|

市场调查报告书

商品编码

1365588

教育市场中的人工智慧:按组成部分、部署模式、技术、用途和最终用户:2023-2032 年全球机会分析和产业预测Artificial Intelligence in Education Market By Component, By Deployment Mode, By Technology, By Application, By End User : Global Opportunity Analysis and Industry Forecast, 2023-2032 |

||||||

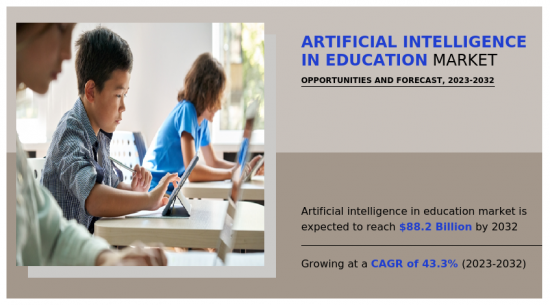

根据联合市场研究公司发布的新报告《教育领域的人工智慧市场》,预计2022年教育领域的人工智慧市场价值将达到25亿美元,2032年将达到882亿美元,并在2023年至2032年期间扩大。年复合成长率为 43.3%。

目录

第1章简介

第2章执行摘要

第3章市场概况

- 市场定义和范围

- 主要发现

- 影响要素

- 主要投资机会

- 波特五力分析

- 市场动态

- 促进因素

- 个体化教育和适应性学习

- 虚拟助理与智慧辅导

- 提高管理效率

- 抑制因素

- 隐私和道德问题

- 准入问题和公平问题

- 机会

- 提高学生的积极性和积极性

- 资料主导决策

- 促进因素

- COVID-19 市场影响分析

第4章教育领域的人工智慧市场:按组成部分

- 概述

- 解决方案

- 服务

第5章教育人工智慧市场:依部署模式

- 概述

- 本地

- 云

第6章教育领域的人工智慧市场:依技术划分

- 概述

- 机器学习和深度学习

- 自然语言处理(NLP)

第7章教育领域的人工智慧市场:依用途

- 概述

- 学习平台与虚拟辅导员

- 智慧内容交付

- 诈欺和风险管理

- 智慧辅导系统(ITS)

- 其他的

第8章教育领域的人工智慧市场:按最终用户划分

- 概述

- 高等教育

- K-12教育

- 企业培训与学习

- 其他的

第9章教育人工智慧市场:按地区

- 概述

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 其他的

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 其他的

- 拉丁美洲

- 拉丁美洲

- 中东

- 非洲

第10章竞争形势

- 介绍

- 关键成功策略

- 10家主要企业产品图谱

- 竞争仪表板

- 竞争热图

- 2022年主要企业定位

第11章公司简介

- Microsoft Corporation

- International Business Machines Corporation

- Amazon Web Services, Inc.

- Google LLC

- Cognizant

- DreamBox Learning, Inc.

- BridgeU

- Carnegie Learning, Inc.

- Pearson PLC

- Nuance Communications, Inc.

According to a new report published by Allied Market Research, titled, "Artificial Intelligence in Education Market," The artificial intelligence in education market was valued at $2.5 billion in 2022, and is estimated to reach $88.2 billion by 2032, growing at a CAGR of 43.3% from 2023 to 2032.

In addition, software used in education and training is enhanced with the use of technologies such as deep learning, machine learning, and natural language processing (NLP). All technological advancements are made in accordance with educational models such as the learner model, pedagogical model, and domain model in order to enhance educational systems and enable better knowledge delivery and assessment.

Moreover, the demand for artificial intelligence (AI) in education is being driven by factors such as rising investments in AI and EdTech by the public and private sectors, as well as rising edutainment penetration. Moreover, the demand for AI in education globally is also being fueled by technological innovation. Industries all across the world were severely affected by the COVID-19 pandemic. But during the epidemic, the market saw a marked increase in demand for creative AI-based teaching solutions.

Furthermore, personalized education and adaptive learning, virtual assistants and smart tutoring and improvements in administrative efficiency are primarily driving the growth of artificial intelligence in education market. However, privacy and ethical issues and access issues and equity concerns hamper the market growth to some extent. Moreover, enhanced motivation and engagement of students and data-driven decision making are expected to provide lucrative opportunities for market growth during the forecast period.

On the basis of component, solution segment dominated the AI in education market in 2022, and is expected to maintain its dominance in the upcoming years owing to rising usage and development of artificial intelligence technologies in the educational sector propels the market growth significantly. However, service segment is expected segment is expected to witness highest growth, owing to gain knowledge about learning patterns, instructional efficacy, and student outcomes, these platforms gather and analyze enormous volumes of educational data, including student performance, engagement, and behavior.

Artificial intelligence in education market is segmented into component, deployment, technology, application, end user, and region. On the basis of component, it is segregated into solutions and services. On the basis of deployment, it is segregated into on-premise and cloud. On the basis of technology, it is segregated into machine learning and deep learning and natural language. On the basis of application, it is segregated into learning platform & virtual facilitators, smart content delivery, fraud and risk management, intelligent tutoring system (ITS) and others. On the basis of end user, it is segregated into corporate learning, K-12 education, higher education and others. On the basis of region, it is analyzed across North America, Europe, Asia-Pacific, and LAMEA.

On the basis of region, North America region dominated the AI in education market in 2022, and is expected to maintain its dominance in the upcoming years, owing to to the increasing technical developments that are entirely revolutionizing the landscape of the IT industry and, in turn, encouraging the drive for the implementation of efficient servers and networking solutions. However, Asia Pacific region is expected segment is expected to witness highest growth, owing to increase the efficacy and quality of education offered by artificial intelligence in education industry has increased due to the sizeable population and growing emphasis on education in Asia-Pacific.

Key Benefits For Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the artificial intelligence in education market analysis from 2022 to 2032 to identify the prevailing artificial intelligence in education market opportunities.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the artificial intelligence in education market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global artificial intelligence in education market trends, key players, market segments, application areas, and market growth strategies.

Additional benefits you will get with this purchase are:

- Quarterly Update and* (only available with a corporate license, on listed price)

- 5 additional Company Profile of client Choice pre- or Post-purchase, as a free update.

- Free Upcoming Version on the Purchase of Five and Enterprise User License.

- 16 analyst hours of support* (post-purchase, if you find additional data requirements upon review of the report, you may receive support amounting to 16 analyst hours to solve questions, and post-sale queries)

- 15% Free Customization* (in case the scope or segment of the report does not match your requirements, 20% is equivalent to 3 working days of free work, applicable once)

- Free data Pack on the Five and Enterprise User License. (Excel version of the report)

- Free Updated report if the report is 6-12 months old or older.

- 24-hour priority response*

- Free Industry updates and white papers.

Possible Customization with this report (with additional cost and timeline talk to the sales executive to know more)

- Senario Analysis & Growth Trend Comparision

- Market share analysis of players by products/segments

- Regulatory Guidelines

- Additional company profiles with specific to client's interest

- Additional country or region analysis- market size and forecast

- Expanded list for Company Profiles

- Key player details (including location, contact details, supplier/vendor network etc. in excel format)

- SWOT Analysis

Key Market Segments

By Application

- Learning Platform and Virtual Facilitators

- Smart Content Delivery

- Fraud and Risk Management

- Intelligent Tutoring System (ITS)

- Others

By End User

- Higher Education

- K-12 Education

- Corporate Training and Learning

- Others

By Component

- Solution

- Services

By Deployment Mode

- On-premise

- Cloud

By Technology

- Machine Learning and Deep Learning

- Natural Language Processing (NLP)

By Region

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- LAMEA

- Latin America

- Middle East

- Africa

Key Market Players:

- Amazon Web Services, Inc.

- BridgeU

- Carnegie Learning, Inc.

- Cognizant

- DreamBox Learning, Inc.

- Google LLC

- International Business Machines Corporation

- Microsoft Corporation

- Nuance Communications, Inc.

- Pearson PLC

TABLE OF CONTENTS

CHAPTER 1: INTRODUCTION

- 1.1. Report description

- 1.2. Key market segments

- 1.3. Key benefits to the stakeholders

- 1.4. Research Methodology

- 1.4.1. Primary research

- 1.4.2. Secondary research

- 1.4.3. Analyst tools and models

CHAPTER 2: EXECUTIVE SUMMARY

- 2.1. CXO Perspective

CHAPTER 3: MARKET OVERVIEW

- 3.1. Market definition and scope

- 3.2. Key findings

- 3.2.1. Top impacting factors

- 3.2.2. Top investment pockets

- 3.3. Porter's five forces analysis

- 3.3.1. Low bargaining power of suppliers

- 3.3.2. Low threat of new entrants

- 3.3.3. Low threat of substitutes

- 3.3.4. Low intensity of rivalry

- 3.3.5. Low bargaining power of buyers

- 3.4. Market dynamics

- 3.4.1. Drivers

- 3.4.1.1. Personalized Education and Adaptive Learning

- 3.4.1.2. Virtual assistants and smart tutoring

- 3.4.1.3. Improvements in Administrative Efficiency

- 3.4.1. Drivers

- 3.4.2. Restraints

- 3.4.2.1. Privacy and Ethical Issues

- 3.4.2.2. Access Issues and Equity Concerns

- 3.4.3. Opportunities

- 3.4.3.1. Enhanced motivation and engagement of students

- 3.4.3.2. Data-Driven Decision Making

- 3.5. COVID-19 Impact Analysis on the market

CHAPTER 4: ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT

- 4.1. Overview

- 4.1.1. Market size and forecast

- 4.2. Solution

- 4.2.1. Key market trends, growth factors and opportunities

- 4.2.2. Market size and forecast, by region

- 4.2.3. Market share analysis by country

- 4.3. Services

- 4.3.1. Key market trends, growth factors and opportunities

- 4.3.2. Market size and forecast, by region

- 4.3.3. Market share analysis by country

CHAPTER 5: ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE

- 5.1. Overview

- 5.1.1. Market size and forecast

- 5.2. On-premise

- 5.2.1. Key market trends, growth factors and opportunities

- 5.2.2. Market size and forecast, by region

- 5.2.3. Market share analysis by country

- 5.3. Cloud

- 5.3.1. Key market trends, growth factors and opportunities

- 5.3.2. Market size and forecast, by region

- 5.3.3. Market share analysis by country

CHAPTER 6: ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY

- 6.1. Overview

- 6.1.1. Market size and forecast

- 6.2. Machine Learning and Deep Learning

- 6.2.1. Key market trends, growth factors and opportunities

- 6.2.2. Market size and forecast, by region

- 6.2.3. Market share analysis by country

- 6.3. Natural Language Processing (NLP)

- 6.3.1. Key market trends, growth factors and opportunities

- 6.3.2. Market size and forecast, by region

- 6.3.3. Market share analysis by country

CHAPTER 7: ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION

- 7.1. Overview

- 7.1.1. Market size and forecast

- 7.2. Learning Platform and Virtual Facilitators

- 7.2.1. Key market trends, growth factors and opportunities

- 7.2.2. Market size and forecast, by region

- 7.2.3. Market share analysis by country

- 7.3. Smart Content Delivery

- 7.3.1. Key market trends, growth factors and opportunities

- 7.3.2. Market size and forecast, by region

- 7.3.3. Market share analysis by country

- 7.4. Fraud and Risk Management

- 7.4.1. Key market trends, growth factors and opportunities

- 7.4.2. Market size and forecast, by region

- 7.4.3. Market share analysis by country

- 7.5. Intelligent Tutoring System (ITS)

- 7.5.1. Key market trends, growth factors and opportunities

- 7.5.2. Market size and forecast, by region

- 7.5.3. Market share analysis by country

- 7.6. Others

- 7.6.1. Key market trends, growth factors and opportunities

- 7.6.2. Market size and forecast, by region

- 7.6.3. Market share analysis by country

CHAPTER 8: ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER

- 8.1. Overview

- 8.1.1. Market size and forecast

- 8.2. Higher Education

- 8.2.1. Key market trends, growth factors and opportunities

- 8.2.2. Market size and forecast, by region

- 8.2.3. Market share analysis by country

- 8.3. K-12 Education

- 8.3.1. Key market trends, growth factors and opportunities

- 8.3.2. Market size and forecast, by region

- 8.3.3. Market share analysis by country

- 8.4. Corporate Training and Learning

- 8.4.1. Key market trends, growth factors and opportunities

- 8.4.2. Market size and forecast, by region

- 8.4.3. Market share analysis by country

- 8.5. Others

- 8.5.1. Key market trends, growth factors and opportunities

- 8.5.2. Market size and forecast, by region

- 8.5.3. Market share analysis by country

CHAPTER 9: ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY REGION

- 9.1. Overview

- 9.1.1. Market size and forecast By Region

- 9.2. North America

- 9.2.1. Key trends and opportunities

- 9.2.2. Market size and forecast, by Component

- 9.2.3. Market size and forecast, by Deployment Mode

- 9.2.4. Market size and forecast, by Technology

- 9.2.5. Market size and forecast, by Application

- 9.2.6. Market size and forecast, by End User

- 9.2.7. Market size and forecast, by country

- 9.2.7.1. U.S.

- 9.2.7.1.1. Key market trends, growth factors and opportunities

- 9.2.7.1.2. Market size and forecast, by Component

- 9.2.7.1.3. Market size and forecast, by Deployment Mode

- 9.2.7.1.4. Market size and forecast, by Technology

- 9.2.7.1.5. Market size and forecast, by Application

- 9.2.7.1.6. Market size and forecast, by End User

- 9.2.7.2. Canada

- 9.2.7.2.1. Key market trends, growth factors and opportunities

- 9.2.7.2.2. Market size and forecast, by Component

- 9.2.7.2.3. Market size and forecast, by Deployment Mode

- 9.2.7.2.4. Market size and forecast, by Technology

- 9.2.7.2.5. Market size and forecast, by Application

- 9.2.7.2.6. Market size and forecast, by End User

- 9.3. Europe

- 9.3.1. Key trends and opportunities

- 9.3.2. Market size and forecast, by Component

- 9.3.3. Market size and forecast, by Deployment Mode

- 9.3.4. Market size and forecast, by Technology

- 9.3.5. Market size and forecast, by Application

- 9.3.6. Market size and forecast, by End User

- 9.3.7. Market size and forecast, by country

- 9.3.7.1. UK

- 9.3.7.1.1. Key market trends, growth factors and opportunities

- 9.3.7.1.2. Market size and forecast, by Component

- 9.3.7.1.3. Market size and forecast, by Deployment Mode

- 9.3.7.1.4. Market size and forecast, by Technology

- 9.3.7.1.5. Market size and forecast, by Application

- 9.3.7.1.6. Market size and forecast, by End User

- 9.3.7.2. Germany

- 9.3.7.2.1. Key market trends, growth factors and opportunities

- 9.3.7.2.2. Market size and forecast, by Component

- 9.3.7.2.3. Market size and forecast, by Deployment Mode

- 9.3.7.2.4. Market size and forecast, by Technology

- 9.3.7.2.5. Market size and forecast, by Application

- 9.3.7.2.6. Market size and forecast, by End User

- 9.3.7.3. France

- 9.3.7.3.1. Key market trends, growth factors and opportunities

- 9.3.7.3.2. Market size and forecast, by Component

- 9.3.7.3.3. Market size and forecast, by Deployment Mode

- 9.3.7.3.4. Market size and forecast, by Technology

- 9.3.7.3.5. Market size and forecast, by Application

- 9.3.7.3.6. Market size and forecast, by End User

- 9.3.7.4. Italy

- 9.3.7.4.1. Key market trends, growth factors and opportunities

- 9.3.7.4.2. Market size and forecast, by Component

- 9.3.7.4.3. Market size and forecast, by Deployment Mode

- 9.3.7.4.4. Market size and forecast, by Technology

- 9.3.7.4.5. Market size and forecast, by Application

- 9.3.7.4.6. Market size and forecast, by End User

- 9.3.7.5. Spain

- 9.3.7.5.1. Key market trends, growth factors and opportunities

- 9.3.7.5.2. Market size and forecast, by Component

- 9.3.7.5.3. Market size and forecast, by Deployment Mode

- 9.3.7.5.4. Market size and forecast, by Technology

- 9.3.7.5.5. Market size and forecast, by Application

- 9.3.7.5.6. Market size and forecast, by End User

- 9.3.7.6. Rest of Europe

- 9.3.7.6.1. Key market trends, growth factors and opportunities

- 9.3.7.6.2. Market size and forecast, by Component

- 9.3.7.6.3. Market size and forecast, by Deployment Mode

- 9.3.7.6.4. Market size and forecast, by Technology

- 9.3.7.6.5. Market size and forecast, by Application

- 9.3.7.6.6. Market size and forecast, by End User

- 9.4. Asia-Pacific

- 9.4.1. Key trends and opportunities

- 9.4.2. Market size and forecast, by Component

- 9.4.3. Market size and forecast, by Deployment Mode

- 9.4.4. Market size and forecast, by Technology

- 9.4.5. Market size and forecast, by Application

- 9.4.6. Market size and forecast, by End User

- 9.4.7. Market size and forecast, by country

- 9.4.7.1. China

- 9.4.7.1.1. Key market trends, growth factors and opportunities

- 9.4.7.1.2. Market size and forecast, by Component

- 9.4.7.1.3. Market size and forecast, by Deployment Mode

- 9.4.7.1.4. Market size and forecast, by Technology

- 9.4.7.1.5. Market size and forecast, by Application

- 9.4.7.1.6. Market size and forecast, by End User

- 9.4.7.2. Japan

- 9.4.7.2.1. Key market trends, growth factors and opportunities

- 9.4.7.2.2. Market size and forecast, by Component

- 9.4.7.2.3. Market size and forecast, by Deployment Mode

- 9.4.7.2.4. Market size and forecast, by Technology

- 9.4.7.2.5. Market size and forecast, by Application

- 9.4.7.2.6. Market size and forecast, by End User

- 9.4.7.3. India

- 9.4.7.3.1. Key market trends, growth factors and opportunities

- 9.4.7.3.2. Market size and forecast, by Component

- 9.4.7.3.3. Market size and forecast, by Deployment Mode

- 9.4.7.3.4. Market size and forecast, by Technology

- 9.4.7.3.5. Market size and forecast, by Application

- 9.4.7.3.6. Market size and forecast, by End User

- 9.4.7.4. Australia

- 9.4.7.4.1. Key market trends, growth factors and opportunities

- 9.4.7.4.2. Market size and forecast, by Component

- 9.4.7.4.3. Market size and forecast, by Deployment Mode

- 9.4.7.4.4. Market size and forecast, by Technology

- 9.4.7.4.5. Market size and forecast, by Application

- 9.4.7.4.6. Market size and forecast, by End User

- 9.4.7.5. South Korea

- 9.4.7.5.1. Key market trends, growth factors and opportunities

- 9.4.7.5.2. Market size and forecast, by Component

- 9.4.7.5.3. Market size and forecast, by Deployment Mode

- 9.4.7.5.4. Market size and forecast, by Technology

- 9.4.7.5.5. Market size and forecast, by Application

- 9.4.7.5.6. Market size and forecast, by End User

- 9.4.7.6. Rest of Asia-Pacific

- 9.4.7.6.1. Key market trends, growth factors and opportunities

- 9.4.7.6.2. Market size and forecast, by Component

- 9.4.7.6.3. Market size and forecast, by Deployment Mode

- 9.4.7.6.4. Market size and forecast, by Technology

- 9.4.7.6.5. Market size and forecast, by Application

- 9.4.7.6.6. Market size and forecast, by End User

- 9.5. LAMEA

- 9.5.1. Key trends and opportunities

- 9.5.2. Market size and forecast, by Component

- 9.5.3. Market size and forecast, by Deployment Mode

- 9.5.4. Market size and forecast, by Technology

- 9.5.5. Market size and forecast, by Application

- 9.5.6. Market size and forecast, by End User

- 9.5.7. Market size and forecast, by country

- 9.5.7.1. Latin America

- 9.5.7.1.1. Key market trends, growth factors and opportunities

- 9.5.7.1.2. Market size and forecast, by Component

- 9.5.7.1.3. Market size and forecast, by Deployment Mode

- 9.5.7.1.4. Market size and forecast, by Technology

- 9.5.7.1.5. Market size and forecast, by Application

- 9.5.7.1.6. Market size and forecast, by End User

- 9.5.7.2. Middle East

- 9.5.7.2.1. Key market trends, growth factors and opportunities

- 9.5.7.2.2. Market size and forecast, by Component

- 9.5.7.2.3. Market size and forecast, by Deployment Mode

- 9.5.7.2.4. Market size and forecast, by Technology

- 9.5.7.2.5. Market size and forecast, by Application

- 9.5.7.2.6. Market size and forecast, by End User

- 9.5.7.3. Africa

- 9.5.7.3.1. Key market trends, growth factors and opportunities

- 9.5.7.3.2. Market size and forecast, by Component

- 9.5.7.3.3. Market size and forecast, by Deployment Mode

- 9.5.7.3.4. Market size and forecast, by Technology

- 9.5.7.3.5. Market size and forecast, by Application

- 9.5.7.3.6. Market size and forecast, by End User

CHAPTER 10: COMPETITIVE LANDSCAPE

- 10.1. Introduction

- 10.2. Top winning strategies

- 10.3. Product Mapping of Top 10 Player

- 10.4. Competitive Dashboard

- 10.5. Competitive Heatmap

- 10.6. Top player positioning, 2022

CHAPTER 11: COMPANY PROFILES

- 11.1. Microsoft Corporation

- 11.1.1. Company overview

- 11.1.2. Key Executives

- 11.1.3. Company snapshot

- 11.1.4. Operating business segments

- 11.1.5. Product portfolio

- 11.1.6. Business performance

- 11.1.7. Key strategic moves and developments

- 11.2. International Business Machines Corporation

- 11.2.1. Company overview

- 11.2.2. Key Executives

- 11.2.3. Company snapshot

- 11.2.4. Operating business segments

- 11.2.5. Product portfolio

- 11.2.6. Business performance

- 11.2.7. Key strategic moves and developments

- 11.3. Amazon Web Services, Inc.

- 11.3.1. Company overview

- 11.3.2. Key Executives

- 11.3.3. Company snapshot

- 11.3.4. Operating business segments

- 11.3.5. Product portfolio

- 11.3.6. Business performance

- 11.3.7. Key strategic moves and developments

- 11.4. Google LLC

- 11.4.1. Company overview

- 11.4.2. Key Executives

- 11.4.3. Company snapshot

- 11.4.4. Operating business segments

- 11.4.5. Product portfolio

- 11.4.6. Business performance

- 11.4.7. Key strategic moves and developments

- 11.5. Cognizant

- 11.5.1. Company overview

- 11.5.2. Key Executives

- 11.5.3. Company snapshot

- 11.5.4. Operating business segments

- 11.5.5. Product portfolio

- 11.5.6. Business performance

- 11.5.7. Key strategic moves and developments

- 11.6. DreamBox Learning, Inc.

- 11.6.1. Company overview

- 11.6.2. Key Executives

- 11.6.3. Company snapshot

- 11.6.4. Operating business segments

- 11.6.5. Product portfolio

- 11.7. BridgeU

- 11.7.1. Company overview

- 11.7.2. Key Executives

- 11.7.3. Company snapshot

- 11.7.4. Operating business segments

- 11.7.5. Product portfolio

- 11.7.6. Key strategic moves and developments

- 11.8. Carnegie Learning, Inc.

- 11.8.1. Company overview

- 11.8.2. Key Executives

- 11.8.3. Company snapshot

- 11.8.4. Operating business segments

- 11.8.5. Product portfolio

- 11.8.6. Key strategic moves and developments

- 11.9. Pearson PLC

- 11.9.1. Company overview

- 11.9.2. Key Executives

- 11.9.3. Company snapshot

- 11.9.4. Operating business segments

- 11.9.5. Product portfolio

- 11.9.6. Business performance

- 11.9.7. Key strategic moves and developments

- 11.10. Nuance Communications, Inc.

- 11.10.1. Company overview

- 11.10.2. Key Executives

- 11.10.3. Company snapshot

- 11.10.4. Operating business segments

- 11.10.5. Product portfolio

- 11.10.6. Business performance

- 11.10.7. Key strategic moves and developments

LIST OF TABLES

- TABLE 01. GLOBAL ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 02. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR SOLUTION, BY REGION, 2022-2032 ($MILLION)

- TABLE 03. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR SERVICES, BY REGION, 2022-2032 ($MILLION)

- TABLE 04. GLOBAL ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

- TABLE 05. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR ON-PREMISE, BY REGION, 2022-2032 ($MILLION)

- TABLE 06. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR CLOUD, BY REGION, 2022-2032 ($MILLION)

- TABLE 07. GLOBAL ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 08. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR MACHINE LEARNING AND DEEP LEARNING, BY REGION, 2022-2032 ($MILLION)

- TABLE 09. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR NATURAL LANGUAGE PROCESSING (NLP), BY REGION, 2022-2032 ($MILLION)

- TABLE 10. GLOBAL ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 11. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR LEARNING PLATFORM AND VIRTUAL FACILITATORS , BY REGION, 2022-2032 ($MILLION)

- TABLE 12. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR SMART CONTENT DELIVERY, BY REGION, 2022-2032 ($MILLION)

- TABLE 13. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR FRAUD AND RISK MANAGEMENT, BY REGION, 2022-2032 ($MILLION)

- TABLE 14. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR INTELLIGENT TUTORING SYSTEM (ITS), BY REGION, 2022-2032 ($MILLION)

- TABLE 15. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR OTHERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 16. GLOBAL ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 17. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR HIGHER EDUCATION, BY REGION, 2022-2032 ($MILLION)

- TABLE 18. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR K-12 EDUCATION, BY REGION, 2022-2032 ($MILLION)

- TABLE 19. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR CORPORATE TRAINING AND LEARNING, BY REGION, 2022-2032 ($MILLION)

- TABLE 20. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR OTHERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 21. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY REGION, 2022-2032 ($MILLION)

- TABLE 22. NORTH AMERICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 23. NORTH AMERICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

- TABLE 24. NORTH AMERICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 25. NORTH AMERICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 26. NORTH AMERICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 27. NORTH AMERICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 28. U.S. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 29. U.S. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

- TABLE 30. U.S. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 31. U.S. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 32. U.S. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 33. CANADA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 34. CANADA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

- TABLE 35. CANADA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 36. CANADA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 37. CANADA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 38. EUROPE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 39. EUROPE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

- TABLE 40. EUROPE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 41. EUROPE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 42. EUROPE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 43. EUROPE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 44. UK ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 45. UK ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

- TABLE 46. UK ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 47. UK ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 48. UK ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 49. GERMANY ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 50. GERMANY ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

- TABLE 51. GERMANY ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 52. GERMANY ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 53. GERMANY ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 54. FRANCE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 55. FRANCE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

- TABLE 56. FRANCE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 57. FRANCE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 58. FRANCE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 59. ITALY ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 60. ITALY ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

- TABLE 61. ITALY ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 62. ITALY ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 63. ITALY ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 64. SPAIN ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 65. SPAIN ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

- TABLE 66. SPAIN ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 67. SPAIN ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 68. SPAIN ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 69. REST OF EUROPE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 70. REST OF EUROPE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

- TABLE 71. REST OF EUROPE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 72. REST OF EUROPE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 73. REST OF EUROPE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 74. ASIA-PACIFIC ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 75. ASIA-PACIFIC ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

- TABLE 76. ASIA-PACIFIC ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 77. ASIA-PACIFIC ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 78. ASIA-PACIFIC ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 79. ASIA-PACIFIC ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 80. CHINA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 81. CHINA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

- TABLE 82. CHINA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 83. CHINA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 84. CHINA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 85. JAPAN ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 86. JAPAN ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

- TABLE 87. JAPAN ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 88. JAPAN ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 89. JAPAN ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 90. INDIA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 91. INDIA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

- TABLE 92. INDIA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 93. INDIA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 94. INDIA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 95. AUSTRALIA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 96. AUSTRALIA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

- TABLE 97. AUSTRALIA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 98. AUSTRALIA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 99. AUSTRALIA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 100. SOUTH KOREA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 101. SOUTH KOREA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

- TABLE 102. SOUTH KOREA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 103. SOUTH KOREA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 104. SOUTH KOREA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 105. REST OF ASIA-PACIFIC ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 106. REST OF ASIA-PACIFIC ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

- TABLE 107. REST OF ASIA-PACIFIC ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 108. REST OF ASIA-PACIFIC ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 109. REST OF ASIA-PACIFIC ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 110. LAMEA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 111. LAMEA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

- TABLE 112. LAMEA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 113. LAMEA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 114. LAMEA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 115. LAMEA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 116. LATIN AMERICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 117. LATIN AMERICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

- TABLE 118. LATIN AMERICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 119. LATIN AMERICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 120. LATIN AMERICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 121. MIDDLE EAST ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 122. MIDDLE EAST ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

- TABLE 123. MIDDLE EAST ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 124. MIDDLE EAST ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 125. MIDDLE EAST ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 126. AFRICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022-2032 ($MILLION)

- TABLE 127. AFRICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022-2032 ($MILLION)

- TABLE 128. AFRICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 129. AFRICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 130. AFRICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 131. MICROSOFT CORPORATION: KEY EXECUTIVES

- TABLE 132. MICROSOFT CORPORATION: COMPANY SNAPSHOT

- TABLE 133. MICROSOFT CORPORATION: SERVICE SEGMENTS

- TABLE 134. MICROSOFT CORPORATION: PRODUCT PORTFOLIO

- TABLE 135. MICROSOFT CORPORATION: KEY STRATERGIES

- TABLE 136. INTERNATIONAL BUSINESS MACHINES CORPORATION: KEY EXECUTIVES

- TABLE 137. INTERNATIONAL BUSINESS MACHINES CORPORATION: COMPANY SNAPSHOT

- TABLE 138. INTERNATIONAL BUSINESS MACHINES CORPORATION: SERVICE SEGMENTS

- TABLE 139. INTERNATIONAL BUSINESS MACHINES CORPORATION: PRODUCT PORTFOLIO

- TABLE 140. INTERNATIONAL BUSINESS MACHINES CORPORATION: KEY STRATERGIES

- TABLE 141. AMAZON WEB SERVICES, INC.: KEY EXECUTIVES

- TABLE 142. AMAZON WEB SERVICES, INC.: COMPANY SNAPSHOT

- TABLE 143. AMAZON WEB SERVICES, INC.: SERVICE SEGMENTS

- TABLE 144. AMAZON WEB SERVICES, INC.: PRODUCT PORTFOLIO

- TABLE 145. AMAZON WEB SERVICES, INC.: KEY STRATERGIES

- TABLE 146. GOOGLE LLC: KEY EXECUTIVES

- TABLE 147. GOOGLE LLC: COMPANY SNAPSHOT

- TABLE 148. GOOGLE LLC: SERVICE SEGMENTS

- TABLE 149. GOOGLE LLC: PRODUCT PORTFOLIO

- TABLE 150. GOOGLE LLC: KEY STRATERGIES

- TABLE 151. COGNIZANT: KEY EXECUTIVES

- TABLE 152. COGNIZANT: COMPANY SNAPSHOT

- TABLE 153. COGNIZANT: SERVICE SEGMENTS

- TABLE 154. COGNIZANT: PRODUCT PORTFOLIO

- TABLE 155. COGNIZANT: KEY STRATERGIES

- TABLE 156. DREAMBOX LEARNING, INC.: KEY EXECUTIVES

- TABLE 157. DREAMBOX LEARNING, INC.: COMPANY SNAPSHOT

- TABLE 158. DREAMBOX LEARNING, INC.: SERVICE SEGMENTS

- TABLE 159. DREAMBOX LEARNING, INC.: PRODUCT PORTFOLIO

- TABLE 160. BRIDGEU: KEY EXECUTIVES

- TABLE 161. BRIDGEU: COMPANY SNAPSHOT

- TABLE 162. BRIDGEU: SERVICE SEGMENTS

- TABLE 163. BRIDGEU: PRODUCT PORTFOLIO

- TABLE 164. BRIDGEU: KEY STRATERGIES

- TABLE 165. CARNEGIE LEARNING, INC.: KEY EXECUTIVES

- TABLE 166. CARNEGIE LEARNING, INC.: COMPANY SNAPSHOT

- TABLE 167. CARNEGIE LEARNING, INC.: SERVICE SEGMENTS

- TABLE 168. CARNEGIE LEARNING, INC.: PRODUCT PORTFOLIO

- TABLE 169. CARNEGIE LEARNING, INC.: KEY STRATERGIES

- TABLE 170. PEARSON PLC: KEY EXECUTIVES

- TABLE 171. PEARSON PLC: COMPANY SNAPSHOT

- TABLE 172. PEARSON PLC: SERVICE SEGMENTS

- TABLE 173. PEARSON PLC: PRODUCT PORTFOLIO

- TABLE 174. PEARSON PLC: KEY STRATERGIES

- TABLE 175. NUANCE COMMUNICATIONS, INC.: KEY EXECUTIVES

- TABLE 176. NUANCE COMMUNICATIONS, INC.: COMPANY SNAPSHOT

- TABLE 177. NUANCE COMMUNICATIONS, INC.: PRODUCT SEGMENTS

- TABLE 178. NUANCE COMMUNICATIONS, INC.: PRODUCT PORTFOLIO

- TABLE 179. NUANCE COMMUNICATIONS, INC.: KEY STRATERGIES

LIST OF FIGURES

- FIGURE 01. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032

- FIGURE 02. SEGMENTATION OF ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032

- FIGURE 03. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET,2022-2032

- FIGURE 04. TOP INVESTMENT POCKETS IN ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET (2023-2032)

- FIGURE 05. LOW BARGAINING POWER OF SUPPLIERS

- FIGURE 06. LOW THREAT OF NEW ENTRANTS

- FIGURE 07. LOW THREAT OF SUBSTITUTES

- FIGURE 08. LOW INTENSITY OF RIVALRY

- FIGURE 09. LOW BARGAINING POWER OF BUYERS

- FIGURE 10. GLOBAL ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET:DRIVERS, RESTRAINTS AND OPPORTUNITIES

- FIGURE 11. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY COMPONENT, 2022(%)

- FIGURE 12. COMPARATIVE SHARE ANALYSIS OF ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR SOLUTION, BY COUNTRY 2022-2032(%)

- FIGURE 13. COMPARATIVE SHARE ANALYSIS OF ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR SERVICES, BY COUNTRY 2022-2032(%)

- FIGURE 14. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY DEPLOYMENT MODE, 2022(%)

- FIGURE 15. COMPARATIVE SHARE ANALYSIS OF ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR ON-PREMISE, BY COUNTRY 2022-2032(%)

- FIGURE 16. COMPARATIVE SHARE ANALYSIS OF ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR CLOUD, BY COUNTRY 2022-2032(%)

- FIGURE 17. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY TECHNOLOGY, 2022(%)

- FIGURE 18. COMPARATIVE SHARE ANALYSIS OF ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR MACHINE LEARNING AND DEEP LEARNING, BY COUNTRY 2022-2032(%)

- FIGURE 19. COMPARATIVE SHARE ANALYSIS OF ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR NATURAL LANGUAGE PROCESSING (NLP), BY COUNTRY 2022-2032(%)

- FIGURE 20. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY APPLICATION, 2022(%)

- FIGURE 21. COMPARATIVE SHARE ANALYSIS OF ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR LEARNING PLATFORM AND VIRTUAL FACILITATORS , BY COUNTRY 2022-2032(%)

- FIGURE 22. COMPARATIVE SHARE ANALYSIS OF ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR SMART CONTENT DELIVERY, BY COUNTRY 2022-2032(%)

- FIGURE 23. COMPARATIVE SHARE ANALYSIS OF ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR FRAUD AND RISK MANAGEMENT, BY COUNTRY 2022-2032(%)

- FIGURE 24. COMPARATIVE SHARE ANALYSIS OF ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR INTELLIGENT TUTORING SYSTEM (ITS), BY COUNTRY 2022-2032(%)

- FIGURE 25. COMPARATIVE SHARE ANALYSIS OF ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR OTHERS, BY COUNTRY 2022-2032(%)

- FIGURE 26. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, BY END USER, 2022(%)

- FIGURE 27. COMPARATIVE SHARE ANALYSIS OF ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR HIGHER EDUCATION, BY COUNTRY 2022-2032(%)

- FIGURE 28. COMPARATIVE SHARE ANALYSIS OF ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR K-12 EDUCATION, BY COUNTRY 2022-2032(%)

- FIGURE 29. COMPARATIVE SHARE ANALYSIS OF ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR CORPORATE TRAINING AND LEARNING, BY COUNTRY 2022-2032(%)

- FIGURE 30. COMPARATIVE SHARE ANALYSIS OF ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET FOR OTHERS, BY COUNTRY 2022-2032(%)

- FIGURE 31. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET BY REGION, 2022

- FIGURE 32. U.S. ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

- FIGURE 33. CANADA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

- FIGURE 34. UK ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

- FIGURE 35. GERMANY ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

- FIGURE 36. FRANCE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

- FIGURE 37. ITALY ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

- FIGURE 38. SPAIN ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

- FIGURE 39. REST OF EUROPE ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

- FIGURE 40. CHINA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

- FIGURE 41. JAPAN ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

- FIGURE 42. INDIA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

- FIGURE 43. AUSTRALIA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

- FIGURE 44. SOUTH KOREA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

- FIGURE 45. REST OF ASIA-PACIFIC ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

- FIGURE 46. LATIN AMERICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

- FIGURE 47. MIDDLE EAST ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

- FIGURE 48. AFRICA ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET, 2022-2032 ($MILLION)

- FIGURE 49. TOP WINNING STRATEGIES, BY YEAR

- FIGURE 50. TOP WINNING STRATEGIES, BY DEVELOPMENT

- FIGURE 51. TOP WINNING STRATEGIES, BY COMPANY

- FIGURE 52. PRODUCT MAPPING OF TOP 10 PLAYERS

- FIGURE 53. COMPETITIVE DASHBOARD

- FIGURE 54. COMPETITIVE HEATMAP: ARTIFICIAL INTELLIGENCE IN EDUCATION MARKET

- FIGURE 55. TOP PLAYER POSITIONING, 2022

- FIGURE 56. MICROSOFT CORPORATION: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 57. INTERNATIONAL BUSINESS MACHINES CORPORATION: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 58. INTERNATIONAL BUSINESS MACHINES CORPORATION: RESEARCH & DEVELOPMENT EXPENDITURE, 2019-2021 ($MILLION

- FIGURE 59. INTERNATIONAL BUSINESS MACHINES CORPORATION: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 60. INTERNATIONAL BUSINESS MACHINES CORPORATION: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 61. AMAZON WEB SERVICES, INC.: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 62. AMAZON WEB SERVICES, INC.: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 63. AMAZON WEB SERVICES, INC.: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 64. GOOGLE LLC: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 65. GOOGLE LLC: RESEARCH & DEVELOPMENT EXPENDITURE, 2020-2022 ($MILLION)

- FIGURE 66. GOOGLE LLC: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 67. GOOGLE LLC: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 68. COGNIZANT: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 69. COGNIZANT: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 70. PEARSON PLC: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 71. PEARSON PLC: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 72. PEARSON PLC: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 73. NUANCE COMMUNICATIONS, INC.: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 74. NUANCE COMMUNICATIONS, INC.: RESEARCH & DEVELOPMENT EXPENDITURE, 2020-2022 ($MILLION)

- FIGURE 75. NUANCE COMMUNICATIONS, INC.: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 76. NUANCE COMMUNICATIONS, INC.: REVENUE SHARE BY REGION, 2022 (%)

教育领域人工智慧市场规模、份额及成长分析(按组件、部署、技术、应用、最终用途和地区)-2025 年至 2032 年产业预测

教育领域人工智慧市场规模、份额及成长分析(按组件、部署、技术、应用、最终用途和地区)-2025 年至 2032 年产业预测 2025 年全球教育人工智慧市场报告

2025 年全球教育人工智慧市场报告 全球教育人工智慧 (AI) 市场(2025-2029)

全球教育人工智慧 (AI) 市场(2025-2029) 教育市场中的人工智慧(AI):未来预测(2025-2030)2024 年数位学习人工智慧 (AI) 全球市场报告

教育市场中的人工智慧(AI):未来预测(2025-2030)2024 年数位学习人工智慧 (AI) 全球市场报告 教育领域人工智慧的全球市场:按产品、按应用、按技术、按地区 - 到 2030 年的预测

教育领域人工智慧的全球市场:按产品、按应用、按技术、按地区 - 到 2030 年的预测 教育领域人工智慧市场规模、份额、趋势分析报告:按组件、按部署、按技术、按应用、按最终用途、按地区、按细分市场、预测,2025-2030 年

教育领域人工智慧市场规模、份额、趋势分析报告:按组件、按部署、按技术、按应用、按最终用途、按地区、按细分市场、预测,2025-2030 年 教育领域的人工智慧市场:按组成部分、技术、部署、应用程式和最终用途 - 2025-2030 年全球预测全球人工智慧教育市场2024-2031全球人工智慧教育市场报告

教育领域的人工智慧市场:按组成部分、技术、部署、应用程式和最终用途 - 2025-2030 年全球预测全球人工智慧教育市场2024-2031全球人工智慧教育市场报告