|

市场调查报告书

商品编码

1742160

微LED的显示器及非显示器用途的市场分析 (2025年)2025 Micro LED Display and Non-Display Application Market Analysis |

||||||

[洞察] Micro LED 拓展至显示器领域,为透明与非显示器应用开启新的可能性

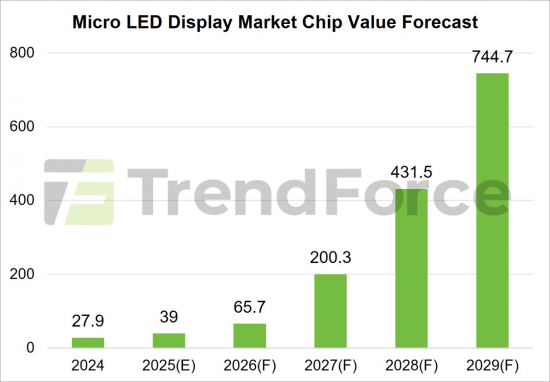

据报道,目前 Micro LED 技术在显示器领域的发展主要面临两大课题:透过设计和生产改进来优化製造成本,以及找到独特的利基市场。预计到2029年,用于显示应用的Micro LED晶片市场规模将达到7.4亿美元,2024年至2029年的复合年增长率为93%。

大型显示器的成本改进正在进行中

目前,Micro LED显示器市场主要以大型显示器为主,三星在该领域处于领先地位。未来的成长需要突破几个关键製造工艺,并需要中国晶片製造商与品牌製造商合作,共同推动晶片小型化。预计这将进一步增强量产Micro LED大型显示器的成本优势。

此外,随着人工智慧的发展,头戴式设备的使用范围不断扩大,而智慧驾驶生态系统的发展也带动了对先进车载显示器的需求不断增长,因此这两个领域有望成为未来MicroLED显示器市场的主要支柱。

TrendForce指出,Micro LED大萤幕显示器的业界标准通常为4K或更高解析度,但目前商用化并量产的像素间距仅为0.5毫米。进一步缩小像素间距对于与Mini LED显示器的差异化至关重要,同时也必须克服驱动器连接良率低和麵板接缝问题等课题。

成本优化工作也正在转向背板侧,透过简化製造流程来提高良率,并透过减少接缝来减少组装步骤。这些努力有助于降低总成本。

Micro LED 凭藉其高亮度、高对比度和高透明度等独特特性,持续吸引厂商的投资,这些特性使得 Micro LED 能够整合到车窗透明显示器、AR-HUD 和 P-HUD 等系统中,满足驾驶员和乘客对虚拟与现实资讯无缝融合的需求。此外,Micro LED 与硅基板的结合,可为 AR 眼镜的近眼显示器提供强大的解决方案,而 Micro LED 也正在成为下一代支援元宇宙的头戴式装置的标准技术。

本报告提供微LED的显示器及非显示器用途的市场调查,彙整微LED的技术开发趋势,微LED的显示器及非显示器用途的市场规模的转变·预测,微LED透明显示器趋势,主要製造商的简介等资讯。

目录

第1章 微LED显示器市场分析

- 市场规模的分析:大型显示器

- 市场规模的分析:穿戴式显示器

- 市场规模的分析:头戴设备

- 市场规模的分析:汽车显示器

- 市场规模的分析

- 晶圆需求的分析

第2章 微LED技术的开发

- 模组尺寸增大

- Micro LED 模组尺寸增加/拼接减少

- Micro LED 模组尺寸增加的优点 (1/2) - 无拼接

- Micro LED 模组尺寸增大的优点 (2/2) - 成本与商业效益

- 模组尺寸与拼接尺寸之间的关係

- 决定经济最优的模组尺寸

- Micro LED 模组尺寸增大的课题

- Micro LED 拼接:大模组 vs. 小模组

- 拼接显示幕

- 拼接连结点的技术课题

- Micro LED 拼接的商业策略:从像素间距角度

- Micro LED 拼接的最小可商业化尺寸:UHD(超高清)

- Micro LED 拼接的最大可商业化尺寸:从经济拼接角度

- 商业化大型 Micro LED 显示器的最佳尺寸

- 玻璃:蓝宝石基 COC 的潜在竞争对手

- Micro LED 的散热课题

- Micro LED 的 PPI 课题

- 高效 Micro LED 的宣告:即将实现

- Micro LED 产业趋势 (1/2):部署到专业显示器

- MicroLED 产业趋势 (2/2):专注于 AR 的 MicroLED 公司

第3章 微LED透明显示器

- 两种类型的透明显示器:直视型和微显示投影型

- 直视型与投影型的主要差异 (1/2):视角

- 直视型与投影型的主要差异 (2/2):焦点问题

- 透明直视型显示器面临的课题:在逼真度和真实度之间做出权衡

- 两种类型透明显示器的基准比较

- 透明直视型显示器的 SWOT 分析

- 透明直视型显示器按应用的 SWOT 分析

- 透明直视型显示器发展趋势分析

- 选择透明显示器应用时的注意事项

- 不同透明显示器技术原理的差异

- JDI 以其 OLED 显示器重新进军透明显示器市场LCD

- 透明显示器的应用范例

- 透明显示器亮度与透过率的悖论

- MicroLED 透明显示器

- 各种透明显示技术比较

- 量产透明显示器价格比较

第4章 微LED製造商趋势

- 2025年的微LED企业的製造能力分析

- PlayNitride

- Ennostar

- HC Semitek

- AUO

- Innolux

- Extremely PQ

- Tianma

- BOE

- LGD

- Samsung

- Hisense

- Hongshi

- VueReal

- Aledia

附录

[Insight] Micro LED Expands Beyond Displays, Unlocking New Opportunities in Transparent and Non-Display Applications

TrendForce's latest report, "2025 Micro LED Display and Non-Display Application Market Analysis", reveals that the current development of Micro LED technology in the display sector focuses on two key challenges: optimizing manufacturing costs through design and production improvements, and identifying unique niche markets.

TrendForce forecasts that the chip market value for Micro LED display applications will reach US$740 million by 2029, with a CAGR of 93% from 2024 to 2029.

Cost improvements continue for large-sized displays

Presently, the bulk of Micro LED's display-related market value is driven by large-sized displays, where Samsung holds a leading position. Future growth will rely not only on breakthrough across several critical manufacturing processes but also on collaborations between Chinese chipmakers and brand manufacturers to push chip miniaturization. This will further enhance cost advantages for mass-produced Micro LED large-sized displays.

Additionally, as AI broadens the application scenarios for head-mounted devices and as smart driving ecosystems drive up demand for advanced automotive displays, these two sectors are expected to become major pillars of Micro LED display market value in the years ahead.

TrendForce notes that the industry standard for Micro LED large-sized displays is typically 4K resolution or higher; however, the currently commercialized, mass-producible pixel pitch remains at 0.5 mm. Continued efforts to reduce pixel pitch are essential to further differentiate Micro LED from Mini LED video wall , along with overcoming challenges like low yield rates in driver connections and issues with panel seams.

Cost optimization is also shifting toward the backplane, where simplifying the manufacturing process can improve yields, and reducing the number of seams can cut down assembly steps. This contributes to overall cost reductions.

Micro LED's standout characteristics-high brightness, high contrast, and high transparency-continue to attract investment from manufacturers. These features enable Micro LED to integrate into transparent displays for automotive windows or as part of AR-HUD or P-HUD systems, meeting the growing demand for seamless integration of virtual and real-world information for drivers and passengers. Additionally, combining Micro LED with silicon substrates offers a robust solution for near-eye displays in AR glasses, positioning Micro LED as a benchmark for next-generation metaverse-focused head-mounted devices.

Transparent displays hold great promise; non-display applications open new doors

Micro LED technology also shows strong potential in transparent display applications. These can be categorized into direct-view and micro-projection systems, with the key differences lying in viewing angels and focal distance management. In terms of use case, transparent direct-view displays are better suited for public environments where content is viewed by multiple people, and Micro LED's combination of high brightness and high transparency makes it an ideal technology.

Meanwhile, micro-projection systems hold greater promise in privacy-sensitive personal electronic devices, where Micro LED offers ultra-miniaturized light engine solutions and is seen as the best option for micro-display technology in AR applications. Overall, Micro LED has significant room for expansion across diverse transparent display segments by developing both TFT and CMOS backplane platforms.

TrendForce emphasizes that the immediate priority for the Micro LED industry is to scale up the market quickly in order to realize economic efficiencies. As a result, non-display sectors have increasingly become important avenues for growth in addition to focusing on display applications.

These non-display opportunities span a wide range, including optical communication applications accelerated by AI, biotechnology-related medical uses, and industrial production areas such as 3D printing and photopolymerization. Ongoing innovations in these areas are adding further momentum to Micro LED's market expansion.

Table of Contents

Chapter 1. Micro LED Display Market Analysis

- 2025-2029 Micro LED Market Value Analysis-Large-sized Displays

- 2025-2029 Micro LED Market Value Analysis-Wearable Displays

- 2025-2029 Micro LED Market Value Analysis-Head-mounted Devices

- 2025-2029 Micro LED Market Value Analysis-Automotive Displays

- 2025-2029 Micro LED Market Value Analysis

- 2025-2029 Micro LED Wafer Demand Analysis

Chapter 2. Micro LED Technology Development

- 2.1. Module Enlargement

- Micro LED Module Enlargement/Reduced Tiling

- Enlarging Micro LED Modules Advantages (1/2) - Tiling Omitted

- Enlarging Micro LED Modules Advantages (2/2) - Cost and Commercial Benefits

- Relationships between Module Size and Tiling Size

- Deciding Economic Module Size

- Micro LED Module Enlargement Challenges

- Micro LED Tiling: Large Modules vs. Small Modules

- 2.2. Tiling Display

- Tiling Seams Technical Challenges

- Micro LED Tiling Commercial Strategies : A Pixel Pitch Perspective

- Lower Limit of Commercialization Size for Micro LED-tiled Displays: UHD

- Upper Limit of Commercialization Size for Micro LED-tiled Displays: Economic Tiling

- Most Suitable Sizes for Commercialized Large-sized Micro LED Displays

- Glass: A Potential Competitor to Sapphire-based COC

- Micro LED Heat Dissipation Challenges

- Micro LED PPI Challenges

- Manifesto for Achieving High-Efficiency Micro LED is Within Reach

- Micro LED Industrial Trends (1/2): Towards Specialized Display

- Micro LED Industrial Trends (2/2): Micro LED Enterprises to Focus on AR

Chapter 3. Micro LED Transparent Display

- Two Systems for See-through Displays: Direct-view and Micro display Projection

- Key Differences between Direct-view and Projection Systems (1/2): Viewing Angle

- Key Differences between Direct-view and Projection Systems (2/2): Focus Issues

- Transparent Direct-View Displays Challenges : Mutually Exclusive Relationship between Vitality and Reality

- Benchmarks between the Two Types of Transparent Displays

- Transparent Direct-view Displays SWOT Analysis

- Transparent Direct-view Displays across Different Applications SWOT Analysis

- Transparent Direct-view Displays Development Trend Analysis

- Things to Consider When Selecting Transparent Display Applications

- Technology Principles by Different Transparent Displays

- JDI Brings LCD Back to Transparent Display Competition

- Transparent Display Application Cases

- The Brightness-Transmittance Paradox in Transparent Displays

- Micro LED Transparent Displays

- Comparison between Different Transparent Display Technologies

- Prices of Mass-produced Transparent Displays

Chapter 4. Micro LED Manufacturer Dynamic

- 2025 Micro LED Player Capacity Analysis.

- PlayNitride

- Ennostar

- HC Semitek

- AUO

- Innolux

- Extremely PQ

- Tianma

- BOE

- LGD

- Samsung

- Hisense

- Hongshi

- VueReal

- Aledia

Appendix

- Intel-Samsung Patent Sale

- Advancing non-display Micro LED Technology Development - Avicena

LED电影萤幕市场规模、份额和成长分析(按产品类型、技术、萤幕尺寸、最终用户、销售管道和地区划分)-2026-2033年产业预测

LED电影萤幕市场规模、份额和成长分析(按产品类型、技术、萤幕尺寸、最终用户、销售管道和地区划分)-2026-2033年产业预测 LED模组化显示器市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、形状、材质、最终用户和安装类型划分迷你LED显示器市场分析及预测(至2035年):依类型、产品类型、技术、组件、应用、材料类型、最终用户、功能及安装类型划分

LED模组化显示器市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、形状、材质、最终用户和安装类型划分迷你LED显示器市场分析及预测(至2035年):依类型、产品类型、技术、组件、应用、材料类型、最终用户、功能及安装类型划分 日本LED显示器市场规模、份额、趋势及预测(依技术、颜色、应用、最终用途及地区划分),2026-2034年

日本LED显示器市场规模、份额、趋势及预测(依技术、颜色、应用、最终用途及地区划分),2026-2034年 2026年智慧装卸区发光二极体(LED)显示器全球市场报告

2026年智慧装卸区发光二极体(LED)显示器全球市场报告 LED剧院显示器市场按像素间距、萤幕尺寸、解析度、安装类型、剧院类型、配置和最终用户划分,全球预测,2026-2032年迷你直下式显示电视市场:按萤幕大小、解析度、技术、应用、销售管道和价格范围划分-全球预测(2026-2032年)

LED剧院显示器市场按像素间距、萤幕尺寸、解析度、安装类型、剧院类型、配置和最终用户划分,全球预测,2026-2032年迷你直下式显示电视市场:按萤幕大小、解析度、技术、应用、销售管道和价格范围划分-全球预测(2026-2032年) LED模组化显示器市场规模、份额及成长分析(按显示类型、应用和地区划分)-2026-2033年产业预测

LED模组化显示器市场规模、份额及成长分析(按显示类型、应用和地区划分)-2026-2033年产业预测 LED显示器的全球市场

LED显示器的全球市场 全球LED模组显示器市场

全球LED模组显示器市场