|

市场调查报告书

商品编码

1919789

全球医疗人工智慧市场(至 2040 年):按平台类型、组件类型、应用类型、技术类型、最终用户、主要地区、主要参与者、行业趋势和预测Artificial Intelligence (AI) in Healthcare Market, till 2040: Distribution by Type of Platform, Type of Component, Type of Application, Type of Technology, End User, Key Geographical Regions and Leading Players: Industry Trends and Global Forecasts |

||||||

医疗人工智慧市场展望

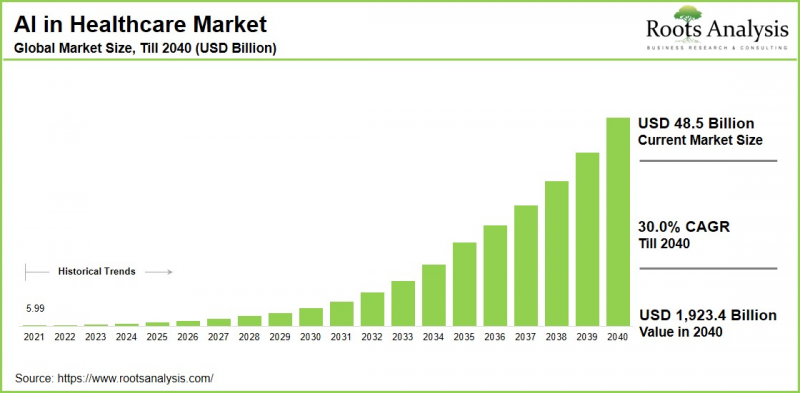

预计到 2040 年,全球医疗人工智慧市场规模将从目前的 485 亿美元增长至 19,234 亿美元,预测期内复合年增长率 (CAGR) 为 30%。

人工智慧正在迅速改变医疗保健产业,改善疾病在临床环境中的检测、治疗和管理方式。这使临床医生能够更有效率地工作,同时为患者提供更安全、更个人化的照护。人工智慧系统可以分析大量的医疗数据,包括影像、实验室数值和电子健康记录,以识别可能预示疾病早期迹象的细微模式。在放射学、病理学、心臟病学和肿瘤学领域,演算法正在透过提高诊断准确性和降低人为错误风险来辅助临床医生。除了诊断之外,人工智慧还能帮助制定个人化治疗方案、预测疾病进展并优化药物选择,从而支持向精准医疗的更广泛转变。

在营运方面,人工智慧透过自动化临床文件、虚拟助理和整合到医院资讯系统中的决策支援工具来简化工作流程。这些应用减轻了行政负担,使医疗专业人员能够更专注于直接的病患照护和复杂的决策。同时,透过人工智慧穿戴装置进行的远端患者监测有助于持续追踪生命征象并及早发现併发症,从而将医疗保健从被动应对转变为主动预防。考虑到以上因素,预计医疗保健人工智慧市场在预测期内将经历显着增长。

高阶主管的策略洞察

人工智慧在远端监测和个人化医疗中的变革性作用

人工智慧透过实现持续、数据驱动的医疗服务,增强了远距患者监测 (RPM) 和个人化医疗。穿戴式装置和居家感光元件即时追踪心率、血压、血氧饱和度和血糖值等生命征象。人工智慧演算法能够侦测细微的异常情况,例如心律不整和血氧饱和度下降,并及时向医疗专业人员发出警报,从而促进早期干预。这优化了门诊环境下慢性疾病(例如糖尿病、心血管疾病和慢性阻塞性肺病 (COPD))的管理。

在个人化医疗中,人工智慧整合了个人的基因组图谱、生活方式因素和历史健康数据,以製定个人化的优化治疗策略,预测治疗结果,并动态调整剂量和治疗方案。这些功能的结合使用可降低医疗成本,扩大医疗服务的覆盖范围,并促进居家医疗模式的发展。

医疗保健人工智慧市场的主要成长驱动因素

医疗保健人工智慧的成长受多种因素驱动,包括糖尿病和心血管疾病等慢性疾病的日益增多以及全球人口老化。这为先进的诊断和管理解决方案创造了巨大的需求。来自电子健康记录、穿戴式装置和诊断测试的大量健康数据集的涌现,使人工智慧能够改善预测分析、诊断和个人化治疗。机器学习演算法的进步、经济高效的运算基础设施和可扩展的云端技术正在推动人工智慧的广泛应用。临床人才短缺正在推动日常工作的自动化,从而降低成本并加速药物研发进程。大量的风险投资和企业投资进一步刺激了该市场的创新和成长。

医疗保健领域人工智慧的演进:产业新兴趋势

医疗保健领域人工智慧的新兴趋势包括:先进的可穿戴设备,能够实现即时健康监测,并主动提醒临床医生注意心律不整等异常情况。生成式人工智慧有助于实现临床文件的自动化,产生用于安全模型训练的合成患者数据,并加速药物研发进程。此外,自主人工智慧代理可作为虚拟助手,简化预约安排和治疗后追踪流程。增强型诊断利用人工智慧透过影像技术快速检测恶性肿瘤和脑血管疾病,并辅以精准医疗,根据基因组资讯和生活方式特征量身订做治疗方案。预测分析透过早期预警降低败血症等疾病的风险,而增强型远距医疗则整合了人工智慧聊天机器人和虚拟护理,以优化效率、成本效益和全球可及性。这些进步使人工智慧成为下一代医疗保健的基础,推动了患者疗效、营运效率和全球公平医疗服务取得的变革性改善。

本报告研究了全球医疗保健人工智慧市场,提供了市场规模估算、机会分析、竞争格局和公司概况。

目录

第一部分:报告概述

第一章:引言

第二章:研究方法

第三章:市场动态

第四章:宏观经济指标

第二部分:质性研究结果

第五章:摘要整理

第六章:引言

第七章:监理环境

第三部分:市场概览

第八章:关键指标综合资料库

第九章:竞争格局

第十章:市场空白分析

第十一章:竞争分析

第十二章:医疗人工智慧市场的新创企业生态系统

第四部分:公司简介

第十三章:公司简介

- 章节概述

- 通用电气医疗保健

- IBM

- 英特尔

- 伊特雷克斯

- IQVIA

- 微软

- 美敦力

- 医疗数据

- 默克

- 英伟达

- 甲骨文

第 5 部分:市场趋势

第 14 章:大趋势分析

第 15 章:专利分析

第 16 章:最新进展

第 6 部分:市场机会分析

第 17 章:全球医疗保健人工智慧市场

第 18 章:平台市场机会类型

第19章:依组件类型划分的市场机会

第20章:按应用类型划分的市场机会

第21章:依技术类型划分的市场机会

第22章:依最终用户划分的市场机会

第23章:北美医疗保健人工智慧市场机会

第24章:欧洲医疗保健人工智慧市场机会

第25章:亚洲医疗保健人工智慧市场机会

第26章:中东和北非(MENA)医疗保健人工智慧市场机会

第27章:市场机会拉丁美洲医疗保健人工智慧市场

第28章:其他地区医疗保健人工智慧市场的市场机会

第29章:主要参与者的市场集中度分析

第30章:邻近市场分析

第7节:策略工具

第31章:关键成功策略

第32章:波特五力分析

第33章:SWOT分析

第34章:Roots策略建议

第8节:其他独家发现

第35章:一手调查结果

第36章:报告结论

第9节:附录

AI in Healthcare Market Outlook

As per Roots Analysis, the global AI in healthcare market size is estimated to grow from USD 48.5 billion in the current year to USD 1,923.4 billion by 2040, at a CAGR of 30% during the forecast period, till 2040. The new study provides market size, growth scenarios, industry trends and future forecasts.

Artificial intelligence is rapidly reshaping healthcare by improving how diseases are detected, treated, and managed across care settings. It enables clinicians to work more efficiently while offering patients safer, more personalized care. AI systems can analyze vast volumes of medical data, such as images, lab values, and electronic health records, to identify subtle patterns that may signal early disease. In radiology, pathology, cardiology, and oncology, algorithms support clinicians by enhancing diagnostic accuracy and reducing the risk of human error. Beyond diagnosis, AI helps design tailored treatment plans, predict disease progression, and optimize drug selection, supporting the broader move toward precision medicine.

Operationally, AI streamlines workflows through automated clinical documentation, virtual assistants, and decision-support tools embedded in hospital information systems. These applications reduce administrative burden, allowing healthcare professionals to focus more on direct patient interaction and complex decision-making. At the same time, remote patient monitoring powered by AI-enabled wearables supports continuous tracking of vital signs and early detection of complications, shifting healthcare from reactive to preventive models. Considering the above mentioned factors, the AI in healthcare market is expected to grow significantly throughout the forecast period.

Strategic Insights for Senior Leaders

Transformative Role of Artificial Intelligence in Remote Monitoring and Personalized Medicine

Artificial Intelligence (AI) enhances remote patient monitoring (RPM) and personalized medicine by enabling continuous, data-driven care delivery. Wearable devices and home sensors track vital signs, including heart rate, blood pressure, oxygen saturation, and glucose levels in real time. AI algorithms detect subtle anomalies, such as irregular cardiac rhythms or declining oxygenation, triggering timely alerts to clinicians and facilitating early interventions. This optimizes management of chronic conditions like diabetes, cardiovascular disease, and chronic obstructive pulmonary disease (COPD) in outpatient settings.

In personalized medicine, AI integrates individual genomic profiles, lifestyle factors, and historical health data to develop tailored treatment strategies, forecast therapeutic responses, and dynamically adjust dosages or regimens. Collectively, these capabilities reduce healthcare costs, expand access, and facilitate home-based models.

Key Drivers Propelling Growth of AI in Healthcare Market

The growth of artificial intelligence (AI) in healthcare is being driven by several key factors including the rising prevalence of chronic diseases, such as diabetes and cardiovascular conditions along with a globally aging population. This generates substantial demand for advanced diagnostic and management solutions. The proliferation of vast health datasets from electronic health records, wearables, and diagnostic tests enables AI to enhance predictive analytics, diagnostics, and personalized therapies. Advancements in machine learning algorithms, cost-effective computing infrastructure, and scalable cloud technologies facilitate broader AI adoption. Workforce shortages among clinicians drive automation of routine tasks, cost reductions, and accelerated drug discovery processes. Substantial venture capital and corporate investments further fuels innovation and growth within this market.

AI in Healthcare Evolution: Emerging Trends in the Industry

Emerging trends in artificial intelligence (AI) for healthcare include advanced wearable devices that enable real-time health monitoring and proactive clinician alerts for anomalies such as arrhythmias. Generative AI facilitates automated clinical documentation, synthetic patient data generation for secure model training, and accelerated drug discovery pipelines. Further, autonomous AI agents function as virtual assistants, streamlining appointment scheduling and post-care follow-up. Enhanced diagnostics leverage AI for rapid detection of malignancies and cerebrovascular events in imaging. complemented by precision medicine that customizes therapies based on genomic and lifestyle profiles. Predictive analytics mitigates risks like sepsis through early warnings, while expanded remote care integrates AI-driven chatbots and virtual nursing, optimizing efficiency, cost-effectiveness, and global accessibility. These advancements collectively position AI as a cornerstone of next-generation healthcare, driving transformative improvements in patient outcomes, operational efficiency, and equitable access worldwide.

Key Market Challenges

The AI in healthcare market faces several critical challenges that hinder its full-scale adoption. These include data quality issues, with healthcare datasets frequently fragmented, incomplete, which complicates accurate model training. Privacy and cybersecurity vulnerabilities are also prominent, as patient data demands stringent protection against breaches. Further, high implementation costs, regulatory ambiguity, and ethical concerns over accountability foster reluctance among clinicians and institutions. To overcome these issues, the industry needs better data standards, skilled professionals, and strong policies to unlock the full potential of AI in healthcare.

AI in Healthcare Market: Key Market Segmentation

Type of Platform

- Solutions

- Services

Type of Component

- Hardware

- Software Solution

- Services

- Others

Type of Application

- Robot-Assisted Surgery

- Virtual Assistants

- Administrative Workflow Assistants

- Connected Medical Devices

- Medical Imaging & Diagnostics

- Clinical Trials

- Fraud Detection

- Cybersecurity

- Dosage Error Reduction

- Precision Medicine

- Drug Discovery & Development

- Lifestyle Management & Remote Patient Monitoring Wearables

- Other Applications

Type of Technology

- Machine Learning

- Natural Language Processing

- Context-aware Computing

- Computer Vision

End User

- Healthcare Providers

- Healthcare Payers

- Healthcare Companies

- Patients

- Other End Users

Geographical Regions

- North America

- US

- Canada

- Mexico

- Other North American countries

- Europe

- Austria

- Belgium

- Denmark

- France

- Germany

- Ireland

- Italy

- Netherlands

- Norway

- Russia

- Spain

- Sweden

- Switzerland

- UK

- Other European countries

- Asia

- China

- India

- Japan

- Singapore

- South Korea

- Other Asian countries

- Latin America

- Brazil

- Chile

- Colombia

- Venezuela

- Other Latin American countries

- Middle East and North Africa

- Egypt

- Iran

- Iraq

- Israel

- Kuwait

- Saudi Arabia

- UAE

- Other MENA countries

- Rest of the World

- Australia

- New Zealand

- Other countries

Example Players in AI in Healthcare Market

- GE Healthcare

- IBM

- Intel

- Itrex

- IQVIA

- Microsoft

- Medtronic

- Medidata

- Merck

- NVIDIA

- Oracle

AI in Healthcare Market: Report Coverage

The report on the AI in healthcare market features insights on various sections, including:

- Market Sizing and Opportunity Analysis: An in-depth analysis of the AI in healthcare market, focusing on key market segments, including [A] type of platform, [B] type of component, [C] type of application, [D] type of technology, [E] end user, and [F] key geographical regions.

- Competitive Landscape: A comprehensive analysis of the companies engaged in the AI in healthcare market, based on several relevant parameters, such as [A] year of establishment, [B] company size, [C] location of headquarters and [D] ownership structure.

- Company Profiles: Elaborate profiles of prominent players engaged in the AI in healthcare market, providing details on [A] location of headquarters, [B] company size, [C] company mission, [D] company footprint, [E] management team, [F] contact details, [G] financial information, [H] operating business segments, [I] technology / platform portfolio, [J] recent developments, and an informed future outlook.

- Megatrends: An evaluation of ongoing megatrends in the AI in healthcare industry.

- Patent Analysis: An insightful analysis of patents filed / granted in the AI in healthcare domain, based on relevant parameters, including [A] type of patent, [B] patent publication year, [C] patent age and [D] leading players.

- Recent Developments: An overview of the recent developments made in the AI in healthcare market, along with analysis based on relevant parameters, including [A] year of initiative, [B] type of initiative, [C] geographical distribution and [D] most active players.

- Porter's Five Forces Analysis: An analysis of five competitive forces prevailing in the AI in healthcare market, including threats of new entrants, bargaining power of buyers, bargaining power of suppliers, threats of substitute products and rivalry among existing competitors.

- SWOT Analysis: An insightful SWOT framework, highlighting the strengths, weaknesses, opportunities and threats in the domain. Additionally, it provides Harvey ball analysis, highlighting the relative impact of each SWOT parameter.

Key Questions Answered in this Report

- What is the current and future market size?

- Who are the leading companies in this market?

- What are the growth drivers that are likely to influence the evolution of this market?

- What are the key partnership and funding trends shaping this industry?

- Which region is likely to grow at higher CAGR till 2040?

- How is the current and future market opportunity likely to be distributed across key market segments?

Reasons to Buy this Report

- Detailed Market Analysis: The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- In-depth Analysis of Trends: Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. Each report maps ecosystem activity across partnerships, funding, and patent landscapes to reveal growth hotspots and white spaces in the industry.

- Opinion of Industry Experts: The report features extensive interviews and surveys with key opinion leaders and industry experts to validate market trends mentioned in the report.

- Decision-ready Deliverables: The report offers stakeholders with strategic frameworks (Porter's Five Forces, value chain, SWOT), and complimentary Excel / slide packs with customization support.

Additional Benefits

- Complimentary Dynamic Excel Dashboards for Analytical Modules

- Exclusive 15% Free Content Customization

- Personalized Interactive Report Walkthrough with Our Expert Research Team

- Free Report Updates for Versions Older than 6-12 Months

TABLE OF CONTENTS

SECTION I: REPORT OVERVIEW

1. PREFACE

- 1.1. Introduction

- 1.2. Market Share Insights

- 1.3. Key Market Insights

- 1.4. Report Coverage

- 1.5. Key Questions Answered

- 1.6. Chapter Outlines

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Introduction

- 2.4.2.2. Types

- 2.4.2.2.1. Qualitative

- 2.4.2.2.2. Quantitative

- 2.4.2.3. Advantages

- 2.4.2.4. Techniques

- 2.4.2.4.1. Interviews

- 2.4.2.4.2. Surveys

- 2.4.2.4.3. Focus Groups

- 2.4.2.4.4. Observational Research

- 2.4.2.4.5. Social Media Interactions

- 2.4.2.5. Stakeholders

- 2.4.2.5.1. Company Executives (CXOs)

- 2.4.2.5.2. Board of Directors

- 2.4.2.5.3. Company Presidents and Vice Presidents

- 2.4.2.5.4. Key Opinion Leaders

- 2.4.2.5.5. Research and Development Heads

- 2.4.2.5.6. Technical Experts

- 2.4.2.5.7. Subject Matter Experts

- 2.4.2.5.8. Scientists

- 2.4.2.5.9. Doctors and Other Healthcare Providers

- 2.4.2.6. Ethics and Integrity

- 2.4.2.6.1. Research Ethics

- 2.4.2.6.2. Data Integrity

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

3. MARKET DYNAMICS

- 3.1. Forecast Methodology

- 3.1.1. Top-Down Approach

- 3.1.2. Bottom-Up Approach

- 3.1.3. Hybrid Approach

- 3.2. Market Assessment Framework

- 3.2.1. Total Addressable Market (TAM)

- 3.2.2. Serviceable Addressable Market (SAM)

- 3.2.3. Serviceable Obtainable Market (SOM)

- 3.2.4. Currently Acquired Market (CAM)

- 3.3. Forecasting Tools and Techniques

- 3.3.1. Qualitative Forecasting

- 3.3.2. Correlation

- 3.3.3. Regression

- 3.3.4. Time Series Analysis

- 3.3.5. Extrapolation

- 3.3.6. Convergence

- 3.3.7. Forecast Error Analysis

- 3.3.8. Data Visualization

- 3.3.9. Scenario Planning

- 3.3.10. Sensitivity Analysis

- 3.4. Key Considerations

- 3.4.1. Demographics

- 3.4.2. Market Access

- 3.4.3. Reimbursement Scenarios

- 3.4.4. Industry Consolidation

- 3.5. Robust Quality Control

- 3.6. Key Market Segmentations

- 3.7. Limitations

4. MACRO-ECONOMIC INDICATORS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Overview of Major Currencies Affecting the Market

- 4.2.2.2. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Exchange Impact

- 4.2.3.1. Evaluation of Foreign Exchange Rates and Their Impact on Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.4.2. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.6. Interest Rates

- 4.2.6.1. Overview of Interest Rates and Their Impact on the Market

- 4.2.6.2. Strategies for Managing Interest Rate Risk

- 4.2.7. Commodity Flow Analysis

- 4.2.7.1. Type of Commodity

- 4.2.7.2. Origins and Destinations

- 4.2.7.3. Values and Weights

- 4.2.7.4. Modes of Transportation

- 4.2.8. Global Trade Dynamics

- 4.2.8.1. Import Scenario

- 4.2.8.2. Export Scenario

- 4.2.9. War Impact Analysis

- 4.2.9.1. Russian-Ukraine War

- 4.2.9.2. Israel-Hamas War

- 4.2.10. COVID Impact / Related Factors

- 4.2.10.1. Global Economic Impact

- 4.2.10.2. Industry-specific Impact

- 4.2.10.3. Government Response and Stimulus Measures

- 4.2.10.4. Future Outlook and Adaptation Strategies

- 4.2.11. Other Indicators

- 4.2.11.1. Fiscal Policy

- 4.2.11.2. Consumer Spending

- 4.2.11.3. Gross Domestic Product (GDP)

- 4.2.11.4. Employment

- 4.2.11.5. Taxes

- 4.2.11.6. R&D Innovation

- 4.2.11.7. Stock Market Performance

- 4.2.11.8. Supply Chain

- 4.2.11.9. Cross-Border Dynamics

- 4.2.1. Time Period

SECTION II: QUALITATIVE INSIGHTS

5. EXECUTIVE SUMMARY

6. INTRODUCTION

- 6.1. Chapter Overview

- 6.2. Overview of AI in Healthcare Market

- 6.2.1. Historical Evolution

- 6.2.2. Key Applications

- 6.2.3. Impact on Healthcare

- 6.3. Future Perspective

7. REGULATORY SCENARIO

SECTION III: MARKET OVERVIEW

8. COMPREHENSIVE DATABASE OF LEADING PLAYERS

9. COMPETITIVE LANDSCAPE

- 9.1. Chapter Overview

- 9.2. AI in Healthcare Market: Overall Market Landscape

- 9.2.1. Analysis by Year of Establishment

- 9.2.2. Analysis by Company Size

- 9.2.3. Analysis by Location of Headquarters

- 9.2.4. Analysis by Ownership Structure

10. WHITE SPACE ANALYSIS

11. COMPANY COMPETITIVENESS ANALYSIS

12. STARTUP ECOSYSTEM IN THE AI IN HEALTHCARE MARKET

- 12.1. Ai in healthcare Market: Market Landscape of Startups

- 12.1.1. Analysis by Year of Establishment

- 12.1.2. Analysis by Company Size

- 12.1.3. Analysis by Company Size and Year of Establishment

- 12.1.4. Analysis by Location of Headquarters

- 12.1.5. Analysis by Company Size and Location of Headquarters

- 12.1.6. Analysis by Ownership Structure

- 12.2. Key Findings

SECTION IV: COMPANY PROFILES

13. COMPANY PROFILES

- 13.1. Chapter Overview

- 13.2. Google*

- 13.2.1. Company Overview

- 13.2.2. Company Mission

- 13.2.3. Company Footprint

- 13.2.4. Management Team

- 13.2.5. Contact Details

- 13.2.6. Financial Performance

- 13.2.7. Operating Business Segments

- 13.2.8. Technology / Platform Portfolio

- 13.2.9. MOAT Analysis

- 13.2.10. Recent Developments and Future Outlook

- 13.3. GE Healthcare

- 13.4. IBM

- 13.5. Intel

- 13.6. Itrex

- 13.7. IQVIA

- 13.8. Microsoft

- 13.9. Medtronic

- 13.10. Medidata

- 13.11. Merck

- 13.12. NVIDIA

- 13.13. Oracle

SECTION V: MARKET TRENDS

14. MEGA TRENDS ANALYSIS

15. PATENT ANALYSIS

16. RECENT DEVELOPMENTS

- 16.1. Chapter Overview

- 16.2. Recent Funding

- 16.3. Recent Partnerships

- 16.4. Other Recent Initiatives

SECTION VI: MARKET OPPORTUNITY ANALYSIS

17. GLOBAL AI IN HEALTHCARE MARKET

- 17.1. Chapter Overview

- 17.2. Key Assumptions and Methodology

- 17.3. Trends Disruption Impacting Market

- 17.4. Demand Side Trends

- 17.5. Supply Side Trends

- 17.6. Global AI in Healthcare Market, Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 17.7. Multivariate Scenario Analysis

- 17.7.1. Conservative Scenario

- 17.7.2. Optimistic Scenario

- 17.8. Investment Feasibility Index

- 17.9. Key Market Segmentations

18. MARKET OPPORTUNITIES BASED ON TYPE OF PLATFORM

- 18.1. Chapter Overview

- 18.2. Key Assumptions and Methodology

- 18.3. Revenue Shift Analysis

- 18.4. Market Movement Analysis

- 18.5. Penetration-Growth (P-G) Matrix

- 18.6. AI in Healthcare Market for Solutions: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 18.7. AI in Healthcare Market for Services: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 18.8. Data Triangulation and Validation

- 18.8.1. Secondary Sources

- 18.8.2. Primary Sources

- 18.8.3. Statistical Modeling

19. MARKET OPPORTUNITIES BASED ON TYPE OF COMPONENT

- 19.1. Chapter Overview

- 19.2. Key Assumptions and Methodology

- 19.3. Revenue Shift Analysis

- 19.4. Market Movement Analysis

- 19.5. Penetration-Growth (P-G) Matrix

- 19.6. AI in Healthcare Market for Hardware: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 19.7. AI in Healthcare Market for Software Solutions: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 19.8. AI in Healthcare Market for Services: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 19.9. AI in Healthcare Market for Others: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 19.10. Data Triangulation and Validation

- 19.10.1. Secondary Sources

- 19.10.2. Primary Sources

- 19.10.3. Statistical Modeling

20. MARKET OPPORTUNITIES BASED ON TYPE OF APPLICATION

- 20.1. Chapter Overview

- 20.2. Key Assumptions and Methodology

- 20.3. Revenue Shift Analysis

- 20.4. Market Movement Analysis

- 20.5. Penetration-Growth (P-G) Matrix

- 20.6. AI in Healthcare Market for Robot-Assisted Surgery: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 20.7. AI in Healthcare Market for Virtual Assistants: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 20.9. AI in Healthcare Market for Administrative Workflow Assistants: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 20.10. AI in Healthcare Market for Connected Medical Devices: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 20.11. AI in Healthcare Market for Medical Imaging & Diagnostics: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 20.12. AI in Healthcare Market for Clinical Trials: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 20.13. AI in Healthcare Market for Fraud Detection: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 20.14. AI in Healthcare Market for Cybersecurity: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 20.15. AI in Healthcare Market for Dosage Error Reduction: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 20.16. AI in Healthcare Market for Precision Medicine: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 20.17. AI in Healthcare Market for Drug Discovery & Development: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 20.18. AI in Healthcare Market for Lifestyle Management & Remote Patient Monitoring Wearables: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 20.19. AI in Healthcare Market for Other Applications: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 20.20. Data Triangulation and Validation

- 20.20.1. Secondary Sources

- 20.20.2. Primary Sources

- 20.20.3. Statistical Modeling

21. MARKET OPPORTUNITIES BASED ON TYPE OF TECHNOLOGY

- 21.1. Chapter Overview

- 21.2. Key Assumptions and Methodology

- 21.3. Revenue Shift Analysis

- 21.4. Market Movement Analysis

- 21.5. Penetration-Growth (P-G) Matrix

- 21.6. AI in Healthcare Market for Machine Learning: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 21.7. AI in Healthcare Market for Natural Language Processing: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 21.8. AI in Healthcare Market for Context-aware Computing: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 21.9. AI in Healthcare Market for Computer Vision: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 21.10. Data Triangulation and Validation

- 21.10.1. Secondary Sources

- 21.10.2. Primary Sources

- 21.10.3. Statistical Modeling

22. MARKET OPPORTUNITIES BASED ON END USER

- 22.1. Chapter Overview

- 22.2. Key Assumptions and Methodology

- 22.3. Revenue Shift Analysis

- 22.4. Market Movement Analysis

- 22.5. Penetration-Growth (P-G) Matrix

- 22.6. AI in Healthcare Market for Healthcare Providers: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 22.7. AI in Healthcare Market for Healthcare Payers: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 22.8. AI in Healthcare Market for Healthcare Companies: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 22.9. AI in Healthcare Market for Patients: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 22.10. AI in Healthcare Market for Other End Users: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 22.11. Data Triangulation and Validation

- 22.11.1. Secondary Sources

- 22.11.2. Primary Sources

- 22.11.3. Statistical Modeling

23. MARKET OPPORTUNITIES FOR AI IN HEALTHCARE MARKET IN NORTH AMERICA

- 23.1. Chapter Overview

- 23.2. Key Assumptions and Methodology

- 23.3. Revenue Shift Analysis

- 23.4. Market Movement Analysis

- 23.5. Penetration-Growth (P-G) Matrix

- 23.6. AI in Healthcare Market in North America: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 23.6.1. AI in Healthcare Market in the US: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 23.6.2. AI in Healthcare Market in Canada: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 23.6.3. AI in Healthcare Market in Mexico: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 23.6.4. AI in Healthcare Market in Other North American Countries: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 23.7. Data Triangulation and Validation

24. MARKET OPPORTUNITIES FOR AI IN HEALTHCARE MARKET IN EUROPE

- 24.1. Chapter Overview

- 24.2. Key Assumptions and Methodology

- 24.3. Revenue Shift Analysis

- 24.4. Market Movement Analysis

- 24.5. Penetration-Growth (P-G) Matrix

- 24.6. AI in Healthcare Market in Europe: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 24.6.1. AI in Healthcare Market in Austria: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 24.6.2. AI in Healthcare Market in Belgium: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 24.6.3. AI in Healthcare Market in Denmark: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 24.6.4. AI in Healthcare Market in France: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 24.6.5. AI in Healthcare Market in Germany: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 24.6.6. AI in Healthcare Market in Ireland: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 24.6.7. AI in Healthcare Market in Italy: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 24.6.8. AI in Healthcare Market in Netherlands: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 24.6.9. AI in Healthcare Market in Norway: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 24.6.10. AI in Healthcare Market in Russia: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 24.6.11. AI in Healthcare Market in Spain: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 24.6.12. AI in Healthcare Market in Sweden: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 24.6.13. AI in Healthcare Market in Switzerland: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 24.6.14. AI in Healthcare Market in the UK: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 24.6.15. AI in Healthcare Market in Other European Countries: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 24.7. Data Triangulation and Validation

25. MARKET OPPORTUNITIES FOR AI IN HEALTHCARE MARKET IN ASIA

- 25.1. Chapter Overview

- 25.2. Key Assumptions and Methodology

- 25.3. Revenue Shift Analysis

- 25.4. Market Movement Analysis

- 25.5. Penetration-Growth (P-G) Matrix

- 25.6. AI in Healthcare Market in Asia: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 25.6.1. AI in Healthcare Market in China: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 25.6.2. AI in Healthcare Market in India: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 25.6.3. AI in Healthcare Market in Japan: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 25.6.4. AI in Healthcare Market in Singapore: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 25.6.5. AI in Healthcare Market in South Korea: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 25.6.6. AI in Healthcare Market in Other Asian Countries: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 25.7. Data Triangulation and Validation

26. MARKET OPPORTUNITIES FOR AI IN HEALTHCARE MARKET IN MIDDLE EAST AND NORTH AFRICA (MENA)

- 26.1. Chapter Overview

- 26.2. Key Assumptions and Methodology

- 26.3. Revenue Shift Analysis

- 26.4. Market Movement Analysis

- 26.5. Penetration-Growth (P-G) Matrix

- 26.6. AI in Healthcare Market in Middle East and North Africa (MENA): Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 26.6.1. AI in Healthcare Market in Egypt: Historical Trends (Since 2020) and Forecasted Estimates (Till 205)

- 26.6.2. AI in Healthcare Market in Iran: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 26.6.3. AI in Healthcare Market in Iraq: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 26.6.4. AI in Healthcare Market in Israel: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 26.6.5. AI in Healthcare Market in Kuwait: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 26.6.6. AI in Healthcare Market in Saudi Arabia: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 26.6.7. AI in Healthcare Market in United Arab Emirates (UAE): Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 26.6.8. AI in Healthcare Market in Other MENA Countries: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 26.7. Data Triangulation and Validation

27. MARKET OPPORTUNITIES FOR AI IN HEALTHCARE MARKET IN LATIN AMERICA

- 27.1. Chapter Overview

- 27.2. Key Assumptions and Methodology

- 27.3. Revenue Shift Analysis

- 27.4. Market Movement Analysis

- 27.5. Penetration-Growth (P-G) Matrix

- 27.6. AI in Healthcare Market in Latin America: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 27.6.1. AI in Healthcare Market in Argentina: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 27.6.2. AI in Healthcare Market in Brazil: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 27.6.3. AI in Healthcare Market in Chile: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 27.6.4. AI in Healthcare Market in Colombia Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 27.6.5. AI in Healthcare Market in Venezuela: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 27.6.6. AI in Healthcare Market in Other Latin American Countries: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 27.7. Data Triangulation and Validation

28. MARKET OPPORTUNITIES FOR AI IN HEALTHCARE MARKET IN REST OF THE WORLD

- 28.1. Chapter Overview

- 28.2. Key Assumptions and Methodology

- 28.3. Revenue Shift Analysis

- 28.4. Market Movement Analysis

- 28.5. Penetration-Growth (P-G) Matrix

- 28.6. AI in Healthcare Market in Rest of the World: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 28.6.1. AI in Healthcare Market in Australia: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 28.6.2. AI in Healthcare Market in New Zealand: Historical Trends (Since 2020) and Forecasted Estimates (Till 2040)

- 28.6.3. AI in Healthcare Market in Other Countries

- 28.7. Data Triangulation and Validation

29. MARKET CONCENTRATION ANALYSIS: DISTRIBUTION BY LEADING PLAYERS

- 29.1. Leading Player 1

- 29.2. Leading Player 2

- 29.3. Leading Player 3

- 29.4. Leading Player 4

- 29.5. Leading Player 5

- 29.6. Leading Player 6

- 29.7. Leading Player 7

- 29.8. Leading Player 8

30. ADJACENT MARKET ANALYSIS

SECTION VII: STRATEGIC TOOLS

31. KEY WINNING STRATEGIES

32. PORTER'S FIVE FORCES ANALYSIS

33. SWOT ANALYSIS

34. ROOTS STRATEGIC RECOMMENDATIONS

- 34.1. Chapter Overview

- 34.2. Key Business-related Strategies

- 34.2.1. Research & Development

- 34.2.2. Product Manufacturing

- 34.2.3. Commercialization / Go-to-Market

- 34.2.4. Sales and Marketing

- 34.3. Key Operations-related Strategies

- 34.3.1. Risk Management

- 34.3.2. Workforce

- 34.3.3. Finance

- 34.3.4. Others

SECTION VIII: OTHER EXCLUSIVE INSIGHTS

35. INSIGHTS FROM PRIMARY RESEARCH

36. REPORT CONCLUSION

SECTION IX: APPENDIX

37. TABULATED DATA

38. LIST OF COMPANIES AND ORGANIZATIONS

39. ROOTS SUBSCRIPTION SERVICES

40. AUTHOR DETAILS

医疗保健领域人工智慧 (AI) 市场到 2035 年的分析和预测:按类型、产品类型、技术、组件、应用、部署模式、最终用户、解决方案和交付模式划分。

医疗保健领域人工智慧 (AI) 市场到 2035 年的分析和预测:按类型、产品类型、技术、组件、应用、部署模式、最终用户、解决方案和交付模式划分。 全球人工智慧药物定序市场:按治疗领域、药物类型、最终用户、部署方法、国家和地区划分-产业分析、市场规模、份额和预测(2025-2032年)

全球人工智慧药物定序市场:按治疗领域、药物类型、最终用户、部署方法、国家和地区划分-产业分析、市场规模、份额和预测(2025-2032年) 人工智慧市场规模、份额及成长分析(收入週期管理):按产品类型、应用、交付方式、最终用途、地区和产业预测,2026-2033年

人工智慧市场规模、份额及成长分析(收入週期管理):按产品类型、应用、交付方式、最终用途、地区和产业预测,2026-2033年 全球生命科学人工智慧市场(至 2040 年):依部署方式、交付类型、技术类型、应用领域和主要地区划分:行业趋势和预测

全球生命科学人工智慧市场(至 2040 年):依部署方式、交付类型、技术类型、应用领域和主要地区划分:行业趋势和预测 2026年全球医疗保健领域数位助理市场报告2026年人工智慧(AI)增强型神经復健外骨骼全球市场报告2026年人工智慧(AI)赋能义肢全球市场报告2026年人工智慧(AI)赋能的扩增实境(AR)远距手术导引市场报告人工智慧在阿兹海默症早期检测市场分析及预测(至2035年):按类型、产品、服务、技术、组件、应用、设备、最终用户、部署和解决方案划分人工智慧市场分析及预测(至2035年):预测性健康分析-按类型、产品、服务、技术、组件、应用、部署、最终用户、功能和解决方案划分

2026年全球医疗保健领域数位助理市场报告2026年人工智慧(AI)增强型神经復健外骨骼全球市场报告2026年人工智慧(AI)赋能义肢全球市场报告2026年人工智慧(AI)赋能的扩增实境(AR)远距手术导引市场报告人工智慧在阿兹海默症早期检测市场分析及预测(至2035年):按类型、产品、服务、技术、组件、应用、设备、最终用户、部署和解决方案划分人工智慧市场分析及预测(至2035年):预测性健康分析-按类型、产品、服务、技术、组件、应用、部署、最终用户、功能和解决方案划分