|

市场调查报告书

商品编码

1680166

全球国防陆上平台发动机市场:2025-2035年Global Defense Land Platforms Engine Market 2025-2035 |

||||||

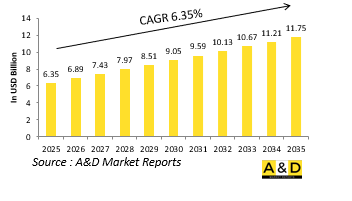

全球国防陆上平台发动机市场规模预计到2025年将成长至 63.5亿美元,到2035年将成长至 117.5亿美元,2025-2035年预测期内的年复合成长率(CAGR)为 6.35%。

全球国防陆上平台发动机市场透过为用于作战、后勤、侦察和人员运输的各种装甲和非装甲地面车辆提供动力,在军事行动中发挥着非常重要的作用。由于陆战仍然是军事战略的基石,对强大、可靠且省油的引擎的需求显着增加。主战坦克、步兵战车、自走炮和战术运输卡车等国防陆上平台需要能够在沙漠环境到北极寒冷等恶劣条件下运作的引擎。这些引擎必须提供高扭矩、增强的机动性和卓越的燃油效率,以支援长时间任务并确保战斗场景中的作战效能。由于进行的军事现代化努力、地缘政治紧张局势和新出现的威胁,全球对陆基防御平台先进推进技术的投资日益增加。引擎製造商和国防承包商致力于下一代动力系统,该系统可提供更高的性能、更少的维护要求以及更强的混合电动和替代燃料适应性。

技术塑造国防陆上平台引擎的发展,并在动力效率、耐用性和数位整合方面取得了重大进步。向混合电力推进的转变是最具变革性的趋势之一,其驱动力来自于降低燃料消耗、减少热讯号和增强隐身能力的需求。研究人员考虑为装甲车辆,特别是侦察和支援车辆采用混合电动和全电动推进系统。先进的柴油引擎技术继续主导市场,涡轮增压、共轨直喷和排气后处理系统的改进提高了燃油经济性并减少了排放。模组化引擎设计使其更容易升级和适应不同的车辆平台。数位引擎管理系统也成为标准,将预测性维护功能与即时诊断和人工智慧(AI)驱动的性能最佳化结合在一起。积层製造彻底改变引擎零件的生产方式,实现轻量化设计、更快的原型製作和弹性材料,延长引擎寿命并提高性能。此外,国防陆上平台的氢燃料电池技术研究也在进行中,军方为未来的作战车辆寻求可持续、后勤高效的推进解决方案。

以军事现代化计划为主导的几个关键驱动因素推动国防陆上平台发动机市场的成长。世界各国都在用更强大、更有效率的引擎升级其装甲车队,以满足不断变化的战场需求。以城市战、不对称威胁和多领域作战为特征的地面战斗日益复杂,需要开发速度更快、机动性更强、弹性更大、更先进的推进系统。对自动和远端控制地面车辆的不断成长的需求也是引擎创新的主要驱动力之一。战略机动性已成为国防军考虑的重点,更强调更轻、更强大的发动机,以提高在各种地形上的部署能力。提高燃料效率也是一个关键驱动因素,因为长期衝突期间的物流和供应链脆弱性凸显了减少燃料依赖的重要性。此外,混合电力和替代燃料技术的整合符合军队更广泛的永续发展计划,确保未来的陆上平台既具有作战效率,也对环境负责。

国防陆上平台发动机市场的区域趋势反映了国家国防优先事项、工业能力和采购策略的差异。北美,特别是美国,仍然是市场的主导力量,主要的国防计画推动着对下一代发动机技术的需求。美国陆军的下一代战斗车(NGCV)计画目的是取代布雷德利战车等老化的装甲平台,并需要创新的推进系统来提高机动性和生存力。配备燃气涡轮发动机的艾布拉姆斯主战坦克进行升级,以提高燃油效率和战场续航能力。General Dynamics、Cummins、Honeywell等主要国防承包商引领陆上平台引擎的进步,采用混合动力系统和人工智慧驱动的诊断技术来提高车辆性能。加拿大也在这个市场中发挥作用,重点是升级其装甲车队并将先进的动力系统解决方案整合到未来的收购中。

本报告研究了全球国防陆上平台发动机市场,并提供了依细分市场的10年市场预测、技术趋势、机会分析、公司概况和国家资料。

目录

国防陆上平台发动机市场报告定义

国防陆上平台发动机市场细分

- 依HP

- 依平台

- 依地区

未来 10年国防陆上平台发动机市场分析

国防陆上平台发动机市场的市场技术

全球国防陆上平台发动机市场预测

国防陆上平台引擎市场趋势与预测(依地区)

- 北美洲

- 驱动因素、限制因素与挑战

- PEST

- 市场预测与情境分析

- 大型公司

- 供应商层级结构

- 企业基准

- 欧洲

- 中东

- 亚太地区

- 南美洲

国防陆上平台发动机市场国家分析

- 美国

- 国防计划

- 最新消息

- 专利

- 目前该市场的技术成熟度

- 市场预测与情境分析

- 加拿大

- 义大利

- 法国

- 德国

- 荷兰

- 比利时

- 西班牙

- 瑞典

- 希腊

- 澳洲

- 南非

- 印度

- 中国

- 俄罗斯

- 韩国

- 日本

- 马来西亚

- 新加坡

- 巴西

国防陆上平台引擎市场机会矩阵

国防陆上平台发动机市场报告专家意见

结论

关于航空和国防市场报告

The Global defense land platforms engine market is estimated at USD 6.35 billion in 2025, projected to grow to USD 11.75 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 6.35% over the forecast period 2025-2035.

Introduction to Defense Land Platforms Engine Market:

The global defense land platforms engine market plays a vital role in military operations, powering a range of armored and unarmored ground vehicles used for combat, logistics, reconnaissance, and personnel transport. As land-based warfare remains a cornerstone of military strategy, the need for powerful, reliable, and fuel-efficient engines has grown significantly. Defense land platforms, including main battle tanks, infantry fighting vehicles, self-propelled artillery, and tactical transport trucks, require engines that can operate in extreme conditions, from desert environments to arctic terrains. These engines must deliver high torque, enhanced mobility, and superior fuel efficiency to support extended missions and ensure operational effectiveness in combat scenarios. With ongoing military modernization efforts, geopolitical tensions, and emerging threats, investments in advanced propulsion technologies for land-based defense platforms are increasing worldwide. Engine manufacturers and defense contractors are focusing on next-generation powertrains that offer improved performance, reduced maintenance requirements, and greater adaptability for hybrid-electric and alternative fuel applications.

Technology Impact in Defense Land Platforms Engine Market:

Technology is shaping the evolution of defense land platform engines, with significant advancements in power efficiency, durability, and digital integration. The shift towards hybrid-electric propulsion is one of the most transformative trends, driven by the need for reduced fuel consumption, lower thermal signatures, and enhanced stealth capabilities. Hybrid-electric and fully electric propulsion systems are being explored for armored vehicles, particularly for reconnaissance and support roles, where silent operations provide a tactical advantage. Advanced diesel engine technologies remain dominant in the market, with improvements in turbocharging, common rail direct injection, and exhaust after-treatment systems enhancing fuel efficiency and reducing emissions. The use of modular engine designs has gained traction, allowing for easier upgrades and adaptability across different vehicle platforms. Digital engine management systems are also becoming standard, incorporating predictive maintenance capabilities through real-time diagnostics and artificial intelligence (AI)-driven performance optimization. Additive manufacturing is revolutionizing the production of engine components, enabling lightweight designs, faster prototyping, and more resilient materials that enhance engine longevity and performance. Additionally, research into hydrogen fuel cell technology for defense land platforms is ongoing, as military forces seek sustainable and logistically efficient propulsion solutions for future combat vehicles.

Key Drivers in Defense Land Platforms Engine Market:

Several key drivers are fueling the growth of the defense land platforms engine market, with military modernization programs at the forefront. Nations worldwide are upgrading their armored vehicle fleets with more powerful and efficient engines to meet evolving battlefield requirements. The increasing complexity of ground combat, characterized by urban warfare, asymmetric threats, and multi-domain operations, has necessitated the development of high-performance propulsion systems that offer greater speed, maneuverability, and resilience. The rise in demand for autonomous and remotely operated ground vehicles is another major factor driving engine innovation, as these platforms require power solutions that maximize endurance and operational flexibility. Strategic mobility has become a critical consideration for defense forces, leading to a greater emphasis on lightweight yet high-output engines that enhance deployability across diverse terrains. The push for improved fuel efficiency is also a significant driver, as logistics and supply chain vulnerabilities in extended conflicts highlight the importance of reducing fuel dependence. Additionally, the integration of hybrid-electric and alternative fuel technologies aligns with broader military sustainability initiatives, ensuring that future land-based platforms remain both operationally effective and environmentally conscious.

Regional Trends in Defense Land Platforms Engine Market:

Regional trends in the defense land platforms engine market reflect varying defense priorities, industrial capabilities, and procurement strategies. North America, particularly the United States, remains a dominant force in the market, with major defense programs driving demand for next-generation engine technologies. The U.S. Army's Next-Generation Combat Vehicle (NGCV) program, aimed at replacing aging armored platforms such as the Bradley Fighting Vehicle, is pushing for innovative propulsion systems that enhance mobility and survivability. The Abrams Main Battle Tank, powered by a gas turbine engine, is undergoing upgrades to improve fuel efficiency and battlefield endurance. Major defense contractors, including General Dynamics, Cummins, and Honeywell, are leading advancements in land platform engines, incorporating hybrid-electric powertrains and AI-driven diagnostics to enhance vehicle performance. Canada also plays a role in the market, focusing on upgrading its armored vehicle fleets and integrating advanced powertrain solutions into future acquisitions.

In Europe, the defense land platforms engine market is characterized by multinational collaboration and a strong emphasis on indigenous defense manufacturing. Countries such as Germany, France, and the United Kingdom are at the forefront of armored vehicle engine development, with companies like MTU Friedrichshafen, Renault Trucks Defense, and Rolls-Royce contributing to cutting-edge propulsion technologies. The European Main Battle Tank (EMBT) program, a joint effort between France's Nexter and Germany's KMW, is driving research into next-generation tank engines with improved efficiency and modularity. The UK's Challenger 3 program, which focuses on upgrading the British Army's main battle tanks, includes enhancements to powertrain systems for better speed and fuel economy. Europe's emphasis on interoperability within NATO forces has also led to standardization efforts in engine technologies, ensuring seamless integration across allied armored vehicle fleets.

The Asia-Pacific region is experiencing significant growth in the defense land platforms engine market, fueled by increasing military expenditures, regional security concerns, and indigenous defense production initiatives. China has made substantial investments in developing advanced land-based propulsion systems, with its Type 99 main battle tank featuring high-performance diesel engines designed for enhanced speed and endurance. The country is also exploring hybrid-electric technologies for future armored vehicle platforms. India's defense industry is making strides in indigenous tank engine development, with the Defence Research and Development Organisation (DRDO) working on next-generation powertrains for the Arjun main battle tank and other armored vehicles. Japan and South Korea are similarly advancing their land platform capabilities, with South Korea's K2 Black Panther tank incorporating a powerful and efficient engine system that enhances battlefield mobility. The region's focus on self-reliance in defense manufacturing is driving investments in domestic engine production capabilities, reducing reliance on foreign suppliers.

The Middle East presents a strong market for defense land platform engines, with nations such as Saudi Arabia, the United Arab Emirates, and Israel investing heavily in armored vehicle modernization. These countries rely on a mix of Western and locally produced defense technologies, with ongoing procurement of advanced main battle tanks, infantry fighting vehicles, and tactical transport platforms. Harsh desert environments necessitate engines that can withstand extreme temperatures and operate efficiently under high dust and sand exposure. The region's defense programs emphasize both new acquisitions and engine upgrades for existing fleets, ensuring that military ground forces maintain operational readiness and strategic mobility.

Africa's defense land platforms engine market is relatively smaller but growing steadily as regional security challenges drive military procurement and modernization efforts. Many African nations operate legacy armored vehicles that require engine upgrades or replacements to remain viable in contemporary combat scenarios. Countries such as Egypt, Algeria, and South Africa are leading players in the region's defense sector, investing in both Western and Russian-made land platforms. Additionally, the demand for light tactical vehicles with high-performance engines is increasing due to counterterrorism operations and border security initiatives. Maintenance, repair, and overhaul (MRO) services are crucial in Africa, as many defense forces seek cost-effective solutions to extend the lifespan of their existing vehicle fleets.

Key Defense Land Platforms Engine Program:

Russia will supply new engines for the Indian Army's T-72 Soviet-era battle tanks under a $248-million contract awarded by the Indian Ministry of Defence to Rosoboronexport. As part of the agreement, the Russian state-owned defense exporter will deliver modern 1,000-horsepower engines to upgrade India's aging T-72 Ural main battle tanks. The Indian military currently operates around 2,500 T-72 tanks, which have been equipped with legacy 780-horsepower engines since their production began in the 1970s.

The Australian Department of Defence has signed a contract with Penske Australia to provide local industry support for diesel engine sustainment, ensuring the Australian Defence Force (ADF) remains operationally ready for deployment whenever required. Acting Deputy Secretary for Naval Shipbuilding and Sustainment, Rear Admiral Wendy Malcolm, stated that the five-year, $190 million agreement builds on the benefits of the previous contract while introducing greater cost transparency, improved risk management, and enhanced opportunities to strengthen sovereign capability.

Table of Contents

Defense Land Platform Engines Market Report Definition

Defense Land Platform Engines Market Segmentation

By HP

By Platform

By Region

Defense Land Platform Engines Market Analysis for next 10 Years

The 10-year defense land platform engines market analysis would give a detailed overview of defense land platform engines market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Land Platform Engines Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Land Platform Engines Market Forecast

The 10-year defense land platform engines market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Land Platform Engines Market Trends & Forecast

The regional defense land platform engines market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense Land Platform Engines Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Land Platform Engines Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Land Platform Engines Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2025-2035

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2025-2035

- Table 18: Scenario Analysis, Scenario 1, By Platform Type, 2025-2035

- Table 19: Scenario Analysis, Scenario 1, By Engine Type, 2025-2035

- Table 20: Scenario Analysis, Scenario 2, By Region, 2025-2035

- Table 21: Scenario Analysis, Scenario 2, By Platform Type, 2025-2035

- Table 22: Scenario Analysis, Scenario 2, By Engine Type, 2025-2035

List of Figures

- Figure 1: Global Land Platform Engine Market Forecast, 2025-2035

- Figure 2: Global Land Platform Engine Market Forecast, By Region, 2025-2035

- Figure 3: Global Land Platform Engine Market Forecast, By Platform Type, 2025-2035

- Figure 4: Global Land Platform Engine Market Forecast, By Engine Type, 2025-2035

- Figure 5: North America, Land Platform Engine Market, Market Forecast, 2025-2035

- Figure 6: Europe, Land Platform Engine Market, Market Forecast, 2025-2035

- Figure 7: Middle East, Land Platform Engine Market, Market Forecast, 2025-2035

- Figure 8: APAC, Land Platform Engine Market, Market Forecast, 2025-2035

- Figure 9: South America, Land Platform Engine Market, Market Forecast, 2025-2035

- Figure 10: United States, Land Platform Engine Market, Technology Maturation, 2025-2035

- Figure 11: United States, Land Platform Engine Market, Market Forecast, 2025-2035

- Figure 12: Canada, Land Platform Engine Market, Technology Maturation, 2025-2035

- Figure 13: Canada, Land Platform Engine Market, Market Forecast, 2025-2035

- Figure 14: Italy, Land Platform Engine Market, Technology Maturation, 2025-2035

- Figure 15: Italy, Land Platform Engine Market, Market Forecast, 2025-2035

- Figure 16: France, Land Platform Engine Market, Technology Maturation, 2025-2035

- Figure 17: France, Land Platform Engine Market, Market Forecast, 2025-2035

- Figure 18: Germany, Land Platform Engine Market, Technology Maturation, 2025-2035

- Figure 19: Germany, Land Platform Engine Market, Market Forecast, 2025-2035

- Figure 20: Netherlands, Land Platform Engine Market, Technology Maturation, 2025-2035

- Figure 21: Netherlands, Land Platform Engine Market, Market Forecast, 2025-2035

- Figure 22: Belgium, Land Platform Engine Market, Technology Maturation, 2025-2035

- Figure 23: Belgium, Land Platform Engine Market, Market Forecast, 2025-2035

- Figure 24: Spain, Land Platform Engine Market, Technology Maturation, 2025-2035

- Figure 25: Spain, Land Platform Engine Market, Market Forecast, 2025-2035

- Figure 26: Sweden, Land Platform Engine Market, Technology Maturation, 2025-2035

- Figure 27: Sweden, Land Platform Engine Market, Market Forecast, 2025-2035

- Figure 28: Brazil, Land Platform Engine Market, Technology Maturation, 2025-2035

- Figure 29: Brazil, Land Platform Engine Market, Market Forecast, 2025-2035

- Figure 30: Australia, Land Platform Engine Market, Technology Maturation, 2025-2035

- Figure 31: Australia, Land Platform Engine Market, Market Forecast, 2025-2035

- Figure 32: India, Land Platform Engine Market, Technology Maturation, 2025-2035

- Figure 33: India, Land Platform Engine Market, Market Forecast, 2025-2035

- Figure 34: China, Land Platform Engine Market, Technology Maturation, 2025-2035

- Figure 35: China, Land Platform Engine Market, Market Forecast, 2025-2035

- Figure 36: Saudi Arabia, Land Platform Engine Market, Technology Maturation, 2025-2035

- Figure 37: Saudi Arabia, Land Platform Engine Market, Market Forecast, 2025-2035

- Figure 38: South Korea, Land Platform Engine Market, Technology Maturation, 2025-2035

- Figure 39: South Korea, Land Platform Engine Market, Market Forecast, 2025-2035

- Figure 40: Japan, Land Platform Engine Market, Technology Maturation, 2025-2035

- Figure 41: Japan, Land Platform Engine Market, Market Forecast, 2025-2035

- Figure 42: Malaysia, Land Platform Engine Market, Technology Maturation, 2025-2035

- Figure 43: Malaysia, Land Platform Engine Market, Market Forecast, 2025-2035

- Figure 44: Singapore, Land Platform Engine Market, Technology Maturation, 2025-2035

- Figure 45: Singapore, Land Platform Engine Market, Market Forecast, 2025-2035

- Figure 46: United Kingdom, Land Platform Engine Market, Technology Maturation, 2025-2035

- Figure 47: United Kingdom, Land Platform Engine Market, Market Forecast, 2025-2035

- Figure 48: Opportunity Analysis, Land Platform Engine Market, By Region (Cumulative Market), 2025-2035

- Figure 49: Opportunity Analysis, Land Platform Engine Market, By Region (CAGR), 2025-2035

- Figure 50: Opportunity Analysis, Land Platform Engine Market, By Platform Type (Cumulative Market), 2025-2035

- Figure 51: Opportunity Analysis, Land Platform Engine Market, By Platform Type (CAGR), 2025-2035

- Figure 52: Opportunity Analysis, Land Platform Engine Market, By Engine Type (Cumulative Market), 2025-2035

- Figure 53: Opportunity Analysis, Land Platform Engine Market, By Engine Type (CAGR), 2025-2035

- Figure 54: Scenario Analysis, Land Platform Engine Market, Cumulative Market, 2025-2035

- Figure 55: Scenario Analysis, Land Platform Engine Market, Global Market, 2025-2035

- Figure 56: Scenario 1, Land Platform Engine Market, Total Market, 2025-2035

- Figure 57: Scenario 1, Land Platform Engine Market, By Region, 2025-2035

- Figure 58: Scenario 1, Land Platform Engine Market, By Platform Type, 2025-2035

- Figure 59: Scenario 1, Land Platform Engine Market, By Engine Type, 2025-2035

- Figure 60: Scenario 2, Land Platform Engine Market, Total Market, 2025-2035

- Figure 61: Scenario 2, Land Platform Engine Market, By Region, 2025-2035

- Figure 62: Scenario 2, Land Platform Engine Market, By Platform Type, 2025-2035

- Figure 63: Scenario 2, Land Platform Engine Market, By Engine Type, 2025-2035

- Figure 64: Company Benchmark, Land Platform Engine Market, 2025-2035