|

市场调查报告书

商品编码

1958447

软体市场(至2035年):依软体类型、部署方式、应用开发软体、交付方式、应用模式、最终用户、公司规模、商业模式和主要地区划分-产业趋势和全球预测Software Market, Till 2035: Distribution by Type of Software, Deployment, Application Development Software, Offering, Mode of Application, End User, Company Size, Business Model, and Key Geographical Regions: Industry Trends and Global Forecasts |

||||||

全球软体市场预计将从目前的7,182.6亿美元成长到2035年的2.0889兆美元,预测期内复合年增长率(CAGR)为10.19%。

软体市场机会分类:

软体类型

- 应用软体

- 客户关係管理 (CRM)

- 教育软体

- 企业协作软体

- 企业内容管理 (ECM) 软体

- 企业资源规划 (ERP)

- 供应链管理 (SCM)

- 其他

- 系统基础设施软体

- 网路管理系统 (NMS)

- 储存软体

- 安全软体

- 开发和部署软体

- 应用程式伺服器

- 商业分析与报告工具

- 资料品质工具

- 企业资料管理 (EDM)

- 整合与编排中间件

- 生产力软体

- 创意软体

- 办公室软体

- 其他

部署模型

- 云端部署

- 混合部署

- 本地部署

应用程式开发软体

- 低程式码软体

- 无程式码软体

办公室软体

- 电子表格软体

- 可视化软体

企业软体

- 云端运算软体

- 供应链管理软体

服务类别

- 平台

- 服务

应用模式

- 企业软体

- 游戏软体

- 电子商务平台

- 教育软体

- 社群媒体应用

- 其他

最终使用者

- 银行、金融服务和保险 (BFSI)

- 能源和公用事业

- 政府与公部门

- 医疗保健

- IT和电信

- 零售

- 其他

公司规模

- 大型企业

- 中小企业

业务模式

- B2B

- B2C

- B2B2C

地理区域

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 其他北美洲国家

- 欧洲

- 奥地利

- 比利时

- 丹麦

- 法国

- 德国

- 爱尔兰

- 义大利

- 荷兰

- 挪威

- 俄罗斯

- 西班牙

- 瑞典

- 瑞士

- 英国

- 其他欧洲国家

- 亚洲

- 中国

- 印度

- 日本

- 新加坡

- 韩国

- 其他亚洲国家

- 拉丁美洲美洲

- 巴西

- 智利

- 哥伦比亚

- 委内瑞拉

- 其他拉丁美洲国家

- 中东和北非

- 埃及

- 伊朗

- 伊拉克

- 以色列

- 科威特

- 沙乌地阿拉伯

- 阿拉伯联合大公国

- 其他中东和北非国家

- 世界其他地区

- 澳大利亚

- 纽西兰

- 其他国家

软体市场:成长与趋势

软体产业是一个充满活力且快速发展的产业,它融合了尖端技术,推动众多领域的创新。该产业对于提升企业软体、云端解决方案和行动应用等各个领域的营运效率、生产力和创新能力至关重要。 随着企业向数位化平台转型,对软体解决方案的需求日益增长,这使得企业能够优化营运、增强客户互动并应对不断变化的市场环境。

对数据驱动决策和自动化的日益依赖正在推动先进软体应用的普及,从而增强企业的敏捷性和适应性。此外,对网路安全和合规性的日益重视也促使企业加大对安全软体解决方案的投资,以确保企业在遵守法律义务的同时安全运作。

高昂的开发成本、快速的技术进步和网路安全威胁等障碍依然存在。由于资源有限,中小企业往往难以应付这些挑战。儘管有这些障碍,软体市场仍然展现出巨大的成长潜力。人工智慧 (AI)、机器学习 (ML) 和物联网 (IoT) 等创新技术正在改变各行各业,为提高效率和功能提供了极具吸引力的机会。鑑于上述因素,软体市场预计在预测期内将以显着的速度成长。

本报告针对全球软体市场进行分析,提供市场概览、背景介绍、市场影响因素分析、市场规模趋势及预测、依细分市场和地区划分的详细分析、竞争格局以及主要公司简介。

目录

第一章:引言

第二章:研究方法

第三章:经济及其他专案特定考量

第四章:宏观经济指标

第五章:摘要整理

第六章:引言

第七章:竞争格局

第8章 企业简介

- 章概要

- Adobe

- Apple

- ANSYS

- Autodesk

- Alphabet

- Block

- IBM

- Intuit

- McAfee

- Microsoft

- Oracle

- Salesforce.com

- ServiceNow

第 9 章:价值链分析

第 10 章:SWOT 分析

第 11 章:全球软体市场

第 12 章:依软体类型划分的市场机会

第 13 章:依部署划分的市场机会类型

第十四章:依应用程式开发软体划分的市场机会

第十五章:以办公室软体类型划分的市场机会

第十六章:依企业软体类型划分的市场机会

第十七章:依服务细分划分的市场机会

第十八章:以应用模式划分的市场机会

第十九章:依最终使用者划分的市场机会

第二十章:依公司规模划分的市场机会

第二十一章:依商业模式划分的市场机会

第二十二章:北美软体市场机会

章节第23章:欧洲软体市场机会

第24章:亚洲软体市场机会

第25章:中东和北非软体市场机会

第26章:拉丁美洲软体市场机会

第27章:世界其他地区软体市场机会

第28章:表格资料

第29章:公司和组织列表

第30章:客製化机会

第31章:ROOTS订阅服务

第32章:作者资讯

Software Market Overview

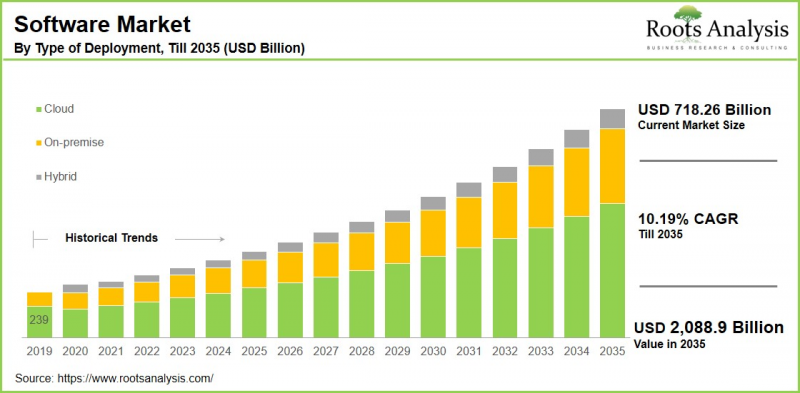

As per Roots Analysis, the global software market size is estimated to grow from USD 718.26 billion in the current year USD 2,088.9 billion by 2035, at a CAGR of 10.19% during the forecast period, till 2035.

The opportunity for software market has been distributed across the following segments:

Type of Software

- Application Software

- Customer Relationship Management (CRM)

- Education Software

- Enterprise Collaboration Software

- Enterprise Content Management (ECM) Software

- Enterprise Resource Planning (ERP)

- Supply Chain Management (SCM)

- Others

- System Infrastructure Software

- Network Management Systems (NMS)

- Storage Software

- Security Software

- Development and Deployment Software

- Application Servers

- Business Analytics & Reporting Tools

- Data Quality Tools

- Enterprise Data Management (EDM)

- Integration & Orchestration Middleware

- Productivity Software

- Creative Software

- Office Software

- Others

Type of Deployment

- Cloud

- Hybrid

- On-premises

Type of Application Development Software

- Low Code

- No Code

Type of Office Software

- Spreadsheet

- Visualization

Type of Enterprise Software

- Cloud Computing

- Supply Chain Management

Type of Offering

- Platform

- Services

Mode of Application

- Enterprise Software

- Gaming Software

- E-commerce Platforms

- Educational Software

- Social Media Applications

- Others

End User

- Banking, Financial Services, and Insurance (BFSI)

- Energy & Utilities

- Government/Public Sector

- Healthcare

- IT & Telecom

- Retail

- Others

Company Size

- Large Enterprises

- Small and Medium-sized Enterprises (SMEs)

Business Model

- B2B

- B2C

- B2B2C

Geographical Regions

- North America

- US

- Canada

- Mexico

- Other North American countries

- Europe

- Austria

- Belgium

- Denmark

- France

- Germany

- Ireland

- Italy

- Netherlands

- Norway

- Russia

- Spain

- Sweden

- Switzerland

- UK

- Other European countries

- Asia

- China

- India

- Japan

- Singapore

- South Korea

- Other Asian countries

- Latin America

- Brazil

- Chile

- Colombia

- Venezuela

- Other Latin American countries

- Middle East and North Africa

- Egypt

- Iran

- Iraq

- Israel

- Kuwait

- Saudi Arabia

- UAE

- Other MENA countries

- Rest of the World

- Australia

- New Zealand

- Other countries

Software Market: Growth and Trends

The software industry is a vibrant and swiftly changing field that revolutionizes numerous sectors by integrating cutting-edge technologies. This industry is essential for boosting operational effectiveness, productivity, and innovation across different areas, including enterprise software, cloud solutions, mobile apps, and beyond. As organizations shift towards digital platforms, the need for software solutions has amplified, allowing businesses to optimize their operations, enhance customer interactions, and respond to evolving market conditions.

The growing dependence on data-informed decision-making and automation has driven the uptake of sophisticated software applications, promoting greater agility and adaptability within companies. Moreover, the increasing focus on cybersecurity and compliance has led to higher investments in secure software solutions, ensuring that businesses can function securely while meeting legal obligations.

Obstacles such as high development expenses, fast-paced technological advancements, and cybersecurity threats continue to exist. Small and medium-sized enterprises (SMEs) frequently find it challenging to navigate these difficulties due to limited resources. Regardless of these obstacles, the software market continues to show significant growth potential. Innovations such as artificial intelligence (AI), machine learning (ML), and the internet of things (IoT) are transforming the landscape, presenting exciting opportunities for improved efficiency and functionality. Considering the above mentioned factors, the software market is expected to grow at a significant rate during the forecast period.

Software Market: Key Segments

Market Share by Type of Software

Based on type of software, the global software market is segmented into application software and system infrastructure software. According to our estimates, currently, the application software segment captures the majority of the market share. This dominance can be attributed to a surge in demand for business automation, collaboration tools, and productivity enhancements. Organizations focus on solutions that enhance functionality and user experience, rendering application software essential for operational success and digital transformation efforts.

Market Share by Type of Deployment

Based on type of deployment, the global software market is segmented into cloud, hybrid, and on-premises. According to our estimates, currently, the cloud segment captures the majority of the market share. This dominance is due to its adaptability, cost efficiency, and simplicity in scalability, enabling businesses to utilize software services remotely without substantial infrastructure costs.

Market Share by Type of Application Development Software

Based on type of application development software, the global software market is segmented into low code and no code application development software. According to our estimates, currently, the low code platforms capture the majority of the market share. This is due to the fact that low code platforms empower developers to build applications with minimal coding effort, whereas no code platforms allow users with little to no programming knowledge to create applications using visual tools.

Market Share by Type of Office Software

Based on type of office software, the global software market is segmented into spreadsheet and visualization tools. According to our estimates, currently, the spreadsheet segment captures the majority of the market share. This growth can be attributed to its extensive application in data analysis, financial modeling, and multiple business functions. Its flexibility and the common knowledge of users render it vital for productivity. Although visualization tools are becoming increasingly important for interpreting data, they still occupy a secondary position in terms of overall usage and market share.

Market Share by Type of Enterprise Software

Based on type of enterprise software, the global software market is segmented into cloud computing and supply chain management (SCM). According to our estimates, currently, the cloud computing segment captures the majority of the market share. This growth can be attributed to its adaptability, scalability, and affordability, allowing companies to utilize resources and services online. As businesses increasingly implement digital transformation strategies, cloud solutions enhance remote work and collaborative efforts. Although SCM plays a vital role in streamlining logistics and operations, the widespread adoption of cloud technologies reinforces its dominant position in the industry.

Market Share by Type of Offering

Based on type of offering, the global software market is segmented into platform and services. According to our estimates, currently, the platform segment captures the majority of the market share. This growth can be attributed to the fact that it includes all-encompassing solutions that equip users with a range of tools for development, integration, and deployment, promoting innovation and scalability. Although services, such as support, consulting, and customization, are essential, they often act as a supplement to the platforms. The rising demand for integrated solutions is a significant factor driving the preference for platform offerings within the market.

Market Share by Mode of Application

Based on mode of application, the global software market is segmented into enterprise software, gaming software, e-commerce platforms, educational software, social media applications, and others. According to our estimates, currently, the enterprise software captures the majority of the market share. This growth can be attributed to its vital role in boosting organizational efficiency, supporting data management, and enhancing productivity. The increasing focus on digital transformation among businesses fuels the need for solutions like customer relationship management (CRM) and enterprise resource planning (ERP), making enterprise software crucial for maintaining a competitive edge.

Market Share by End User

Based on end user, the global software market is segmented into banking, financial services, and insurance (BFSI), energy & utilities, government/public sector, healthcare, it & telecom, retail, and others. According to our estimates, currently, the BFSI segment captures the majority of the market share. This growth can be attributed to its significant dependence on software for operational tasks, regulatory compliance, risk management, and engaging with customers. The growing demand for cybersecurity measures, adherence to regulations, and digital banking solutions is fueling this expansion.

Market Share by Company Size

Based on company size, the global software market is segmented into large companies, and small and mid-size companies. According to our estimates, currently, the large companies capture the majority of the market share. This growth can be attributed to the fact that large companies possess the resources and capabilities to invest significantly in research and development, production infrastructure, and marketing, which allows them to offer software at a lower cost per unit compared to their smaller counterparts.

In addition, software solutions available for medium and small businesses serve as affordable, high-quality alternatives. This segment is projected to grow by 2035 due to a rising demand and the increased availability of superior software in the market.

Market Share by Business Model

Based on business model, the global software market is segmented into B2B, B2C and B2B2C. According to our estimates, currently, the B2B segment captures the majority of the market share. This growth can be attributed to the rising incorporation of software technology across various industries, including aerospace, manufacturing, healthcare, finance, and more.

In addition, the B2C model is projected to experience a higher CAGR during this forecast period, driven by the increasing user-friendliness of software technologies and the growing consumer preference for personalized applications, smartphone compatibility, and enhanced user experiences.

Market Share by Geographical Regions

Based on geographical regions, the software market is segmented into North America, Europe, Asia, Latin America, Middle East and North Africa, and the rest of the world. According to our estimates, currently North America captures the majority share of the market. This dominance can be linked to its sophisticated technology infrastructure and innovative businesses that promote the creation and use of software solutions. Furthermore, many top software companies are based in North America, utilizing state-of-the-art technology and research to sustain their competitive advantage. The region also features a sizable and varied market across different industries, such as education and corporate sectors, offering numerous opportunities for software providers to address a wide range of clients.

Example Players in Software Market

- Adobe

- Aplle

- ANSYS

- Autodesk

- Alphabet

- Block

- CA Technologies

- Dassault Systemes

- IBM

- Intuit

- McAfee

- Microsoft

- Norton LifeLock

- Oracle

- Open Text

- Red Hat

- SAP SE

- Salesforce.com

- ServiceNow

- Splunk

- Symantec

- Synopsys

- VMware

Software Market: Research Coverage

The report on the software market features insights on various sections, including:

- Market Sizing and Opportunity Analysis: An in-depth analysis of the software market, focusing on key market segments, including [A] type of software, [B] type of deployment, [C] type of application development software, [D] type of office software, [E] type of enterprise software, [F] type of offering, [G] mode of application, [H] end user, [I] company size, [J] type of business model, [K] and key geographical regions.

- Competitive Landscape: A comprehensive analysis of the companies engaged in the software market, based on several relevant parameters, such as [A] year of establishment, [B] company size, [C] location of headquarters and [D] ownership structure.

- Company Profiles: Elaborate profiles of prominent players engaged in the software market, providing details on [A] location of headquarters, [B] company size, [C] company mission, [D] company footprint, [E] management team, [F] contact details, [G] financial information, [H] operating business segments, [I] portfolio, [J] moat analysis, [K] recent developments, and an informed future outlook.

- Megatrends: An evaluation of ongoing megatrends in the software industry.

- Patent Analysis: An insightful analysis of patents filed / granted in the software domain, based on relevant parameters, including [A] type of patent, [B] patent publication year, [C] patent age and [D] leading players.

- Recent Developments: An overview of the recent developments made in the software market, along with analysis based on relevant parameters, including [A] year of initiative, [B] type of initiative, [C] geographical distribution and [D] most active players.

- Porter's Five Forces Analysis: An analysis of five competitive forces prevailing in the software market, including threats of new entrants, bargaining power of buyers, bargaining power of suppliers, threats of substitute products and rivalry among existing competitors.

- SWOT Analysis: An insightful SWOT framework, highlighting the strengths, weaknesses, opportunities and threats in the domain. Additionally, it provides Harvey ball analysis, highlighting the relative impact of each SWOT parameter.

- Value Chain Analysis: A comprehensive analysis of the value chain, providing information on the different phases and stakeholders involved in the software market.

Key Questions Answered in this Report

- How many companies are currently engaged in software market?

- Which are the leading companies in this market?

- What factors are likely to influence the evolution of this market?

- What is the current and future market size?

- What is the CAGR of this market?

- How is the current and future market opportunity likely to be distributed across key market segments?

Reasons to Buy this Report

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. By analyzing the competitive landscape, businesses can make informed decisions to optimize their market positioning and develop effective go-to-market strategies.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

Additional Benefits

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 15% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

1. PREFACE

- 1.1. Introduction

- 1.2. Market Share Insights

- 1.3. Key Market Insights

- 1.4. Report Coverage

- 1.5. Key Questions Answered

- 1.6. Chapter Outlines

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Introduction

- 2.4.2.2. Types

- 2.4.2.2.1. Qualitative

- 2.4.2.2.2. Quantitative

- 2.4.2.3. Advantages

- 2.4.2.4. Techniques

- 2.4.2.4.1. Interviews

- 2.4.2.4.2. Surveys

- 2.4.2.4.3. Focus Groups

- 2.4.2.4.4. Observational Research

- 2.4.2.4.5. Social Media Interactions

- 2.4.2.5. Stakeholders

- 2.4.2.5.1. Company Executives (CXOs)

- 2.4.2.5.2. Board of Directors

- 2.4.2.5.3. Company Presidents and Vice Presidents

- 2.4.2.5.4. Key Opinion Leaders

- 2.4.2.5.5. Research and Development Heads

- 2.4.2.5.6. Technical Experts

- 2.4.2.5.7. Subject Matter Experts

- 2.4.2.5.8. Scientists

- 2.4.2.5.9. Doctors and Other Healthcare Providers

- 2.4.2.6. Ethics and Integrity

- 2.4.2.6.1. Research Ethics

- 2.4.2.6.2. Data Integrity

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

3. ECONOMIC AND OTHER PROJECT SPECIFIC CONSIDERATIONS

- 3.1. Forecast Methodology

- 3.1.1. Top-Down Approach

- 3.1.2. Bottom-Up Approach

- 3.1.3. Hybrid Approach

- 3.2. Market Assessment Framework

- 3.2.1. Total Addressable Market (TAM)

- 3.2.2. Serviceable Addressable Market (SAM)

- 3.2.3. Serviceable Obtainable Market (SOM)

- 3.2.4. Currently Acquired Market (CAM)

- 3.3. Forecasting Tools and Techniques

- 3.3.1. Qualitative Forecasting

- 3.3.2. Correlation

- 3.3.3. Regression

- 3.3.4. Time Series Analysis

- 3.3.5. Extrapolation

- 3.3.6. Convergence

- 3.3.7. Forecast Error Analysis

- 3.3.8. Data Visualization

- 3.3.9. Scenario Planning

- 3.3.10. Sensitivity Analysis

- 3.4. Key Considerations

- 3.4.1. Demographics

- 3.4.2. Market Access

- 3.4.3. Reimbursement Scenarios

- 3.4.4. Industry Consolidation

- 3.5. Robust Quality Control

- 3.6. Key Market Segmentations

- 3.7. Limitations

4. MACRO-ECONOMIC INDICATORS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Overview of Major Currencies Affecting the Market

- 4.2.2.2. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Exchange Impact

- 4.2.3.1. Evaluation of Foreign Exchange Rates and Their Impact on Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.4.2. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.6. Interest Rates

- 4.2.6.1. Overview of Interest Rates and Their Impact on the Market

- 4.2.6.2. Strategies for Managing Interest Rate Risk

- 4.2.7. Commodity Flow Analysis

- 4.2.7.1. Type of Commodity

- 4.2.7.2. Origins and Destinations

- 4.2.7.3. Values and Weights

- 4.2.7.4. Modes of Transportation

- 4.2.8. Global Trade Dynamics

- 4.2.8.1. Import Scenario

- 4.2.8.2. Export Scenario

- 4.2.9. War Impact Analysis

- 4.2.9.1. Russian-Ukraine War

- 4.2.9.2. Israel-Hamas War

- 4.2.10. COVID Impact / Related Factors

- 4.2.10.1. Global Economic Impact

- 4.2.10.2. Industry-specific Impact

- 4.2.10.3. Government Response and Stimulus Measures

- 4.2.10.4. Future Outlook and Adaptation Strategies

- 4.2.11. Other Indicators

- 4.2.11.1. Fiscal Policy

- 4.2.11.2. Consumer Spending

- 4.2.11.3. Gross Domestic Product (GDP)

- 4.2.11.4. Employment

- 4.2.11.5. Taxes

- 4.2.11.6. R&D Innovation

- 4.2.11.7. Stock Market Performance

- 4.2.11.8. Supply Chain

- 4.2.11.9. Cross-Border Dynamics

- 4.2.1. Time Period

5. EXECUTIVE SUMMARY

6. INTRODUCTION

- 6.1. Chapter Overview

- 6.2. Overview of Software Market

- 6.2.1. Key Characteristics of Software Market

- 6.2.2. Type of Product

- 6.2.3. Type of Usage

- 6.2.4. Category of Modem

- 6.2.5. Location of Installation

- 6.2.6. Type of Device

- 6.2.7. Type of Network

- 6.2.8. Type of Industry

- 6.2.9. Mode of Application

- 6.2.10. Type of End User

- 6.3. Future Perspective

7. COMPETITIVE LANDSCAPE

- 7.1. Chapter Overview

- 7.2. Software: Overall Market Landscape

- 7.2.1. Analysis by Year of Establishment

- 7.2.2. Analysis by Company Size

- 7.2.3. Analysis by Location of Headquarters

- 7.2.4. Analysis by Ownership Structure

8. COMPANY PROFILES

- 8.1. Chapter Overview

- 8.2. Adobe*

- 8.2.1. Company Overview

- 8.2.2. Company Mission

- 8.2.3. Company Footprint

- 8.2.4. Management Team

- 8.2.5. Contact Details

- 8.2.6. Financial Performance

- 8.2.7. Operating Business Segments

- 8.2.8. Service / Product Portfolio (project specific)

- 8.2.9. MOAT Analysis

- 8.2.10. Recent Developments and Future Outlook

- 8.3. Apple

- 8.4. ANSYS

- 8.5. Autodesk

- 8.6. Alphabet

- 8.7. Block

- 8.8. IBM

- 8.9. Intuit

- 8.10. McAfee

- 8.11. Microsoft

- 8.12. Oracle

- 8.13. Salesforce.com

- 8.14. ServiceNow

9. VALUE CHAIN ANALYSIS

10. SWOT ANALYSIS

11. GLOBAL SOFTWARE MARKET

- 11.1. Chapter Overview

- 11.2. Key Assumptions and Methodology

- 11.3. Trends Disruption Impacting Market

- 11.4. Global Software Market, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 11.5. Multivariate Scenario Analysis

- 11.5.1. Conservative Scenario

- 11.5.2. Optimistic Scenario

- 11.6. Key Market Segmentations

12. MARKET OPPORTUNITIES BASED ON TYPE OF SOFTWARE

- 12.1. Chapter Overview

- 12.2. Key Assumptions and Methodology

- 12.3. Revenue Shift Analysis

- 12.4. Market Movement Analysis

- 12.5. Penetration-Growth (P-G) Matrix

- 12.6. Software Market for Application Software: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 12.7. Software Market for System Infrastructure Software: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 12.8. Software Market for Development and Deployment Software: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 12.9. Software Market for Productivity Software: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 12.10. Data Triangulation and Validation

13. MARKET OPPORTUNITIES BASED ON TYPE OF DEPLOYMENT

- 13.1. Chapter Overview

- 13.2. Key Assumptions and Methodology

- 13.3. Revenue Shift Analysis

- 13.4. Market Movement Analysis

- 13.5. Penetration-Growth (P-G) Matrix

- 13.6. Software Market for Cloud: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 13.7. Software Market for Hybrid: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 13.8. Software Market for On-Premises: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 13.9. Data Triangulation and Validation

14. MARKET OPPORTUNITIES BASED ON TYPE OF APPLICATION DEVELOPMENT SOFTWARE

- 14.1. Chapter Overview

- 14.2. Key Assumptions and Methodology

- 14.3. Revenue Shift Analysis

- 14.4. Market Movement Analysis

- 14.5. Penetration-Growth (P-G) Matrix

- 14.6. Software Market for Low Code: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 14.7. Software Market for No Code: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 14.8. Data Triangulation and Validation

15. MARKET OPPORTUNITIES BASED ON TYPE OF OFFICE SOFTWARE

- 15.1. Chapter Overview

- 15.2. Key Assumptions and Methodology

- 15.3. Revenue Shift Analysis

- 15.4. Market Movement Analysis

- 15.5. Penetration-Growth (P-G) Matrix

- 15.6. Software Market for Spreadsheet: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 15.7. Software Market for Visualization: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 15.8. Data Triangulation and Validation

16. MARKET OPPORTUNITIES BASED ON TYPE OF ENTERPRISE SOFTWARE

- 16.1. Chapter Overview

- 16.2. Key Assumptions and Methodology

- 16.3. Revenue Shift Analysis

- 16.4. Market Movement Analysis

- 16.5. Penetration-Growth (P-G) Matrix

- 16.6. Software Market for Cloud Computing: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 16.7. Software Market for Supply Chain Management: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 16.8. Data Triangulation and Validation

17. MARKET OPPORTUNITIES BASED ON TYPE OF OFFERING

- 17.1. Chapter Overview

- 17.2. Key Assumptions and Methodology

- 17.3. Revenue Shift Analysis

- 17.4. Market Movement Analysis

- 17.5. Penetration-Growth (P-G) Matrix

- 17.6. Software Market for Platform: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 17.7. Software Market for Services: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 17.8. Data Triangulation and Validation

18. MARKET OPPORTUNITIES BASED ON MODE OF APPLICATION

- 18.1. Chapter Overview

- 18.2. Key Assumptions and Methodology

- 18.3. Revenue Shift Analysis

- 18.4. Market Movement Analysis

- 18.5. Penetration-Growth (P-G) Matrix

- 18.6. Software Market for Enterprise Software: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 18.7. Software Market for Gaming Software: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 18.8. Software Market for E-commerce Platforms: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 18.9. Software Market for Educational Software: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 18.10. Software Market for Social Media Applications: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 18.11. Software Market for Others: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 18.12. Data Triangulation and Validation

19. MARKET OPPORTUNITIES BASED ON END USER

- 19.1. Chapter Overview

- 19.2. Key Assumptions and Methodology

- 19.3. Revenue Shift Analysis

- 19.4. Market Movement Analysis

- 19.5. Penetration-Growth (P-G) Matrix

- 19.6. Software Market for BFSI: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.7. Software Market for Energy and Utility: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.8. Software Market for Government/Public Sector: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.9. Software Market for Healthcare: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.10. Software Market for IT & Telecom: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.11. Software Market for Retail: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.12. Software Market for Others: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.13. Data Triangulation and Validation

20. MARKET OPPORTUNITIES BASED ON COMPANY SIZE

- 20.1. Chapter Overview

- 20.2. Key Assumptions and Methodology

- 20.3. Revenue Shift Analysis

- 20.4. Market Movement Analysis

- 20.5. Penetration-Growth (P-G) Matrix

- 20.6. Software Market for Large Enterprises: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 20.7. Software Market for Small and Medium-sized Enterprises (SMEs): Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 20.8. Data Triangulation and Validation

21. MARKET OPPORTUNITIES BASED ON BUSINESS MODEL

- 21.1. Chapter Overview

- 21.2. Key Assumptions and Methodology

- 21.3. Revenue Shift Analysis

- 21.4. Market Movement Analysis

- 21.5. Penetration-Growth (P-G) Matrix

- 21.6. Software Market for B2B: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.7. Software Market for B2C: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.8. Software Market for B2B2C: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.9. Data Triangulation and Validation

22. MARKET OPPORTUNITIES FOR SOFTWARE IN NORTH AMERICA

- 22.1. Chapter Overview

- 22.2. Key Assumptions and Methodology

- 22.3. Revenue Shift Analysis

- 22.4. Market Movement Analysis

- 22.5. Penetration-Growth (P-G) Matrix

- 22.6. Software Market in North America: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.6.1. Software Market in the US: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.6.2. Software Market in Canada: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.6.3. Software Market in Mexico: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.6.4. Software Market in Other North American Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.7. Data Triangulation and Validation

23. MARKET OPPORTUNITIES FOR SOFTWARE IN EUROPE

- 23.1. Chapter Overview

- 23.2. Key Assumptions and Methodology

- 23.3. Revenue Shift Analysis

- 23.4. Market Movement Analysis

- 23.5. Penetration-Growth (P-G) Matrix

- 23.6. Software Market in Europe: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.1. Software Market in the Austria: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.2. Software Market in Belgium: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.3. Software Market in Denmark: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.4. Software Market in France: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.5. Software Market in Germany: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.6. Software Market in Ireland: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.7. Software Market in Italy: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.8. Software Market in Netherlands: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.9. Software Market in Norway: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.10. Software Market in Russia: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.11. Software Market in Spain: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.12. Software Market in Sweden: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.13. Software Market in Switzerland: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.14. Software Market in the UK: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.15. Software Market in Other European Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.7. Data Triangulation and Validation

24. MARKET OPPORTUNITIES FOR SOFTWARE IN ASIA

- 24.1. Chapter Overview

- 24.2. Key Assumptions and Methodology

- 24.3. Revenue Shift Analysis

- 24.4. Market Movement Analysis

- 24.5. Penetration-Growth (P-G) Matrix

- 24.6. Software Market in Asia: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.1. Software Market in China: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.2. Software Market in India: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.3. Software Market in Japan: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.4. Software Market in Singapore: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.5. Software Market in South Korea: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.6. Software Market in Other Asian Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.7. Data Triangulation and Validation

25. MARKET OPPORTUNITIES FOR SOFTWARE IN MIDDLE EAST AND NORTH AFRICA (MENA)

- 25.1. Chapter Overview

- 25.2. Key Assumptions and Methodology

- 25.3. Revenue Shift Analysis

- 25.4. Market Movement Analysis

- 25.5. Penetration-Growth (P-G) Matrix

- 25.6. Software Market in Middle East and North Africa (MENA): Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.1. Software Market in Egypt: Historical Trends (Since 2019) and Forecasted Estimates (Till 205)

- 25.6.2. Software Market in Iran: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.3. Software Market in Iraq: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.4. Software Market in Israel: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.5. Software Market in Kuwait: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.6. Software Market in Saudi Arabia: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.7. Software Market in United Arab Emirates (UAE): Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.8. Software Market in Other MENA Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.7. Data Triangulation and Validation

26. MARKET OPPORTUNITIES FOR SOFTWARE IN LATIN AMERICA

- 26.1. Chapter Overview

- 26.2. Key Assumptions and Methodology

- 26.3. Revenue Shift Analysis

- 26.4. Market Movement Analysis

- 26.5. Penetration-Growth (P-G) Matrix

- 26.6. Software Market in Latin America: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.1. Software Market in Argentina: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.2. Software Market in Brazil: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.3. Software Market in Chile: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.4. Software Market in Colombia Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.5. Software Market in Venezuela: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.6.6. Software Market in Other Latin American Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 26.7. Data Triangulation and Validation

27. MARKET OPPORTUNITIES FOR SOFTWARE IN REST OF THE WORLD

- 27.1. Chapter Overview

- 27.2. Key Assumptions and Methodology

- 27.3. Revenue Shift Analysis

- 27.4. Market Movement Analysis

- 27.5. Penetration-Growth (P-G) Matrix

- 27.6. Software Market in Rest of the World: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.6.1. Software Market in Australia: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.6.2. Software Market in New Zealand: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 27.6.3. Software Market in Other Countries

- 27.7. Data Triangulation and Validation