|

市场调查报告书

商品编码

1964918

无电池化催生巨大的新市场:2026-2046Battery Elimination Creates Large New Markets 2026-2046 |

||||||

摘要

预计2026年至2046年间,电能储存市场规模将成长三倍以上。特别是无电池储能,预计将呈指数级成长,达到惊人的4,100亿美元,市场占有率将从20%成长至约40%。

电池市场预计在未来20年内达到饱和。这主要是由于激烈的价格竞争、电动车市场(最大的应用领域)成长放缓,以及无法满足重要且快速成长的新兴市场的需求,例如电网、资料中心和微电网的长期储能,以及电磁武器和核融合发电等脉衝功率应用。无电池储能技术在新兴应用中具有更高的安全性、显着延长的使用寿命和更低的平准化储能成本(LCOS)。光是抽水蓄能发电一项,每年就已创造超过 500亿美元的收入。

此外,完全无需储能的新型系统崛起,成为一个价值数十亿美元的新兴市场。例如,计画中的第六代(6G)第二阶段将采用反向散射技术为客户端设备供电,而穿戴式装置将采用多模式能量采集技术。

本报告深入分析了无电池技术市场,并全面概述了市场背景、电池面临的挑战和无电池设备的发展趋势、电池储能设备与非电池储能设备的市场规模趋势和预测、主要无电池技术的概述、研发趋势、关键企业举措以及企业简介。

标题:储能设备市场(电池 vs. 非电池)来源:Zhar Research 报告 "Battery Elimination Creates Large New Markets 2026-2046"

目录

第1章 执行摘要与结论

- 报告目标和范围

- 研究方法

- 主要结论

- 电池目前面临的挑战以及替代方案的采用原因

- 无电池方案:淘汰储能还是采用替代储能

- 从感测器到吉瓦级电力,电池淘汰趋势

- 除直接替换电池之外,还有更多无电池储能方案可供选择设备

- 资讯图表:13 种摆脱电网 LDES 的途径

- 资讯图表:摆脱资料中心微电网及类似 LDES 的途径

- 无电池储能设备工具包及 SWOT 分析

- 路线图

- 市场预测

第2章 引言

- 概述

- 电池的局限性

- 锂离子电池起火事故持续发生

- 电气化、电池应用及电池淘汰的宏观趋势

- 对储能的影响

- 电池供电和无电池固定式储能技术的持续时间和功率关係及未来趋势

- 电池市场占有率预计下降

- 对 LDES 的需求及设计原则

第3章 摆脱电池的途径:反向散射(EAS、RFID、6G SWIPT)、无电池电路、其他电子方案和 LDES 路径

- 概述

- 无电池储存设备以外的电池替代方案

- 减少或消除储存的策略

- 实现可组合的自供电无电池设备

- 反向散射通讯和 SWOT 分析

- 电子商品防盗系统(EAS)、被动式 RFID 等

- 用于 6G 通讯和物联网的SWIPT AmBC 和 CD-ZED

- SWOT 和其他发展

- 最大限度缩短电池寿命的电路设计

- 无电池电路(BEC):在无人机和电动车中的应用

- 间歇性电源的电子技术: BFree

- V2G、V2H、V2V 以及太阳能板直接充电,以减少或消除电池

- 需求管理:无储存太阳能海水淡化系统

- 能源资源管理的进展

- 调整规格以消除电池

- 无电池无人机(感测器/物联网应用)

- 无电池相机

- 无电池能量采集

- 主要能量采集技术概述与比较

- 能量采集系统的组成要素

- 机械能量采集详情,包括声能采集

- 电磁能量撷取详情

- 柔性层流能量采集的重要性

- 摆脱长期储能(LDES)的途径

- 整体状况两张资讯图

- 全球案例:丹麦、新加坡、中国和美国

- 风能和太阳能容量係数与低能耗系统需求的关係

- 低能耗系统规避技术研究

- 家庭能源管理系统研究

第4章 抽水蓄能发电(PHES/APHES)

- 传统抽水蓄能发电概述

- 研究进展与展望

- 全球专案与规划

- 经济效益

- 政策建议

- 抽水蓄能发电性能评估

- 抽水蓄能发电的SWOT分析

- 非山区先进抽水蓄能发电

- APHES概述及SWOT分析

- 矿区利用

- 地下加压法(Quidnet Energy)

- 重水利用法(RheEnergise)

- 海水/盐水利用(洞穴能源、大型能源等)

- 海底储能(StEnSea、Ocean Grazer)

- 水下储能的SWOT分析

- 混合技术

- 最新研究

第5章 固体重力储能(SGES)

- 概述及研究进展

- 概述

- 三阶段运行流程

- 三种结构类型

- 与抽水蓄能发电的比较

- 基本原理

- SGES SWOT分析

- SGES效能评估

- 资本支出问题

- 运行成本问题

- 使用沙子的可能性

- 液压活塞系统替代电缆

- 其他SGES研究

第6章 压缩空气储能(CAES)

- 概述与研究进展

- 市场拓展与模仿技术

- 市场定位

- SWOT分析与参数比较

- CAES技术选项

- 热力学

- 等容或等压储能

- 绝缘

- CAES专案、子系统製造商和目标

- 概要:中国最大的项目

- Siemens Energy Germany

- MAN Energy Solutions Germany

- 延长CAES储能与放电週期

- 英国和欧盟的研究

- CAES公司简介

- ALCAES Switzerland

- APEX CAES USA

- Augwind Energy Israel

- Keep Energy Systems UK formerly Cheesecake

- Corre Energy Netherlands

- Huaneng Group China

- Hydrostor Canada

- LiGE Pty South Africa

- Storelectric UK

- Terrastor Energy Corporation USA

第7章 延迟供电热能储存(ETES)

- 概述与研究进展

- 从失败中学到的教训:Siemens Gamesa, Azelio, Steisdal, Lumenion

- 热机方法的进展:Echogen USA

- 超高温 + 太阳能电池方法

- Antora USA

- Fourth Power USA

- 热电联产电站

- MGA Thermal Australia

- Malta Inc Germany

第8章 含氢及其他化学中间体的低密度储能系统

- 概述及研究进展

- 低密度储能系统中氢气储存参数的评估

- 低密度储能系统中的氢气、甲烷和氨:SWOT分析

- 实际专案案例

- 研究表明,氢气储存系统(H2ES)仅适用于季节性储存应用,但未来可能仍有其他需求。

- 由于缺乏运行资料,一些计算得出了不同的结论。

- LDES系统中氢气储存的候选技术

第9章 静电储存:超级电容器、赝电容器、锂离子电容器及其他BSH应用

- 电容器及其衍生产品的寻找途径

- 选择范围:从电容器到超级电容器到电池

- 研究方向:纯超级电容器

- 研究方向:混合方法

- 研究方向:赝电容器

- 超级电容器及其衍生产品的实际和潜在关键应用

- 概述

- 航空航太

- 电动车:AGV、物料搬运、汽车、卡车、巴士、电车、火车

- 电网、微电网、削峰、再生能源不间断电源(UPS)

- 医疗及穿戴设备

- 军事:雷射炮、电磁轨道炮、脉衝线性加速武器、雷达、卡车等

- 电力及讯号电子,资料中心即时恢復

- 焊接

- 超级电容器公司分析(103 家公司)

- 锂离子电容器及其他电池、超级电容器、混合 BSH 储能

- 定义及选项

- 市场定位

- 能量密度比较

- 资讯图表:市场需求与技术比较

- 研究分析及建议

- SWOT 分析及路线图

Summary

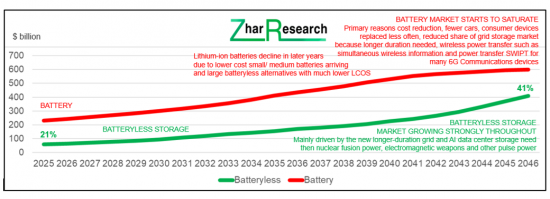

From 2026-2046, the electrical energy storage market will more than triple but the battery-less storage part will surge to a massive $410 billion - about 40% from 20% today. Time to look beyond batteries. On cue we have the new Zhar Research 546-page report, "Battery Elimination Creates Large New Markets 2026-2046" detailing this massive opportunity.

Within 20 years the battery value market will saturate due to vicious price wars, the largest application - electric cars - levelling and the inability of batteries to perform to the requirements of important new, fast-growing markets. These include months of grid, data center and microgrid storage, and pulsing new electromagnetic weapons and nuclear fusion power. Increasingly, batteryless storage is safer, with much longer life and able to provide lower Levelised Cost of Storage LCOS in the growth applications. Already, pumped hydro alone sells at over $50 billion yearly.

Another emerging multi-billion-dollar market will be for new systems that eliminate energy storage completely, such as planned 6G Communications Phase Two using backscatter for client devices. Wearables adopt multi-mode energy harvesting. Uniquely, this report appraises the commercial opportunity for all this with 133 company batteryless activity profiles.

The Executive Summary and Conclusions (58 pages) is sufficient for those with limited time. Here are the basics, methodology, key conclusions, technology comparisons, ongoing battery limitations, emerging large batteryless applications, 12 SWOT appraisals of the toolkit and 35 forecasts as tables and graphs with explanation. The Introduction (36 pages) details energy fundamentals, ongoing battery limitations. Understand why batteries will retain the dominant share of energy storage value markets 2026-2046 but lose share rapidly. Grasp emerging applications that batteries poorly address such as coping with long intermittency of wind and solar power everywhere. See the performance parameters of current batteryless solutions against batteries.

The rest of the report presents a through investigation of escape routes from batteries and sometimes from all energy storage. Specific batteryless technologies are detailed including research advances through 2025-6. The 78 pages of Chapter 3 closely examine "Escape routes from batteries: backscatter (EAS, RFID, 6G SWIPT), battery elimination circuits, other electronics options, LDES escape routes". Understand increasing deployment of escape routes from batteries and energy storage generally and the heroic future plans. The largest deployment of electronics in numbers is passive RFID tags and their subset anti-theft tags, none with energy storage. Next, their backscatter principle will be applied to 6G Communications client devices such as internet of things IOT tags also in tens of billions of units. See how the intermittency of wind and solar power can be sometimes tolerated and other times reduced without storage.

Chapter 4. Pumped hydro: conventional PHES and advanced APHES (74 pages) presents what is already selling at over $50 billion yearly, the improvements ahead including avoiding the need for mountainsides and the use of seawater. Realise that this takes the batteryless opportunity beyond massive grid storage to smaller applications. See the activities and intentions of key companies involved and 2025-6 research papers.

Chapter 5. Solid gravity energy storage SGES (37 pages) involves lifting weights instead of water as an improvement on grid batteries. Invented in Europe, it is most energetically pursued in China, initially as many huge buildings providing hours of grid storage but potentially even seasonal. See latest research and structures and the ongoing work on variants, including company profiles of use in mines in Europe and Australia.

Chapter 6. Compressed air energy storage CAES has 64 pages because there are ten companies profiled and widespread use worldwide mainly in huge underground caverns for hours of duration and potentially months (beyond batteries). So far, CAES is the strongest pumped hydro competitor. Contrast Chapter 7. Thermal energy storage for delayed electricity ETES where only four companies can be profiled and lessons of a number of exits are presented. Some new proponents have pivoted to combined heat and power or to thermovoltaic versions with white heat. Understand one large commercial version of ETES in Alaska using heat pumps.

Chapter 8. Hydrogen and other chemical intermediary LDES explains how use of intermediary chemical production and then converting it all back to electricity is very inefficient but hydrogen is more attractive than other gases for this. Enthusiasm for the Hydrogen Economy meets serious challenges of safety, leaking through everything and indirectly causing global warming. Use in salt caverns is strongly advocated by the Royal Society in the UK and many other eminent bodies because it can delay the most GWh, they say even seasonally. However, large H2ES projects are not being funded beyond China on hydrogen generally with electricity-to-electricity as a back story. See the small microgrid application in the USA using overground tanks for 24-hour duration and future plans.

Primary author and CEO of Zhar Research Dr Peter Harrop advises, "From all this it is clear that batteries are losing the extremes of grid storage and pulse/ fast charge-discharge applications so the report ends with the latter toolkit - essentially supercapacitors and their variants - in detail."

Chapter 9. "Electrostatic storage: Supercapacitors, pseudocapacitors, lithium-ion capacitors, other BSH" is the longest chapter at 118 pages because 103 companies are profiled plus a deep dive into the strongly emerging needs including massive banks pulsing nuclear fusion power. Sections cover aircraft and aerospace; electric vehicles: AGV, material handling, car, truck, bus, tram, train; grid, microgrid, peak shaving, renewable energy, uninterrupted power supplies, medical and wearables. Importantly see military: laser cannon, railgun, pulsed linear accelerator weapon, radar, trucks, other pulse-power electronics, data center instant emergency power, welding, pulse metal forming. Since most of the big applications emerge late in the 2026-2046 timeframe, the forecasts only take this to around $14 billion. Add a minor part of the regular capacitor business of around $70 billion at that time. However, there is considerable upside potential on these forecasts.

The new Zhar Research 548-page report, "Battery Elimination Creates Large New Markets 2026-2046" is your essential source of opportunities and latest research in this exciting emerging business serving the future - from nuclear fusion power to AI data centers, smart grids and microgrids.

CAPTION: Energy storage device market battery vs batteryless $ billion 2025-2046. Source: Zhar Research report, "Battery Elimination Creates Large New Markets 2026-2046".

Table of Contents

1. Executive summary and conclusions

- 1.1 Purpose and scope of this report

- 1.2 Methodology of this analysis

- 1.3 Primary conclusions

- 1.4 Battery current challenges and why alternatives are being adopted

- 1.4.1 General situation in electronics and electrical engineering

- 1.4.2 Lithium-ion battery fires are ongoing emitting toxic gas

- 1.4.3 Energy storage decision tree with battery-free examples

- 1.4.4 Battery emerging challenges 2026-2046

- 1.4.5 Battery challenges for 6G Communications and IoT and action arising 2026-2046

- 1.5 Battery-free options: eliminating storage or using alternative storage 2026-2046

- 1.6 Battery elimination trend from sensors to GW power

- 1.7 Battery elimination options beyond drop-in replacement by battery-less storage devices

- 1.7.1 Electronics, telecommunication, electrical engineering

- 1.7.2 To the rescue: WPT, WIET, SWIPT evolution to 2046

- 1.7.3 Evolution of wireless electronic devices needing no on-board energy storage 1980-2046

- 1.7.4 13 primary energy harvesting technologies compared

- 1.8 Infogram: 13 escape routes from grid LDES 2026-2046

- 1.9 Infogram: Escape routes from data center microgrid and similar LDES 2026-2046

- 1.10 Battery-less storage device toolkit 2025-2045 with SWOT appraisals

- 1.10.1 Options by size

- 1.10.2 Example: Lithium-ion capacitor LIC market positioning by energy density spectrum

- 1.10.3 Long duration energy storage LDES toolkit for grids, microgrids, 6G base stations, data centers 2026-2046

- 1.10.4 Possible scenario: stationary storage batteries vs alternatives TWh cumulative 2026-2046

- 1.10.5 Duration hours vs power delivered by project and 12 technologies in 2026

- 1.10.6 System strategies to achieve less or no storage: combine and compromise

- 1.10.7 Enablers of self-powered, battery-free devices that can be combined

- 1.10.6 12 SWOT appraisals of the battery-less device toolkit

- 1.11 Roadmaps 2026-2046

- 1.12 Market forecasts 2026-2046 in 35 lines

- 1.12.1 Energy storage device market battery vs batteryless $ billion 2025-2046

- 1.12.2 Battery-less storage for electricity-to-electricity $ billion 2025-2046 in 11 lines

- 1.12.3 Battery-less storage for pulse and fastest response $ billion 2025-2046 in 4 lines

- 1.12.4 LDES market in 9 technology categories $ billion 2026-2046 table, graphs, explanation

- 1.12.5 Total LDES value market % in three size categories 2026-2046 table, graph, explanation

- 1.12.6 Regional share of LDES value market % in four regions 2026-2046 table, graph, explanation

- 1.12.7 Market for seven types of equipment fitting battery-free storage $ billion 2025-2046

2. Introduction

- 2.1 Overview

- 2.2 Battery limitations

- 2.3 How lithium-ion battery fires are ongoing

- 2.4 Megatrends of electrification, battery adoption and battery elimination

- 2.5 Implications for storage 2026 - 2046

- 2.6 Duration vs power of many battery and batteryless stationary storage technologies deployed and deploying in 2025 showing future trends

- 2.7 How batteries will lose share 2026-2046

- 2.8 LDES need and design principles

- 2.8.1 Energy fundamentals

- 2.8.2 Racing into renewables with rapid cost reduction: 2025 statistics and trends

- 2.8.3 Solar winning and the intermittency challenge

- 2.8.4 Adoption of LDES of increasing duration driven by increased wind/solar percentage and cost reduction

- 2.8.5 LDES definitions and needs

- 2.8.6 LDES metrics

- 2.8.7 LDES projects in 2025-6 showing leading technology subsets

- 2.8.8 LDES impediments, alternatives and investment climate

- 2.8.9 LDES toolkit

- 2.8.10 Latest independent assessments of performance by technology

- 2.8.11 Leading reports on LDES 2026-2046

- 2.8.12 Example: Installed and committed stationary storage projects 2026 showing many battery and battery-less options competing

3. Escape routes from batteries: backscatter (EAS, RFID, 6G SWIPT), battery elimination circuits, other electronics options, LDES escape routes

- 3.1 Overview

- 3.1.1 Battery elimination options beyond drop-in replacement by battery-less storage devices

- 3.1.2 Strategies to achieve less or no storage

- 3.1.3 Enablers of self-powered, battery-free devices that can be combined

- 3.2 Backscatter with SWOT

- 3.2.1 Electronic Article Surveillance EAS , passive RFID and beyond

- 3.2.2 SWIPT AmBC and CD-ZED for 6G Communications and IOT

- 3.2.3 SWOT and 34 other advances in

- 3.3 Circuit design to minimise batteries

- 3.3.1 Battery elimination circuits BEC in drones and electric cars

- 3.3.2 Intermittency tolerant electronics: BFree

- 3.4 Battery reduction and elimination by V2G, V2H, V2V and vehicle charging directly from solar panels

- 3.5 Demand management: storage-free solar desalinators

- 3.6 Source management advances

- 3.7 Specification compromise eliminates batteries

- 3.7.1 Battery-free drones as sensors and IOT

- 3.7.2 Battery-free cameras

- 3.8 Energy harvesting eliminating batteries

- 3.8.1 Overview and 13 primary energy harvesting technologies compared

- 3.8.2 Elements of a harvesting system

- 3.8.3 Mechanical harvesting including acoustic in detail

- 3.8.4 Harvesting of electromagnetic energy in detail

- 3.8.5 Importance of flexible laminar energy harvesting 2026-2046

- 3.9 Escape routes from Long Duration Energy Storage LDES

- 3.9.1 General situation with two infograms

- 3.9.2 Examples across the world: Denmark, Singapore, China, USA

- 3.9.3 Capacity factor of wind, solar and options that need little or no LDES

- 3.9.4 Extensive 2025 research on LDES escape routes

- 3.9.5 Research in 2025 on Home Energy Management Systems coping with

4. Pumped hydro: conventional PHES and advanced APHES

- 4.1 Conventional PHES overview

- 4.1.1 Three options

- 4.1.2 History, environmental, timescales, potential sites, DOE appraisal

- 4.1.3 Site-limited primarily due environmental concerns not number of appropriate topologies

- 4.1.4 Problem analysis, actions to reduce PHES emissions, ugliness, water use, cost

- 4.2 Research advances and view of potential through 2025

- 4.3 Projects and intentions across the world

- 4.3.1 Geographical

- 4.3.2 Large pumped hydro schemes worldwide

- 4.4 Economics

- 4.5 Policy recommendations

- 4.6 Parameter appraisal of conventional pumped hydro PHES

- 4.7 SWOT appraisal of conventional pumped hydro PHES

- 4.8 Advanced pumped hydro does not need mountains

- 4.8.1 APHES overview with SWOT

- 4.8.2 Using mining sites including research advances through 2025-6

- 4.8.3 Pressurised underground: Quidnet Energy USA

- 4.8.4 Using heavier water up mere hills: RheEnergise UK

- 4.8.5 Using seawater or other brine: Cavern Energy, Sizable Energy, others, SWOT

- 4.8.6 StEnSea Germany, Ocean Grazer Netherlands

- 4.8.7 SWOT appraisal of underwater energy storage for LDES

- 4.8.8 Hybrid technologies: research advances in 2024 and 2025

- 4.8.9 Research advances in 2024 and 2025

5. Solid gravity energy storage SGES

- 5.1 Overview including research in 2025

- 5.1.1 General

- 5.1.2 Three stages of operation

- 5.1.3 Three geometries

- 5.1.4 Pumped hydro gravity storage compared to the three SGES options

- 5.1.5 Basics

- 5.1.6 SWOT appraisal of solid gravity storage SGES for LDES

- 5.1.7 Parameter appraisal of solid gravity energy storage SGES for LDES

- 5.1.8 CAPEX challenge

- 5.1.9 Challenge of ongoing expenses

- 5.1.10 Possibility of pumping sand

- 5.1.11 Hydraulic piston lift instead of cable: 2025 modelling

- 5.1.12 Appraisal of other SGES research through 2025

- 5.2 ARES USA

- 5.3 Energy Vault Switzerland, USA and China, India licensees

- 5.4 Gravitricity

- 5.5 Green Gravity Australia

- 5.6 SinkFloatSolutions France

6. Compressed air energy storage CAES

- 6.1 Overview including research advances announced in 2025

- 6.1.1 Basics

- 6.1.2 Research advances in 2025

- 6.2 Undersupply attracts clones

- 6.3 Market positioning of CAES

- 6.4 SWOT appraisal and parameter comparison of CAES for LDES

- 6.5 CAES technology options

- 6.5.1 Thermodynamic

- 6.4.2 Isochoric or isobaric storage

- 6.4.3 Adiabatic choice of cooling is winning

- 6.6 CAES projects, subsystem manufacturers, objectives, research 2025 onwards

- 6.6.1 Overview: largest projects are in China

- 6.6.2 Siemens Energy Germany

- 6.6.3 MAN Energy Solutions Germany

- 6.6.4 Increasing the CAES storage time and discharge duration

- 6.6.5 Research in UK and European Union 2025 onwards

- 6.7 Profiles of CAES company progress with Zhar Research appraisals

- 6.7.1 ALCAES Switzerland

- 6.7.2 APEX CAES USA

- 6.7.3 Augwind Energy Israel

- 6.7.4 Keep Energy Systems UK formerly Cheesecake

- 6.7.5 Corre Energy Netherlands

- 6.7.6 Huaneng Group China

- 6.7.7 Hydrostor Canada

- 6.7.8 LiGE Pty South Africa

- 6.7.9 Storelectric UK

- 6.7.10 Terrastor Energy Corporation USA

7. Thermal energy storage for delayed electricity ETES

- 7.1 Overview and research advances in 2025

- 7.2 Research advances in 2025 and 2024

- 7.3 Lessons of failure: Siemens Gamesa, Azelio, Steisdal, Lumenion

- 7.4 The heat engine approach proceeds: Echogen USA

- 7.5 Use of extreme temperatures and photovoltaic conversion

- 7.5.1 Antora USA

- 7.5.2 Fourth Power USA

- 7.6 Marketing delayed heat and electricity from one plant

- 7.6.1 Overview

- 7.6.2 MGA Thermal Australia

- 7.6.3 Malta Inc Germany

8. Hydrogen and other chemical intermediary LDES

- 8.1 Overview with research progress in 2025-6

- 8.1.1 Overview

- 8.1.2 Sweet spot for chemical intermediary LDES but safety issues

- 8.1.3 Mainstream research through 2025-6

- 8.1.4 Research dreaming of niches through 2025-6

- 8.1.5 Research on complex mechanisms for hydrogen loss

- 8.1.6 Research on hydrogen leakage causing global warming

- 8.1.7 Examples of hydrogen storage advances 2025-6

- 8.2 Parameter appraisal of hydrogen storage for LDES

- 8.3 SWOT appraisal of hydrogen, methane, ammonia for LDES

- 8.4 The small number of actual projects

- 8.4.1 Calistoga Resiliency Centre USA 48-hour microgrid

- 8.4.2 Ulm University microgrid trial Germany 2025-2027

- 8.4.3 China plans in 2025 and 2026

- 8.5 Calculations showing H2ES best only for seasonal storage, needed later

- 8.6 Calculations with other conclusions partly due to lack of operating data

- 8.7 Candidate technologies for hydrogen storage within LDES systems

9. Electrostatic storage: Supercapacitors, pseudocapacitors, lithium-ion capacitors, other BSH

- 9.1 The place of capacitors and their variants

- 9.2 Spectrum of choice - capacitor to supercapacitor to battery

- 9.3 Research pipeline: pure supercapacitors

- 9.4 Research pipeline: hybrid approaches

- 9.5 Research pipeline: pseudocapacitors

- 9.6 Actual and potential major applications of supercapacitors and their derivatives

- 9.6.1 Overview

- 9.6.2 Aircraft and aerospace

- 9.6.3 Electric vehicles: AGV, material handling, car, truck, bus, tram, train

- 9.6.4 Grid, microgrid, peak shaving, renewable energy and uninterrupted power supplies

- 9.6.5 Medical and wearables

- 9.6.6 Military: Laser cannon, railgun, pulsed linear accelerator weapon, radar, trucks, other

- 9.6.7 Power and signal electronics, data center instant recovery

- 9.6.8 Welding

- 9.7 103 supercapacitor companies assessed in 10 columns

- 9.8 Lithium-ion capacitors and other battery-supercapacitor hybrid BSH storage

- 9.8.1 Definitions and choices

- 9.8.2 BSH market positioning and choices and LIC market positioning by energy density spectrum

- 9.8.3 Infograms: the most impactful market needs, comparative solutions, 13 conclusions

- 9.8.4 Research analysis and recommendations 2025-2045

- 9.8.5 Two SWOT appraisals and roadmap 2025-2045

氨基储能市场预测:至2034年-按储能类型、技术、应用、最终用户和地区分類的全球分析

氨基储能市场预测:至2034年-按储能类型、技术、应用、最终用户和地区分類的全球分析 雷射核融合中子源市场:按雷射类型、能量范围、应用和终端用户产业划分-全球预测,2026-2032年

雷射核融合中子源市场:按雷射类型、能量范围、应用和终端用户产业划分-全球预测,2026-2032年 储能市场规模、份额和成长分析:按技术、连接方式、产品、应用、最终用途和地区划分-2026-2033年产业预测储能电感器市场按产品类型、磁芯材料、电路类型、绕组类型、输入电压、端子、应用和终端用户-全球预测,2026-2032年

储能市场规模、份额和成长分析:按技术、连接方式、产品、应用、最终用途和地区划分-2026-2033年产业预测储能电感器市场按产品类型、磁芯材料、电路类型、绕组类型、输入电压、端子、应用和终端用户-全球预测,2026-2032年 全球先进半导体市场规模、占有率及预测(依技术节点、产品类型、应用、终端用户产业及封装技术划分)

全球先进半导体市场规模、占有率及预测(依技术节点、产品类型、应用、终端用户产业及封装技术划分) 离网电池储能市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034年预测可再生能源併网电力电子元件,全球市场预测至2034年:按元件类型、应用、最终用户和地区划分

离网电池储能市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034年预测可再生能源併网电力电子元件,全球市场预测至2034年:按元件类型、应用、最终用户和地区划分 2026年全球人工智慧(AI)储能解决方案市场报告2026年全球可再生能源储存市场报告

2026年全球人工智慧(AI)储能解决方案市场报告2026年全球可再生能源储存市场报告 储能市场-全球产业规模、份额、趋势、机会和预测:按技术、类型、最终用户、地区和竞争格局划分,2021-2031年

储能市场-全球产业规模、份额、趋势、机会和预测:按技术、类型、最终用户、地区和竞争格局划分,2021-2031年