|

市场调查报告书

商品编码

1684522

海军舰艇市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测Naval Vessels Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

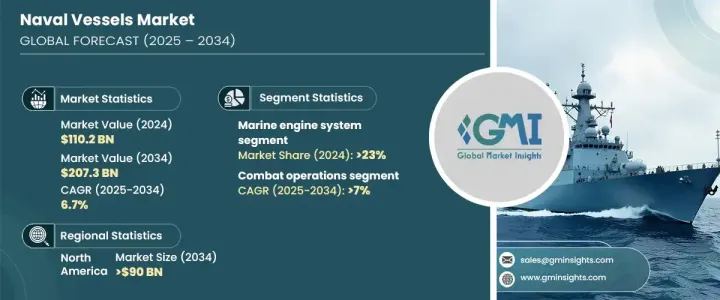

2024 年全球海军舰艇市场规模将达到 1102 亿美元,预计在 2025 年至 2034 年期间的复合年增长率为 6.7%。世界各国政府和国防组织正在大力投资尖端海军技术,以加强海上安全并应对不断演变的威胁。海军舰队的现代化,加上人工智慧(AI)、自主系统和先进推进技术的融合,正在重塑市场格局。日益加剧的地缘政治紧张局势和海洋领土争端进一步凸显了海军舰艇在国家安全战略中的关键作用。此外,向环保推进系统的转变表明了该行业对严格的环境法规的回应,强调永续性和营运效率。

市场依系统细分为船用引擎系统、武器发射系统、控制系统、电气系统、通讯系统等。其中,船用引擎系统部门在 2024 年占据了 23% 的市场份额,预计未来几年将大幅扩大。海军舰艇的推进技术正在迅速发展,明显转向混合动力和生物燃料驱动系统。这些技术将电动马达与传统燃料引擎结合在一起,符合环境要求,同时满足现代驱逐舰和潜艇的战术和作战需求。对节能係统的推动反映出人们越来越重视在不影响性能的情况下减少军事行动的碳足迹。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 1102亿美元 |

| 预测值 | 2073亿美元 |

| 复合年增长率 | 6.7% |

根据应用,市场分为沿海作业、搜救任务、作战行动、水雷对抗 (MCM) 作业等。作战行动领域预计将经历强劲成长,到 2034 年复合年增长率将达到 7%。这些技术增强了武器的射程、准确性和整体效能,为沿海地区及其他地区提供了卓越的防御能力。此外,人工智慧和自主技术的融合从根本上改变了海军作战,实现了快速威胁侦测、简化任务执行并增强了跨多个领域的态势感知。

北美仍然是海军舰艇市场的主要参与者,特别是在驱逐舰和潜艇领域。在美国注重提升海军能力的推动下,该地区预计到 2034 年将创造 900 亿美元的价值。美国继续在高超音速武器和自主系统方面投入大量资金,引领市场,确保战略主导地位和无与伦比的作战效率。海军舰艇市场的成长得益于国防投资的增加、推进技术的进步以及人工智慧和自主解决方案的日益普及,巩固了其在全球海上安全中的关键作用。

目录

第 1 章:方法论与范围

- 市场范围和定义

- 基础估算与计算

- 预测计算

- 资料来源

- 基本的

- 次要

- 付费来源

- 公共资源

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 供应商概况

- 利润率分析

- 重要新闻及倡议

- 监管格局

- 衝击力

- 成长动力

- 地缘政治紧张局势加剧和军事现代化

- 增加国防预算

- 潜舰战略防御需求不断成长

- 海上安全日益受关注

- 更加重视海军舰队多样化

- 产业陷阱与挑战

- 开发和维护成本高

- 地缘政治不稳定与监管限制

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:依船舶类型,2021-2034 年

- 主要趋势

- 驱逐舰

- 护卫舰

- 潜水艇

- 护卫舰

- 航空母舰

- 其他的

第 6 章:市场估计与预测:按系统,2021 年至 2034 年

- 主要趋势

- 船舶引擎系统

- 武器发射系统

- 控制系统

- 电气系统

- 通讯系统

- 其他的

第 7 章:市场估计与预测:按应用,2021 年至 2034 年

- 主要趋势

- 搜救

- 战斗行动

- 反水雷 (MCM) 行动

- 沿海作业

- 其他的

第 8 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中东及非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- Austal

- BAE Systems

- Damen Shipyards

- Fincantieri

- General Dynamics

- Hanwha Ocean

- HD Korea Shipbuilding

- Huntington Ingalls

- Larsen & Toubro

- Lockheed Martin

- Naval Group

- ThyssenKrupp

The Global Naval Vessels Market reached USD 110.2 billion in 2024 and is poised to grow at a CAGR of 6.7% between 2025 and 2034. This growth trajectory reflects the rising prevalence of security threats across the globe, which has led to an unprecedented surge in demand for advanced offensive and defensive weapon systems. Governments and defense organizations worldwide are investing heavily in cutting-edge naval technologies to strengthen their maritime security and address evolving threats. The modernization of naval fleets, combined with the integration of artificial intelligence (AI), autonomous systems, and advanced propulsion technologies, is reshaping the market landscape. Increasing geopolitical tensions and disputes over maritime territories further underscore the critical role of naval vessels in national security strategies. Additionally, the transition toward eco-friendly propulsion systems demonstrates the sector's response to stringent environmental regulations, emphasizing sustainability alongside operational efficiency.

The market is segmented by system into marine engine systems, weapon launch systems, control systems, electrical systems, communication systems, and others. Among these, the marine engine systems segment accounted for 23% of the market share in 2024 and is anticipated to expand significantly in the coming years. Propulsion technologies for naval vessels are advancing rapidly, with a notable shift toward hybrid and biofuel-driven systems. These technologies integrate electric motors with conventional fuel engines, aligning with environmental mandates while addressing the tactical and operational needs of modern destroyers and submarines. The push for energy-efficient systems reflects a growing emphasis on reducing the carbon footprint of military operations without compromising performance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $110.2 billion |

| Forecast Value | $207.3 billion |

| CAGR | 6.7% |

By application, the market is categorized into coastal operations, search and rescue missions, combat operations, Mine Countermeasures (MCM) operations, and others. The combat operations segment is expected to witness robust growth, registering a CAGR of 7% through 2034. Revolutionary advancements such as hypersonic missile technology, directed energy systems, and precision torpedoes are transforming the capabilities of naval combat forces. These technologies enhance weapon range, accuracy, and overall effectiveness, providing superior defense capabilities for coastal regions and beyond. Furthermore, the integration of AI and autonomous technologies has fundamentally changed naval operations, enabling rapid threat detection, streamlined mission execution, and enhanced situational awareness across multiple domains.

North America remains a key player in the naval vessels market, particularly in the destroyers and submarines segments. The region is projected to generate USD 90 billion in value by 2034, driven by the United States' focus on advancing naval capabilities. The U.S. continues to lead the market with substantial investments in hypersonic weapons and autonomous systems, ensuring strategic dominance and unmatched operational efficiency. The naval vessels market growth is fueled by rising defense investments, advancements in propulsion technologies, and the growing incorporation of AI and autonomous solutions, solidifying its critical role in global maritime security.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Growing geopolitical tensions and military modernization

- 3.6.1.2 Increasing defense budgets

- 3.6.1.3 Growing demand for submarine-based strategic defense

- 3.6.1.4 Rising focus on maritime security

- 3.6.1.5 Increased focus on naval fleet diversification

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High development and maintenance costs

- 3.6.2.2 Geopolitical instability and regulatory constraints

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vessel Type, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Destroyers

- 5.3 Frigates

- 5.4 Submarines

- 5.5 Corvettes

- 5.6 Aircraft carriers

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By System, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Marine engine system

- 6.3 Weapon launch system

- 6.4 Control system

- 6.5 Electrical system

- 6.6 Communication system

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Search and rescue

- 7.3 Combat operations

- 7.4 Mine countermeasures (MCM) operations

- 7.5 Coastal Operations

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Austal

- 9.2 BAE Systems

- 9.3 Damen Shipyards

- 9.4 Fincantieri

- 9.5 General Dynamics

- 9.6 Hanwha Ocean

- 9.7 HD Korea Shipbuilding

- 9.8 Huntington Ingalls

- 9.9 Larsen & Toubro

- 9.10 Lockheed Martin

- 9.11 Naval Group

- 9.12 ThyssenKrupp

海军舰艇和水面作战舰艇市场-全球产业规模、份额、趋势、机会及预测(按舰艇类型、系统类型、地区和竞争格局划分,2021-2031年)海军舰艇维护与修理市场-全球产业规模、份额、趋势、机会和预测:按舰艇类型、维护/修理类型、地区和竞争格局划分,2021-2031年

海军舰艇和水面作战舰艇市场-全球产业规模、份额、趋势、机会及预测(按舰艇类型、系统类型、地区和竞争格局划分,2021-2031年)海军舰艇维护与修理市场-全球产业规模、份额、趋势、机会和预测:按舰艇类型、维护/修理类型、地区和竞争格局划分,2021-2031年 2026-2030年全球海军舰艇市场

2026-2030年全球海军舰艇市场 海军舰艇和水面作战舰艇市场规模、份额和成长分析(按平台、系统、应用和地区划分)-2026-2033年产业预测

海军舰艇和水面作战舰艇市场规模、份额和成长分析(按平台、系统、应用和地区划分)-2026-2033年产业预测 2025-2029年全球海军舰艇MRO市场

2025-2029年全球海军舰艇MRO市场 管道铺设船的全球市场:各管线施工系统类型,水深,各地区,机会,预测,2018年~2032年

管道铺设船的全球市场:各管线施工系统类型,水深,各地区,机会,预测,2018年~2032年 无人水面载具(USV)·无人水下载具(UUV)的全球市场(2025年~2035年)管道铺设船市场-全球产业规模、份额、趋势、机会及预测(按安装类型、按定位系统、按深度、按地区及竞争情况细分,2020-2030 年)舰艇·水上战斗机的全球市场:各舰艇类型,各系统,各用途,各地区,机会,预测,2018年~2032年全球海军舰艇市场:趋势、预测与竞争分析(至 2031 年)

无人水面载具(USV)·无人水下载具(UUV)的全球市场(2025年~2035年)管道铺设船市场-全球产业规模、份额、趋势、机会及预测(按安装类型、按定位系统、按深度、按地区及竞争情况细分,2020-2030 年)舰艇·水上战斗机的全球市场:各舰艇类型,各系统,各用途,各地区,机会,预测,2018年~2032年全球海军舰艇市场:趋势、预测与竞争分析(至 2031 年)