|

市场调查报告书

商品编码

1344552

自助超市感测器市场:按组件、类型:2023-2032 年全球机会分析与产业预测Self Service Supermarket Sensor Market By Component (Systems, Services), By Type (Cash Based System, Cashless Based Systems): Global Opportunity Analysis and Industry Forecast, 2023-2032 |

||||||

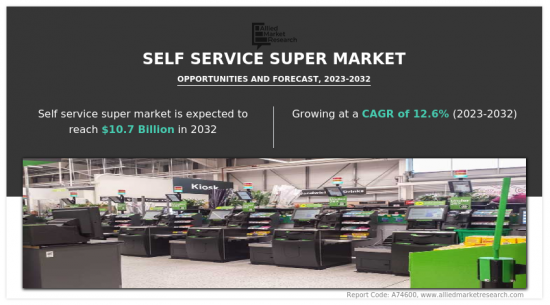

2022 年自助超市感测器市场价值为 34 亿美元,预计 2023 年至 2032 年复合年增长率为 12.6%,到 □□2032 年达到 107 亿美元。

自助超市感测器是零售企业、超市和医院的自动化技术,让顾客在没有工作人员帮助的情况下自助订购和结帐。 以前的自助结帐系统由在商店购买的单独零件组成,需要大量储存空间。 相反,更新和创建新的自助结帐系统是为了满足消费者需求、匹配业务布局并改善功能、成本、外形尺寸和可靠性。 由于对安全自助支付技术的需求不断增长,自助服务终端供应商已经提供无现金解决方案。

自助超市感测器技术彻底改变了大卖场的现代零售范式。 消费者,尤其是城市和郊区的消费者,对这种新颖的方法很感兴趣。 由于满足消费者基本需求和家居产品要求的广泛产品和品牌,大卖场吸引了消费者。 消费者积极参与购物体验的各个方面,使这种现代零售模式与众不同。 然而,科技的进步和对现代生活的日益重视正在加速自助式大卖场的出现。

为了满足精通科技的消费者的需求,大卖场的传统结帐作业正在透过引入自动化自助结帐站进行转变。 这些站点配备了最先进的自助超市感测器技术。 这些感测器允许顾客独立扫描和处理物品,加快结帐过程并减少对人类收银员的依赖。 这种完整的自助服务设计提供了符合现代消费者需求的无缝且高效的购物体验。

但是,某些挑战预计会阻碍自助超市感测器的采用,包括资料外洩、设备故障、网路钓鱼尝试、软体和网路缺陷。 例如,资料透过不安全的网路遭到骇客攻击的网路威胁风险很高。 资料骇客可以快速渗透和存取敏感资料和讯息,包括消费者企业帐户中的财务资讯。 结果,可能会发生重大的财务损失和声誉损害。 这是预计在预测期内阻碍市场收入成长的主要因素之一。

目录

第一章简介

第 2 章执行摘要

第三章市场概述

- 市场定义和范围

- 主要发现

- 影响因素

- 主要投资机会

- 波特五力分析

- 市场动态

- 促进因素

- 抑制因素

- 机会

- 新冠肺炎 (COVID-19):市场影响分析

- 平均售价

- 品牌占有率分析

- 主要监理分析

- 市占率分析

- 专利情况

- 监理指南

- 价值链分析

第 4 章自助超市感测器市场:按组成部分

- 摘要

- 系统

- 服务

第五章自助超市感测器市场:按类型

- 摘要

- 基于快取的系统

- 无现金系统

第六章自助超市感测器市场:按地区

- 摘要

- 北美

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳大利亚

- 其他亚太地区

- 拉丁美洲/中东/非洲

- 巴西

- 沙乌地阿拉伯

- 阿拉伯联合大公国

- 南非

- 其他拉丁美洲/中东/非洲

第七章竞争态势

- 简介

- 关键成功策略

- 10家主要公司的产品图谱

- 竞争对手仪表板

- 竞争热图

- 2022 年主要公司的定位

第八章公司简介

- Diebold Nixdorf, Incorporated

- ECR Software Corporation

- Fujitsu Limited

- Gilbarco Inc.

- ITAB Group

- NCR Corporation

- Pan-Oston

- PCMS Group Ltd.

- Strong Point

- Toshiba Corporation

According to a new report published by Allied Market Research, titled, "Self Service Supermarket Sensor Market," The self service supermarket sensor market was valued at $3.4 billion in 2022, and is estimated to reach $10.7 billion by 2032, growing at a CAGR of 12.6% from 2023 to 2032.

Self service supermarket sensors are automated technologies that help customers self-order and check out without the aid of any staff members in the retail, supermarket, and hospitality industry. The earlier self-checkout systems were made up of separate, store-bought parts and needed a lot of storage space. On the contrary, new self-checkout systems are updated and created to meet consumer demand, match the layout of the business, and improve functionality, cost, form factors, and dependability. Kiosk vendors are already providing cashless solutions due to the rising demand for safe and self-payment technologies.

Self service supermarket sensor technology has transformed the modern retailing paradigm of hypermarkets. Consumers, particularly in urban and suburban regions, are enthusiastic about this novel approach. Customers are attracted to hypermarkets due to the extensive range of products and brands available, which fulfills their essential needs and household product requirements. The active participation of consumers in all aspects of the shopping experience distinguishes this modern retailing model. However, technological advancements and an increasing emphasis on modern lives have accelerated the emergence of self-service hypermarkets.

To fulfill the demands of tech-savvy customers, traditional cashiering operations in hypermarkets are being revolutionized through the incorporation of automatic self-checkout stations. These stations feature cutting-edge self service supermarket sensor technology. Customers can independently scan and process their goods by utilizing these sensors, expediting the checkout process, and lowering dependency on human cashiers. This totally self-service design provides a seamless and efficient shopping experience that aligns with modern consumer desires.

However, certain challenges such as data leaks, device malfunctions, phishing attempts, software, and network flaws are expected to hamper the adoption of self service supermarket sensors. For example, there is a high danger of cyber threats in which data can be hacked through unsafe and insecure networks. Data hackers can quickly breach and access crucial data and information, such as the financial credentials of consumer company accounts. This might result in significant financial loss as well as reputational damage. This is one of the major factors projected to hamper the market revenue growth during the forecast period.

Artificial intelligence is changing the retail shopping experience, allowing customers to pick up what they want and walk out the door without having to scan products or wait in a queue to pay. With the use of AI, machine vision, and deep learning, an increasing number of merchants are using autonomous shopping technology. During the COVID-19 pandemic, smart self-checkout solutions, such as AI-powered smart checkout systems and shopping carts, incorporate product recognition to give consumers contactless and automated checkout services. . Customers get a better shopping experience, and business owners save money on personnel overhead. The Al-powered smart checkout systems and shopping carts incorporate AI smart cameras, sensors, an edge AI system, and AI learning technology to speed up checkout services and eliminate human errors, allowing customers to enjoy quick checkout by completing purchases with speed, convenience, and simplicity. The smart camera takes a picture of the purchased item and displays it on the touchscreen. When the consumer authorizes the purchase, the screen displays payment information such as the number of things to be purchased and the total amount to be paid.

The COVID-19 pandemic has had significant impact on the self service supermarket sensor market. The need for self-service checkout supermarkets has rapidly expanded with the acceptance of remote work and virtual collaboration. The COVID-19 pandemic has also caused issues in the self service supermarket sensor industry. Consumer footfall at retail outlets, notably supermarkets, fell as a result of the fear and uncertainty about the virus. This decrease in consumer traffic influenced the adoption and use of self-service technologies. The pandemic also prompted the deployment of additional hygiene and sanitization methods. To maintain a safe shopping environment, supermarkets were required to ensure that self service supermarket sensors are cleaned and disinfected on a regular basis. These additional restrictions led to an increase in the operational challenges and costs for merchants.

The key players profiled in this report include: Nudge Rewards Inc., GuideSpark, Beekeeper AG, Sociabble, Inc., SocialChorus. Inc., Poppulo, OurPeople, Smarp, theemployeeapp, and Workvivo Limited. The market players are continuously striving to achieve a strong position in this competitive market using strategies such as collaborations and acquisitions.

Key Benefits For Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the self service supermarket sensor market analysis from 2022 to 2032 to identify the prevailing self service supermarket sensor market opportunities.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the self service supermarket sensor market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global self service supermarket sensor market trends, key players, market segments, application areas, and market growth strategies.

Key Market Segments

By Component

- Systems

- Services

By Type

- Cash Based System

- Cashless Based Systems

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Spain

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- LAMEA

- Brazil

- Saudi Arabia

- UAE

- South Africa

- Rest of LAMEA

Key Market Players:

- Diebold Nixdorf, Incorporated.

- ECR Software Corporation

- Fujitsu Limited

- Gilbarco Inc.

- ITAB Group

- NCR Corporation

- Pan-Oston

- PCMS Group Ltd.

- Strong Point

- Toshiba Corporation.

TABLE OF CONTENTS

CHAPTER 1: INTRODUCTION

- 1.1. Report description

- 1.2. Key market segments

- 1.3. Key benefits to the stakeholders

- 1.4. Research Methodology

- 1.4.1. Primary research

- 1.4.2. Secondary research

- 1.4.3. Analyst tools and models

CHAPTER 2: EXECUTIVE SUMMARY

- 2.1. CXO Perspective

CHAPTER 3: MARKET OVERVIEW

- 3.1. Market definition and scope

- 3.2. Key findings

- 3.2.1. Top impacting factors

- 3.2.2. Top investment pockets

- 3.3. Porter's five forces analysis

- 3.4. Market dynamics

- 3.4.1. Drivers

- 3.4.2. Restraints

- 3.4.3. Opportunities

- 3.5. COVID-19 Impact Analysis on the market

- 3.6. Average Selling Price

- 3.7. Brand Share Analysis

- 3.8. Key Regulation Analysis

- 3.9. Market Share Analysis

- 3.10. Patent Landscape

- 3.11. Regulatory Guidelines

- 3.12. Value Chain Analysis

CHAPTER 4: SELF SERVICE SUPERMARKET SENSOR MARKET, BY COMPONENT

- 4.1. Overview

- 4.1.1. Market size and forecast

- 4.2. Systems

- 4.2.1. Key market trends, growth factors and opportunities

- 4.2.2. Market size and forecast, by region

- 4.2.3. Market share analysis by country

- 4.3. Services

- 4.3.1. Key market trends, growth factors and opportunities

- 4.3.2. Market size and forecast, by region

- 4.3.3. Market share analysis by country

CHAPTER 5: SELF SERVICE SUPERMARKET SENSOR MARKET, BY TYPE

- 5.1. Overview

- 5.1.1. Market size and forecast

- 5.2. Cash Based System

- 5.2.1. Key market trends, growth factors and opportunities

- 5.2.2. Market size and forecast, by region

- 5.2.3. Market share analysis by country

- 5.3. Cashless Based Systems

- 5.3.1. Key market trends, growth factors and opportunities

- 5.3.2. Market size and forecast, by region

- 5.3.3. Market share analysis by country

CHAPTER 6: SELF SERVICE SUPERMARKET SENSOR MARKET, BY REGION

- 6.1. Overview

- 6.1.1. Market size and forecast By Region

- 6.2. North America

- 6.2.1. Key trends and opportunities

- 6.2.2. Market size and forecast, by Component

- 6.2.3. Market size and forecast, by Type

- 6.2.4. Market size and forecast, by country

- 6.2.4.1. U.S.

- 6.2.4.1.1. Key market trends, growth factors and opportunities

- 6.2.4.1.2. Market size and forecast, by Component

- 6.2.4.1.3. Market size and forecast, by Type

- 6.2.4.2. Canada

- 6.2.4.2.1. Key market trends, growth factors and opportunities

- 6.2.4.2.2. Market size and forecast, by Component

- 6.2.4.2.3. Market size and forecast, by Type

- 6.2.4.3. Mexico

- 6.2.4.3.1. Key market trends, growth factors and opportunities

- 6.2.4.3.2. Market size and forecast, by Component

- 6.2.4.3.3. Market size and forecast, by Type

- 6.3. Europe

- 6.3.1. Key trends and opportunities

- 6.3.2. Market size and forecast, by Component

- 6.3.3. Market size and forecast, by Type

- 6.3.4. Market size and forecast, by country

- 6.3.4.1. Germany

- 6.3.4.1.1. Key market trends, growth factors and opportunities

- 6.3.4.1.2. Market size and forecast, by Component

- 6.3.4.1.3. Market size and forecast, by Type

- 6.3.4.2. UK

- 6.3.4.2.1. Key market trends, growth factors and opportunities

- 6.3.4.2.2. Market size and forecast, by Component

- 6.3.4.2.3. Market size and forecast, by Type

- 6.3.4.3. France

- 6.3.4.3.1. Key market trends, growth factors and opportunities

- 6.3.4.3.2. Market size and forecast, by Component

- 6.3.4.3.3. Market size and forecast, by Type

- 6.3.4.4. Spain

- 6.3.4.4.1. Key market trends, growth factors and opportunities

- 6.3.4.4.2. Market size and forecast, by Component

- 6.3.4.4.3. Market size and forecast, by Type

- 6.3.4.5. Italy

- 6.3.4.5.1. Key market trends, growth factors and opportunities

- 6.3.4.5.2. Market size and forecast, by Component

- 6.3.4.5.3. Market size and forecast, by Type

- 6.3.4.6. Rest of Europe

- 6.3.4.6.1. Key market trends, growth factors and opportunities

- 6.3.4.6.2. Market size and forecast, by Component

- 6.3.4.6.3. Market size and forecast, by Type

- 6.4. Asia-Pacific

- 6.4.1. Key trends and opportunities

- 6.4.2. Market size and forecast, by Component

- 6.4.3. Market size and forecast, by Type

- 6.4.4. Market size and forecast, by country

- 6.4.4.1. China

- 6.4.4.1.1. Key market trends, growth factors and opportunities

- 6.4.4.1.2. Market size and forecast, by Component

- 6.4.4.1.3. Market size and forecast, by Type

- 6.4.4.2. Japan

- 6.4.4.2.1. Key market trends, growth factors and opportunities

- 6.4.4.2.2. Market size and forecast, by Component

- 6.4.4.2.3. Market size and forecast, by Type

- 6.4.4.3. India

- 6.4.4.3.1. Key market trends, growth factors and opportunities

- 6.4.4.3.2. Market size and forecast, by Component

- 6.4.4.3.3. Market size and forecast, by Type

- 6.4.4.4. South Korea

- 6.4.4.4.1. Key market trends, growth factors and opportunities

- 6.4.4.4.2. Market size and forecast, by Component

- 6.4.4.4.3. Market size and forecast, by Type

- 6.4.4.5. Australia

- 6.4.4.5.1. Key market trends, growth factors and opportunities

- 6.4.4.5.2. Market size and forecast, by Component

- 6.4.4.5.3. Market size and forecast, by Type

- 6.4.4.6. Rest of Asia-Pacific

- 6.4.4.6.1. Key market trends, growth factors and opportunities

- 6.4.4.6.2. Market size and forecast, by Component

- 6.4.4.6.3. Market size and forecast, by Type

- 6.5. LAMEA

- 6.5.1. Key trends and opportunities

- 6.5.2. Market size and forecast, by Component

- 6.5.3. Market size and forecast, by Type

- 6.5.4. Market size and forecast, by country

- 6.5.4.1. Brazil

- 6.5.4.1.1. Key market trends, growth factors and opportunities

- 6.5.4.1.2. Market size and forecast, by Component

- 6.5.4.1.3. Market size and forecast, by Type

- 6.5.4.2. Saudi Arabia

- 6.5.4.2.1. Key market trends, growth factors and opportunities

- 6.5.4.2.2. Market size and forecast, by Component

- 6.5.4.2.3. Market size and forecast, by Type

- 6.5.4.3. UAE

- 6.5.4.3.1. Key market trends, growth factors and opportunities

- 6.5.4.3.2. Market size and forecast, by Component

- 6.5.4.3.3. Market size and forecast, by Type

- 6.5.4.4. South Africa

- 6.5.4.4.1. Key market trends, growth factors and opportunities

- 6.5.4.4.2. Market size and forecast, by Component

- 6.5.4.4.3. Market size and forecast, by Type

- 6.5.4.5. Rest of LAMEA

- 6.5.4.5.1. Key market trends, growth factors and opportunities

- 6.5.4.5.2. Market size and forecast, by Component

- 6.5.4.5.3. Market size and forecast, by Type

CHAPTER 7: COMPETITIVE LANDSCAPE

- 7.1. Introduction

- 7.2. Top winning strategies

- 7.3. Product Mapping of Top 10 Player

- 7.4. Competitive Dashboard

- 7.5. Competitive Heatmap

- 7.6. Top player positioning, 2022

CHAPTER 8: COMPANY PROFILES

- 8.1. Diebold Nixdorf, Incorporated.

- 8.1.1. Company overview

- 8.1.2. Key Executives

- 8.1.3. Company snapshot

- 8.2. ECR Software Corporation

- 8.2.1. Company overview

- 8.2.2. Key Executives

- 8.2.3. Company snapshot

- 8.3. Fujitsu Limited

- 8.3.1. Company overview

- 8.3.2. Key Executives

- 8.3.3. Company snapshot

- 8.4. Gilbarco Inc.

- 8.4.1. Company overview

- 8.4.2. Key Executives

- 8.4.3. Company snapshot

- 8.5. ITAB Group

- 8.5.1. Company overview

- 8.5.2. Key Executives

- 8.5.3. Company snapshot

- 8.6. NCR Corporation

- 8.6.1. Company overview

- 8.6.2. Key Executives

- 8.6.3. Company snapshot

- 8.7. Pan-Oston

- 8.7.1. Company overview

- 8.7.2. Key Executives

- 8.7.3. Company snapshot

- 8.8. PCMS Group Ltd.

- 8.8.1. Company overview

- 8.8.2. Key Executives

- 8.8.3. Company snapshot

- 8.9. Strong Point

- 8.9.1. Company overview

- 8.9.2. Key Executives

- 8.9.3. Company snapshot

- 8.10. Toshiba Corporation.

- 8.10.1. Company overview

- 8.10.2. Key Executives

- 8.10.3. Company snapshot

LIST OF TABLES

- TABLE 01. GLOBAL SELF SERVICE SUPERMARKET SENSOR MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 02. SELF SERVICE SUPERMARKET SENSOR MARKET FOR SYSTEMS, BY REGION, 2022-2032 ($MILLION)

- TABLE 03. SELF SERVICE SUPERMARKET SENSOR MARKET FOR SERVICES, BY REGION, 2022-2032 ($MILLION)

- TABLE 04. GLOBAL SELF SERVICE SUPERMARKET SENSOR MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 05. SELF SERVICE SUPERMARKET SENSOR MARKET FOR CASH BASED SYSTEM, BY REGION, 2022-2032 ($MILLION)

- TABLE 06. SELF SERVICE SUPERMARKET SENSOR MARKET FOR CASHLESS BASED SYSTEMS, BY REGION, 2022-2032 ($MILLION)

- TABLE 07. SELF SERVICE SUPERMARKET SENSOR MARKET, BY REGION, 2022-2032 ($MILLION)

- TABLE 08. NORTH AMERICA SELF SERVICE SUPERMARKET SENSOR MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 09. NORTH AMERICA SELF SERVICE SUPERMARKET SENSOR MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 10. NORTH AMERICA SELF SERVICE SUPERMARKET SENSOR MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 11. U.S. SELF SERVICE SUPERMARKET SENSOR MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 12. U.S. SELF SERVICE SUPERMARKET SENSOR MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 13. CANADA SELF SERVICE SUPERMARKET SENSOR MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 14. CANADA SELF SERVICE SUPERMARKET SENSOR MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 15. MEXICO SELF SERVICE SUPERMARKET SENSOR MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 16. MEXICO SELF SERVICE SUPERMARKET SENSOR MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 17. EUROPE SELF SERVICE SUPERMARKET SENSOR MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 18. EUROPE SELF SERVICE SUPERMARKET SENSOR MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 19. EUROPE SELF SERVICE SUPERMARKET SENSOR MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 20. GERMANY SELF SERVICE SUPERMARKET SENSOR MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 21. GERMANY SELF SERVICE SUPERMARKET SENSOR MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 22. UK SELF SERVICE SUPERMARKET SENSOR MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 23. UK SELF SERVICE SUPERMARKET SENSOR MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 24. FRANCE SELF SERVICE SUPERMARKET SENSOR MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 25. FRANCE SELF SERVICE SUPERMARKET SENSOR MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 26. SPAIN SELF SERVICE SUPERMARKET SENSOR MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 27. SPAIN SELF SERVICE SUPERMARKET SENSOR MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 28. ITALY SELF SERVICE SUPERMARKET SENSOR MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 29. ITALY SELF SERVICE SUPERMARKET SENSOR MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 30. REST OF EUROPE SELF SERVICE SUPERMARKET SENSOR MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 31. REST OF EUROPE SELF SERVICE SUPERMARKET SENSOR MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 32. ASIA-PACIFIC SELF SERVICE SUPERMARKET SENSOR MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 33. ASIA-PACIFIC SELF SERVICE SUPERMARKET SENSOR MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 34. ASIA-PACIFIC SELF SERVICE SUPERMARKET SENSOR MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 35. CHINA SELF SERVICE SUPERMARKET SENSOR MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 36. CHINA SELF SERVICE SUPERMARKET SENSOR MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 37. JAPAN SELF SERVICE SUPERMARKET SENSOR MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 38. JAPAN SELF SERVICE SUPERMARKET SENSOR MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 39. INDIA SELF SERVICE SUPERMARKET SENSOR MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 40. INDIA SELF SERVICE SUPERMARKET SENSOR MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 41. SOUTH KOREA SELF SERVICE SUPERMARKET SENSOR MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 42. SOUTH KOREA SELF SERVICE SUPERMARKET SENSOR MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 43. AUSTRALIA SELF SERVICE SUPERMARKET SENSOR MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 44. AUSTRALIA SELF SERVICE SUPERMARKET SENSOR MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 45. REST OF ASIA-PACIFIC SELF SERVICE SUPERMARKET SENSOR MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 46. REST OF ASIA-PACIFIC SELF SERVICE SUPERMARKET SENSOR MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 47. LAMEA SELF SERVICE SUPERMARKET SENSOR MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 48. LAMEA SELF SERVICE SUPERMARKET SENSOR MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 49. LAMEA SELF SERVICE SUPERMARKET SENSOR MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 50. BRAZIL SELF SERVICE SUPERMARKET SENSOR MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 51. BRAZIL SELF SERVICE SUPERMARKET SENSOR MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 52. SAUDI ARABIA SELF SERVICE SUPERMARKET SENSOR MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 53. SAUDI ARABIA SELF SERVICE SUPERMARKET SENSOR MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 54. UAE SELF SERVICE SUPERMARKET SENSOR MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 55. UAE SELF SERVICE SUPERMARKET SENSOR MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 56. SOUTH AFRICA SELF SERVICE SUPERMARKET SENSOR MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 57. SOUTH AFRICA SELF SERVICE SUPERMARKET SENSOR MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 58. REST OF LAMEA SELF SERVICE SUPERMARKET SENSOR MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 59. REST OF LAMEA SELF SERVICE SUPERMARKET SENSOR MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 60. DIEBOLD NIXDORF, INCORPORATED.: KEY EXECUTIVES

- TABLE 61. DIEBOLD NIXDORF, INCORPORATED.: COMPANY SNAPSHOT

- TABLE 62. ECR SOFTWARE CORPORATION: KEY EXECUTIVES

- TABLE 63. ECR SOFTWARE CORPORATION: COMPANY SNAPSHOT

- TABLE 64. FUJITSU LIMITED: KEY EXECUTIVES

- TABLE 65. FUJITSU LIMITED: COMPANY SNAPSHOT

- TABLE 66. GILBARCO INC.: KEY EXECUTIVES

- TABLE 67. GILBARCO INC.: COMPANY SNAPSHOT

- TABLE 68. ITAB GROUP: KEY EXECUTIVES

- TABLE 69. ITAB GROUP: COMPANY SNAPSHOT

- TABLE 70. NCR CORPORATION: KEY EXECUTIVES

- TABLE 71. NCR CORPORATION: COMPANY SNAPSHOT

- TABLE 72. PAN-OSTON: KEY EXECUTIVES

- TABLE 73. PAN-OSTON: COMPANY SNAPSHOT

- TABLE 74. PCMS GROUP LTD.: KEY EXECUTIVES

- TABLE 75. PCMS GROUP LTD.: COMPANY SNAPSHOT

- TABLE 76. STRONG POINT: KEY EXECUTIVES

- TABLE 77. STRONG POINT: COMPANY SNAPSHOT

- TABLE 78. TOSHIBA CORPORATION.: KEY EXECUTIVES

- TABLE 79. TOSHIBA CORPORATION.: COMPANY SNAPSHOT

LIST OF FIGURES

- FIGURE 01. SELF SERVICE SUPERMARKET SENSOR MARKET, 2022-2032

- FIGURE 02. SEGMENTATION OF SELF SERVICE SUPERMARKET SENSOR MARKET, 2022-2032

- FIGURE 03. TOP INVESTMENT POCKETS IN SELF SERVICE SUPERMARKET SENSOR MARKET (2023-2032)

- FIGURE 04. PORTER FIVE-1

- FIGURE 05. PORTER FIVE-2

- FIGURE 06. PORTER FIVE-3

- FIGURE 07. PORTER FIVE-4

- FIGURE 08. PORTER FIVE-5

- FIGURE 09. DRIVERS, RESTRAINTS AND OPPORTUNITIES: GLOBALSELF SERVICE SUPERMARKET SENSOR MARKET

- FIGURE 10. IMPACT OF KEY REGULATION: SELF SERVICE SUPERMARKET SENSOR MARKET

- FIGURE 11. MARKET SHARE ANALYSIS: SELF SERVICE SUPERMARKET SENSOR MARKET

- FIGURE 12. PATENT ANALYSIS BY COMPANY

- FIGURE 13. PATENT ANALYSIS BY COUNTRY

- FIGURE 14. REGULATORY GUIDELINES: SELF SERVICE SUPERMARKET SENSOR MARKET

- FIGURE 15. VALUE CHAIN ANALYSIS: SELF SERVICE SUPERMARKET SENSOR MARKET

- FIGURE 16. SELF SERVICE SUPERMARKET SENSOR MARKET, BY COMPONENT, 2022(%)

- FIGURE 17. COMPARATIVE SHARE ANALYSIS OF SELF SERVICE SUPERMARKET SENSOR MARKET FOR SYSTEMS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 18. COMPARATIVE SHARE ANALYSIS OF SELF SERVICE SUPERMARKET SENSOR MARKET FOR SERVICES, BY COUNTRY 2022 AND 2032(%)

- FIGURE 19. SELF SERVICE SUPERMARKET SENSOR MARKET, BY TYPE, 2022(%)

- FIGURE 20. COMPARATIVE SHARE ANALYSIS OF SELF SERVICE SUPERMARKET SENSOR MARKET FOR CASH BASED SYSTEM, BY COUNTRY 2022 AND 2032(%)

- FIGURE 21. COMPARATIVE SHARE ANALYSIS OF SELF SERVICE SUPERMARKET SENSOR MARKET FOR CASHLESS BASED SYSTEMS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 22. SELF SERVICE SUPERMARKET SENSOR MARKET BY REGION, 2022

- FIGURE 23. U.S. SELF SERVICE SUPERMARKET SENSOR MARKET, 2022-2032 ($MILLION)

- FIGURE 24. CANADA SELF SERVICE SUPERMARKET SENSOR MARKET, 2022-2032 ($MILLION)

- FIGURE 25. MEXICO SELF SERVICE SUPERMARKET SENSOR MARKET, 2022-2032 ($MILLION)

- FIGURE 26. GERMANY SELF SERVICE SUPERMARKET SENSOR MARKET, 2022-2032 ($MILLION)

- FIGURE 27. UK SELF SERVICE SUPERMARKET SENSOR MARKET, 2022-2032 ($MILLION)

- FIGURE 28. FRANCE SELF SERVICE SUPERMARKET SENSOR MARKET, 2022-2032 ($MILLION)

- FIGURE 29. SPAIN SELF SERVICE SUPERMARKET SENSOR MARKET, 2022-2032 ($MILLION)

- FIGURE 30. ITALY SELF SERVICE SUPERMARKET SENSOR MARKET, 2022-2032 ($MILLION)

- FIGURE 31. REST OF EUROPE SELF SERVICE SUPERMARKET SENSOR MARKET, 2022-2032 ($MILLION)

- FIGURE 32. CHINA SELF SERVICE SUPERMARKET SENSOR MARKET, 2022-2032 ($MILLION)

- FIGURE 33. JAPAN SELF SERVICE SUPERMARKET SENSOR MARKET, 2022-2032 ($MILLION)

- FIGURE 34. INDIA SELF SERVICE SUPERMARKET SENSOR MARKET, 2022-2032 ($MILLION)

- FIGURE 35. SOUTH KOREA SELF SERVICE SUPERMARKET SENSOR MARKET, 2022-2032 ($MILLION)

- FIGURE 36. AUSTRALIA SELF SERVICE SUPERMARKET SENSOR MARKET, 2022-2032 ($MILLION)

- FIGURE 37. REST OF ASIA-PACIFIC SELF SERVICE SUPERMARKET SENSOR MARKET, 2022-2032 ($MILLION)

- FIGURE 38. BRAZIL SELF SERVICE SUPERMARKET SENSOR MARKET, 2022-2032 ($MILLION)

- FIGURE 39. SAUDI ARABIA SELF SERVICE SUPERMARKET SENSOR MARKET, 2022-2032 ($MILLION)

- FIGURE 40. UAE SELF SERVICE SUPERMARKET SENSOR MARKET, 2022-2032 ($MILLION)

- FIGURE 41. SOUTH AFRICA SELF SERVICE SUPERMARKET SENSOR MARKET, 2022-2032 ($MILLION)

- FIGURE 42. REST OF LAMEA SELF SERVICE SUPERMARKET SENSOR MARKET, 2022-2032 ($MILLION)

- FIGURE 43. TOP WINNING STRATEGIES, BY YEAR

- FIGURE 44. TOP WINNING STRATEGIES, BY DEVELOPMENT

- FIGURE 45. TOP WINNING STRATEGIES, BY COMPANY

- FIGURE 46. PRODUCT MAPPING OF TOP 10 PLAYERS

- FIGURE 47. COMPETITIVE DASHBOARD

- FIGURE 48. COMPETITIVE HEATMAP: SELF SERVICE SUPERMARKET SENSOR MARKET

- FIGURE 49. TOP PLAYER POSITIONING, 2022

2030 年自助服务技术市场预测:按产品类型、部署模式、介面、最终用户和地区进行的全球分析

2030 年自助服务技术市场预测:按产品类型、部署模式、介面、最终用户和地区进行的全球分析 2025 年自助服务技术市场报告自助服务市场规模、份额和成长分析(按类型、最终用户和地区)- 2025-2032 年产业预测自助超级市场市场规模、份额、成长分析,按技术、按产品、按应用、按最终用户、按地区 - 行业预测,2025 年至 2032 年

2025 年自助服务技术市场报告自助服务市场规模、份额和成长分析(按类型、最终用户和地区)- 2025-2032 年产业预测自助超级市场市场规模、份额、成长分析,按技术、按产品、按应用、按最终用户、按地区 - 行业预测,2025 年至 2032 年 自助服务:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)自助服务技术市场 - 全球产业规模、份额、趋势、机会和预测,按机器类型、应用、介面、地区和竞争细分,2019-2029F

自助服务:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)自助服务技术市场 - 全球产业规模、份额、趋势、机会和预测,按机器类型、应用、介面、地区和竞争细分,2019-2029F 自助服务技术的全球市场

自助服务技术的全球市场 自助服务应用程式市场,按产品类型、按组件、按部署、按应用程式、按国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测

自助服务应用程式市场,按产品类型、按组件、按部署、按应用程式、按国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测 自助服务技术的全球市场 2024-2028

自助服务技术的全球市场 2024-2028