapeutics: Annual Revenues, Since FY 2021 (USD Million)

- Table 29.17 Beam Therapeutics: Annual Revenues, Since FY 2021 (USD Million)

- Table 29.18 Caribou Biosciences: Annual Revenues, Since FY 2021 (USD Million)

- Table 29.19 Century Therapeutics: Annual Revenues, Since FY 2022 (USD Million)

- Table 29.20 CRISPR Therapeutics: Annual Revenues, Since FY 2021 (USD Million)

- Table 29.21 Editas Medicine: Annual Revenues, Since FY 2021 (USD Million)

- Table 29.22 Intellia Therapeutics: Annual Revenues, Since FY 2021 (USD Million)

- Table 29.23 Partnerships and Collaborations: Cumulative Year-wise Trend

- Table 29.24 Partnerships and Collaborations: Distribution by Type of Partnership

- Table 29.25 Partnerships and Collaborations: Distribution by Year and Type of Partnership

- Table 29.26 Technology Licensing Agreements / Technology Integration Agreements: Distribution by Purpose of Partnership

- Table 29.27 Partnerships and Collaborations: Distribution by Type of Partner

- Table 29.28 Partnerships and Collaborations: Distribution by Location of Headquarters of Partner

- Table 29.29 Most Active Players: Distribution by Number of Partnerships

- Table 29.30 Partnership and Collaborations: Local and International Agreements

- Table 29.31 Partnerships and Collaborations: Intracontinental and Intercontinental Agreements

- Table 29.32 Patent Analysis: Distribution by Type of Patent

- Table 29.33 Patent Analysis: Distribution by Patent Application Year

- Table 29.34 Patent Analysis: Distribution by Patent Publication Year

- Table 29.35 Patent Analysis: Distribution by Type of Patents and Publication Year

- Table 29.36 Patent Analysis: Distribution by Patent Jurisdiction

- Table 29.37 Patent Analysis: Cumulative Year-wise Trend by Type of Applicant

- Table 29.38 Leading Industry Players: Distribution by Number of Patents

- Table 29.39 Leading Non-Industry Players: Distribution by Number of Patents

- Table 29.40 Leading Individual Assignees: Distribution by Number of Patents

- Table 29.41 Patent Analysis: Distribution by Patent Age

- Table 29.42 Genome editing: Patent Valuation

- Table 29.43 Funding and Investment Analysis: Cumulative Year-wise Trend

- Table 29.44 Funding and Investment Analysis: Cumulative Year-wise Trend of Amount Invested (USD Million)

- Table 29.45 Funding and Investment Analysis: Distribution of Funding Instances by Type of Funding

- Table 29.46 Funding and Investment Analysis: Distribution of Amount Invested by Type of Funding (USD Million)

- Table 29.47 Funding and Investment Analysis: Distribution by Year and Type of Funding

- Table 29.48 Funding and Investments: Distribution of Funding Instances by Geography

- Table 29.49 Most Active Players: Distribution by Amount Invested and Number of Funding Instances

- Table 29.50 Leading Investors: Distribution by Number of Funding Instances

- Table 29.51 Global Genome Editing Technologies Market, Forecasted Estimates, till 2035 (USD Billion)

- Table 29.52 Global Genome Editing Technologies Market, Forecasted Estimates, till 2035: Conservative Scenario (USD Billion)

- Table 29.53 Global Genome Editing Technologies Market, Forecasted Estimates, till 2035: Optimistic Scenario (USD Billion)

- Table 29.54 Genome Editing Technologies Market: Distribution by Type of Payment Method Employed

- Table 29.55 Genome Editing Technologies Market for Milestone Payments: Forecasted Estimates, till 2035 (USD Million)

- Table 29.56 Genome Editing Technologies Market for Upfront Payments: Forecasted Estimates, till 2035 (USD Million)

- Table 29.57 Genome Editing Technologies Market: Distribution by Type of Gene Editing Technique

- Table 29.58 Genome Editing Technologies Market for CRISPR-Cas System: Forecasted Estimates, till 2035 (USD Million)

- Table 29.59 Genome Editing Technologies Market for TALENs: Forecasted Estimates, till 2035 (USD Million)

- Table 29.60 Genome Editing Technologies Market for Meganucleases: Forecasted Estimates, till 2035 (USD Million)

- Table 29.61 Genome Editing Technologies Market for ZFNs: Forecasted Estimates, till 2035 (USD Million)

- Table 29.62 Genome Editing Technologies Market for Other Techniques: Forecasted Estimates, till 2035 (USD Million)

- Table 29.63 Genome Editing Technologies Market: Distribution by Type of Gene Editing Approach

- Table 29.64 Genome Editing Technologies Market for Gene Knock-Out: Forecasted Estimates, till 2035 (USD Million)

- Table 29.65 Genome Editing Technologies Market for Gene Knock-In: Forecasted Estimates, till 2035 (USD Million)

- Table 29.66 Genome Editing Technologies Market: Distribution by Type of Gene Delivery Method

- Table 29.67 Genome Editing Technologies Market for Ex vivo: Forecasted Estimates, till 2035 (USD Million)

- Table 29.68 Genome Editing Technologies Market for In vivo: Forecasted Estimates, till 2035 (USD Million)

- Table 29.69 Genome Editing Technologies Market: Distribution by Type of Gene Delivery Modality

- Table 29.70 Genome Editing Technologies Market for Viral Vectors: Forecasted Estimates, till 2035 (USD Million)

- Table 29.71 Genome Editing Technologies Market for Non-Viral Vectors: Forecasted Estimates, till 2035 (USD Million)

- Table 29.72 Genome Editing Technologies Market: Distribution by Type of Therapy

- Table 29.73 Genome Editing Technologies Market for Cell Therapies: Forecasted Estimates, till 2035 (USD Million)

- Table 29.74 Genome Editing Technologies Market for Gene Therapies: Forecasted Estimates, till 2035 (USD Million)

- Table 29.75 Genome Editing Technologies Market for Other Therapies: Forecasted Estimates, till 2035 (USD Million)

- Table 29.76 Genome Editing Technologies Market: Distribution by Application Area

- Table 29.77 Genome Editing Technologies Market for Drug Discovery and Development: Forecasted Estimates, till 2035 (USD Million)

- Table 29.78 Genome Editing Technologies Market for Diagnostics: Forecasted Estimates, till 2035 (USD Million)

- Table 29.79 Genome Editing Technologies Market: Distribution by Type of End-User

- Table 29.80 Genome Editing Technologies Market for Pharmaceutical and Biotechnology Companies: Forecasted Estimates, till 2035 (USD Million)

- Table 29.81 Genome Editing Technologies Market for Academic and Research Institutes: Forecasted Estimates, till 2035 (USD Million)

- Table 29.82 Genome Editing Technologies Market: Distribution by Geographical Regions

- Table 29.83 Genome Editing Technologies Market in North America: Forecasted Estimates, till 2035 (USD Million)

- Table 29.84 Genome Editing Technologies Market in the US: Forecasted Estimates, till 2035 (USD Million)

- Table 29.85 Genome Editing Technologies Market in Canada: Forecasted Estimates, till 2035 (USD Million)

- Table 29.86 Genome Editing Technologies Market in Europe: Forecasted Estimates till 2035 (USD Million)

- Table 29.87 Genome Editing Technologies Market in Germany: Forecasted Estimates till 2035 (USD Million)

- Table 29.88 Genome Editing Technologies Market in France: Forecasted Estimates till 2035 (USD Million)

- Table 29.89 Genome Editing Technologies Market in Ireland: Forecasted Estimates till 2035 (USD Million)

- Table 29.90 Genome Editing Technologies Market in Asia-Pacific: Forecasted Estimates, till 2035 (USD Million)

- Table 29.91 Genome Editing Technologies Market in South Korea: Forecasted Estimates, till 2035 (USD Million)

- Table 29.92 Genome Editing Technologies Market in China: Forecasted Estimates, till 2035 (USD Million)

- Table 29.93 Genome Editing Technologies Market in Japan: Forecasted Estimates, till 2035 (USD Million)

质体定序市场总体状况:按服务、技术、样本类型、时间要求、应用和最终用户划分-2026-2032年全球预测

质体定序市场总体状况:按服务、技术、样本类型、时间要求、应用和最终用户划分-2026-2032年全球预测 基因组编辑市场-全球产业规模、份额、趋势、机会及预测(按技术、交付模式、应用、模式、最终用户、地区和竞争格局划分,2021-2031年)多重基因突变检测试剂盒市场(依产品类型、技术、疾病类型、应用和最终用户划分)-2026-2032年全球预测

基因组编辑市场-全球产业规模、份额、趋势、机会及预测(按技术、交付模式、应用、模式、最终用户、地区和竞争格局划分,2021-2031年)多重基因突变检测试剂盒市场(依产品类型、技术、疾病类型、应用和最终用户划分)-2026-2032年全球预测 基因组编辑市场规模、份额和成长分析(按技术、交付方式、应用、改进和地区划分)—产业预测(2026-2033 年)

基因组编辑市场规模、份额和成长分析(按技术、交付方式、应用、改进和地区划分)—产业预测(2026-2033 年) 基因组编辑市场规模、份额和趋势分析报告:按技术、交付方式、应用、模式、最终用途、地区和细分市场预测(2026-2033 年)

基因组编辑市场规模、份额和趋势分析报告:按技术、交付方式、应用、模式、最终用途、地区和细分市场预测(2026-2033 年) 基因写入和可程式基因组工程:精准基因插入、修復和合成DNA写入平台-技术、研发管线趋势、竞争情报和全球市场展望(2025-2045)基因组编辑市场(按技术、应用、最终用户、治疗领域和交付方式)—2025-2032 年全球预测基因组编辑突变检测试剂套件市场:依技术、检测方法、应用、最终用户、通路和工作流程阶段划分-2025-2032年全球预测

基因写入和可程式基因组工程:精准基因插入、修復和合成DNA写入平台-技术、研发管线趋势、竞争情报和全球市场展望(2025-2045)基因组编辑市场(按技术、应用、最终用户、治疗领域和交付方式)—2025-2032 年全球预测基因组编辑突变检测试剂套件市场:依技术、检测方法、应用、最终用户、通路和工作流程阶段划分-2025-2032年全球预测 基因组编辑:科技与全球市场日本基因组编辑市场规模、份额、趋势分析报告:按技术、交付方式、应用、最终用途、模式和细分市场预测,2025 年至 2033 年

基因组编辑:科技与全球市场日本基因组编辑市场规模、份额、趋势分析报告:按技术、交付方式、应用、最终用途、模式和细分市场预测,2025 年至 2033 年