|

市场调查报告书

商品编码

1735755

无人水面载具(USV)·无人水下载具(UUV)的全球市场(2025年~2035年)Global Unmanned Surface and Underwater Vessels Market 2025-2035 |

||||||

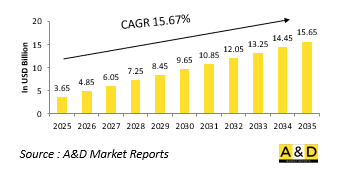

全球无人水面航行器 (USV) 和无人水下航行器 (UUV) 市场规模预计在 2025 年达到 36.5 亿美元,预计到 2035 年将达到 156.5 亿美元,在 2025-2035 年预测期内的复合年增长率为 15.67%。

科技对无人水面艇 (USV) 和无人水下艇 (UUV) 市场的影响

技术创新正在显着重塑无人水面艇 (USV) 和无人水下艇 (UUV) 在国防行动中的角色和能力。这些系统如今利用先进的导航、推进和感测器技术,实现高度自主和精确的运作。舰载智慧系统使它们能够规划最佳路线、规避危险,并在最少的人工干预下完成任务。水面舰艇透过整合雷达、光学追踪和电子战套件,增强了威胁侦测和交战能力。另一方面,潜水器配备了声纳成像、磁异常感测器和声学通讯系统,使其能够在复杂的海底环境中导航和作业。人工智慧在实现自适应行为方面发挥关键作用,使舰艇能够评估情况并即时调整战术。增强型能源系统支援更长时间的作业,而低噪音推进系统则最大限度地降低了探测风险。安全的通讯框架确保即使在对抗环境中也能与指挥链和其他资产进行协调。这些技术还支援无人船与有人船、飞机和卫星网路协同作战,从而实现一体化防御。随着软体和硬体的不断发展,这些平台正变得更具弹性、更有效率、用途更广泛,突破了传统海上交战的界限,并为海战效能树立了新的标准。

无人水面航行器 (USV) 和无人水下航行器 (UUV) 市场的关键推动因素

无人水面航行器 (USV) 和无人水下航行器 (UUV) 在国防战略中的崛起,是由几个相互关联的因素推动的,这些因素凸显了它们的战略价值。其中最重要的是扩大作战范围,同时最大限度地降低人员风险。这些平台可以部署在高威胁区域,执行重复性或危险任务,并且可以长时间作战而不会疲劳。围绕领海和水下资源的战略竞争也促使各国加强其海军情报和监视能力。无人船提供了一种经济高效的持续监视解决方案,可以单独运行,也可以作为更广泛系统的一部分运行。此外,水雷和隐形潜艇的威胁日益增加,使得那些能够在不危及有人船的情况下进行探测和扫荡的平台重新受到关注。技术可行性使这些系统更具吸引力,因为自主性、续航能力和感测器整合度的提升提高了可靠性和作战成功率。海上行动分散化的政策转变进一步支持部署无人系统作为力量倍增器。无人系统能够灵活应对从威慑到快速危机应变等一系列场景。简而言之,战略必要性、技术准备和作战效率的整合正在推动全球部署这些先进海军装备的势头。

无人水面航行器 (USV) 和无人水下航行器 (UUV) 市场的区域趋势

各区域对无人水面航行器 (USV) 和无人水下航行器 (UUV) 的国防部署方式反映了不同的安全优先事项和技术投资。在印度-太平洋地区,海上衝突和战略水道保护正在推动水面和水下无人装备的积极发展和部署。海岸监视、反入侵行动和海事感知是该地区多个国家的关键领域。北美军队正优先将这些系统纳入大型海军演习和舰队现代化计划,以保持远程作战和水下优势。

本报告提供全球无人水面载具(USV)·无人水下载具(UUV)市场相关调查分析,提供今后10年成长促进因素,预测,各地区趋势等资讯。

目录

无人水面载具(USV)·无人水下载具(UUV)市场报告定义

无人水面载具(USV)·无人水下载具(UUV)市场区隔

各地区

各用途

按行动方式

今后10年的无人水面载具(USV)·无人水下载具(UUV)市场分析

无人水面载具(USV)·无人水下载具(UUV)市场技术

全球无人水面载具(USV)·无人水下载具(UUV)市场预测

地区的无人水面载具(USV)·无人水下载具(UUV)市场趋势与预测

北美

促进因素,阻碍因素,课题

PEST

市场预测与情势分析

主要企业

供应商层级格局

企业基准

欧洲

中东

亚太地区

南美

无人水面载具(USV)·无人水下载具(UUV)市场分析:各国

美国

最新消息

专利

这个市场上目前技术成熟度

市场预测与情势分析

加拿大

义大利

法国

德国

荷兰

比利时

西班牙

瑞典

希腊

澳洲

南非

印度

中国

俄罗斯

韩国

日本

马来西亚

新加坡

巴西

无人水面载具(USV)·无人水下载具(UUV)市场机会矩阵

无人水面载具(USV)·无人水下载具(UUV)市场报告相关专家的意见

结论

关于Aviation and Defense Market Reports

The Global Unmanned Surface and Underwater Vessels market is estimated at USD 3.65 billion in 2025, projected to grow to USD 15.65 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 15.67% over the forecast period 2025-2035.

Introduction to Unmanned Surface and Underwater Vessels Market:

Defense unmanned surface and underwater vessels have become central to the modernization of naval forces worldwide. These platforms offer strategic capabilities that enhance situational awareness, extend operational reach, and reduce the exposure of personnel in dangerous maritime environments. By operating autonomously or under remote control, these vessels support a wide range of missions such as anti-submarine warfare, mine countermeasures, intelligence collection, and maritime patrols. Surface units navigate above water to perform visible deterrence and surveillance, while underwater systems execute stealth missions that involve detection, reconnaissance, or precision strikes. The demand for these technologies is accelerating as maritime challenges evolve, requiring persistent presence and rapid adaptability. With increased activity in littoral zones, contested waterways, and strategic choke points, navies are seeking reliable solutions that can perform effectively across various ocean conditions. The modular nature of these systems allows for mission-specific configurations, making them suitable for both routine security and high-threat operations. Defense organizations are integrating unmanned maritime vessels into their existing fleets to complement traditional assets and support distributed operational models. As maritime threats become more unpredictable and technologically sophisticated, unmanned surface and underwater systems are proving indispensable in maintaining maritime dominance and executing complex naval strategies with greater precision and flexibility.

Technology Impact in Unmanned Surface and Underwater Vessels Market:

Technological innovation is dramatically reshaping the roles and capabilities of unmanned surface and underwater vessels in defense operations. These systems now leverage advanced navigation, propulsion, and sensor technologies to execute missions with high levels of autonomy and accuracy. Onboard intelligence enables them to chart optimal routes, avoid hazards, and complete tasks with minimal human input. In surface vessels, integration of radar, optical tracking, and electronic warfare suites enhances threat detection and engagement. Meanwhile, underwater vehicles benefit from sonar imaging, magnetic anomaly sensors, and acoustic communication systems that allow them to navigate and operate in complex sub-sea environments. Artificial intelligence plays a crucial role in enabling adaptive behavior, allowing vessels to assess conditions and adjust tactics in real time. Enhanced energy systems support longer missions, while low-noise propulsion minimizes detection risk. Secure communication frameworks ensure coordination with command structures and other assets, even in contested environments. These technologies also support the use of unmanned vessels in coordinated operations with manned ships, aircraft, and satellite networks, enabling a unified defense approach. As software and hardware continue to evolve, these platforms are becoming more resilient, efficient, and versatile, pushing the boundaries of traditional naval engagement and setting new standards in maritime warfare effectiveness.

Key Drivers in Unmanned Surface and Underwater Vessels market:

The rise of unmanned surface and underwater vessels in defense strategy is propelled by multiple interrelated factors that underscore their strategic value. Foremost is the need to extend operational reach while minimizing the risk to personnel. These platforms can be deployed in high-threat zones, perform repetitive or hazardous tasks, and conduct long-endurance missions without fatigue. Strategic competition over maritime territories and underwater resources is also prompting nations to enhance their naval intelligence and surveillance capabilities. Unmanned vessels offer cost-effective solutions for persistent monitoring and can operate independently or as part of a broader system. The increasing threat of underwater mines and stealthy submarines has also led to a renewed focus on platforms capable of conducting detection and clearance without endangering manned vessels. Technological feasibility has made these systems more attractive, as improvements in autonomy, durability, and sensor integration have increased their reliability and mission success rates. Policy shifts toward distributed maritime operations further support the deployment of unmanned systems as force multipliers. They enable flexible response to a variety of scenarios, from deterrence to rapid crisis response. Ultimately, the convergence of strategic necessity, technological readiness, and operational efficiency is driving the global momentum behind the deployment of these advanced naval assets.

Regional Trends in Unmanned Surface and Underwater Vessels Market:

Regional approaches to defense unmanned surface and underwater vessels reflect diverse security priorities and technological investments. In the Indo-Pacific, maritime disputes and the protection of strategic waterways have driven aggressive development and deployment of both surface and sub-sea unmanned assets. Coastal surveillance, anti-intrusion missions, and maritime domain awareness are key focus areas for several nations in this region. North American forces are emphasizing the integration of these systems into large-scale naval exercises and fleet modernization programs, seeking to maintain an edge in long-range operations and undersea dominance. European nations are balancing innovation with collaborative frameworks, often pooling resources to develop interoperable platforms suitable for both national and allied missions. This cooperative model enables broader surveillance coverage and cost efficiency. Middle Eastern countries are increasingly turning to unmanned surface vehicles to monitor critical maritime infrastructure and shipping lanes, especially in areas with a history of sabotage and asymmetric threats. African and Latin American defense entities, while at earlier stages of adoption, are beginning to invest in these technologies for coastal security, anti-smuggling efforts, and environmental monitoring. Across all regions, the trend is clear: unmanned surface and underwater vessels are transitioning from experimental tools to vital components of modern naval defense, driven by specific regional imperatives and evolving maritime threats.

Key Defense Unmanned Surface and Underwater Vessels Program:

HII announced that its Mission Technologies division has been awarded a contract to produce nine small unmanned undersea vehicles (SUUVs) for the U.S. Navy's Lionfish System program. The agreement includes the potential for expansion to up to 200 vehicles over the next five years, with a total contract value exceeding $347 million. The Lionfish System is derived from HII's REMUS 300-a compact, two-person-deployable SUUV featuring an open architecture and flexible payload configurations. In early 2022, the REMUS 300 was designated as the Navy's official program of record for its next-generation SUUV platform. Managed by Naval Sea Systems Command, the contract covers the production and support of these advanced SUUVs, along with associated afloat and auxiliary support equipment and engineering services. The vehicles, equipped with cutting-edge autonomous and unmanned technologies, are intended to perform vital undersea missions for the Navy.

Table of Contents

Unmanned Surface and Underwater Vessels Market Report Definition

Unmanned Surface and Underwater Vessels Market Segmentation

By Region

By Application

By Mode of Operation

Unmanned Surface and Underwater Vessels Market Analysis for next 10 Years

The 10-year unmanned surface and underwater vessels market analysis would give a detailed overview of unmanned surface and underwater vessels market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Unmanned Surface and Underwater Vessels Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Unmanned Surface and Underwater Vessels Market Forecast

The 10-year unmanned surface and underwater vessels market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Unmanned Surface and Underwater Vessels Market Trends & Forecast

The regional unmanned surface and underwater vessels market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Unmanned Surface and Underwater Vessels Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Unmanned Surface and Underwater Vessels Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Unmanned Surface and Underwater Vessels Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2025-2035

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2025-2035

- Table 18: Scenario Analysis, Scenario 1, By Control, 2025-2035

- Table 19: Scenario Analysis, Scenario 1, By Application, 2025-2035

- Table 20: Scenario Analysis, Scenario 2, By Region, 2025-2035

- Table 21: Scenario Analysis, Scenario 2, By Control, 2025-2035

- Table 22: Scenario Analysis, Scenario 2, By Application, 2025-2035

List of Figures

- Figure 1: Global Unmanned Surface and Underwater Vessels Market Forecast, 2025-2035

- Figure 2: Global Unmanned Surface and Underwater Vessels Market Forecast, By Region, 2025-2035

- Figure 3: Global Unmanned Surface and Underwater Vessels Market Forecast, By Control, 2025-2035

- Figure 4: Global Unmanned Surface and Underwater Vessels Market Forecast, By Application, 2025-2035

- Figure 5: North America, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 6: Europe, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 7: Middle East, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 8: APAC, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 9: South America, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 10: United States, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 11: United States, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 12: Canada, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 13: Canada, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 14: Italy, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 15: Italy, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 16: France, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 17: France, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 18: Germany, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 19: Germany, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 20: Netherlands, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 21: Netherlands, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 22: Belgium, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 23: Belgium, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 24: Spain, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 25: Spain, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 26: Sweden, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 27: Sweden, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 28: Brazil, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 29: Brazil, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 30: Australia, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 31: Australia, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 32: India, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 33: India, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 34: China, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 35: China, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 36: Saudi Arabia, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 37: Saudi Arabia, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 38: South Korea, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 39: South Korea, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 40: Japan, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 41: Japan, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 42: Malaysia, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 43: Malaysia, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 44: Singapore, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 45: Singapore, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 46: United Kingdom, Unmanned Surface and Underwater Vessels Market, Technology Maturation, 2025-2035

- Figure 47: United Kingdom, Unmanned Surface and Underwater Vessels Market, Market Forecast, 2025-2035

- Figure 48: Opportunity Analysis, Unmanned Surface and Underwater Vessels Market, By Region (Cumulative Market), 2025-2035

- Figure 49: Opportunity Analysis, Unmanned Surface and Underwater Vessels Market, By Region (CAGR), 2025-2035

- Figure 50: Opportunity Analysis, Unmanned Surface and Underwater Vessels Market, By Control (Cumulative Market), 2025-2035

- Figure 51: Opportunity Analysis, Unmanned Surface and Underwater Vessels Market, By Control (CAGR), 2025-2035

- Figure 52: Opportunity Analysis, Unmanned Surface and Underwater Vessels Market, By Application (Cumulative Market), 2025-2035

- Figure 53: Opportunity Analysis, Unmanned Surface and Underwater Vessels Market, By Application (CAGR), 2025-2035

- Figure 54: Scenario Analysis, Unmanned Surface and Underwater Vessels Market, Cumulative Market, 2025-2035

- Figure 55: Scenario Analysis, Unmanned Surface and Underwater Vessels Market, Global Market, 2025-2035

- Figure 56: Scenario 1, Unmanned Surface and Underwater Vessels Market, Total Market, 2025-2035

- Figure 57: Scenario 1, Unmanned Surface and Underwater Vessels Market, By Region, 2025-2035

- Figure 58: Scenario 1, Unmanned Surface and Underwater Vessels Market, By Control, 2025-2035

- Figure 59: Scenario 1, Unmanned Surface and Underwater Vessels Market, By Application, 2025-2035

- Figure 60: Scenario 2, Unmanned Surface and Underwater Vessels Market, Total Market, 2025-2035

- Figure 61: Scenario 2, Unmanned Surface and Underwater Vessels Market, By Region, 2025-2035

- Figure 62: Scenario 2, Unmanned Surface and Underwater Vessels Market, By Control, 2025-2035

- Figure 63: Scenario 2, Unmanned Surface and Underwater Vessels Market, By Application, 2025-2035

- Figure 64: Company Benchmark, Unmanned Surface and Underwater Vessels Market, 2025-2035

海军舰艇和水面作战舰艇市场-全球产业规模、份额、趋势、机会及预测(按舰艇类型、系统类型、地区和竞争格局划分,2021-2031年)海军舰艇维护与修理市场-全球产业规模、份额、趋势、机会和预测:按舰艇类型、维护/修理类型、地区和竞争格局划分,2021-2031年

海军舰艇和水面作战舰艇市场-全球产业规模、份额、趋势、机会及预测(按舰艇类型、系统类型、地区和竞争格局划分,2021-2031年)海军舰艇维护与修理市场-全球产业规模、份额、趋势、机会和预测:按舰艇类型、维护/修理类型、地区和竞争格局划分,2021-2031年 2026-2030年全球海军舰艇市场

2026-2030年全球海军舰艇市场 海军舰艇和水面作战舰艇市场规模、份额和成长分析(按平台、系统、应用和地区划分)-2026-2033年产业预测

海军舰艇和水面作战舰艇市场规模、份额和成长分析(按平台、系统、应用和地区划分)-2026-2033年产业预测 2025-2029年全球海军舰艇MRO市场

2025-2029年全球海军舰艇MRO市场 管道铺设船的全球市场:各管线施工系统类型,水深,各地区,机会,预测,2018年~2032年管道铺设船市场-全球产业规模、份额、趋势、机会及预测(按安装类型、按定位系统、按深度、按地区及竞争情况细分,2020-2030 年)舰艇·水上战斗机的全球市场:各舰艇类型,各系统,各用途,各地区,机会,预测,2018年~2032年

管道铺设船的全球市场:各管线施工系统类型,水深,各地区,机会,预测,2018年~2032年管道铺设船市场-全球产业规模、份额、趋势、机会及预测(按安装类型、按定位系统、按深度、按地区及竞争情况细分,2020-2030 年)舰艇·水上战斗机的全球市场:各舰艇类型,各系统,各用途,各地区,机会,预测,2018年~2032年 全球海军舰艇市场:趋势、预测与竞争分析(至 2031 年)

全球海军舰艇市场:趋势、预测与竞争分析(至 2031 年) 海军舰艇市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测

海军舰艇市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测