|

市场调查报告书

商品编码

1348023

手持式条码扫描器的全球市场The Global Market for Handheld Barcode Scanners |

||||||

目标供应商

|

|

|

执行摘要

由于大流行影响、供应链限制、引发通膨的定价和部门需求变化,导致市场表现多年波动,但市场已经正常化,并转向更可预测的成长模式。

同时,我们需要解决与通路库存过剩和价格持续波动相关的问题。 此外,可穿戴式扫描器等替代外形因素带来的挑战,以及利用智慧型行动装置(智慧型手机、平板电脑等)摄影机进行基于软体的扫描的日益增多,消除了传统上由专用手持式扫描器支持的机会。可能性。

主要发现

通路库存过剩导致近期销售放缓:在2023 年第一季整体强劲之后,主要供应商正在考虑产品库存过剩对其通路合作伙伴的影响。我们预计需求模式将在年底前软化今年的。 分销合作伙伴承担了大量库存,以填补大流行期间和之后的积压。 市场可能需要一些时间来吸收运送给分销商和合作伙伴的产品。 VDC 预计这一问题将在 2024 年上半年缓解。

医疗保健作为一个成长市场:虽然医疗产业历来对手持式扫描器有着持续的需求,但该产业的成长机会在过去几年中显着增加。 在北美尤其如此,医疗保健是继零售和製造之后手持式扫描器的第三大市场。 医疗产业的需求还包括更昂贵和更专业的解决方案,例如需要能够抵抗医疗环境中使用的消毒剂的特殊塑胶。

超越扫描器的差异化:随着向2D 扫描器(从传统雷射扫描器和线性成像仪)的过渡接近完成,原始设备製造商正在定位其产品组合,以让自己在竞争中脱颖而出。我们正在探索替代方案让我们与众不同。 这包括为特殊用例设计扫描仪,例如可以承受消毒溶液的医疗扫描仪或用于工业应用的加固扫描仪。 此外,OEM 正在增加对软体实用程式的投资,以帮助客户支援和管理他们的扫描器。 此外,扫描引擎设计用于支援更复杂的资料撷取应用,例如同时扫描多个程式码、识别和解码正确的符号,以及支援 OCR 和其他影像撷取和处理功能。

不断变化的竞争格局:全球三大手持式扫描器OEM(Zebra、Honeywell、Datalogic)凭藉差异化的产品组合和强大的合作伙伴网络占据有利地位。然而,竞争格局正在改变。 亚洲供应商不断推出具有价格竞争力的产品,其中许多供应商依赖主要原始设备製造商来采购扫描引擎。 此外,新的外形尺寸正在挑战传统的手持式扫描器用例。 例如,在物流环境中,手套或手掌大小的扫描仪的使用尤其普遍,这为有利于免持操作的扫描密集型应用提供了更符合人体工学和无缝的选择。 此外,基于软体的扫描解决方案的性能不断提高,挑战了专用扫描引擎的现状(儘管这对于配备扫描仪的行动数据终端来说是一个更大的挑战)。

本报告研究和分析了全球手持式条码扫描器市场,提供了关键策略问题、趋势和驱动因素、技术趋势、成长机会和供应商概况等资讯。

目录

执行摘要

世界市场概览

- 垂直市场

- 零售

- 工业/製造

- 医疗

- 交通/物流

- 商业服务

- 市场趋势

- 2027 年日出 - GS1

- 二维、雷射、线性

- 基于软体的扫描

- 产品趋势

- 穿戴式

- 积压和缺少的组件

区域预测

- 美洲

- 欧洲/中东/非洲

- 亚太地区

供应商注意事项/简介

关于 VDC 研究

报告图表

资料集图

市场分析 - 美洲

INSIDE THIS REPORT:

This report provides a detailed analysis of the key strategic issues, trends and drivers for handheld barcode scanners, including 2D imagers, linear imagers (CCD scanners) and laser scanners. The research provides detailed analysis by geography, industry, distribution channel and scanner technology with detailed five-year forecasts. Our analyst research and commentary covers global and regional market forces, technology trends, growth opportunities and in-depth intelligence on over a dozen leading vendors of handheld barcode scanners.

WHAT QUESTIONS ARE ADDRESSED?

- What is the new basis of competition in the handheld industry? What is the forecast for post-pandemic growth, and what are the underlying drivers?

- How do vendors need to formulate product and market development to compete in this highly commoditized industry?

- How will traditional vertical markets and geographical regions perform in the near- and long-term for handheld barcode offerings?

- What are the changing verticals for handhelds? How are handhelds marketed in conjunction with other technologies, such as emerging wearables?

- Who and the leading and emerging handheld scanner vendors and how are they competing?

- What impact is software-based scanning and other data collection technologies such as RFID having on the handheld scanner market?

WHO SHOULD READ THIS REPORT?

This annual research has been carefully designed for senior managers and executives at barcode technology and solution provider companies, especially individuals in the following roles:

- CEOs and supporting C-level management

- Corporate development and M&A professionals

- Product Management and Marketing professionals

- Strategic Directors and Marketing Communications managers

- Business development and sales

- Channel developers and managers

- Senior management of leading retailers

VENDORS COVERED IN THIS REPORT:

|

|

|

EXECUTIVE SUMMARY:

Following several years of volatile performance - driven in part by the impact of the pandemic, supply chain constraints, inflationary pricing and shifts in demand by sector - the market is projected to normalize and transition to a more predictable growth pattern. Near term, the market will need to work through issues related to channel over-stock and continued pricing volatility. In addition, challenges from alternative form factors (such as wearable scanners) and the growing presence of SW-based scanning that leverages cameras in smart mobile devices (smartphones, tablets, etc.) could erode some of the opportunity traditionally supported by purpose-built handheld scanners.

KEY FINDINGS:

Channel overstock is slowing near-term sales: Following a generally strong Q1 2023, leading vendors are expecting softening demand patterns through the end of the year due in part to overstocking of products among channel partners. Distribution partners accumulated high stocks during the pandemic and post-pandemic period when they filled backlogged orders. The market will take some time to absorb the products that have been shipped to distributors and partners. VDC expects this issue to subside by the first half of 2024.

Healthcare as a growth market: While the healthcare sector has shown consistent historical demand for handheld scanners, opportunities in this sector have increased substantially over the past couple of years. This is especially evident in North America where healthcare is the third largest market for handheld scanners, behind retail and manufacturing. Demand in the healthcare sector is also characterized by higher value and more specialized solutions, including the need for specialized plastics that resist the disinfectants used in healthcare settings.

Differentiation beyond the scanner: With the transition to 2D scanners largely complete (from legacy laser scanners and linear imagers), OEMs are looking for alternative options to competitively differentiate their portfolios. Some of this will be designing scanners for specialized use cases - such as healthcare scanners that can tolerate disinfectants or ruggedized scanners for industrial use cases. In addition, OEMs have been investing more in software utilities for customers to support and manage their scanner fleets. They are also leveraging the scan engine's capabilities to support more sophisticated data capture applications, such as scanning multiple codes simultaneously, identifying the correct symbology to decode or supporting OCR and other image capture and image processing capabilities.

Shifting competitive landscape: While the top three global handheld scanner OEMs (Zebra, Honeywell and Datalogic) are well positioned with a differentiated product portfolio and strong partner networks, the competitive landscape is changing. The emergence of cost-competitive products from vendors in Asia continues, although several rely on the leading OEMs to source scan engines. In addition, alternative form factors are challenging some traditional handheld scanner use cases. In logistics environments, for example, the use of glove or top of hand scanners have become especially popular, providing a more ergonomic and seamless option for scan-intensive applications that benefit hands-free operations. In addition, the performance of software-based scanning solutions continues to improve, challenging the dedicated scan engine status quo (although this is more of a challenge to mobile computers with integrated scanners).

ABOUT THE AUTHORS:

Andy Adelson

Currently serving VDC's AutoID & Data Capture practice, Andy Adelson has spent his career as an analyst, consultant and research expert. During the first half of his career, Andy excelled as an IT industry analyst, covering several technologies which were precursors and adjacent to AI&DC. He has provided continuous syndicated services, plus consults to clients for their more complex challenges. During the past decade, Andrew held executive sales and management roles with research and insights providers. Andy also serves on the Board of the New England chapter of The Insights Association, the largest US trade association for research professionals. Andy earned an MBA from Babson in Marketing, and a BA from the University of Michigan in English and Economics.

Richa Gupta

Richa is a Consultant working for VDC's AutoID & Data Capture practice. She has been tracking the markets for a range of AIDC technologies at VDC since 2010, including, but not limited to, barcode scanners and printers, labeling solutions, machine vision solutions, and robotics automation. Over the years, she has undertaken market opportunity sizing and forecasting, competitive landscape analysis, and offered strategic marketing assistance, while also providing valuable thought leadership for this technology segment. Richa holds a degree in Computer Engineering and an MBA from India.

David Krebs

David has more than twenty years' experience covering enterprise and government mobility solutions, wireless infrastructure and automatic identification and data capture technologies. David's research focuses on the intersection of digital and mobile solutions with today's business and mission critical frontline mobile workforce and how organizations are leveraging mobile solutions to improve workforce productivity and enhance customer engagement. David's consulting and strategic advisory experience is far reawching and includes technology and market opportunity assessments, technology penetration and adoption analysis, product and service development and M&A due diligence support. David has extensive primary market research management and execution experience to support market sizing and forecasting, total cost of ownership (TCO), comparative product performance evaluation, competitive benchmarking and end user requirements analysis. David is a graduate of Boston University (BSBA).

Table of Contents

Executive Summary

- Key Findings

Global Market Overview

- Vertical Markets

- Retail

- Industrial/Manufacturing

- Healthcare

- Transportation & Logistics

- Commercial Services

- Market Trends

- Sunrise 2027 - GS1

- 2D, Laser and Linear

- Software-Based Scanning

- Product Trends

- Wearables

- Backlogs and Component Shortages

Regional Forecasts

- Americas

- EMEA

- Asia Pacific

Vendor Insights & Profiles

About VDC Research

Report Exhibits

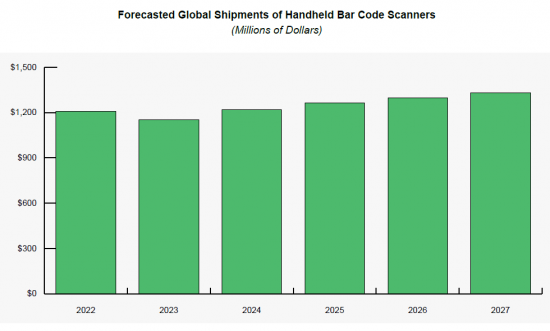

- Exhibit 1: Forecasted Global Shipments of Handheld Bar Code Scanners (Millions of Dollars)

- Exhibit 2: Forecasted Global Shipments of Handheld Bar Code Scanners Segmented by Product Type (Millions of Dollars)

- Exhibit 3: Forecasted Global Shipments of Handheld Bar Code Scanners Segmented by Product Type (Thousands of Units)

- Exhibit 4: Long-Term Global Shipments of Handheld Barcode Scanners (Millions of Dollars)

- Exhibit 5: Forecasted Global Shipments of Handheld Barcode Scanners Segmented by Economic Sector (Millions of Dollars)

- Exhibit 6: Forecasted Americas Shipments of Handheld Barcode Scanners Segmented by Product Type (Millions of Dollars)

- Exhibit 7: Forecasted EMEA Shipments of Handheld Barcode Scanners Segmented by Product Type (Millions of Dollars)

- Exhibit 8: Forecasted Asia-Pacific Shipments of Handheld Barcode Scanners Segmented by Product Type (Millions of Dollars)

- Exhibit 9: Global Vendor Shares of Handheld Barcode Scanners (Percentage of Dollars)

Dataset Exhibits

- Exhibit 1: Forecasted Global Shipments of Handheld Barcode Scanners Segmented by Product Type (Millions of Dollars)

- Exhibit 2: Forecasted Global Shipments of Handheld Barcode Scanners Segmented by Product Type (Thousands of Units)

- Exhibit 3: Forecasted Global Shipments of Handheld Barcode Scanners Segmented by Product Type (Average Factory Selling Price (AFSP) - Dollars)

- Exhibit 4: Forecasted Global Shipments of Handheld Laser Barcode Scanners Segmented by Scanning Technology (Millions of Dollars)

- Exhibit 5: Forecasted Global Shipments of Handheld Laser Barcode Scanners Segmented by Scanning Technology (Thousands of Units)

- Exhibit 6: Forecasted Global Shipments of Handheld Laser Barcode Scanners Segmented by Scanning Technology (Average Factory Selling Price (AFSP) - Dollars)

- Exhibit 7: Forecasted Global Shipments of Handheld Laser Barcode Scanners Segmented by Ruggedization (Millions of Dollars)

- Exhibit 8: Forecasted Global Shipments of Handheld Linear Imager Barcode Scanners Segmented by Ruggedization (Millions of Dollars)

- Exhibit 9: Forecasted Global Shipments of Handheld 2D Imager Barcode Scanners Segmented by Ruggedization (Millions of Dollars)

- Exhibit 10: Forecasted Global Shipments of Handheld Barcode Scanners Segmented by Connectivity (Millions of Dollars)

- Exhibit 11: Forecasted Global Shipments of Handheld Barcode Scanners Segmented by Economic Sector (Millions of Dollars)

- Exhibit 12: Forecasted Global Shipments of 2D Imager Barcode Scanners Segmented by Economic Sector (Millions of Dollars)

- Exhibit 13: Forecasted Global Shipments of Linear Imager Barcode Scanners Segmented by Economic Sector (Millions of Dollars)

- Exhibit 14: Forecasted Global Shipments of Laser Barcode Scanners Segmented by Economic Sector (Millions of Dollars)

- Exhibit 15: Forecasted Global Shipments of Handheld Barcode Scanners Segmented by Distribution Channel (Millions of Dollars)

- Exhibit 16: Forecasted Global Shipments of 2D Imager Barcode Scanners Segmented by Distribution Channel (Millions of Dollars)

- Exhibit 17: Forecasted Global Shipments of Linear Imager Barcode Scanners Segmented by Distribution Channel (Millions of Dollars)

- Exhibit 18: Forecasted Global Shipments of Laser Barcode Scanners Segmented by Distribution Channel (Millions of Dollars)

- Exhibit 19: Forecasted Global Shipments of Handheld Barcode Scanners by Country Market (Millions of Dollars)

Market Analysis - Americas

- Exhibit 1: Forecasted Americas Shipments of Handheld Barcode Scanners Segmented by Product Type (Millions of Dollars)

- Exhibit 2: Forecasted Americas Shipments of Handheld Barcode Scanners Segmented by Product Type (Thousands of Units)

- Exhibit 3: Forecasted Americas Shipments of Handheld Barcode Scanners Segmented by Product Type (Average Factory Selling Price (AFSP) - Dollars)

- Exhibit 4: Forecasted North American Shipments of Handheld Barcode Scanners Segmented by Product Type (Millions of Dollars)

- Exhibit 5: Forecasted North American Shipments of Handheld Barcode Scanners Segmented by Product Type (Thousands of Units)

- Exhibit 6: Forecasted North American Shipments of Handheld Barcode Scanners Segmented by Product Type (Average Factory Selling Price (AFSP) - Dollars)

- Exhibit 7: Forecasted Central & Latin American Shipments of Handheld Barcode Scanners Segmented by Product Type (Millions of Dollars)

- Exhibit 8: Forecasted Central & Latin American Shipments of Handheld Barcode Scanners Segmented by Product Type (Thousands of Units)

- Exhibit 9: Forecasted Central & Latin American of Handheld Barcode Scanners Segmented by Product Type (Average Factory Selling Price (AFSP) - Dollars)

- Exhibit 10: Forecasted Americas Shipments of Handheld Laser Barcode Scanners Segmented by Scanning Technology (Millions of Dollars)

- Exhibit 11: Forecasted Americas Shipments of Handheld Laser Barcode Scanners Segmented by Scanning Technology (Thousands of Units)

- Exhibit 12: Forecasted Americas Shipments of Handheld Laser Barcode Scanners Segmented by Scanning Technology (Average Factory Selling Price (AFSP) - Dollars)

2024-2032 年按产品、类型、扫描器类型、技术、组件、最终用途行业和地区分類的条码扫描器市场报告

2024-2032 年按产品、类型、扫描器类型、技术、组件、最终用途行业和地区分類的条码扫描器市场报告 条码扫描器市场:按产品类型、技术和最终用途 – 2023-2030 年全球预测

条码扫描器市场:按产品类型、技术和最终用途 – 2023-2030 年全球预测 全球条码扫描仪市场

全球条码扫描仪市场 产业用条形码扫描仪市场:趋势,机会,竞争分析【2023-2028年】

产业用条形码扫描仪市场:趋势,机会,竞争分析【2023-2028年】 条码扫描仪市场 - 2023 年至 2028 年预测

条码扫描仪市场 - 2023 年至 2028 年预测 产业用条形码扫瞄仪的全球市场 2023-2027

产业用条形码扫瞄仪的全球市场 2023-2027 条码扫描器的全球市场调查报告-产业分析,规模,占有率,成长,趋势,2022年~2028年前的预测

条码扫描器的全球市场调查报告-产业分析,规模,占有率,成长,趋势,2022年~2028年前的预测 条码扫描器的全球市场:各扫描机类型,各类别,各地区分析-预测(~2028年)

条码扫描器的全球市场:各扫描机类型,各类别,各地区分析-预测(~2028年) 条码扫描器的全球市场:各产品类型(手持,固定型),终端用户,技术(笔型读取器,雷射扫描机,CCD读取器,相机为基础的读取器),地区,规模,占有率,展望,机会分析(2022年~2028年)

条码扫描器的全球市场:各产品类型(手持,固定型),终端用户,技术(笔型读取器,雷射扫描机,CCD读取器,相机为基础的读取器),地区,规模,占有率,展望,机会分析(2022年~2028年)