|

市场调查报告书

商品编码

1811813

特殊用途陆上车辆的全球市场:2025年~2035年Global Special Purpose Land Vehicles Market 2025 - 2035 |

||||||

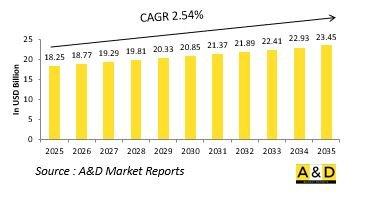

2025年,全球特殊用途陆地车辆市场规模估计为182.5亿美元,预计到2035年将增长至234.5亿美元,2025年至2035年的复合年增长率 (CAGR) 为2.54%。

特殊用途陆地车辆市场简介

国防特殊用途陆地车辆是全球国防工业的重要组成部分,旨在执行标准军用平台无法有效完成的任务。这些车辆的设计考虑了从战术机动和侦察到指挥、技术支援和救援行动等特定功能。它们的主要优势在于能够适应不同的地形和任务要求,这使得它们在战斗和支援任务中都至关重要。与传统的装甲车辆和运输工具不同,它们采用了专门的系统、设备和结构改进,以增强其在复杂环境中的适应性。市场受到不断变化的战争和安全需求的影响。现代衝突不仅需要防御力量和火力,还需要快速适应能力、后勤效率和特定任务的表现。因此,此类车辆的设计和采购强调模组化、生存力以及与更广泛作战网路的整合。这些车辆作为地面骨干支援部队,保障供应链安全,并在具有课题性的情况下确保部队的机动性。无论是部署在现役作战、人道主义援助或衝突地区的基础设施维修中,国防特种用途陆地车辆在确保军队保持作战能力、韧性和作战灵活性方面都发挥着至关重要的作用。

科技对特殊用途陆地车辆市场的影响

科技在塑造国防特种任务飞机方面的作用日益突出,推动了其能力的提升和任务效能的提升。先进技术正在将这些平台转变为高度网路化的资产,在情报、监视、电子战和通讯支援等任务中发挥重要作用。整合尖端感测器组件,能够以前所未有的精度探测、追踪和分析多域活动。这些改进使部队能够在复杂、衝突频繁的环境中保持态势感知。数位化是核心主题,它能够与地面、海军和太空资产实现即时资讯共享和互通性。飞机现在充当飞行指挥中心,即时向决策者和前线部队传输关键讯息。人工智慧和机器学习等新兴技术透过提供预测性洞察和自动化威胁侦测,进一步优化了任务规划和执行。材料科学和推进领域的创新也发挥作用,使其拥有更长的续航时间和更高的效率。此外,电子战和网路安全措施确保这些飞机在敌方可能试图破坏通讯和感测器性能的对抗战场上保持有效作战能力。总而言之,这些进步显示了科技对特种任务飞机发展的决定性影响。

特种用途陆地车辆市场的关键驱动因素

国防特种用途陆地车辆的需求受安全需求、作战需求和技术机会等因素共同影响。成长的一个关键驱动因素是威胁性质的变化,要求军队同时应对常规和非常规战争场景。特种用途车辆提供应对这种多样性所需的客製化能力,提供标准军用平台无法提供的增强防护、机动性和任务专用装备。另一个驱动因素是对韧性和部队防护的需求。现代衝突通常涉及不对称战术,例如伏击和简易爆炸装置,这需要车辆配备先进的装甲、防御系统和高生存能力标准。军方也意识到速度和机动性的重要性,要求车辆能够在城市景观、偏远地区和崎岖地形中行驶,且不影响安全性。经济和后勤的考虑进一步影响了需求。模组化和多用途车辆极具吸引力,因为它们能够降低生命週期成本,并透过支援多项任务来最大限度地提高车队效用。军队不仅在战斗中扮演日益重要的角色,还在人道援助、维和和基础设施修復方面发挥越来越重要的作用,这强化了多用途车辆的需求。国防需求与民用用途的整合使市场处于重要的战略地位。

特种用途陆地车辆市场的区域趋势

不同区域对国防特种用途陆地车辆的需求反映了不同的作战环境、战略重点和工业能力。边境地区广阔且衝突频繁的国家优先考虑能够确保持续监视和快速反应能力的侦察和巡逻车辆。地形复杂(例如山区、沙漠和茂密森林)的国家则需要针对越野耐久性、后勤支援和工程作业进行最佳化的平台。这些地理因素显着影响采购选择,从而形成了区域性的特定需求。技术先进的地区注重现代化和数位系统整合。这些军队优先考虑具有模组化架构、先进防护和网路化能力的车辆,以确保与盟军的互通性。相较之下,新兴国家往往青睐成本效益高、用途广泛的平台,这些平台能够适应各种任务,同时仍能提供可靠的效能。这种务实的做法使他们能够在预算限制和作战效能之间取得平衡。此外,非战斗任务也会影响区域战略。易受自然灾害影响的地区会投资可用于救援和重建的车辆,而参与维和行动的国家则优先考虑机动性和防护能力,以支持稳定行动。国内工业能力也发挥关键作用,有些国家优先考虑国内发展,而有些国家则寻求合作或进口。这种多样性使得区域市场能够根据区域优先事项和全球趋势发展。

大型特种用途陆地车辆计画

芬兰国防军后勤司令部 (FDFLOGCOM) 已完成扩展采购合约的最后阶段,以 3,650 万欧元(4,050 万美元)的价格采购了 29 辆 Patria XA-300 (6x6) 装甲运兵车。这些车辆将增强芬兰陆军的作战能力,并提供一种预计将服役至 2060 年代的现代化机动装备。此次订单标誌着 2023 年合约的最后阶段,该合约包含最多 70 辆追加车辆的选择权。此次采购使 Patria XA-300 车队更接近原始合约的全部范围,原始合约涵盖 91 辆车辆,并可选择追加 70 辆。

目录

特殊用途陆上车辆市场报告定义

特殊用途陆上车辆市场区隔

各用途

各地区

各类型

未来10年专用陆地车辆市场分析

本章详细概述了专用陆地车辆市场的成长、变化趋势、技术采用概况以及整体市场吸引力。

专用陆地车辆市场的市场技术

本部分讨论了预计将影响该市场的十大技术,以及这些技术可能对整体市场产生的潜在影响。

全球专用陆地车辆市场预测

本报告对上述细分市场进行了详细的10年专用陆地车辆市场预测。

专用陆上车辆市场趋势及各地区预测

本部分涵盖各地区专用陆地车辆市场趋势、驱动因素、限制因素、课题以及政治、经济、社会和技术层面。此外,本部分也提供详细的区域市场预测和情境分析。区域分析包括主要公司概况、供应商格局和公司基准分析。目前市场规模是基于常规情境估算。

北美

驱动因素、限制因素与课题

PEST

市场预测与情境分析

主要公司

供应商层级结构

公司基准测试

欧洲

中东

亚太地区

南美洲

特殊用途陆地车辆市场国家分析

本章涵盖该市场的主要国防项目以及该市场的最新新闻和专利申请情况。本章也提供未来10年的市场预测和国家/地区情境分析。

美国

国防计画

最新消息

专利

该市场目前的技术成熟度

市场预测与情势分析

加拿大

义大利

法国

德国

荷兰

比利时

西班牙

瑞典

希腊

澳洲

南非

印度

中国

俄罗斯

韩国

日本

马来西亚

新加坡

巴西

特殊用途陆上车辆市场机会矩阵

机会矩阵帮助读者了解该市场中高机会细分市场。

特殊用途陆上车辆市场报告方面的专家见解

我们提供专家对该市场潜力分析的意见。

结论

关于调查公司

The Global Special Purpose Land Vehicles market is estimated at USD 18.25 billion in 2025, projected to grow to USD 23.45 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 2.54% over the forecast period 2025-2035.

Introduction to Special Purpose Land Vehicles Market:

Defense special purpose land vehicles form a vital segment of the global defense industry, built to serve missions that standard military platforms cannot address effectively. These vehicles are engineered with specific functions in mind, ranging from tactical mobility and reconnaissance to command, engineering support, and recovery operations. Their primary strength lies in their ability to adapt to diverse terrains and mission requirements, making them essential in both combat and support roles. Unlike conventional armored or transport vehicles, they are tailored with specialized systems, equipment, and structural modifications that enhance their suitability for complex environments. The market is shaped by the evolving nature of warfare and security needs. Modern conflicts demand not only protection and firepower but also rapid adaptability, logistical efficiency, and mission-specific performance. As a result, the design and procurement of such vehicles emphasize modularity, survivability, and integration with broader operational networks. They serve as the ground-level backbone that supports troops, ensures supply chains, and enables force mobility in challenging scenarios. Whether deployed for active combat, humanitarian assistance, or infrastructure repair in conflict zones, defense special purpose land vehicles play a crucial role in ensuring that armed forces remain capable, resilient, and operationally versatile.

Technology Impact in Special Purpose Land Vehicles Market:

The role of technology in shaping defense special mission aircraft has become increasingly pronounced, driving both capability enhancement and mission effectiveness. Advanced technologies are transforming these platforms into highly networked assets that operate at the intersection of intelligence gathering, surveillance, electronic warfare, and communication support. The integration of modern sensor suites provides the ability to detect, track, and analyze activity across multiple domains with unprecedented accuracy. These improvements allow forces to maintain situational awareness even in complex and contested environments. Digitalization is a central theme, enabling real-time information sharing and interoperability with ground, naval, and space assets. Aircraft now act as flying command centers, transmitting critical intelligence instantly to decision-makers and frontline units. Emerging technologies such as artificial intelligence and machine learning are further optimizing mission planning and execution by offering predictive insights and automating aspects of threat detection. Materials science and propulsion innovations have also played a role, allowing for extended endurance and improved efficiency. In addition, electronic warfare and cybersecurity measures are ensuring that these aircraft remain effective in highly competitive theaters where adversaries may attempt to disrupt communications or sensor performance. Collectively, these advancements highlight technology's decisive impact on the evolution of special mission aircraft.

Key Drivers in Special Purpose Land Vehicles Market:

The demand for defense special purpose land vehicles is shaped by a combination of security imperatives, operational requirements, and technological opportunities. A key factor driving growth is the changing nature of threats, where forces must be prepared for both conventional battles and irregular warfare scenarios. Special purpose vehicles provide the tailored capabilities needed to address this diversity, offering enhanced protection, mobility, and mission-specific equipment that cannot be achieved with standard military platforms. Another driver lies in the need for resilience and force protection. Modern conflicts often involve asymmetric tactics, such as ambushes and improvised explosive devices, which necessitate vehicles equipped with advanced armor, defensive systems, and high survivability standards. Militaries also recognize the importance of speed and maneuverability, requiring vehicles capable of operating in urban landscapes, remote areas, and rugged terrains without compromising safety. Economic and logistical considerations further shape demand. Modular and multi-role vehicles are appealing because they reduce lifecycle costs and maximize fleet utility by supporting multiple missions. Beyond combat, the growing role of armed forces in humanitarian aid, peacekeeping, and infrastructure restoration has strengthened the case for versatile vehicles. This blend of defense necessity and civil utility positions the market as strategically significant.

Regional Trends in Special Purpose Land Vehicles Market:

Regional demand for defense special purpose land vehicles reflects distinct operational environments, strategic priorities, and industrial capacities. Nations with expansive and often contested borders prioritize reconnaissance and patrol vehicles that ensure persistent monitoring and quick reaction capability. Countries with difficult terrain, such as mountains, deserts, or dense forests, seek platforms optimized for off-road endurance, logistics, and engineering tasks. These geographical factors heavily influence procurement choices, leading to diverse requirements across regions. In technologically advanced regions, emphasis is placed on modernization and the integration of digital systems. These militaries prioritize vehicles with modular configurations, advanced protection measures, and network-enabled capabilities to ensure interoperability with allied forces. By contrast, emerging economies often favor cost-efficient, multipurpose platforms that provide solid performance while remaining adaptable to various missions. This pragmatic approach allows them to balance budgetary constraints with operational effectiveness. Additionally, non-combat missions have influenced regional strategies. Areas prone to natural disasters invest in vehicles that can be deployed for relief and reconstruction, while countries engaged in peacekeeping focus on mobility and protection for stability operations. Domestic industrial capacity also plays a role, with some nations emphasizing indigenous development while others pursue partnerships or imports. This variety ensures that regional markets evolve in line with local priorities and global trends.

Key Special Purpose Land Vehicles Program:

The Finnish Defence Forces Logistics Command (FDFLOGCOM) has completed the acquisition of 29 Patria XA-300 (6X6) armoured personnel carriers for €36.5 million ($40.5 million), concluding the final phase of an expanded procurement agreement. These vehicles will strengthen the Finnish Army's operational capability, providing modern mobility assets expected to remain in service through the 2060s. This order represents the concluding tranche of a 2023 agreement that included an option for up to 70 additional units. With this procurement, the total fleet of Patria XA-300s moves closer to the full scope of the original contract, which initially covered 91 vehicles with an option for 70 more.

Table of Contents

Special Purpose Land Vehicles Market Report Definition

Special Purpose Land Vehicles Market Segmentation

By Application

By Region

By Type

Special Purpose Land Vehicles Market Analysis for next 10 Years

The 10-year special purpose land vehicles market analysis would give a detailed overview of special purpose land vehicles market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Special Purpose Land Vehicles Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Special Purpose Land Vehicles Market Forecast

The 10-year special purpose land vehicles market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Special Purpose Land Vehicles Market Trends & Forecast

The regional special purpose land vehicles market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Special Purpose Land Vehicles Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Special Purpose Land Vehicles Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Special Purpose Land Vehicles Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2025-2035

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2025-2035

- Table 18: Scenario Analysis, Scenario 1, By Type, 2025-2035

- Table 19: Scenario Analysis, Scenario 1, By Application, 2025-2035

- Table 20: Scenario Analysis, Scenario 2, By Region, 2025-2035

- Table 21: Scenario Analysis, Scenario 2, By Type, 2025-2035

- Table 22: Scenario Analysis, Scenario 2, By Application, 2025-2035

List of Figures

- Figure 1: Global Special Purpose Land Market Forecast, 2025-2035

- Figure 2: Global Special Purpose Land Market Forecast, By Region, 2025-2035

- Figure 3: Global Special Purpose Land Market Forecast, By Type, 2025-2035

- Figure 4: Global Special Purpose Land Market Forecast, By Application, 2025-2035

- Figure 5: North America, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 6: Europe, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 7: Middle East, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 8: APAC, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 9: South America, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 10: United States, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 11: United States, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 12: Canada, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 13: Canada, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 14: Italy, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 15: Italy, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 16: France, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 17: France, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 18: Germany, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 19: Germany, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 20: Netherlands, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 21: Netherlands, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 22: Belgium, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 23: Belgium, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 24: Spain, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 25: Spain, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 26: Sweden, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 27: Sweden, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 28: Brazil, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 29: Brazil, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 30: Australia, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 31: Australia, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 32: India, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 33: India, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 34: China, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 35: China, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 36: Saudi Arabia, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 37: Saudi Arabia, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 38: South Korea, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 39: South Korea, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 40: Japan, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 41: Japan, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 42: Malaysia, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 43: Malaysia, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 44: Singapore, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 45: Singapore, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 46: United Kingdom, Special Purpose Land Market, Technology Maturation, 2025-2035

- Figure 47: United Kingdom, Special Purpose Land Market, Market Forecast, 2025-2035

- Figure 48: Opportunity Analysis, Special Purpose Land Market, By Region (Cumulative Market), 2025-2035

- Figure 49: Opportunity Analysis, Special Purpose Land Market, By Region (CAGR), 2025-2035

- Figure 50: Opportunity Analysis, Special Purpose Land Market, By Type (Cumulative Market), 2025-2035

- Figure 51: Opportunity Analysis, Special Purpose Land Market, By Type (CAGR), 2025-2035

- Figure 52: Opportunity Analysis, Special Purpose Land Market, By Application (Cumulative Market), 2025-2035

- Figure 53: Opportunity Analysis, Special Purpose Land Market, By Application (CAGR), 2025-2035

- Figure 54: Scenario Analysis, Special Purpose Land Market, Cumulative Market, 2025-2035

- Figure 55: Scenario Analysis, Special Purpose Land Market, Global Market, 2025-2035

- Figure 56: Scenario 1, Special Purpose Land Market, Total Market, 2025-2035

- Figure 57: Scenario 1, Special Purpose Land Market, By Region, 2025-2035

- Figure 58: Scenario 1, Special Purpose Land Market, By Type, 2025-2035

- Figure 59: Scenario 1, Special Purpose Land Market, By Application, 2025-2035

- Figure 60: Scenario 2, Special Purpose Land Market, Total Market, 2025-2035

- Figure 61: Scenario 2, Special Purpose Land Market, By Region, 2025-2035

- Figure 62: Scenario 2, Special Purpose Land Market, By Type, 2025-2035

- Figure 63: Scenario 2, Special Purpose Land Market, By Application, 2025-2035

- Figure 64: Company Benchmark, Special Purpose Land Market, 2025-2035