|

市场调查报告书

商品编码

1498832

全球介电前驱体(关键材料)市场,2024-2025Dielectric Precursors Market Report 2024-2025 (Critical Materials Report) |

||||||

价格

该报告涵盖了半导体装置製造中使用的前驱物的市场趋势和供应链。包含主要供应商的资讯、材料供应链的问题和趋势、供应商市场占有率的估计和预测、材料细分市场的预测等。

样本视图

目录

第1章 内容提要

第2章 研究范围、目的与方法

第3章 半导体产业:市场现况与前景

- 世界经济与展望

- 半导体产业与全球经济的连结

- 半导体销售额成长

- 台湾外包厂商每月销售趋势

- 晶片销售额:依电子产品领域划分

- 电子展望

- 汽车产业展望

- 智慧型手机前景

- 电脑展望

- 伺服器/IT市场

- 半导体製造业的成长与扩张

- 晶片扩产投入大量资金

- 美国新工厂

- 世界各地製造工厂的扩张推动成长

- 资本投资趋势

- 先进逻辑技术路线图

- 评估製造工厂投资

- 政策/贸易趋势和影响

- 半导体材料概述

- 预测引入的晶圆数量(到 2028 年)

- 材料市场预测(~2028)

第4章 材料市场趋势

- CVD/ALD/金属:High-K和先进电介质前驱体市场趋势

- 2023 年前驱体市场:与 2024 年的联繫

- 开拓市场前景

- 电介质前驱体出货量预测:依细分市场(未来 5 年)

- 顶级供应商电介质产量

- 电介质产量:依地区划分

- 扩大ALD/CVD材料产能

- 投资公告摘要

- 价格趋势

- 技术趋势/技术推动因素—概述

- 前驱物的整体技术概述:技术趋势

- 客户驱动的技术

- NAND 路线图与课题:堆迭/分层 3D NAND 级别

- 3D NAND 製程需要进步

- Micron推出突破性 NVDRAM:双层 32 GB 非挥发性铁电记忆体,具有类似 DRAM 的效能

- 先进逻辑路线图与课题:逻辑电晶体EST.Roadmap

- 高阶逻辑(代工)节点 HVM 估算

- 高阶逻辑:未来的技术课题

- 光刻技术进步的影响

- CFET 架构:CFET 扩展的优势

- 无机 EUV 光阻:旋涂沉积

- SADP(自对准多重模式)

- EUV/多重图案化/地缘政治

- 区域选择性沉积(ASD)

- 特殊/新兴介电材料及应用领域

- 区域考虑因素:电介质

- 区域因素和驱动因素

- EHS 与贸易/物流问题 - 金属、高 K、电介质

- 分析师对介电市场趋势的评估

第5章 供给侧市场情势

- 前驱体材料市占率

- 当前季度活动 - MERCK

- 当前季度活动 - 液化空气集团

- 本季活动 - ENTEGRIS

- ADEKA

- 併购活动和伙伴关係

- 工厂关闭

- 新进入者

- MSP 推出 TURBO II (TM) 蒸发器:半导体製造的下一代效率

- 供应商或零件/产品线面临停产风险

- 领先供应商的分析师评估

第6章 次级(下层)供应链/前体

- 细分供应链:供应商与市场概述

- 次级供应链:供应商和市场概况 - 二级案例研究 (NOURYON/GELEST)

- Subtier 供应链:供应商和市场概况 - 化学品和气体管理系统

- Subtier 供应链:供应商和市场概览 - 化学品交付柜

- Subtier 供应链:供应商和市场概览 - 阀门歧管盒 (VMB)

- Subtier 供应链:供应商和市场概况 - 散装规格气体系统

- Subtier 供应链:供应商和市场概况 - 气柜

- Subtier 供应链:供应商和市场概况 - 成型气体和掺杂气体混合器

- Subtier 供应链:供应商和市场概况 - 化学监测和分析系统

- 高级材料:CVD-ALD 前驱体的趋势

- 精细材质:工业级与半导体级

- 半导体级次级材料供应商的国际网络:Merck

- 半导体级次级材料供应商的国际网路:Air Liquide

- 半导体级次级材料供应商最新讯息

- 供应链颠覆者

- 次级供应链T:分析师评估

第七章 供应商简介

- ADEKA CORPORATION

- AIR LIQUIDE (MAKER, PURIFIER, SUPPLIER)

- AZMAX CO., LTD

- CITY CHEMICAL LLC

- DNF CO., LTD

- 其他20多家企业

This report covers the market landscape and supply-chain for Precursors used in semiconductor device fabrication. It includes information about key suppliers, issues/trends in the material supply chain, estimates on supplier market share, and forecast for the material segments.

SAMPLE VIEW

Table of Contents

1 Executive Summary

- 1.1 PRECURSORS BUSINESS - MARKET OVERVIEW

- 1.2 PRECURSORS MARKET TRENDS IMPACTING 2024 OUTLOOK

- 1.3 5-YEAR UNIT SHIPMENT FORECAST BY SEGMENT: DIELECTRIC PRECURSORS

- 1.4 PRECURSOR TRENDS

- 1.5 PRECURSOR TECHNOLOGY TRENDS

- 1.6 COMPETITIVE LANDSCAPE DIELECTRIC PRECURSORS

- 1.7 ANALYST ASSESSMENT OF DIELECTRIC PRECURSORS

2 Scope, Purpose, and Methodology

- 2.1 SCOPE

- 2.2 METHODOLOGY

- 2.3 OVERVIEW OF OTHER TECHCET CMR(TM) OFFERINGS

3 Semiconductor Industry Market Status & Outlook

- 3.1 WORLDWIDE ECONOMY AND OUTLOOK

- 3.1.1 SEMICONDUCTOR INDUSTRIES TIES TO THE GLOBAL ECONOMY

- 3.1.2 SEMICONDUCTOR SALES GROWTH

- 3.1.3 TAIWAN OUTSOURCE MANUFACTURER MONTHLY SALES TRENDS

- 3.2 CHIPS SALES BY ELECTRONIC GOODS SEGMENT

- 3.2.1 ELECTRONICS OUTLOOK

- 3.2.2 AUTOMOTIVE INDUSTRY OUTLOOK

- 3.2.2.1 ELECTRIC VEHICLE (EV) MARKET TRENDS

- 3.2.2.2 INCREASE IN SEMICONDUCTOR CONTENT FOR AUTOS

- 3.2.3 SMARTPHONE OUTLOOK

- 3.2.4 PC OUTLOOK

- 3.2.5 SERVERS / IT MARKET

- 3.3 SEMICONDUCTOR FABRICATION GROWTH - EXPANSION

- 3.3.1 IN THE MIDST OF HUGE INVESTMENT IN CHIP EXPANSIONS

- 3.3.2 NEW FABS IN THE US

- 3.3.3 WW FAB EXPANSION DRIVING GROWTH

- 3.3.4 EQUIPMENT SPENDING TRENDS

- 3.3.5 ADVANCED LOGIC TECHNOLOGY ROADMAPS

- 3.3.5.1 DRAM TECHNOLOGY ROADMAPS

- 3.3.5.2 3D NAND TECHNOLOGY ROADMAPS

- 3.3.6 FAB INVESTMENT ASSESSMENT

- 3.4 POLICY & TRADE TRENDS AND IMPACT

- 3.5 SEMICONDUCTOR MATERIALS OVERVIEW

- 3.5.1 TECHCET WAFER STARTS FORECAST THROUGH 2028

- 3.5.2 TECHCET MATERIALS MARKET FORECAST THROUGH 2028

4 Material Market Trends

- 4.1 CVD, ALD METAL - HIGH-K AND ADVANCED DIELECTRIC PRECURSORS MARKET TRENDS

- 4.1.1 2023 PRECURSOR MARKET LEADING INTO 2024

- 4.1.2 PRECURSOR MARKET OUTLOOK

- 4.1.3 DIELECTRIC PRECURSORS 5-YEAR UNIT SHIPMENT FORECAST BY SEGMENT

- 4.1.4 DIELECTRIC PRODUCTION OF TOP SUPPLIERS

- 4.1.5 DIELECTRIC PRODUCTION BY REGION

- 4.1.6 ALD/CVD MATERIAL PRODUCTION CAPACITY EXPANSIONS

- 4.1.7 INVESTMENT ANNOUNCEMENTS OVERVIEW

- 4.2 PRICING TRENDS

- 4.3 TECHNOLOGY TRENDS/TECHNICAL DRIVERS - OUTLINE

- 4.3.1 PRECURSOR GENERAL TECHNOLOGY OVERVIEW - TECHNOLOGY TRENDS

- 4.3.2 CUSTOMER DRIVEN TECHNOLOGIES

- 4.3.3 NAND ROADMAPS AND CHALLENGES - 3D NAND LEVELS W/ STACKS/TIERS

- 4.3.4 3D NAND PROCESS ADVANCES REQUIRED

- 4.3.5 MICRON UNVEILS BREAKTHROUGH NVDRAM: A DUAL-LAYER 32GBIT NON-VOLATILEFERROELECTRIC MEMORY WITH NEAR-DRAM PERFORMANCE

- 4.3.6 ADVANCED LOGIC ROADMAPS AND CHALLENGES - LOGIC TRANSISTOR EST. ROADMAP

- 4.3.7 ADVANCED LOGIC (FOUNDRY) NODE HVM ESTIMATE

- 4.3.7.1 THE SEMICONDUCTOR SHOWDOWN: SAMSUNG AND TSMC'S GAA FETS VS. INTEL'S RIBBONFET

- 4.3.8 ADV LOGIC FUTURE TECHNOLOGY CHALLENGES

- 4.3.9 ADVANCING TECHNOLOGIES IMPLICATION TO PHOTOLITHOGRAPHY

- 4.3.9.1 ADVANCING TECHNOLOGIES IMPLICATION TO PHOTOLITHOGRAPHY - DSA

- 4.3.9.2 ADVANCING TECHNOLOGIES IMPLICATION TO PHOTOLITHOGRAPHY: CENTURA SCULPTA BY APPLIED MATERIALS: SHAPING THE FUTURE OF SEMICONDUCTOR MANUFACTURING

- 4.3.9.3 ADVANCING TECHNOLOGIES IMPLICATION TO PHOTOLITHOGRAPHY: LINE EDGE ROUGHNESS REDUCTION THRU DEPOSITION

- 4.3.10 CFET ARCHITECTURE: CFET SCALING ADVANTAGE

- 4.3.10.1 CFET ARCHITECTURE: COMPLEMENTARY FETS (CFETS)

- 4.3.10.2 CFET ARCHITECTURE: CFET FUTURE PROSPECTS

- 4.3.11 INORGANIC EUV RESIST - SPIN ON DEPOSITION

- 4.3.11.1 INORGANIC EUV RESIST - ALD DEPOSITED

- 4.3.12 SELF ALIGNED MULTI PATTERNING - SADP

- 4.3.12.1 SELF ALIGNED MULTI PATTERNING - SAQP

- 4.3.12.2 SELF ALIGNED MULTI PATTERNING - PEALD EQUIPMENT

- 4.3.12.3 SELF ALIGNED MULTI PATTERNING - CAN SAQP BYPASS EUV BEYOND 7 NM?

- 4.3.13 EUV, MULTI PATTERNING AND GEOPOLITICS

- 4.3.14 AREA SELECTIVE DEPOSITION (ASD)

- 4.3.14.1 AREA SELECTIVE DEPOSITION (ASD) - TU EINDHOVEN SELECTIVE ALD ENABLED BY PLASMA PRETREATMENT

- 4.3.15 SPECIALTY/EMERGING DIELECTRIC AND APPLICATIONS

- 4.3.16 REGIONAL CONSIDERATIONS - DIELECTRICS

- 4.3.17 REGIONAL ASPECTS AND DRIVERS

- 4.4 EHS AND TRADE/LOGISTIC ISSUES - METALS, HIGH-K AND DIELECTRICS

- 4.5 ANALYST ASSESSMENT OF DIELECTRIC MARKET TRENDS

5 Supply-Side Market Landscape

- 5.1 PRECURSOR MATERIAL MARKET SHARE

- 5.1.1 CURRENT QUARTER ACTIVITY - MERCK

- 5.1.1.1 MERCK

- 5.1.2 CURRENT QUARTER ACTIVITY - AIR LIQUIDE

- 5.1.2.1 AIR LIQUIDE

- 5.1.3 CURRENT QUARTER ACTIVITY -ENTEGRIS

- 5.1.3.1 ENTEGRIS

- 5.1.4 ADEKA

- 5.1.4.1 ADEKA

- 5.1.1 CURRENT QUARTER ACTIVITY - MERCK

- 5.2 M-A ACTIVITY AND PARTNERSHIPS

- 5.3 PLANT CLOSURES

- 5.4 NEW ENTRANTS

- 5.4.1 MSP LAUNCHES TURBO II(TM) VAPORIZERS: NEXT-GEN EFFICIENCY FOR SEMICONDUCTOR FABRICATION

- 5.5 SUPPLIERS OR PARTS/PRODUCT LINES THAT ARE AT RISK OF DISCONTINUATIONS

- 5.6 TECHCET ANALYST ASSESSMENT OF PRECURSOR SUPPLIERS

6 Sub Tier Supply Chain, Precursors

- 6.1 SUB-TIER SUPPLY CHAIN: SOURCES & MARKETS OVERVIEW

- 6.1.1 SUB-TIER SUPPLY CHAIN: SOURCES & MARKETS OVERVIEW - TIER 2 EXAMPLES NOURYON AND GELEST

- 6.1.2 SUB-TIER SUPPLY CHAIN: SOURCES & MARKETS OVERVIEW - CHEMICAL & GAS MANAGEMENT SYSTEMS

- 6.1.3 SUB-TIER SUPPLY CHAIN: SOURCES & MARKETS OVERVIEW - CHEMICAL DELIVERY CABINETS

- 6.1.4 SUB-TIER SUPPLY CHAIN: SOURCES & MARKETS OVERVIEW - VALVE MANIFOLD BOXES (VMB)

- 6.1.5 SUB-TIER SUPPLY CHAIN: SOURCES & MARKETS OVERVIEW - BULK SPEC GAS SYSTEMS

- 6.1.6 SUB-TIER SUPPLY CHAIN: SOURCES & MARKETS OVERVIEW - GAS CABINETS

- 6.1.7 SUB-TIER SUPPLY CHAIN: SOURCES & MARKETS OVERVIEW - FORMING GAS & DOPANT GAS BLENDERS

- 6.1.8 SUB-TIER SUPPLY CHAIN: SOURCES & MARKETS OVERVIEW CHEMICAL - MONITORING AND ANALYTICAL SYSTEMS

- 6.2 SUB-TIER MATERIAL CVD - ALD PRECURSOR TRENDS

- 6.3 SUB-TIER MATERIAL INDUSTRIAL VS. SEMICONDUCTOR-GRADE

- 6.4 SEMICONDUCTOR-GRADE SUB-TIER MATERIAL SUPPLIER GLOBAL NETWORK MERCK

- 6.5 SEMICONDUCTOR-GRADE SUB-TIER MATERIAL SUPPLIER GLOBAL NETWORK AIR LIQUIDE

- 6.6 SEMICONDUCTOR-GRADE SUB-TIER MATERIAL SUPPLIER NEWS

- 6.7 SUB-TIER SUPPLY-CHAIN DISRUPTORS

- 6.8 SUB-TIER SUPPLY-CHAIN TECHCET ANALYST ASSESSMENT

7 Supplier profiles

- ADEKA CORPORATION

- AIR LIQUIDE (MAKER, PURIFIER, SUPPLIER)

- AZMAX CO., LTD

- CITY CHEMICAL LLC

- DNF CO., LTD

- ...and 20+ more

LIST OF FIGURES

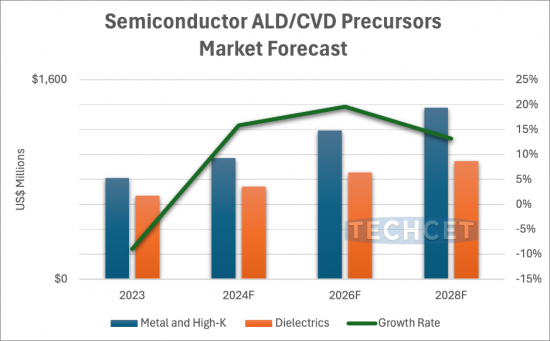

- FIGURE 1.1: DIELECTRIC PRECURSOR REVENUE (M USD) FORECAST BY SEGMENT

- FIGURE 1.2: WW MARKET SHARE - DIELECTRIC PRECURSORS 2023

- FIGURE 3.1: GLOBAL ECONOMY AND THE ELECTRONICS SUPPLY CHAIN (2023)

- FIGURE 3.2: WORLDWIDE SEMICONDUCTOR SALES

- FIGURE 3.3: TECHCET'S TAIWAN SEMICONDUCTOR INDUSTRY INDEX (TTSI)

- FIGURE 3.4: 2023 SEMICONDUCTOR CHIP APPLICATIONS

- FIGURE 3.5: GLOBAL LIGHT VEHICLE UNIT SALES (IN MILLIONS OF UNITS)

- FIGURE 3.6: ELECTRIFICATION TREND BY WORLD REGION

- FIGURE 3.7: AUTOMOTIVE SEMICONDUCTOR PRODUCTION

- FIGURE 3.8: MOBILE PHONE SHIPMENTS, WW ESTIMATES

- FIGURE 3.9: WORLDWIDE PC AND TABLET FORECAST

- FIGURE 3.10: TSMC PHOENIX CAMPUS WITH THE 2ND FAB VISIBLE IN THE BACKGROUND

- FIGURE 3.11: ESTIMATED GLOBAL FAB SPENDING 2023-2028

- FIGURE 3.12: FAB EXPANSIONS WITHIN THE US

- FIGURE 3.13: SEMICONDUCTOR CHIP MANUFACTURING REGIONS OF THE WORLD

- FIGURE 3.14: GLOBAL TOTAL EQUIPMENT SPENDING (US$ M) AND Y-O-Y CHANGE

- FIGURE 3.15: ADVANCED LOGIC DEVICE TECHNOLOGY ROADMAP OVERVIEW

- FIGURE 3.16: DRAM TECHNOLOGY ROADMAP OVERVIEW

- FIGURE 3.17: 3D NAND TECHNOLOGY ROADMAP OVERVIEW

- FIGURE 3.18: INTEL OHIO PLANT SITE AS OF FEB. 2024

- FIGURE 3.19: TECHCET WAFER START FORECAST BY NODE SEGMENTS

- FIGURE 3.20: TECHCET WORLDWIDE MATERIALS FORECAST ($M USD)

- FIGURE 4.1: DIELECTRIC PRECURSOR REVENUE (M USD) FORECAST BY SEGMENT

- FIGURE 4.2: WW MARKET SHARE - DIELECTRIC PRECURSORS 2023

- FIGURE 4.3: DIELECTRIC PRECURSOR MARKET REGIONAL ASSESSMENT 2023

- FIGURE 4.4: END USE APPLICATIONS DRIVING NEW DEVICE PROCESSES

- FIGURE 4.5: 3D NAND STACKING DRIVES DIELECTRICS AND METALS PRECURSOR VOLUME

- FIGURE 4.6: 3D NAND PROGRESSION

- FIGURE 4.7: 32 GB NVDRAM WITH 1T 1C MEMORY LAYERS

- FIGURE 4.8: GATE STRUCTURE ROADMAP

- FIGURE 4.9: ADVANCED LOGIC (FOUNDRY) NODE ROAD MAP

- FIGURE 4.10: RIBBON FET

- FIGURE 4.11: MONO LAYER NANO SHEETS CHANNELS

- FIGURE 4.12: NANO IMPRINT LITHOGRAPHY PROCESS FLOW

- FIGURE 4.13: ALD/ALE ENHANCEMENT OF NANO IMPRINT LITHOGRAPHY

- FIGURE 4.14: DIRECTED SELF-ASSEMBLY

- FIGURE 4.15: DSA PATENT FILING BY COMPANY

- FIGURE 4.16: DSA PATEN FILING SINCE 2023

- FIGURE 4.17: WHAT IS PATTERN SHAPING?

- FIGURE 4.18: REFINING EUV PATTERNING BY APPLIED MATERIALS

- FIGURE 4.19: COMPLEMENTARY FET (CFET)

- FIGURE 4.20: CFET IMPROVES PERFORMANCE IN TRACK SCALING

- FIGURE 4.21: MONOLITHIC CFET PROCESS FLOW EXAMPLE

- FIGURE 4.22: MCFET NEW FEATURE: MIDDLE DIELECTRIC ISOLATION

- FIGURE 4.23: LOW TEMPERATURE GATE STACK OPTION EXAMPLES

- FIGURE 4.24: LOW TEMPERATURE SD/CONTACT OPTION EXAMPLES

- FIGURE 4.25: BSPDN ADVANTAGE: IR DROP REDUCTION

- FIGURE 4.26: INCREASING NUMBER OF ALD STEPS REQUIRED BY NEXT GENERATION GAA-FET AND CFET

- FIGURE 4.27: IMEC SUB-1NM TRANSISTOR ROADMAP, 3D-STACKED CMOS 2.0 PLANS

- FIGURE 4.28: INPRIA EUV MOR

- FIGURE 4.29: INPRIA SPIN ON INORGANIC RESIST IS MUCH THINNER THAN STANDARD STACKS OF PHOTO RESIST

- FIGURE 4.30: PATENT FILING FOR MLD DEPOSITED EUV RESIST SEARCH PERFORMED IN PATBASE

- FIGURE 4.31: SADP PROCESS FLOW USING ALD SPACER

- FIGURE 4.32: ONE OF MANY FLAVORS OF SAQP PROCESS FLOW

- FIGURE 4.33: SELECTIVE ALD ENABLED BY PLASMA PRETREATMENT

- FIGURE 4.34: SPECIALTY/EMERGING DIELECTRIC APPLICATIONS FOR HETEROGENOUS INTEGRATIONS (APPLIED MATERIALS)

- FIGURE 4.35: 2023 DIELECTRIC REVENUE SHARE BY REGION

- FIGURE 5.1: 2023 PRECURSOR MATERIAL SUPPLIER MARKET SHARE BY REVENUE

- FIGURE 5.2: MERCK ELECTRONICS REVENUE 2022-2023 (M EUR), LEFT - SEMICONDUCTOR SOLUTIONS ANNUAL REVENUE FORECAST (M EUR), RIGHT

- FIGURE 5.3: AIR LIQUIDE ELECTRONICS REVENUE FORECAST (M EUR)

- FIGURE 5.4: THE MS (MATERIAL SOLUTIONS) DIVISION OF ENTEGRIS REVENUE FORECAST

- FIGURE 5.5: ADEKA REVENUE ELECTRONICS REVENUE FORECAST (100M JPY)

- FIGURE 6.1: FORMING GAS BLENDER CONFIGURATION

- FIGURE 6.2: TOP COUNTRIES/REGIONS THAT SUPPLY VERSUM MATERIALS US LLC (PANJIVA APRIL 2024)

- FIGURE 6.3: TOP COUNTRIES/REGIONS THAT SUPPLY AIR LIQUIDE AMERICA CORP. (PANJEIVA APRIL 2024)

- FIGURE 6.4: TOP COUNTRIES/REGIONS THAT SUPPLY H.C. STARCK INC. (USA)

LIST OF TABLES

- TABLE 1.1: DIELECTRIC PRECURSOR REVENUES AND GROWTH RATES

- TABLE 1.2: ESTIMATED DIELECTRIC PRECURSOR MARKET SHARE BY SUPPLIER 2023

- TABLE 3.1: GLOBAL GDP AND SEMICONDUCTOR REVENUES

- TABLE 3.2: WORLD BANK ECONOMIC OUTLOOK (JANUARY 2024)

- TABLE 3.3: BATTERY ELECTRIC VEHICLE (BEV) REGIONAL TRENDS

- TABLE 3.4: DATA CENTER SYSTEMS AND COMMUNICATION SERVICES MARKET SPENDING 2023

- TABLE 4.1: PRECURSORS REVENUE AND GROWTH RATES

- TABLE 4.2: DIELECTRIC PRECURSOR REVENUES AND GROWTH RATES

- TABLE 4.3: ESTIMATED DIELECTRIC PRECURSOR MARKET SHARE BY SUPPLIER 2023

- TABLE 4.4: DIELECTRIC PRECURSOR MARKET REGIONAL ASSESSMENT 2023

- TABLE 4.5: OVERVIEW OF ANNOUNCED 2023/2024 MATERIAL SUPPLIER INVESTMENTS

- TABLE 4.6: LEADING EDGE LOGIC DESCRIPTIONS BY NODE (TSMC, INTEL)

- TABLE 4.7: MULTIPATTERNING AT 7NM BY TSMC

- TABLE 4.8: SELECTIVE DEPOSITION - SELECTIVELY DEPOSITED MATERIALS

- TABLE 4.9: REGIONAL PRECURSOR MATERIAL MARKETS

- TABLE 4.10: REGIONAL PRECURSOR MATERIAL MARKETS, CONTINUED

- TABLE 5.1: MERCK QUARTER FINANCIALS

- TABLE 5.2: AIR LIQUIDE CURRENT QUARTER FINANCIALS

- TABLE 5.3: ENTEGRIS SUPPLIER CURRENT QUARTER FINANCIALS

- TABLE 6.1: CVD AND ALD PRECURSOR

02-2729-4219

+886-2-2729-4219

2026年全球低介电常数材料市场报告

2026年全球低介电常数材料市场报告 天然酯绝缘油市场按额定电压、应用、最终用户和分销管道划分-2026-2032年全球预测陶瓷颗粒市场依应用、原料、终端用户产业、形态、通路及粒径划分-2026-2032年全球预测

天然酯绝缘油市场按额定电压、应用、最终用户和分销管道划分-2026-2032年全球预测陶瓷颗粒市场依应用、原料、终端用户产业、形态、通路及粒径划分-2026-2032年全球预测 低介电常数电子织物:全球市场份额和排名、总收入和需求预测(2025-2031 年)

低介电常数电子织物:全球市场份额和排名、总收入和需求预测(2025-2031 年) 全球低介电常数材料市场全球高介电常数材料市场全球介电粉末市场

全球低介电常数材料市场全球高介电常数材料市场全球介电粉末市场 低介电材料市场,按产品类型、材料、应用、国家和地区 - 2025 年至 2032 年全球产业分析、市场规模、市场份额及预测

低介电材料市场,按产品类型、材料、应用、国家和地区 - 2025 年至 2032 年全球产业分析、市场规模、市场份额及预测 全球固体电介质材料市场:市场占有率和排名、总收入和需求预测(2025-2031)

全球固体电介质材料市场:市场占有率和排名、总收入和需求预测(2025-2031) 感应电液体市场:现状分析与未来预测 (2024年~2032年)

感应电液体市场:现状分析与未来预测 (2024年~2032年)

▼