|

市场调查报告书

商品编码

1950748

全球LED照明市场(2026年趋势) - 资料库及主要参与者策略2026 Global LED Lighting Market Trend- Database and Player Strategies |

||||||

根据TrendForce最新发布的报告《全球LED照明市场(2026年趋势) - 资料库及主要参与者策略(2026年上半年)》,全球LED照明市场预计将在2026年迎来关键转折点,在宏观经济波动和需求调整的背景下,市场将从萎缩转向稳定。随着分销通路库存恢復到健康水准,预计年降幅将显着收窄,整体需求预计将逐步恢復到以基本替换需求为主导的成长轨迹。更重要的是,竞争格局经历结构性转变,从价格竞争转向以应用驱动的价值创造和系统整合能力为主导的竞争。

以下是2026年全球LED照明市场的五大策略考察:

1. 通用照明市场:工业和户外领域是关键驱动因素

儘管2026年通用照明市场仍将处于调整阶段,但某些细分市场展现出强劲的成长潜力。

预计工业照明将成为2026年的核心成长引擎,这得益于国防、航空航太、核电、液化天然气(LNG)和战略资源领域的投资。同时,人工智慧资料中心的加速建设推动了对专为液冷系统和伺服器机架设计的基础设施照明的需求。在户外领域,老旧基础设施的更换和隧道照明标准的升级将继续推动改造需求。此外,体育和娱乐场所的照明以及智慧节能解决方案推动市场显着成长。

依地区划分,欧洲仍是市场领导者,其次是北美和亚太地区。预计2025年至2030年,欧洲LED照明市场将以2.3%的年复合成长率成长。该成长主要得益于为遏制不断上涨的能源成本而加速采用节能照明改造解决方案。亚太市场保持成长动力,其中东南亚预计在同一预测期内将以3.6%的年复合成长率成长。

2.智慧照明市场:从技术规格之争转向基于场景、以人为本的价值

根据TrendForce的分析,到2025年,全球照明产业将进入以 "情感照明" 和 "以人为本的照明(HCL)" 为中心的新阶段。竞争焦点正从传统的表现指标(例如发光效率和通讯协定)转向以昼夜节律调节和体验场景为核心的价值主张。

基于人工智慧的调光、全光谱控制和软体定义照明(SDL)推动照明产品从静态硬体设备转变为能够感知和自适应学习的智慧系统节点。根据 TrendForce 的资料,智慧照明市场预计到2030年将达到 217.85亿美元,2025年至2030年的年复合成长率(CAGR)为 13.6%。预计大部分成长将来自人工智慧应用和系统升级带来的价值提升,主要体现在三大应用场景:住宅照明、户外照明和工业照明。

人工智慧、软体定义照明和物联网技术的融合将照明从基本的照明设备转变为智慧生活环境、城市治理系统和工业数位化框架中的关键感知和互动节点。具备软硬体整合能力、生态系统协作能力以及场景感知洞察力的供应商,将在未来智慧照明市场中获得竞争优势。

3.农业照明:区域差异化加剧,欧洲蕴藏成长机会

特种作物更新周期进展不如预期,预算限制持续对终端产品价格构成下行压力。同时,全球新建温室和垂直农场计画在2025年被推迟。

然而,由于能源效率法规和高光合有效辐射(PPF/W,PPE)解决方案的采用,欧洲市场依然保持相对强劲,有效抵消了北美和其他地区的疲软态势。2025年,全球LED园艺照明市场规模达到13.65亿美元(年增4%)。

展望2026年,欧洲高压钠灯(HPS)系统加速被LED取代的趋势将持续推动市场需求,尤其是在温室应用领域。同时,北美、亚洲和中东地区将进入新一轮扩张週期,这主要得益于粮食安全政策和出口导向农业投资。预计市场对高光效、光谱可调和智慧LED照明系统的需求将会增加。 TrendForce预测,2030年,市场规模将达到10.41亿美元,2025年至2030年的年复合成长率(CAGR)为4%。

在LED封装领域,预计2026年多通道光谱技术的应用将加速。许多新註册的产品都具备动态调光功能和高精度控制要求,这将推动对高品质解决方案的需求成长,并促进LED出货量的成长。经过过去的库存调整和产业整合,预计2026年农业照明LED的平均售价将趋于稳定。

4.製造商收入:智慧照明及细分市场占有率不断扩大

根据TrendForce的最新统计资料,2025年全球20家领先照明製造商的总收入达到233.55亿美元,较上年下降2%。前五的公司保持不变:Signify、Acuity Brands、Panasonic、LEDVANCE和Zumtobel。

在具体细分市场中,专业照明领域展现出规模经济优势。同时,受房地产市场低迷以及传统住宅和商业照明市场价格竞争的影响,Signify和LEDVANCE等全球通用照明领导者2025年的收入出现下滑。相较之下,专注于高科技细分领域的公司则保持着强劲的业绩。

专注于防爆和工业照明的Warrom公司预计,在2025年营收将成长5.8%,这主要得益于全球能源开采活动的復苏以及对工业安全需求的不断成长。同样,专注于船舶和海上能源照明的Grammox集团预计将维持3.2%的稳定成长率,这主要得益于欧盟海事碳排放政策的影响,推动了升级版船舶照明的需求。

TrendForce认为,在通用照明市场规模经济效益下降的情况下,高科技细分领域将是製造商维持获利能力和成长的关键。

5.LED封装市场:从价格竞争到稳定与品质提升

根据TrendForce分析,由于西方国际品牌积极采取成本最佳化策略并大力推广高性价比解决方案,2025年照明LED市场将面临价格持续下跌和订单前景疲软的局面。

经过长期的利润率压缩,LED封装市场预计将在2026年摆脱下行週期。随着上游材料成本的上升,LED封装价格预计将趋于稳定,标誌着市场将从持续的价格下跌过渡到销售收缩与价格稳定并存的局面。

在永续发展政策、减碳目标和绿建筑标准不断提高的推动下,产业结构经历质的转变。LED照明产业预计将于2026年触底反弹,并于2027年开始復苏。 TrendForce保持谨慎乐观的态度,预测2030年,全球LED照明市场规模将达到37.34亿美元,2025年至2030年的年复合成长率(CAGR)为2.5%。

TrendForce透过对通用照明、智慧照明和园艺照明三大细分市场的市场规模、价格趋势和区域分布分析,以及对LED封装产业趋势的分析,深入剖析了全球LED照明产业。本报告追踪了前20大製造商的收入和策略,分析了Signify、Acquity、Panasonic、LEDVANCE和Oppel等主要厂商的竞争地位,并基于月度细分市场分析,概述了七大主要照明灯具类别的趋势和价格。

目录

第一部分:引言

- 市场研究方法

- 全球经济(GDP)

- 汇率

第二部分:一般照明市场预测(2026-2030)

- 通用LED照明市场规模 - 需求、市场价值、数量和平均售价 - 依产品分类

- 通用LED照明市场规模、需求、市场价值 - 依类别(灯具和照明设备)分类

- 通用LED照明市场规模、需求、市场价值 - 依地区分类

- 通用LED照明市场规模 - 需求、市场价值和数量 - 依产品和地区分类

- 通用LED照明市场规模、需求、市场价值 - 依应用分类

- 通用LED照明普及率(安装量)

- 通用LED照明市场 - 价值与数量 - 依应用分类

- 通用LED照明市场 - 价值、数量和平均售价(依电力)

- 通用LED照明市场 - 价值、数量和平均售价 - 依封装类型分类

- 通用LED照明市场价值 - 色温(CCT)

- 通用LED照明市场价值与数量 - 显色指数(CRI)

- 通用LED照明价格

第三部分:智慧照明市场预测(2026-2030年)

- 智慧 LED 照明市场规模、需求、市场价值与应用

- 智慧 LED 照明市场规模、需求、市场价值与区域

第四部分:农业照明市场预测(2026-2030年)

- 园艺LED照明市场规模、需求、市场价值,依应用领域

- 园艺LED照明市场规模、需求、市场价值,依区域

- 农业LED照明市场 - 依晶片类型划分的价值和数量

- 农业LED照明市场 - 依电力划分的价值和数量

- 农业LED照明价格

- 园艺LED照明厂商收入排名(2023-2025年预测)

第五部分:照明产业收入排名及预测

- 照明设备製造商收入排名前20(2023-2025年预测)

- 照明设备製造商收入排名前10,依应用领域划分(2023-2025年预测)

- LED照明厂商收入排名(2023-2025年预测)

第六部分:LED照明产品规格及定价

- 产品及价格 - 灯丝灯 - 依地区划分

- 产品及价格 - 路灯 - 依地区划分

- 产品及价格 - 面板灯 - 依地区划分

- 产品及价格 - 槽型灯 - 依地区划分

- 产品及价格 - 高/低棚灯 - 依地区划分

- 产品及价格 - 防爆灯 - 依地区划分

- 产品及价格园艺照明 - 依应用领域划分

(PDF)1.2025年全球 LED 照明市场趋势 - 市场参与者策略

第1章 全球智慧 LED 照明市场趋势

- 全球智慧 LED 照明市场规模分析(2026-2030年)

- 全球智慧 LED 照明市场规模分析:住宅(2026-2030年)

- 智慧家庭照明产品(2025-2026年)

- 全球智慧 LED 照明市场规模分析:户外(2026-2030年)

- 全球智慧 LED 照明市场规模分析:工业(2026-2030年)

- 全球智慧 LED 照明市场规模分析:依地区划分(2026-2030年)

- 智慧照明控制协定 - Bluetooth

- 智慧照明控制协定 - Zhaga

第2章 照明产业收入及市场策略分析

- 照明设备製造商收入排名前20:照明产品(2023-2025)

- 照明製造商收入排名前20:LED照明(2023-2025)

- 照明产业收入及产品策略

- Signify

- Zumtobel

- Fagerhult

- Acuity

- Current

- Panasonic

- Endo Lighting

- 中国照明製造商的收入及产品策略

- LEDVANCE/MLS

- Opple Lighting

- NVC Lighting

- Foshan Lighting

- Yankon Group

(PDF)2.LED照明市场每月报告 - 依细分市场进行应用和产品分析

- 引言

- 趋势展望

- 市场概览及特质分析

- 产品类型及应用情境分析

- 主流产品规格及LED需求分析

- 製造商趋势及竞争格局分析

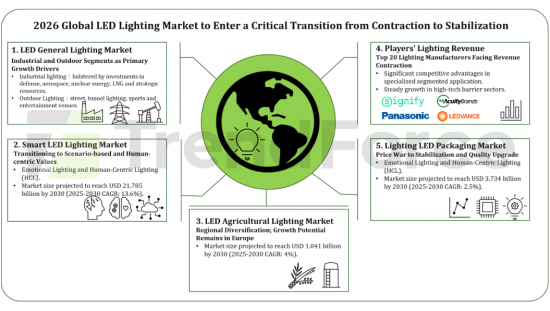

According to the latest TrendForce report, 2026 Global LED Lighting Market Trend- Database and Player Strategies (1H26), the global LED lighting market, after undergoing macroeconomic volatility and demand corrections, is expected to enter a critical transition phase in 2026, shifting from contraction to stabilization. As channel inventories return to healthier levels, the annual decline is projected to narrow significantly, with overall demand gradually reverting to fundamental replacement-driven growth. More importantly, the competitive landscape is undergoing a structural transformation - from price-based competition toward application-driven value creation and system integration capabilities.

Below are 5 strategic observations for the global LED lighting market in 2026:

1. General Lighting Market: Industrial and Outdoor Segments as Primary Growth Drivers

Although general lighting remains in an adjustment phase in 2026, selected subsegments demonstrate resilient growth potential.

Industrial lighting is set to become the core growth engine in 2026, bolstered by investments in defense, aerospace, nuclear energy, liquefied natural gas (LNG), and strategic resources. Simultaneously, the accelerated construction of AI data centers is driving demand for infrastructure lighting tailored for liquid cooling systems and server racks. In the outdoor segment, the renewal of aging infrastructure and upgrades to tunnel lighting standards continue to fuel retrofit demand. Furthermore, lighting for sports and entertainment venues, alongside smart and energy-saving solutions, are providing significant incremental growth to the market.

By region, Europe still dominates the market, followed by the North America and Asia-Pacific regions. The European LED lighting market is projected to expand at a CAGR of 2.3% from 2025 to 2030. This growth is mainly supported by the accelerating enforced adoption of energy-saving lighting retrofit solutions to rein in the rising energy costs. The Asian-Pacific market keeps up its momentum on growth, especially in the Southeastern market, with a CAGR of 3.6% throughout the same forecast period.

2. Smart Lighting Market: Transitioning from Technical Spec Wars to Scenario-based and Human-centric Values

TrendForce indicates that in 2025, the global lighting industry entered a new phase centered on Emotional Lighting and Human-Centric Lighting (HCL). Competitive dynamics are shifting away from traditional performance metrics such as luminous efficacy and communication protocols toward value propositions focused on circadian rhythm regulation and experiential scenarios.

Enabled by AI-based dimming, full-spectrum control, and Software-Defined Lighting (SDL), lighting products evolve from static hardware devices into intelligent system nodes capable of perception and adaptive learning. According to TrendForce data, the smart lighting market is projected to reach USD 21.785 billion by 2030, representing a CAGR of 13.6% from 2025 to 2030. Growth will mostly come from value enhancement through AI enablement and system upgrades in three major application scenarios: residential, outdoor, and industrial lighting.

As AI, SDL, and IoT technologies converge, lighting is transitioning from basic illumination equipment to a critical sensing and interaction node within smart living environments, urban governance systems, and industrial digitalization frameworks. Suppliers with software-hardware integration capabilities, ecosystem collaboration and scenario-aware insights will be well-positioned to gain a competitive edge in the future smart lighting market.

3. Agricultural Lighting: Deepening Regional Differentiation with Upside Potential in Europe

Replacement cycles for specialty crops have not materialized as expected, while budget constraints have led to continued downward pressure on end-product pricing. Meanwhile, new greenhouse and vertical farm construction projects have been postponed globally in 2025.

However, Europe remains comparatively resilient, supported by energy-efficiency regulations and the adoption of high photosynthetic photon efficacy (PPF/W, PPE) solutions, effectively offsetting weakness in North America and other regions. In 2025, the global LED horticultural lighting market reached USD 1.365 billion (+4% YoY).

Looking ahead to 2026, with a specific focus on greenhouse applications, accelerated LED replacement of high-pressure sodium (HPS) systems in Europe will continue to drive demand. Meanwhile, North America, Asia, and the Middle East are entering a new expansion cycle, supported by food security policies and export-oriented agricultural investments. Demand for high-PPE, spectrum-tunable, and intelligent LED lighting systems is expected to increase. TrendForce projects the market to reach USD 1.041 billion by 2030, with a CAGR of 4% from 2025 to 2030.

In the LED packaging segment, 2026 is expected to mark accelerated adoption of multi-channel spectral technologies. Most newly registered products will feature dynamic dimming functionality and higher precision control requirements, driving demand for higher-quality solutions and increased LED shipment volumes. Following previous inventory adjustments and industry consolidation, agricultural lighting LED ASPs are expected to stabilize in 2026.

4. Manufacturer Revenue: Rising Share of Smart Lighting and Segmented Application Markets

According to TrendForce's latest statistics, total revenue of the global top 20 lighting companies is projected to decline 2% YoY to USD 23.355 billion in 2025. The top five players remain unchanged: Signify, Acuity Brands, Panasonic, LEDVANCE, and Zumtobel.

TrendForce observes that at specific segments, professional segmented lighting shows advantages in terms of economies of scale. While global general lighting leaders such as Signify and LEDVANCE face revenue contraction in 2025 due to sluggish real estate markets and price competition in the traditional residential and commercial general lighting markets. Conversely, companies focusing on high-tech niche areas show steady performance.

Warom, specializing in explosion-proof and industrial lighting, is expected to achieve a 5.8% revenue growth for 2025, as it has benefited from the recovery of global energy extraction activities and the rise in industrial safety demands. Similarly, Glamox Group, which focuses on marine and offshore energy lighting, is projected to maintain a steady growth rate of 3.2%, driven by the demand for ship lighting upgrades influenced by the EU's maritime carbon emission policies.

TrendForce believes that as the effect of economies of scale is diminishing in the general lighting market, high-tech niche segments have become the key for manufacturers to maintain profitability and growth.

5. LED Packaging Market: From Price War to Stabilization and Quality Upgrade

TrendForce analysis indicates that in 2025, the lighting LED market faced intensified price erosion and low order visibility due to aggressive cost optimization strategies by international brands from Europe and the USA and concentrated adoption of high cost-performance solutions.

After prolonged margin compression, the LED packaging market is expected to exit its downward cycle in 2026. With rising upstream material costs, LED packaging prices are likely to stabilize, marking a transition from continuous price decline to a volume contraction with price stabilization environment.

Supported by sustainability policies, carbon reduction targets, and strengthened green building standards, the industry structure is undergoing qualitative transformation. The LED lighting industry is expected to complete its cyclical bottoming phase in 2026 and begin recovery in 2027. TrendForce maintains a cautiously optimistic outlook, forecasting the global lighting LED market to reach USD 3.734 billion by 2030, representing a 2025-2030 CAGR of 2.5%.

TrendForce provides in-depth insights into global LED lighting industry trends, covering market size, pricing, and regional distribution across general, smart, and horticultural lighting segments, along with analysis of developments in the LED packaging sector. The report tracks revenue and strategies of the top 20 manufacturers, examines the competitive positioning of leading players such as Signify, Acuity, Panasonic, LEDVANCE, and Opple, and outlines trends and price movements in seven major luminaire categories, supported by monthly segmented markets analysis.

TABLE OF CONTENTS

PART 1 Introduction

- 1.1 Market Research Methodology

- 1.2 Global Economics (GDP)

- 1.3 Exchange Rates

PART 2 General Lighting Market Forecast (2026-2030)

- 2.1 General LED Lighting Market Scale-Demand Market Value & Volume & ASP-by Product

- 2.2 General LED Lighting Market Scale-Demand Market Value-by Category-Lamps & Luminaries

- 2.3 General LED Lighting Market Scale-Demand Market Value-by Region

- 2.4 General LED Lighting Market Scale-Demand Market Value & Volume-by Product & by Region

- 2.5 General LED Lighting Market Scale-Demand Market Value-by Application

- 2.6 General LED Lighting Penetration Rate (Installed Based Volume)

- 2.7 General Lighting LED Market-Value & Volume-by Application

- 2.8 General Lighting LED Market-Value & Volume & ASP-by Power

- 2.9 General Lighting LED Market-Value & Volume & ASP-by Package Type

- 2.10 General Lighting LED Market-Value-by CCT

- 2.11 General Lighting LED Market-Value & Volume-by CRI

- 2.12 General Lighting LED Price

PART 3 Smart Lighting Market Forecast (2026-2030)

- 3.1 Smart LED Lighting Market Scale-Demand Market Value-by Application

- 3.2 Smart LED Lighting Market Scale-Demand Market Value-by Region

PART 4 Agricultural Lighting Market Forecast (2026-2030)

- 4.1 Horticultural LED Lighting Market Scale-Demand Market Value-by Application

- 4.2 Horticultural LED Lighting Market Scale-Demand Market Value-by Region

- 4.3 Agricultural Lighting LED Market-Value & Volume-by Chip Type

- 4.4 Agricultural Lighting LED Market-Value & Volume-by Power

- 4.5 Agricultural Lighting LED Price

- 4.6 Horticultural Lighting LED Player Revenue Ranking (2023-2025E)

PART 5 Lighting Player Revenue Ranking and Estimated

- 5.1 Top 20 Lighting Player Revenue (2023-2025E)

- 5.2 Top 10 Lighting Player Revenue Ranking by Application (2023-2025E)

- 5.3 Lighting LED Player Revenue (2023-2025E)

PART 6 LED Lighting Product Specification and Price

- 6.1 Product & Price- Filament Lamp-by Region

- 6.2 Product & Price- Street Light-by Region

- 6.3 Product & Price- Panel Light-by Region

- 6.4 Product & Price- Troffer-by Region

- 6.5 Product & Price- High/Low Bay-by Region

- 6.6 Product & Price- Explosion Proof Light-by Region

- 6.7 Product & Price- Horticultural Light- by Application

(PDF)1. 2025 Global LED Lighting Market Trend- Player Strategies

Chapter 1 Global Smart LED Lighting Market Trend

- 2026-2030 Global Smart LED Lighting Market Size Analysis

- 2026-2030 Global Smart LED Lighting Market Size Analysis: Residential

- 2025-2026 Smart Residential Lighting Products

- 2026-2030 Global Smart LED Lighting Market Size Analysis: Outdoor

- 2026-2030 Global Smart LED Lighting Market Size Analysis: Industrial

- 2026-2030 Global Smart LED Lighting Market Size Analysis: by Region

- Smart Lighting Control Protocol- Bluetooth

- Smart Lighting Control Protocol- Zhaga

Chapter 2 Lighting Player Revenue and Market Strategies Analysis

- 2023-2025(E) Top 20 Lighting Player Revenue Ranking: Total Lighting

- 2023-2025(E) Top 20 Lighting Player Revenue Ranking: LED Lighting

- Lighting Player Revenue and Product Strategies

- Signify

- Zumtobel

- Fagerhult

- Acuity

- Current

- Panasonic

- Endo Lighting

- Chinese Lighting Player Revenue and Product Strategies

- LEDVANCE / MLS

- Opple Lighting

- NVC Lighting

- Foshan Lighting

- Yankon Group

(PDF)2. LED Lighting Market Monthly Report-Segment Application and Product Analysis

- Foreword

- TrendForce's Perspective

- Market Overview and Feature Analysis

- Product Types and Application Scenario Analysis

- Mainstream Product Specifications and LED Requirement Analysis

- Manufacturer Dynamics and Competitive Landscape Analysis

中东及土耳其照明灯具市场

中东及土耳其照明灯具市场 日本吸顶灯市场规模、份额、趋势及预测(按光源、安装类型、应用、智慧功能、风格和地区划分,2026-2034年)

日本吸顶灯市场规模、份额、趋势及预测(按光源、安装类型、应用、智慧功能、风格和地区划分,2026-2034年) 2026年全球高桿照明市场报告

2026年全球高桿照明市场报告 万圣节照明服务市场(依照明类型、服务内容、最终用户和通路划分)-2026-2032年全球预测户外LED灯桿萤幕市场:按应用、类型、安装方式、技术、萤幕尺寸和控制系统划分,全球预测(2026-2032年)

万圣节照明服务市场(依照明类型、服务内容、最终用户和通路划分)-2026-2032年全球预测户外LED灯桿萤幕市场:按应用、类型、安装方式、技术、萤幕尺寸和控制系统划分,全球预测(2026-2032年) 照明灯具市场规模、份额和成长分析(按光源、产品、通路、应用和地区划分)-2026-2033年产业预测

照明灯具市场规模、份额和成长分析(按光源、产品、通路、应用和地区划分)-2026-2033年产业预测 照明:全球 LED 和灯具市场

照明:全球 LED 和灯具市场 全球照明设备市场:产业分析、规模、份额、成长、趋势与预测(2025-2032)

全球照明设备市场:产业分析、规模、份额、成长、趋势与预测(2025-2032) 亚太地区的照明设备市场2025年全球照明灯具维修服务市场报告

亚太地区的照明设备市场2025年全球照明灯具维修服务市场报告