|

市场调查报告书

商品编码

1896749

全球国防机器人与自动驾驶车辆市场(2026-2036)Global Defense Robots And Autonomous Vehicles Market 2026-2036 |

||||||

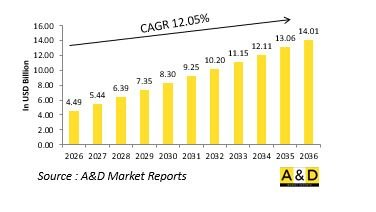

据估计,全球国防机器人和自动驾驶车辆市场在2026年的价值为44.9亿美元,预计到2036年将达到140.1亿美元,2026年至2036年的复合年增长率为12.05%。

国防机器人与自动驾驶车辆市场概述

国防机器人和自动驾驶车辆市场涵盖旨在以最小的人工干预执行复杂军事任务的无人系统。 这些系统可在空中、陆地和海上领域运行,执行侦察、后勤支援、监视、爆炸物处理和作战行动等任务。它们透过在衝突地区和危险环境中执行危险任务,增强部队防护并降低人员风险。将机器人和自主技术融入国防行动,反映了向数位化、网路化和精确作战的更广泛转变。世界各地的国防机构正在加速采用机器人平台,以提高作战效率、保持态势感知并扩大人力部队的作战范围。随着人工智慧 (AI) 和机器学习的不断成熟,自主防御系统正从远端操作工具演变为能够独立执行任务的智慧决策支援资产,从而重新定义现代军事战略的本质。

科技对国防机器人与自主车辆市场的影响:

在人工智慧、先进感测器和机器自主技术的推动下,科技正在深刻地改变国防机器人和自主车辆市场。 人工智慧驱动的导航和感知技术的突破使这些系统能够在复杂多变的环境中自主运作。增强的感测器融合技术能够无缝整合视觉、热成像和雷达数据,从而实现卓越的态势感知和目标识别能力。边缘运算和即时资料处理使自主平台能够在任务执行过程中做出瞬间决策,而无需依赖外部通讯链路。机器人设计的进步使得平台更加轻巧、灵活和节能,能够适应各种地形和任务需求。群体智慧和协作机器人技术是新兴趋势,使多个自主系统能够协同作战。网路安全和安全通讯协定也至关重要,确保系统能够抵御电子战和干扰。这些技术进步使机器人技术和自主系统成为未来国防能力的基础,从而实现精准性、适应性和作战可扩展性。

国防机器人与自主车辆市场的主要驱动因素:

国防机器人和自主车辆市场的成长主要受现代战争中对增强态势感知、部队防护和作战效率的需求所驱动。日益复杂的战场环境、城市作战环境以及不断增加的非对称威胁凸显了能够执行高风险任务的无人系统的价值。国防机构正在优先考虑自动化,以减少伤亡、提高任务连续性并优化后勤和侦察任务。人工智慧和自主技术在监视、作战支援和决策过程中的日益普及进一步推动了这些技术的应用。各国政府也将技术自主和机器人系统的国内研发作为其现代化计画的优先事项。电子战的兴起以及对更快、数据驱动型响应能力日益增长的需求正在推动对智慧连网机器人平台的投资。此外,民用机器人创新与国防应用的整合正在加速这些技术的应用,并塑造无人和自主军事行动的新时代。

国防机器人与自主车辆市场区域趋势:

国防机器人和自主车辆市场的区域趋势反映了各地区战略目标和技术能力的差异。北美地区持续投资于无人地面、空中和海上系统,并将先进的自主技术和人工智慧应用于联合部队作战,从而引领市场发展。欧洲则专注于合作式国防机器人项目,旨在开发用于监视、后勤和作战任务的互操作系统。亚太地区由于国防预算的增加以及对国内机器人技术发展的重视,正经历快速成长,以加强边境和海上监视。中东地区正在投资用于情报收集和基地防御的自主系统,以应对区域安全挑战。拉丁美洲和非洲正透过合作和技术转让,逐步部署用于边境监视和维和任务的无人系统。 在所有地区,建构自主防御能力、数位转型以及向下一代作战方式的迈进,都在加速将机器人和自主系统融入主流军事行动。

主要国防机器人与自主车辆项目:

美国陆军与国防创新部门 (DIU) 合作,已选定卡内基机器人公司 (Carnegie Robotics) 和 Forterra 公司推进自主运输车辆系统 (ATV-S) 的原型开发。 2023 年 12 月,陆军最初向三家供应商——机器人研究自主工业公司 (Robotics Research Autonomous Industries,现为 Forterra 公司)、Neya Systems 公司和卡内基机器人公司——授予总额为 1480 万美元的合同,用于分别开发四个原型。虽然这份新合约的细节(例如金额和条款)尚未披露,但此次选定将使通过初步筛选的原型进入陆军的正式测试和评估阶段。

目录

国防机器人与自动驾驶车辆市场 - 目录

国防机器人与自动驾驶车辆市场报告定义

国防机器人和自动驾驶车辆市场细分

按地区

按应用

按平台

未来十年国防机器人与自动驾驶车辆市场分析

本章将对未来十年国防机器人和自动驾驶车辆市场进行分析,详细概述市场成长、趋势变化、技术应用概况以及整体市场吸引力。

国防机器人与自动驾驶车辆市场技术展望

本部分讨论了预计将影响该市场的十大技术,以及这些技术可能对整体市场产生的影响。

全球国防机器人与自动驾驶车辆市场预测

以上各部分详细涵盖了未来十年的国防机器人和自动驾驶车辆市场预测。

区域国防机器人与自动驾驶车辆市场趋势及预测

本部分涵盖了区域国防机器人和自动驾驶车辆市场的趋势、驱动因素、限制因素和挑战,以及政治、经济、社会和技术因素。此外,本部分也提供了详细的区域市场预测和情境分析。区域分析最后包括主要公司概况、供应商状况和公司基准分析。目前市场规模是基于 "一切照旧" 情境估算的。

北美

驱动因素、限制因素与挑战

PEST分析

市场预测与情境分析

主要公司

供应商层级结构

公司标竿分析

欧洲

中东

亚太地区

南美洲

国防机器人与自动驾驶车辆市场国家分析

本章涵盖该市场的主要国防项目以及最新的市场新闻和专利申请。此外,本章也提供未来十年各国的市场预测和情境分析。

美国

国防项目

最新消息

专利

当前市场技术成熟度

市场预测与情境分析

加拿大

义大利

法国

德国

荷兰

比利时

西班牙

瑞典

希腊

澳洲

南非

印度

中国

俄罗斯

南非韩国

日本

马来西亚

新加坡

巴西

国防机器人与自动驾驶车辆市场机会矩阵

机会矩阵帮助读者了解该市场中高机会细分领域。

关于国防机器人和自动驾驶车辆市场报告的专家意见

本报告总结了我们专家对此市场潜力分析的意见。

结论

关于航空和国防市场报告

The Global Defense Robots and Autonomous Vehicles market is estimated at USD 4.49 billion in 2026, projected to grow to USD 14.01 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 12.05% over the forecast period 2026-2036.

Introduction to Defense Robots and Autonomous Vehicles Market

The defense robots and autonomous vehicles market encompasses unmanned systems designed to perform complex military tasks with minimal human intervention. These systems operate across air, land, and sea domains, executing missions such as reconnaissance, logistics support, surveillance, explosive ordnance disposal, and combat operations. They enhance force protection by performing dangerous tasks in contested or hazardous environments, reducing the risk to human personnel. The integration of robotics and autonomy into defense operations reflects a broader shift toward digitized, networked, and precision-oriented warfare. Defense organizations worldwide are increasingly adopting robotic platforms to boost operational efficiency, maintain situational awareness, and extend the reach of human forces. As artificial intelligence and machine learning continue to mature, autonomous defense systems are evolving from remote-controlled tools to intelligent, decision-supporting assets capable of independent mission execution, redefining the nature of modern military strategy.

Technology Impact in Defense Robots and Autonomous Vehicles Market:

Technology is profoundly transforming the defense robots and autonomous vehicles market through innovations in artificial intelligence, advanced sensors, and machine autonomy. Breakthroughs in AI-driven navigation and perception enable these systems to operate independently in complex and dynamic environments. Enhanced sensor fusion allows seamless integration of visual, thermal, and radar data for superior situational awareness and target identification. Edge computing and real-time data processing empower autonomous platforms to make split-second decisions during missions without relying on external communication links. Robotics design advancements have led to lighter, more agile, and energy-efficient platforms adaptable to multiple terrains and mission profiles. Swarm intelligence and collaborative robotics are emerging trends that allow multiple autonomous systems to coordinate actions in synchronized operations. Cybersecurity and secure communication protocols are also integral, ensuring resilience against electronic warfare and interference. These technological developments are positioning robotics and autonomy as the cornerstone of future defense capabilities, enabling precision, adaptability, and operational scalability.

Key Drivers in Defense Robots and Autonomous Vehicles Market:

The growth of the defense robots and autonomous vehicles market is driven by the need for enhanced situational awareness, force protection, and operational efficiency in modern warfare. Increasing battlefield complexity, urban combat environments, and asymmetric threats have underscored the value of unmanned systems capable of performing high-risk missions. Defense agencies are prioritizing automation to reduce human casualties, increase mission persistence, and optimize logistics and reconnaissance tasks. The expanding use of AI and autonomy in surveillance, combat support, and decision-making processes further fuels adoption. Governments are also emphasizing technological self-reliance and indigenous development of robotic systems as part of modernization programs. The rise of electronic warfare and the demand for faster, data-driven response capabilities encourage investment in intelligent and connected robotic platforms. Moreover, the growing convergence between civilian robotics innovations and defense applications is accelerating the pace of adoption, shaping a new era of unmanned and autonomous military operations.

Regional Trends in Defense Robots and Autonomous Vehicles Market:

Regional trends in the defense robots and autonomous vehicles market reflect varied strategic objectives and technological capabilities. North America leads through sustained investments in unmanned ground, aerial, and maritime systems, integrating advanced autonomy and AI into joint-force operations. Europe focuses on collaborative defense robotics programs aimed at developing interoperable systems for surveillance, logistics, and combat missions. The Asia-Pacific region is experiencing rapid growth, driven by rising defense budgets and emphasis on indigenous robotic development to enhance border security and maritime surveillance. The Middle East is investing in autonomous systems for intelligence gathering and base protection, addressing regional security challenges. Latin America and Africa are gradually adopting unmanned systems for border monitoring and peacekeeping missions through partnerships and technology transfers. Across all regions, the push toward self-reliant defense capabilities, digital transformation, and next-generation combat readiness is accelerating the integration of robotics and autonomy into mainstream military operations.

Key Defense Robots and Autonomous Vehicles Program:

The U.S. Army, in collaboration with the Defense Innovation Unit (DIU), has chosen Carnegie Robotics and Forterra to advance prototyping efforts for the Autonomous Transport Vehicle System (ATV-S). Initially, in December 2023, the Army awarded development and prototyping contracts to three vendors-Robotics Research Autonomous Industries (now Forterra), Neya Systems, and Carnegie Robotics-valued at $14.8 million for four prototypes each. While the specifics of the new contract, including its value and terms, have not been disclosed, this award represents a first down selection, moving the chosen prototypes into formal Army Test and Evaluation.

Table of Contents

Defense Robots And Autonomous Vehicles Market - Table of Contents

Defense Robots And Autonomous Vehicles Market Report Definition

Defense Robots And Autonomous Vehicles Market Segmentation

By Region

By Application

By Platform

Defense Robots And Autonomous Vehicles Market Analysis for next 10 Years

The 10-year Defense Robots And Autonomous Vehicles Market analysis would give a detailed overview of Defense Robots And Autonomous Vehicles Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Robots And Autonomous Vehicles Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Robots And Autonomous Vehicles Market Forecast

The 10-year Defense Robots And Autonomous Vehicles Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Robots And Autonomous Vehicles Market Trends & Forecast

The regional Defense Robots And Autonomous Vehicles Market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense Robots And Autonomous Vehicles Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Robots And Autonomous Vehicles Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Robots And Autonomous Vehicles Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2025-2035

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2025-2035

- Table 18: Scenario Analysis, Scenario 1, By Platform, 2025-2035

- Table 19: Scenario Analysis, Scenario 1, By Application, 2025-2035

- Table 20: Scenario Analysis, Scenario 2, By Region, 2025-2035

- Table 21: Scenario Analysis, Scenario 2, By Platform, 2025-2035

- Table 22: Scenario Analysis, Scenario 2, By Application, 2025-2035

List of Figures

- Figure 1: Global Defense Robots and Autonomous Vehicles Forecast, 2025-2035

- Figure 2: Global Defense Robots and Autonomous Vehicles Forecast, By Region, 2025-2035

- Figure 3: Global Defense Robots and Autonomous Vehicles Forecast, By Platform, 2025-2035

- Figure 4: Global Defense Robots and Autonomous Vehicles Forecast, By Application, 2025-2035

- Figure 5: North America, Defense Robots and Autonomous Vehicles, Market Forecast, 2025-2035

- Figure 6: Europe, Defense Robots and Autonomous Vehicles, Market Forecast, 2025-2035

- Figure 7: Middle East, Defense Robots and Autonomous Vehicles, Market Forecast, 2025-2035

- Figure 8: APAC, Defense Robots and Autonomous Vehicles, Market Forecast, 2025-2035

- Figure 9: South America, Defense Robots and Autonomous Vehicles, Market Forecast, 2025-2035

- Figure 10: United States, Defense Robots and Autonomous Vehicles, Technology Maturation, 2025-2035

- Figure 11: United States, Defense Robots and Autonomous Vehicles, Market Forecast, 2025-2035

- Figure 12: Canada, Defense Robots and Autonomous Vehicles, Technology Maturation, 2025-2035

- Figure 13: Canada, Defense Robots and Autonomous Vehicles, Market Forecast, 2025-2035

- Figure 14: Italy, Defense Robots and Autonomous Vehicles, Technology Maturation, 2025-2035

- Figure 15: Italy, Defense Robots and Autonomous Vehicles, Market Forecast, 2025-2035

- Figure 16: France, Defense Robots and Autonomous Vehicles, Technology Maturation, 2025-2035

- Figure 17: France, Defense Robots and Autonomous Vehicles, Market Forecast, 2025-2035

- Figure 18: Germany, Defense Robots and Autonomous Vehicles, Technology Maturation, 2025-2035

- Figure 19: Germany, Defense Robots and Autonomous Vehicles, Market Forecast, 2025-2035

- Figure 20: Netherlands, Defense Robots and Autonomous Vehicles, Technology Maturation, 2025-2035

- Figure 21: Netherlands, Defense Robots and Autonomous Vehicles, Market Forecast, 2025-2035

- Figure 22: Belgium, Defense Robots and Autonomous Vehicles, Technology Maturation, 2025-2035

- Figure 23: Belgium, Defense Robots and Autonomous Vehicles, Market Forecast, 2025-2035

- Figure 24: Spain, Defense Robots and Autonomous Vehicles, Technology Maturation, 2025-2035

- Figure 25: Spain, Defense Robots and Autonomous Vehicles, Market Forecast, 2025-2035

- Figure 26: Sweden, Defense Robots and Autonomous Vehicles, Technology Maturation, 2025-2035

- Figure 27: Sweden, Defense Robots and Autonomous Vehicles, Market Forecast, 2025-2035

- Figure 28: Brazil, Defense Robots and Autonomous Vehicles, Technology Maturation, 2025-2035

- Figure 29: Brazil, Defense Robots and Autonomous Vehicles, Market Forecast, 2025-2035

- Figure 30: Australia, Defense Robots and Autonomous Vehicles, Technology Maturation, 2025-2035

- Figure 31: Australia, Defense Robots and Autonomous Vehicles, Market Forecast, 2025-2035

- Figure 32: India, Defense Robots and Autonomous Vehicles, Technology Maturation, 2025-2035

- Figure 33: India, Defense Robots and Autonomous Vehicles, Market Forecast, 2025-2035

- Figure 34: China, Defense Robots and Autonomous Vehicles, Technology Maturation, 2025-2035

- Figure 35: China, Defense Robots and Autonomous Vehicles, Market Forecast, 2025-2035

- Figure 36: Saudi Arabia, Defense Robots and Autonomous Vehicles, Technology Maturation, 2025-2035

- Figure 37: Saudi Arabia, Defense Robots and Autonomous Vehicles, Market Forecast, 2025-2035

- Figure 38: South Korea, Defense Robots and Autonomous Vehicles, Technology Maturation, 2025-2035

- Figure 39: South Korea, Defense Robots and Autonomous Vehicles, Market Forecast, 2025-2035

- Figure 40: Japan, Defense Robots and Autonomous Vehicles, Technology Maturation, 2025-2035

- Figure 41: Japan, Defense Robots and Autonomous Vehicles, Market Forecast, 2025-2035

- Figure 42: Malaysia, Defense Robots and Autonomous Vehicles, Technology Maturation, 2025-2035

- Figure 43: Malaysia, Defense Robots and Autonomous Vehicles, Market Forecast, 2025-2035

- Figure 44: Singapore, Defense Robots and Autonomous Vehicles, Technology Maturation, 2025-2035

- Figure 45: Singapore, Defense Robots and Autonomous Vehicles, Market Forecast, 2025-2035

- Figure 46: United Kingdom, Defense Robots and Autonomous Vehicles, Technology Maturation, 2025-2035

- Figure 47: United Kingdom, Defense Robots and Autonomous Vehicles, Market Forecast, 2025-2035

- Figure 48: Opportunity Analysis, Defense Robots and Autonomous Vehicles, By Region (Cumulative Market), 2025-2035

- Figure 49: Opportunity Analysis, Defense Robots and Autonomous Vehicles, By Region (CAGR), 2025-2035

- Figure 50: Opportunity Analysis, Defense Robots and Autonomous Vehicles, By Platform (Cumulative Market), 2025-2035

- Figure 51: Opportunity Analysis, Defense Robots and Autonomous Vehicles, By Platform (CAGR), 2025-2035

- Figure 52: Opportunity Analysis, Defense Robots and Autonomous Vehicles, By Application (Cumulative Market), 2025-2035

- Figure 53: Opportunity Analysis, Defense Robots and Autonomous Vehicles, By Application (CAGR), 2025-2035

- Figure 54: Scenario Analysis, Defense Robots and Autonomous Vehicles, Cumulative Market, 2025-2035

- Figure 55: Scenario Analysis, Defense Robots and Autonomous Vehicles, Global Market, 2025-2035

- Figure 56: Scenario 1, Defense Robots and Autonomous Vehicles, Total Market, 2025-2035

- Figure 57: Scenario 1, Defense Robots and Autonomous Vehicles, By Region, 2025-2035

- Figure 58: Scenario 1, Defense Robots and Autonomous Vehicles, By Platform, 2025-2035

- Figure 59: Scenario 1, Defense Robots and Autonomous Vehicles, By Application, 2025-2035

- Figure 60: Scenario 2, Defense Robots and Autonomous Vehicles, Total Market, 2025-2035

- Figure 61: Scenario 2, Defense Robots and Autonomous Vehicles, By Region, 2025-2035

- Figure 62: Scenario 2, Defense Robots and Autonomous Vehicles, By Platform, 2025-2035

- Figure 63: Scenario 2, Defense Robots and Autonomous Vehicles, By Application, 2025-2035

- Figure 64: Company Benchmark, Defense Robots and Autonomous Vehicles, 2025-2035

自动驾驶汽车处理器市场:按处理器类型、车辆类型、销售管道和应用划分-2026-2032年全球市场预测

自动驾驶汽车处理器市场:按处理器类型、车辆类型、销售管道和应用划分-2026-2032年全球市场预测 Ultracruise 与城市自动驾驶市场机会、成长要素、产业趋势分析及 2026 年至 2035 年预测

Ultracruise 与城市自动驾驶市场机会、成长要素、产业趋势分析及 2026 年至 2035 年预测 全球自动驾驶汽车市场规模、份额、趋势和成长分析报告(2026-2034)全球自动驾驶汽车市场规模、份额、趋势和成长分析报告(2026-2034)

全球自动驾驶汽车市场规模、份额、趋势和成长分析报告(2026-2034)全球自动驾驶汽车市场规模、份额、趋势和成长分析报告(2026-2034) 2026-2030年全球L4级自动驾驶汽车市场按自主等级、推进方式、负载容量、车辆类型、应用和最终用户产业分類的全球自主物流车辆市场预测(2026-2032年)按营运模式、车辆类型、自动驾驶等级、所有权模式和应用程式分類的按需自动驾驶出行市场,全球预测,2026-2032年重型自主移动机器人市场:按导航技术、有效载荷能力、机器人类型、电池类型、环境、终端用户产业和应用划分-全球预测(2026-2032 年)

2026-2030年全球L4级自动驾驶汽车市场按自主等级、推进方式、负载容量、车辆类型、应用和最终用户产业分類的全球自主物流车辆市场预测(2026-2032年)按营运模式、车辆类型、自动驾驶等级、所有权模式和应用程式分類的按需自动驾驶出行市场,全球预测,2026-2032年重型自主移动机器人市场:按导航技术、有效载荷能力、机器人类型、电池类型、环境、终端用户产业和应用划分-全球预测(2026-2032 年) L4级自动驾驶汽车市场:按组件、车辆类型、动力系统、国家及地区划分-全球产业分析、市场规模、市场份额及2025-2032年预测

L4级自动驾驶汽车市场:按组件、车辆类型、动力系统、国家及地区划分-全球产业分析、市场规模、市场份额及2025-2032年预测 2032年自动驾驶合规系统市场预测:按合规类型、部署模式、车辆类型、技术、最终用户和地区分類的全球分析

2032年自动驾驶合规系统市场预测:按合规类型、部署模式、车辆类型、技术、最终用户和地区分類的全球分析