|

市场调查报告书

商品编码

1776873

医疗保健大数据市场:产业趋势及全球预测-按组件、硬体类型、软体类型、服务类型、部署选项、应用领域、医疗保健产业、最终用户、经济状况、地区和主要参与者划分Big Data in Healthcare Market: Industry Trends and Global Forecasts - Distribution by Component, Hardware, Software, Service, Deployment Option, Application Area, Healthcare Vertical, End User, Economic Status, Geography and Leading Players |

||||||

预计到 2035 年,全球医疗保健大数据市场规模将从目前的 780 亿美元成长至 5,400 亿美元,预测期内复合年增长率为 19.20%。

市场区隔根据以下参数划分市场规模与机会:

零组件

- 硬体设备

- 软体

- 服务

硬体设备类型

- 储存·设备

- 网路·基础设施

- 伺服器

软体类型

- 电子健康记录

- 诊疗管理软体

- 收益循环管理软体

- 劳动力管理软体

服务类型

- 说明的分析

- 诊断分析

- 预测分析

- 指示性分析

展开选择

- 云端基础

- 内部部署

应用领域

- 临床资料管理

- 财务管理

- 运用管理

- 族群健康管理

医疗保健各领域

- 医疗保健服务

- 医疗设备

- 医药品

- 其他

终端用户

- 诊所

- 医疗保险代理店

- 医院

- 其他

经济状况

- 高所得国

- 高中所得国

- 低中所得国

主要地区

- 北美

- 欧洲

- 亚洲

- 南美

- 中东·北非

- 其他地区

全球医疗保健大数据市场:成长与趋势

医疗保健大数据是指持续成长且无法使用传统工具有效储存和处理的大量资料。由于医疗保健产业产生的大量数据,尤其是近年来,大数据以及大数据分析工具和技术的普及度呈指数级增长。医疗保健大数据利用大量现有数据,将为患者提供个人化照护的课题转化为机会。此外,大数据可用于医疗保健产业的各个领域,包括人口健康管理、电子健康记录 (EHR) 管理、药物研究以及远距医疗和远距保健。

大数据在医疗保健领域的日益普及,对医疗保健大数据市场的规模产生了重大影响。大数据分析不仅应用于医疗保健市场,也应用于各个领域,利用机器学习和人工智慧来推动组织发展并预测未来趋势。大数据也对金融业产生了重大影响。医疗保健领域的大数据具有许多优势,将预测分析和机器学习演算法与大数据结合,可实现早期疾病检测、个人化治疗方案和精准医疗。

全球医疗保健大数据市场:关键洞察

本报告深入探讨了全球医疗保健大数据市场的现状,并识别了行业内的潜在成长机会。主要发现包括:

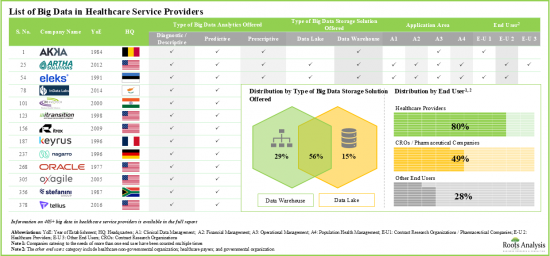

- 超过 405 家公司提供客製化解决方案和服务,以支援医疗保健领域的大数据应用,其中约 55% 的公司提供用于资料管理和分析的资料仓储和资料湖。

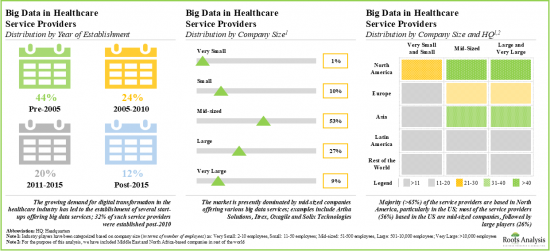

- 大多数服务提供者(超过 65%)位于北美,尤其是美国。大多数美国服务供应商(56%)是中型公司,其次是大型公司(26%)。

- 市场格局高度分散,既有新进者,也有位于不同地区的老牌公司。其中近 55% 的公司是中型公司。

- 各种分析模型从临床、营运和财务数据中获取洞察。 23% 的参与者提供全面的大数据分析软体套件,包括预测性分析、规范分析和描述性分析。

- 为了获得竞争优势,企业正在积极升级现有功能并添加新功能,以增强其产品组合和合作伙伴的大数据产品。

- 分析影响医疗保健市场大数据发展的关键驱动因素和障碍,为深入了解该领域当前和未来的商业机会提供了宝贵的见解。

- 受云端解决方案和服务日益普及的推动,医疗保健领域的大数据市场在未来 12 年内的复合年增长率预计将达到 19.06%。

- 预计市场机会将涵盖大数据的各个组成部分,包括各种类型的硬体、服务和软体。

- 高收入国家正优先采用大数据解决方案来优化营运管理,从而提高医疗保健营运的效率和效益,并推动市场收入成长。

- 随着远距医疗服务和个人化医疗需求的不断增长,医疗保健大数据市场为不同地区的参与者提供了丰厚的机会。

全球医疗保健大数据市场:主要细分市场

依组成部分划分,市场分为大数据硬体、大数据软体及大数据服务。目前,硬体市场在全球医疗保健大数据市场中占据最大占有率(超过 40%)。此外,由于先进技术的日益普及以及对技术创新的持续投入,硬体领域的成长速度可能高于其他领域。

依硬体类型,市场细分为储存设备、网路基础架构和伺服器。目前,储存设备领域占据医疗大数据市场的最大占有率(约 60%)。此外,该领域很可能以相对较高的复合年增长率成长。

依软体类型,市场细分为电子病历、实务管理软体、收入週期管理软体和劳动力管理软体。目前,电子病历领域占据医疗大数据市场的最大占有率(超过 45%)。此外,劳动力管理软体领域很可能以相对较高的复合年增长率成长。

依服务类型,市场细分为描述性分析、诊断性分析、预测性分析及规范性分析。目前,诊断分析领域占据医疗大数据市场的最大占有率(超过 30%)。此外,值得注意的是,医疗大数据市场中的规范分析领域很可能以相对较高的复合年增长率成长。

根据部署方式,市场分为云端部署和本地部署。由于云端部署具有可扩展性、灵活性、成本效益、易于部署和维护以及资料存取等诸多优势,云端部署目前占据医疗大数据市场的最大占有率(约 60%)。预计未来这一趋势将持续下去。

根据应用,市场分为临床资料管理、财务管理、营运管理和人口健康管理。目前,营运管理领域占据医疗大数据市场的最大占有率(超过 30%)。此外,预计在预测期内,人口健康管理领域的复合年增长率将高于其他领域,展现出最高的成长潜力。

依医疗保健领域划分,市场分为医疗服务、医疗器材、药品及其他领域。虽然医疗服务领域预计将成为整体市场的主要驱动力,但值得注意的是,医疗器材领域的全球医疗大数据市场复合年增长率可能超过20%。

依最终用户划分,全球市场分为诊所、医疗保险机构、医院和其他领域。目前,医院领域占最大市场占有率(超过40%)。然而,预计未来几年诊所领域的医疗大数据市场将显着成长。

依经济状况划分,市场分为高收入国家、中上收入国家及中下收入国家。目前,高收入国家在医疗大数据市场中占比最高(约 85%)。此外,值得注意的是,中上收入国家的医疗大数据市场可望维持相对较高的复合年增长率。

依主要地区划分,市场分为北美、欧洲、亚洲、中东及非洲、拉丁美洲等地区。目前,北美(约 60%)在医疗大数据市场中占据主导地位,占据最大的收入占有率。然而,预计亚太地区的市场将以更高的复合年增长率成长。

医疗保健的巨量资料市场参与企业案例

- Accenture

- Akka Technologies

- Altamira.ai

- Amazon Web Services

- Athena Global Technologies

- atom Consultancy Services(ACS)

- Avenga

- Happiest Minds

- InData Labs

- Itransition

- Kellton

- Keyrus

- Lutech

- Microsoft

- Nagarro

- Nous Infosystems

- NTT data

- Oracle

- Orange Mantra

- Oxagile

- Scalefocus

- Softweb Solutions

- Solix Technologies

- Spindox

- Tata Elxsi

- Teradata

- Trianz(formerly CBIG Consulting)

- Trigyn Technologies

- XenonStack

按按本报告提供全球医疗保健的巨量资料市场相关调查,市场概要,以及各零件,硬体设备类别,软体类别,各服务形式,展开选择,应用各领域,医疗保健各领域,各终端用户,经济状况,各地区的趋势,及的加入此市场的主要企业的简介等。

目录

第1章 序文

第2章 调查手法

- 章概要

- 调查的前提

- 计划调查手法

- 预测调查手法

- 坚牢的品管

- 重要的考虑事项

- 主要的市场区隔

第3章 经济以及其他的计划特有的考虑事项

- 章概要

- 市场动态

第4章 摘要整理

第5章 简介

- 章概要

- 巨量资料概要

- 巨量资料分析

- 医疗保健的巨量资料的应用

- 未来展望

第6章 市场形势

第7章 重要的洞察

- 章概要

- 医疗保健服务供应商的巨量资料:重要的洞察

第8章 企业竞争力分析

- 章概要

- 前提主要的参数

- 调查手法

- 医疗保健服务供应商的巨量资料:企业竞争力分析

第9章 企业简介北美的医疗保健服务供应商的巨量资料

- 章概要

- 北美的主要加入企业的详细内容简介

- Amazon Web Services

- Microsoft

- Oracle

- Teradata

- 北美的其他的参与企业的简介

- Itransition

- Nous Infosystems

- Oxagile

- Softweb Solutions

- Solix Technologies

- Trianz(formerly CBIG Consulting)

第10章 企业简介:欧洲的医疗保健服务供应商的巨量资料

- 章概要

- 欧洲的主要加入企业的详细内容简介

- Accenture

- Keyrus

- 欧洲的其他的参与企业的简介

- Akka Technologies

- Altamira.ai

- atom Consultancy Services(ACS)

- Avenga

- Lutech

- Nagarro

- Scalefocus

- Spindox

第11章 企业简介:亚洲及全球其他地区的医疗保健服务供应商的巨量资料

- 章概要

- 亚洲及其他各国的主要加入企业的详细内容简介

- Tata Elxsi

- Kellton

- 亚洲及其他各国的其他的参与企业的简介

- Athena Global Technologies

- Happiest Minds

- InData Labs

- NTT data

- OrangeMantra

- Trigyn Technologies

- XenonStack

第12章 市场影响分析:促进因素,阻碍因素,机会,课题

第13章 医疗保健市场上世界巨量资料

- 章概要

- 与主要的前提调查手法

- 医疗保健市场上全球巨量资料,历史的趋势(2018年以后)与预测(到2035年)

- 主要的市场区隔

第14章 医疗保健市场上巨量资料(各零件)

- 章概要

- 与主要的前提调查手法

- 医疗保健市场上巨量资料:各零件

- 与资料的三角测量检验

第15章 医疗保健市场上巨量资料(各硬体设备)

- 章概要

- 与主要的前提调查手法

- 医疗保健市场上巨量资料:硬体设备类别

- 与资料的三角测量检验

第16章 医疗保健市场上巨量资料(软体类别)

- 章概要

- 与主要的前提调查手法

- 医疗保健市场上巨量资料:软体类别

- 与资料的三角测量检验

第17章 医疗保健市场上巨量资料(各类服务)

- 章概要

- 与主要的前提调查手法

- 医疗保健市场上巨量资料:各服务形式

- 与资料的三角测量检验

第18章 医疗保健市场上巨量资料(展开选择)

- 章概要

- 与主要的前提调查手法

- 按医疗保健市场上巨量资料:展开选择

- 与资料的三角测量检验

第19章 医疗保健市场上巨量资料(应用各领域)

- 章概要

- 与主要的前提调查手法

- 医疗保健市场上巨量资料:应用各领域

- 与资料的三角测量检验

第20章 医疗保健市场上巨量资料(医疗保健各领域)

- 章概要

- 与主要的前提调查手法

- 医疗保健市场上巨量资料:医疗保健各领域

- 与资料的三角测量检验

第21章 医疗保健市场上巨量资料(各终端用户)

- 章概要

- 与主要的前提调查手法

- 医疗保健市场上巨量资料:各终端用户

- 与资料的三角测量检验

第22章 按医疗保健市场上巨量资料(经济状况)

- 章概要

- 与主要的前提调查手法

- 按医疗保健市场上巨量资料:经济状况

- 与资料的三角测量检验

第23章 医疗保健市场上巨量资料(各地区)

- 章概要

- 与主要的前提调查手法

- 医疗保健市场上巨量资料:各地区分布

- 与资料的三角测量检验

第24章 医疗保健市场上巨量资料,主要企业的收益预测

- 章概要

- 与主要的前提调查手法

- Microsoft

- Optum

- IBM

- Oracle

- Allscripts

第25章 结论

第26章 执行洞察

第27章 附录I:表格形式资料

第28章 附录II:企业及组织的一览

GLOBAL BIG DATA IN HEALTHCARE MARKET: OVERVIEW

As per Roots Analysis, the big data in healthcare market is estimated to grow from USD 78 billion in the current year to USD 540 billion by 2035, at a CAGR of 19.20% during the forecast period, till 2035.

The market sizing and opportunity analysis has been segmented across the following parameters:

Component

- Hardware

- Software

- Services

Type of Hardware

- Storage Devices

- Networking Infrastructure

- Servers

Type of Software

- Electronic Health Record

- Practice Management Software

- Revenue Cycle Management Software

- Workforce Management Software

Type of Service

- Descriptive Analytics

- Diagnostic Analytics

- Predictive Analytics

- Prescriptive Analytics

Deployment Option

- Cloud-based

- On-premises

Application Area

- Clinical Data Management

- Financial Management

- Operational Management

- Population Health Management

Healthcare Vertical

- Healthcare Services

- Medical Devices

- Pharmaceuticals

- Other Verticals

End User

- Clinics

- Health Insurance Agencies

- Hospitals

- Other End Users

Economic Status

- High Income Countries

- Upper-Middle Income Countries

- Lower-Middle Income Countries

Key Geographical Regions

- North America

- Europe

- Asia

- Latin America

- Middle East and North Africa

- Rest of the World

GLOBAL BIG DATA IN HEALTHCARE MARKET: GROWTH AND TRENDS

Big Data in healthcare refers to the vast amount of data that is continuously expanding and cannot be efficiently stored or processed using traditional tools. Notably, over the past few years, the popularity of big data / big data analytics tools and technologies has increased exponentially in healthcare due to the large volumes of data being generated in this domain. Big data in healthcare turns the challenges into opportunities to provide personalized care to the patients by using huge amounts of existing data. Further, big data can be used across different verticals of healthcare industry, such as in population health management, Electronic Health Record (EHR) management, pharmaceutical research, and telemedicine and telehealth.

Owing to the increasing popularity of big data in healthcare domain, there is a huge impact of big data in healthcare market size. Big data analysis is used not only in healthcare market but also used in different sectors for the growth of the organization and to forecast future trends using machine learning and artificial intelligence. Moreover, big data has also had a considerable impact on the financial sector. Big data in the healthcare domain has several advantages and the integration of predictive analytics and machine learning algorithms with big data can enable early detection of diseases, personalized treatment plans, and precision medicine.

GLOBAL BIG DATA IN HEALTHCARE MARKET: KEY INSIGHTS

The report delves into the current state of global big data in healthcare market and identifies potential growth opportunities within industry. Some key findings from the report include:

- More than 405 players claim to offer customized solutions and services to support big data in healthcare initiatives, with around 55% offering data warehouses and data lakes for data management and analytics.

- Majority (>65%) of the service providers are based in North America, particularly in the US; most of the service providers (56%) based in the US are mid-sized companies, followed by large players (26%).

- The market landscape is highly fragmented, featuring the presence of both new entrants and established players based across different geographical regions; close to 55% of such players are mid-sized companies.

- Various analytical models derive insights from clinical, operational and financial data; 23% of the players offer a comprehensive software suite of big data analytics including predictive, prescriptive, and descriptive analytics.

- In pursuit of building a competitive edge, players are actively upgrading their existing capabilities and adding new competencies in order to augment their respective portfolios and affiliated big data offerings.

- By analyzing the key drivers and barriers affecting the evolution of big data in healthcare market, valuable insights can be generated leading to a deeper understanding of the current and future opportunities within this domain.

- Driven by the increasing adoption of cloud-based solutions and services, the big data in healthcare market is likely to grow at a CAGR of 19.06% over the next 12 years.

- The projected market opportunity is anticipated to be well distributed across different components of big data, including various types of hardware, services and software.

- High-income countries are driving market revenues by prioritizing the deployment of big data solutions to optimize operational management, leading to enhanced efficiency and effectiveness in healthcare operations.

- With the rise in demand for telehealth services and personalized medicine, the big data in healthcare market presents lucrative opportunities for players based across various geographies.

GLOBAL BIG DATA IN HEALTHCARE MARKET: KEY SEGMENTS

Hardware Segment Occupies the Largest Share of the Big Data in Healthcare Market

Based on the component, the market is segmented into big data hardware, big data software and big data services. At present, hardware segment holds the maximum (>40%) share of the global big data in healthcare market. Additionally, due to the rising adoption of advanced technologies, and ongoing investments in innovation, the hardware segment is likely to grow at a faster pace compared to the other segments.

By Type of Hardware, Storage Devices Segment is the Fastest Growing Segment of the Global Big Data in Healthcare Market

Based on the type of hardware, the market is segmented into storage devices, networking infrastructure and servers. Currently, storage devices segment captures the highest proportion (~60%) of the big data in healthcare market. Further, this segment is likely to grow at a relatively higher CAGR.

Electronic Health Record Segment Occupy the Largest Share of the Big Data in Healthcare Market

Based on the type of software, the market is segmented into electronic health record, practice management software, revenue cycle management software, and workforce management software. At present, the electronic health record segment holds the maximum share (>45%) of the big data in healthcare market. In addition, workforce management software segment is likely to grow at a relatively higher CAGR.

By Type of Service, the Diagnostic Analytics Segment is the Fastest Growing Segment of the Big Data in Healthcare Market During the Forecast Period

Based on the type of service, the market is segmented into descriptive analytics, diagnostic analytics, predictive analytics, and prescriptive analytics. Currently, the diagnostic analytics segment captures the highest proportion (>30%) of the big data in healthcare market. Further, it is worth highlighting that the big data in healthcare market for prescriptive analytics segment is likely to grow at a relatively higher CAGR.

Cloud-based Segment Account for the Largest Share of the Global Big Data in Healthcare Market

Based on the deployment option, the market is segmented into cloud-based deployment and on-premises deployment. Currently, cloud-based segment holds the maximum share (~60%) of the big data in healthcare market owing to the various benefits offered by cloud-based deployment, such as scalability, flexibility, cost-effectiveness, ease of implementation and maintenance, and data accessibility. This trend is likely to remain the same in the coming years.

By Application Area, Operational Management Segment is Likely to Dominate the Big Data in Healthcare Market

Based on the application area, the market is segmented into clinical data management, financial management, operational management, and population health management. At present, the operational management segment holds the maximum share (>30%) of the big data in healthcare market. Additionally, the population health management segment is expected to show the highest growth potential during the forecast period, growing at a higher CAGR, compared to the other segments.

The Healthcare Services Segment in Healthcare Vertical Occupy the Largest Share of the Big Data in Healthcare Market

Based on the healthcare vertical, the market is segmented into healthcare services, medical devices, pharmaceuticals, and other verticals. While healthcare services segment is expected to be the primary driver of the overall market, it is worth highlighting that the global big data in healthcare market for medical devices segment is likely to grow at a relatively higher CAGR of more than 20%.

Currently, Hospitals Segment Holds the Largest Share of the Big Data in Healthcare Market

Based on end users, the global market is segmented into clinics, health insurance agencies, hospitals, and other end users. Currently, the hospitals segment holds the largest market share (>40%). However, the big data in healthcare market for clinics segment is expected to witness substantial growth in the coming years.

By Economic Status, the Upper-Middle Income Countries Segment is the Fastest Growing Segment of the Big Data in Healthcare Market During the Forecast Period

Based on the economic status, the market is segmented into high income countries, upper-middle income countries, and lower-middle income countries. Currently, the high-income countries segment captures the highest proportion (~85%) of the big data in healthcare market. Further, it is worth highlighting that the big data in healthcare market for upper-middle income countries segment is likely to grow at a relatively higher CAGR.

North America Accounts for the Largest Share of the Market

Based on key geographical regions, the market is segmented into North America, Europe, Asia, Middle East and North Africa, Latin America and Rest of the World. Currently, North America (~60%) dominates the big data in healthcare market and accounts for the largest revenue share. However, the market in Asia-Pacific is expected to grow at a higher CAGR.

Example Players in the Big Data in Healthcare Market

- Accenture

- Akka Technologies

- Altamira.ai

- Amazon Web Services

- Athena Global Technologies

- atom Consultancy Services (ACS)

- Avenga

- Happiest Minds

- InData Labs

- Itransition

- Kellton

- Keyrus

- Lutech

- Microsoft

- Nagarro

- Nous Infosystems

- NTT data

- Oracle

- Orange Mantra

- Oxagile

- Scalefocus

- Softweb Solutions

- Solix Technologies

- Spindox

- Tata Elxsi

- Teradata

- Trianz (formerly CBIG Consulting)

- Trigyn Technologies

- XenonStack

PRIMARY RESEARCH OVERVIEW

The opinions and insights presented in this study were influenced by discussions conducted with multiple stakeholders. The research report features detailed transcripts of interviews conducted with the following industry stakeholders:

- Chief Executive Officer and Founder, Company A

- Chief Executive Officer and Co-Founder, Company B

- Chief People Officer and Co-Founder, Company C

- Vice President, Company D

- Vice President, Company E

- Business Head, Company F

- Senior IT Inside Sales Lead, Company G

- Senior Manager, Company H

- Delivery Manager, Company I

- Strategy, Research and Analyst Relations Manager, Company J

- Business Development Manager, Company K

- Business Development Associate, Company L

- Business Development Specialist Advisor, Company M

- Business Development Executive, Company N

GLOBAL BIG DATA IN HEALTHCARE MARKET: RESEARCH COVERAGE

- Market Sizing and Opportunity Analysis: The report features an in-depth analysis of the global big data in healthcare market, focusing on key market segments, including [A] component, [B] type of hardware, [C] type of software, [D] type of service, [E] deployment option, [F] application area, [G] healthcare vertical, [H] end user, [I] economic status and [J] key geographical regions.

- Market Landscape: A comprehensive evaluation of big data in healthcare service providers, considering various parameters, such as [A] year of establishment, [B] company size, [C] location of headquarters, [D] business model, [E] type of offering, [F] type of big data analytics offered, [G] type of big data storage solution offered, [H] deployment option, [I] application area and [J] end user.

- Company Competitiveness Analysis: A comprehensive competitive analysis of big data in healthcare service providers, examining factors, such as [A] supplier strength and [B] portfolio strength.

- Company Profiles: In-depth profiles of companies engaged in offering big data analytics solutions across various geographies, focusing on [A] company overviews, [B] financial information (if available), [C] big data analytics offerings and capabilities and [D] recent developments and an informed future outlook.

- Market Impact Analysis: A thorough analysis of various factors, such as drivers, restraints, opportunities, and existing challenges that are likely to impact market growth.

KEY QUESTIONS ANSWERED IN THIS REPORT

- How many companies are currently engaged in this market?

- Which are the leading companies in this market?

- What factors are likely to influence the evolution of this market?

- What is the current and future market size?

- What is the CAGR of this market?

- How is the current and future market opportunity likely to be distributed across key market segments?

REASONS TO BUY THIS REPORT

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. By analyzing the competitive landscape, businesses can make informed decisions to optimize their market positioning and develop effective go-to-market strategies.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

ADDITIONAL BENEFITS

- Complimentary PPT Insights Packs

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 15% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

1. PREFACE

- 1.1. Introduction

- 1.2. Market Share Insights

- 1.3. Key Market Insights

- 1.4. Report Coverage

- 1.5. Key Questions Answered

- 1.6. Chapter Outlines

2.RESEARCH METHODOLOGY

- 2.1.Chapter Overview

- 2.2.Research Assumptions

- 2.3.Project Methodology

- 2.4.Forecast Methodology

- 2.5.Robust Quality Control

- 2.6.Key Considerations

- 2.6.1.Demographics

- 2.6.2.Economic Factors

- 2.6.3.Government Regulations

- 2.6.4. Supply Chain

- 2.6.5.COVID Impact / Related Factors

- 2.6.6. Market Access

- 2.6.7. Healthcare Policies

- 2.6.8. Industry Consolidation

- 2.7. Key Market Segmentations

3. ECONOMIC AND OTHER PROJECT SPECIFIC CONSIDERATIONS

- 3.1. Chapter Overview

- 3.2. Market Dynamics

- 3.2.1. Time Period

- 3.2.1.1. Historical Trends

- 3.2.1.2. Current and Forecasted Estimates

- 3.2.2. Currency Coverage

- 3.2.2.1. Major Currencies Affecting the Market

- 3.2.2.2. Impact of Currency Fluctuations on the Industry

- 3.2.3. Foreign Exchange Impact

- 3.2.3.1. Evaluation of Foreign Exchange Rates and Their Impact on Market

- 3.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 3.2.4. Recession

- 3.2.4.1. Historical Analysis of Past Recessions and Lessons Learnt

- 3.2.4.2. Assessment of Current Economic Conditions and Potential Impact on the Market

- 3.2.5. Inflation

- 3.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 3.2.5.2. Potential Impact of Inflation on the Market Evolution

- 3.2.1. Time Period

4. EXECUTIVE SUMMARY

- 4.1. Chapter Overview

5. INTRODUCTION

- 5.1. Chapter Overview

- 5.2. Overview of Big Data

- 5.2.1. Types of Big Data

- 5.2.1.1. Structured Data

- 5.2.1.2. Unstructured Data

- 5.2.1.3. Semi-Structured Data

- 5.2.2. Management and Storage of Big Data

- 5.2.1. Types of Big Data

- 5.3. Big Data Analytics

- 5.3.1. Types of Big Data Analytics

- 5.3.1.1. Descriptive Analytics

- 5.3.1.2. Diagnostic Analytics

- 5.3.1.3. Predictive Analytics

- 5.3.1.4. Prescriptive Analytics

- 5.3.1. Types of Big Data Analytics

- 5.4. Applications of Big Data in Healthcare

- 5.5. Future Perspective

6. OVERALL MARKET LANDSCAPE

- 6.1. Chapter Overview

- 6.2. Big Data in Healthcare Service Providers: Overall Market Landscape

- 6.3. Analysis by Year of Establishment

- 6.4. Analysis by Company Size

- 6.5. Analysis by Location of Headquarters

- 6.6. Analysis by Type of Business Model

- 6.7. Analysis by Type of Offering

- 6.8. Analysis by Type of Big Data Analytics Offered

- 6.9. Analysis by Type of Big Data Storage Solution Offered

- 6.10. Analysis by Deployment Option

- 6.11. Analysis by Application Area

- 6.12. Analysis by End User

7. KEY INSIGHTS

- 7.1. Chapter Overview

- 7.2. Big Data in Healthcare Service Providers: Key Insights

- 7.2.1. Analysis by Year of Establishment and Company Size

- 7.2.2. Analysis by Company Size and Location of Headquarters

- 7.2.3. Analysis by Type of Offering and Company Size

- 7.2.4. Analysis by Type of Big Data Analytics Offered and Application Area

- 7.2.5. Analysis by Company Size, Application Area and End User

8. COMPANY COMPETITIVENSS ANALYSIS

- 8.1. Chapter Overview

- 8.2. Assumptions and Key Parameters

- 8.3. Methodology

- 8.4. Big Data in Healthcare Service Providers: Company Competitiveness Analysis

- 8.4.1. Big Data in Healthcare Service Providers based in North America

- 8.4.1.1. Small Service Providers based in North America

- 8.4.1.2. Mid-sized Service Providers based in North America

- 8.4.1.3. Large Service Providers based in North America

- 8.4.1.4. Very LargeService Providers based in North America

- 8.4.2. Big Data in Healthcare Service Providers based in Europe

- 8.4.2.1. Small Service Providers based in Europe

- 8.4.2.2. Mid-sized Service Providers based in Europe

- 8.4.2.3. Large and Very Large Service Providers based in Europe

- 8.4.3. Big Data in Healthcare Service Providers based in Asia and Rest of the World

- 8.4.3.1. Small Service Providers based in Asia and Rest of the World

- 8.4.3.2. Mid-sized Service Providers based in Asia and Rest of the World

- 8.4.3.3. Large Service Providers based in Asia and Rest of the World

- 8.4.3.4. Very Large Service Providers based in Asia and Rest of the World

- 8.4.1. Big Data in Healthcare Service Providers based in North America

9. COMPANY PROFILES: BIG DATA IN HEALTHCARE SERVICE PROVIDERS IN NORTH AMERICA

- 9.1. Chapter Overview

- 9.2. Detailed Company Profiles of Leading Players in North America

- 9.2.1. Amazon Web Services

- 9.2.1.1. Company Overview

- 9.2.1.2. Financial Information

- 9.2.1.3. Big Data Offerings and Capabilities

- 9.2.1.4. Recent Developments and Future Outlook

- 9.2.2. Microsoft

- 9.2.2.1. Company Overview

- 9.2.2.2. Financial Information

- 9.2.2.3. Big Data Offerings and Capabilities

- 9.2.2.4. Recent Developments and Future Outlook

- 9.2.3. Oracle

- 9.2.3.1. Company Overview

- 9.2.3.2. Financial Information

- 9.2.3.3. Big Data Offerings and Capabilities

- 9.2.3.4. Recent Developments and Future Outlook

- 9.2.4. Teradata

- 9.2.4.1. Company Overview

- 9.2.4.2. Financial Information

- 9.2.4.3. Big Data Offerings and Capabilities

- 9.2.4.4. Recent Developments and Future Outlook

- 9.2.1. Amazon Web Services

- 9.3. Short Company Profiles of Other Prominent Players in North America

- 9.3.1. Itransition

- 9.3.1.1. Company Overview

- 9.3.1.2. Big Data Offerings and Capabilities

- 9.3.2 Nous Infosystems

- 9.3.2.1. Company Overview

- 9.3.2.2. Big Data Offerings and Capabilities

- 9.3.3 Oxagile

- 9.3.3.1. Company Overview

- 9.3.3.2. Big Data Offerings and Capabilities

- 9.3.4 Softweb Solutions

- 9.3.4.1. Company Overview

- 9.3.4.2. Big Data Offerings and Capabilities

- 9.3.5 Solix Technologies

- 9.3.5.1. Company Overview

- 9.3.5.2. Big Data Offerings and Capabilities

- 9.3.6 Trianz (formerly CBIG Consulting)

- 9.3.6.1. Company Overview

- 9.3.6.2. Big Data Offerings and Capabilities

- 9.3.1. Itransition

10. COMPANY PROFILES: BIG DATA IN HEALTHCARE SERVICE PROVIDERS IN EUROPE

- 10.1. Chapter Overview

- 10.2. Detailed Company Profiles of Leading Players in Europe

- 10.2.1. Accenture

- 10.2.1.1. Company Overview

- 10.2.1.2. Financial Information

- 10.2.1.3. Big Data Offerings and Capabilities

- 10.2.1.4. Recent Developments and Future Outlook

- 10.2.2. Keyrus

- 10.2.2.1. Company Overview

- 10.2.2.2. Financial Information

- 10.2.2.3. Big Data Offerings and Capabilities

- 10.2.2.4. Recent Developments and Future Outlook

- 10.2.1. Accenture

- 10.3. Short Company Profiles of Other Prominent Players in Europe

- 10.3.1. Akka Technologies

- 10.3.1.1. Company Overview

- 10.3.1.2. Big Data Offerings and Capabilities

- 10.3.2 Altamira.ai

- 10.3.2.1. Company Overview

- 10.3.2.2. Big Data Offerings and Capabilities

- 10.3.3 atom Consultancy Services (ACS)

- 10.3.3.1. Company Overview

- 10.3.3.2. Big Data Offerings and Capabilities

- 10.3.4 Avenga

- 10.3.4.1. Company Overview

- 10.3.4.2. Big Data Offerings and Capabilities

- 10.3.5 Lutech

- 10.3.5.1. Company Overview

- 10.3.5.2. Big Data Offerings and Capabilities

- 10.3.6 Nagarro

- 10.3.6.1. Company Overview

- 10.3.6.2. Big Data Offerings and Capabilities

- 10.3.7 Scalefocus

- 10.3.7.1. Company Overview

- 10.3.7.2. Big Data Offerings and Capabilities

- 10.3.8 Spindox

- 10.3.8.1. Company Overview

- 10.3.8.2. Big Data Offerings and Capabilities

- 10.3.1. Akka Technologies

11. COMPANY PROFILES: BIG DATA IN HEALTHCARE SERVICE PROVIDERS IN ASIA AND REST OF THE WORLD

- 11.1. Chapter Overview

- 11.2. Detailed Company Profiles of Leading Players in Asia and Rest of the World

- 11.2.1. Tata Elxsi

- 11.2.1.1. Company Overview

- 11.2.1.2. Big Data Offerings and Capabilities

- 11.2.1.3. Recent Developments and Future Outlook

- 11.2.2. Kellton

- 11.2.2.1. Company Overview

- 11.2.2.2. Financial Information

- 11.2.2.3. Big Data Offerings and Capabilities

- 11.2.2.4. Recent Developments and Future Outlook

- 11.2.1. Tata Elxsi

- 11.3. Short Company Profiles of Other Prominent Players in Asia and Rest of the World

- 11.3.1. Athena Global Technologies

- 11.3.1.1. Company Overview

- 11.3.1.2. Big Data Offerings and Capabilities

- 11.3.2 Happiest Minds

- 11.3.2.1. Company Overview

- 11.3.2.2. Big Data Offerings and Capabilities

- 11.3.3 InData Labs

- 11.3.3.1. Company Overview

- 11.3.3.2. Big Data Offerings and Capabilities

- 11.3.4 NTT data

- 11.3.4.1. Company Overview

- 11.3.4.2. Big Data Offerings and Capabilities

- 11.3.5 OrangeMantra

- 11.3.5.1. Company Overview

- 11.3.5.2. Big Data Offerings and Capabilities

- 11.3.6 Trigyn Technologies

- 11.3.6.1. Company Overview

- 11.3.6.2. Big Data Offerings and Capabilities

- 11.3.7 XenonStack

- 11.3.7.1. Company Overview

- 11.3.7.2. Big Data Offerings and Capabilities

- 11.3.1. Athena Global Technologies

12. MARKET IMPACT ANALYSIS: DRIVERS, RESTRAINTS, OPPORTUNITIES AND CHALLENGES

- 12.1. Chapter Overview

- 12.2. Market Drivers

- 12.3. Market Restraints

- 12.4. Market Opportunities

- 12.5. Market Challenges

- 12.6. Conclusion

13. GLOBAL BIG DATA IN HEALTHCARE MARKET

- 13.1. Chapter Overview

- 13.2. Key Assumptions and Methodology

- 13.3. Global Big Data in Healthcare Market, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 13.3.1. Scenario Analysis

- 13.3.1.1. Conservative Scenario

- 13.3.1.2. Optimistic Scenario

- 13.3.1. Scenario Analysis

- 13.4. Key Market Segmentations

14. BIG DATA IN HEALTHCARE MARKET, BY COMPONENT

- 14.1. Chapter Overview

- 14.2. Key Assumptions and Methodology

- 14.3. Big Data in Healthcare Market: Distribution by Component

- 14.3.1. Big Data Hardware: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 14.3.2. Big Data Software: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 14.3.3. Big Data Services: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 14.4. Data Triangulation and Validation

15. BIG DATA IN HEALTHCARE MARKET, BY TYPE OF HARDWARE

- 15.1. Chapter Overview

- 15.2. Key Assumptions and Methodology

- 15.3. Big Data in Healthcare Market: Distribution by Type of Hardware

- 15.3.1. Storage Devices: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 15.3.2. Servers: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 15.3.3. Networking Infrastructure: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 15.4. Data Triangulation and Validation

16. BIG DATA IN HEALTHCARE MARKET, BY TYPE OF SOFTWARE

- 16.1. Chapter Overview

- 16.2. Key Assumptions and Methodology

- 16.3. Big Data in Healthcare Market: Distribution by Type of Software

- 16.3.1. Electronic Health Record: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 16.3.2. Revenue Cycle Management Software: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 16.3.3. Practice Management Software: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 16.3.4. Workforce Management Software: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 16.4. Data Triangulation and Validation

17. BIG DATA IN HEALTHCARE MARKET, BY TYPE OF SERVICE

- 17.1. Chapter Overview

- 17.2. Key Assumptions and Methodology

- 17.3. Big Data in Healthcare Market: Distribution by Type of Services

- 17.3.1. Diagnostic Analytics: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 17.3.2. Descriptive Analytics: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 17.3.3. Predictive Analytics: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 17.3.4. Prescriptive Analytics: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 17.4. Data Triangulation and Validation

18. BIG DATA IN HEALTHCARE MARKET, BY DEPLOYMENT OPTION

- 18.1. Chapter Overview

- 18.2. Key Assumptions and Methodology

- 18.3. Big Data in Healthcare Market: Distribution by Deployment Option

- 18.3.1. Cloud-based Deployment: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 18.3.2. On-premises Deployment: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 18.4. Data Triangulation and Validation

19. BIG DATA IN HEALTHCARE MARKET, BY APPLICATION AREA

- 19.1. Chapter Overview

- 19.2. Key Assumptions and Methodology

- 19.3. Big Data in Healthcare Market: Distribution by Application Area

- 19.3.1. Operational Management: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 19.3.2. Clinical Data Management: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 19.3.3. Financial Management: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 19.3.4. Population Health Management: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 19.4. Data Triangulation and Validation

20. BIG DATA IN HEALTHCARE MARKET, BY HEALTHCARE VERTICAL

- 20.1. Chapter Overview

- 20.2. Key Assumptions and Methodology

- 20.3. Big Data in Healthcare Market: Distribution by Healthcare Vertical

- 20.3.1. Healthcare Services: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 20.3.2. Pharmaceuticals: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 20.3.3. Medical Devices: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 20.3.4. Other Verticals: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 20.4. Data Triangulation and Validation

21. BIG DATA IN HEALTHCARE MARKET, BY END USER

- 21.1. Chapter Overview

- 21.2. Key Assumptions and Methodology

- 21.3. Big Data in Healthcare Market: Distribution by End User

- 21.3.1. Hospitals: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 21.3.2. Health Insurance Agencies: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 21.3.3. Clinics: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 21.3.4. Other End Users: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 21.4. Data Triangulation and Validation

22. BIG DATA IN HEALTHCARE MARKET, BY ECONOMIC STATUS

- 22.1. Chapter Overview

- 22.2. Key Assumptions and Methodology

- 22.3. Big Data in Healthcare Market: Distribution by Economic Status

- 22.3.1. High Income Countries: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.1. US: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.2. Canada: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.3. Germany: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.4. UK: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.5. UAE: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.6. South Korea: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.7. France: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.8. Australia: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.9. New Zealand: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.10. Italy: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.11. Saudi Arabia: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1.12. Nordic Countries: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.2. Upper-Middle Income Countries: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.2.1. China: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.2.2. Russia: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.2.3. Brazil: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.2.4. Japan: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.2.5. South Africa: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.3. Lower-Middle Income Countries: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.3.1. India: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.3.1. High Income Countries: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.4. Data Triangulation and Validation

23. BIG DATA IN HEALTHCARE MARKET, BY GEOGRAPHY

- 23.1. Chapter Overview

- 23.2. Key Assumptions and Methodology

- 23.3. Big Data in Healthcare Market: Distribution by Geography

- 23.3.1. North America: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 23.3.2. Europe: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 23.3.3. Asia: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 23.3.4. Middle East and North Africa: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 23.3.5. Latin America: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 23.3.6. Rest of the World: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 23.4. Data Triangulation and Validation

24. BIG DATA IN HEALTHCARE MARKET, REVENUE FORECAST OF LEADING PLAYERS

- 24.1. Chapter Overview

- 24.2. Key Assumptions and Methodology

- 24.3. Microsoft: Revenue Generated from Big Data in Healthcare Offerings Since FY 2018

- 24.4. Optum: Revenue Generated from Big Data in Healthcare Offerings Since FY 2018

- 24.5. IBM: Revenue Generated from Big Data in Healthcare Offerings Since FY 2018

- 24.6. Oracle: Revenue Generated from Big Data in Healthcare Offerings Since FY 2018

- 24.7. Allscripts: Revenue Generated from Big Data in Healthcare Offerings Since FY 2018

25. CONCLUSION

- 25.1. Chapter Overview

26. EXECUTIVE INSIGHTS

- 26.1. Chapter Overview

- 26.2. Company A

- 26.2.1. Company Snapshot

- 26.2.2. Interview Transcript

- 26.3. Company B

- 26.3.1. Company Snapshot

- 26.3.2. Interview Transcript

- 26.4. Company C

- 26.4.1. Company Snapshot

- 26.4.2. Interview Transcript

- 26.5. Company D

- 26.5.1. Company Snapshot

- 26.5.2. Interview Transcrip

- 26.6. Company E

- 26.6.1. Company Snapshot

- 26.6.2. Interview Transcript

- 26.7. Company F

- 26.7.1. Company Snapshot

- 26.7.2. Interview Transcript

- 26.8. Company G

- 26.8.1. Company Snapshot

- 26.8.2. Interview Transcript

- 26.9. Company H

- 26.9.1. Company Snapshot

- 26.9.2. Interview Transcript

- 26.10. Company I

- 26.10.1. Company Snapshot

- 26.10.2. Interview Transcript

- 26.11. Company J

- 26.11.1. Company Snapshot

- 26.11.2. Interview Transcript

- 26.12. Company K

- 26.12.1. Company Snapshot

- 26.12.2. Interview Transcript

- 26.13. Company L

- 26.13.1. Company Snapshot

- 26.13.2. Interview Transcript

- 26.14. Company M

- 26.14.1. Company Snapshot

- 26.14.2. Interview Transcript

- 26.15. Company N

- 26.15.1. Company Snapshot

- 26.15.2. Interview Transcript

27. APPENDIX I: TABULATED DATA

28. APPENDIX II: LIST OF COMPANIES AND ORGANIZATIONS

List of Tables

- Figure 2.1 Research Methodology: Project Methodology

- Figure 2.2 Research Methodology: Forecast Methodology

- Figure 2.3 Research Methodology: Robust Quality Control

- Figure 2.4 Research Methodology: Key Market Segmentation

- Figure 3.1 Lessons Learnt from Past Recessions

- Figure 4.1 Executive Summary: Overall Market Landscape

- Figure 4.2 Executive Summary: Global Market for Big Data in Healthcare by Component, Type of Hardware, Type of Software, Type of Service, and Deployment Option

- Figure 4.3 Executive Summary: Global Market for Big Data in Healthcare by Application Area, Healthcare Vertical, End User, Economic Status, Geography and Leading Players

- Figure 5.1 Types of Big Data Analytics

- Figure 5.2 Applications of Big Data in Healthcare

- Figure 6.1 Big Data in Healthcare Service Providers: Distribution by Year of Establishment

- Figure 6.2 Big Data in Healthcare Service Providers: Distribution by Company Size

- Figure 6.3 Big Data in Healthcare Service Providers: Distribution by Location of Headquarters (Region)

- Figure 6.4 Big Data in Healthcare Service Providers: Distribution by Location of Headquarters (Country)

- Figure 6.5 Big Data in Healthcare Service Providers: Distribution by Type of Business Model

- Figure 6.6 Big Data in Healthcare Service Providers: Distribution by Type of Offering

- Figure 6.7 Big Data in Healthcare Service Providers: Type of Big Data Analytics Offered

- Figure 6.8 Big Data in Healthcare Service Providers: Type of Big Data Storage Solution Offered

- Figure 6.9 Big Data in Healthcare Service Providers: Distribution by Deployment Option

- Figure 6.10 Big Data in Healthcare Service Providers: Distribution by Application Area

- Figure 6.11 Big Data in Healthcare Service Providers: Distribution by End User

- Figure 7.1 Big Data in Healthcare Service Providers: Distribution by Year of Establishment and Company Size

- Figure 7.2 Big Data in Healthcare Service Providers: Distribution by Company Size and Location of Headquarters

- Figure 7.3 Big Data in Healthcare Service Providers: Distribution by Type of Offering and Company Size

- Figure 7.4 Big Data in Healthcare Service Providers: Distribution by Type of Big Data Analytics Offered and Application Area

- Figure 7.5 Big Data in Healthcare Service Providers: Distribution by Company Size, Application Area and End User

- Figure 8.1 Company Competitiveness Analysis: Small Service Providers based in North America

- Figure 8.2 Company Competitiveness Analysis: Mid-sized Service Providers based in North America (I/II)

- Figure 8.3 Company Competitiveness Analysis: Mid-sized Service Providers based in North America (II/II)

- Figure 8.4 Company Competitiveness Analysis: Large Service Providers based in North America (I/II)

- Figure 8.5 Company Competitiveness Analysis: Large Service Providers based in North America (II/II)

- Figure 8.6 Company Competitiveness Analysis: Very Large Service Providers based in North America

- Figure 8.7 Company Competitiveness Analysis: Small Service Providers based in Europe

- Figure 8.8 Company Competitiveness Analysis: Mid-sized Service Providers based in Europe

- Figure 8.9 Company Competitiveness Analysis: Large and Very Large Big Service Providers based in Europe

- Figure 8.10 Company Competitiveness Analysis: Small Service Providers based in Asia and Rest of the World

- Figure 8.11 Company Competitiveness Analysis: Mid-sized Service Providers based in Asia and Rest of the World (I/II)

- Figure 8.12 Company Competitiveness Analysis: Mid-sized Service Providers based in Asia and Rest of the World (II/II)

- Figure 8.13 Company Competitiveness Analysis: Large Big Service Providers based in Asia and Rest of the World

- Figure 8.14 Company Competitiveness Analysis: Very Large Service Providers based in Asia and Rest of the World

- Figure 9.1 Amazon Web Services: Annual Revenues (USD Billion)

- Figure 9.2 Microsoft: Annual Revenues (USD Billion)

- Figure 9.3 Oracle: Annual Revenues (USD Billion)

- Figure 9.4 Teradata: Annual Revenues (USD Billion)

- Figure 10.1 Accenture: Annual Revenues (USD Billion)

- Figure 10.2 Keyrus: Annual Revenues (USD Million)

- Figure 11.1 Tata Elxsi: Annual Revenues (INR Billion)

- Figure 11.2 Kellton: Annual Revenues (INR Billion)

- Figure 12.1 Big Data in Healthcare Market Drivers

- Figure 12.2 Big Data in Healthcare Market Restraints

- Figure 12.3 Big Data in Healthcare Market Opportunities

- Figure 12.4 Big Data in Healthcare Market Challenges

- Figure 13.1 Global Market for Big Data in Healthcare, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 13.2 Global Market for Big Data in Healthcare, Forecasted Estimates (Till 2035): Conservative Scenario (USD Billion)

- Figure 13.3 Global Market for Big Data in Healthcare, Forecasted Estimates (Till 2035): Optimistic Scenario (USD Billion)

- Figure 14.1 Big Data in Healthcare Market: Distribution by Component (USD Billion)

- Figure 14.2 Big Data in Healthcare Market for Hardware, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 14.3 Big Data in Healthcare Market for Software, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 14.4 Big Data in Healthcare Market for Services, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 15.1 Big Data in Healthcare Market: Distribution by Type of Hardware (USD Billion)

- Figure 15.2 Big Data in Healthcare Market for Storage Devices, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 15.3 Big Data in Healthcare Market for Servers, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 15.4 Big Data in Healthcare Market for Networking Infrastructure, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 16.1 Big Data in Healthcare Market: Distribution by Type of Software (USD Billion)

- Figure 16.2 Big Data in Healthcare Market for Electronic Health Records, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 16.3 Big Data in Healthcare Market for Revenue Cycle Management Software, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 16.4 Big Data in Healthcare Market for Practice Management Software, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 16.5 Big Data in Healthcare Market for Workforce Management Software, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 17.1 Big Data in Healthcare Market: Distribution by Type of Service (USD Billion)

- Figure 17.2 Big Data in Healthcare Market for Diagnostic Analytics, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 17.3 Big Data in Healthcare Market for Descriptive Analytics, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 17.4 Big Data in Healthcare Market for Predictive Analytics, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 17.5 Big Data in Healthcare Market for Prescriptive Analytics, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 18.1 Big Data in Healthcare Market: Distribution by Deployment Option (USD Billion)

- Figure 18.2 Big Data in Healthcare Market for Cloud-based Deployment, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 18.3 Big Data in Healthcare Market for On-premises Deployment, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.1 Big Data in Healthcare Market: Distribution by Application Area

- Figure 19.2 Big Data in Healthcare Market for Operational Management, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.3 Big Data in Healthcare Market for Clinical Data Management, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.4 Big Data in Healthcare Market for Financial Management, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.5 Big Data in Healthcare Market for Population Health Management, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.1 Big Data in Healthcare Market: Distribution by Healthcare Vertical

- Figure 20.2 Big Data in Healthcare Market for Healthcare Services, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.3 Big Data in Healthcare Market for Pharmaceuticals, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.4 Big Data in Healthcare Market for Medical Devices, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 20.5 Big Data in Healthcare Market for Other Verticals, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 21.1 Big Data in Healthcare Market: Distribution by End User (USD Billion)

- Figure 21.2 Big Data in Healthcare Market for Hospitals, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 21.3 Big Data in Healthcare Market for Health Insurance Agencies, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 21.4 Big Data in Healthcare Market for Clinics, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 21.5 Big Data in Healthcare Market for Other End Users, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.1 Big Data in Healthcare Market: Distribution by Economic Status

- Figure 22.2 Big Data in Healthcare Market in High Income Countries, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.3 Big Data in Healthcare Market in the US, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.4 Big Data in Healthcare Market in Canada, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.5 Big Data in Healthcare Market in Germany, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.6 Big Data in Healthcare Market in the UK, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.7 Big Data in Healthcare Market in the UAE, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.8 Big Data in Healthcare Market in South Korea, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.9 Big Data in Healthcare Market in France, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.10 Big Data in Healthcare Market in Australia, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.11 Big Data in Healthcare Market in New Zealand, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.12 Big Data in Healthcare Market in Italy, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.13 Big Data in Healthcare Market in Saudi Arabia, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.14 Big Data in Healthcare Market in Nordic Countries, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.15 Big Data in Healthcare Market in Upper-Middle Income Countries, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.16 Big Data in Healthcare Market in China, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.17 Big Data in Healthcare Market in Russia, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.18 Big Data in Healthcare Market in Brazil, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.19 Big Data in Healthcare Market in Japan, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.20 Big Data in Healthcare Market in South Africa, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 22.21 Big Data in Healthcare Market in India, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 23.1 Big Data in Healthcare Market: Distribution by Geography (USD Billion)

- Figure 23.2 Big Data in Healthcare Market in North America, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 23.3 Big Data in Healthcare Market in Europe, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 23.4 Big Data in Healthcare Market in Asia, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 23.5 Big Data in Healthcare Market in Middle East and North Africa, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 23.6 Big Data in Healthcare Market in Latin America, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 23.7 Big Data in Healthcare Market in Rest of the World, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 24.1 Microsoft: Revenue Generated from Big Data in Healthcare Offerings, Since FY 2018 (USD Billion)

- Figure 24.2 Optum: Revenue Generated from Big Data in Healthcare Offerings, Since FY 2018 (USD Billion)

- Figure 24.3 IBM: Revenue Generated from Big Data in Healthcare Offerings, Since FY 2018 (USD Billion)

- Figure 24.4 Oracle: Revenue Generated from Big Data in Healthcare Offerings, Since FY 2018 USD Billion)

- Figure 24.5 Allscripts: Revenue Generated from Big Data in Healthcare Offerings, Since FY 2018 (USD Billion)

医疗保健领域的巨量资料市场:按组件、部署模式、应用和最终用户划分-2026-2032年全球市场预测

医疗保健领域的巨量资料市场:按组件、部署模式、应用和最终用户划分-2026-2032年全球市场预测 2026年全球巨量资料医疗保健市场报告

2026年全球巨量资料医疗保健市场报告 医疗保健巨量资料市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、解决方案和模式划分

医疗保健巨量资料市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、解决方案和模式划分 MES 市场:2025-2031

MES 市场:2025-2031 医疗保健大数据市场-全球产业规模、份额、趋势、机会和预测,按组件、应用、最终用户、地区和竞争格局划分,2020-2030年预测

医疗保健大数据市场-全球产业规模、份额、趋势、机会和预测,按组件、应用、最终用户、地区和竞争格局划分,2020-2030年预测 全球医疗保健巨量资料市场:预测(至 2032 年)—按组件、资料类型、部署方法、应用程式、最终用户和地区进行分析

全球医疗保健巨量资料市场:预测(至 2032 年)—按组件、资料类型、部署方法、应用程式、最终用户和地区进行分析