|

市场调查报告书

商品编码

1927662

全球航空航太与国防工业铜需求(2026-2036 年)Global Copper demand in Aerospace & Defense Industry 2026-2036 |

||||||

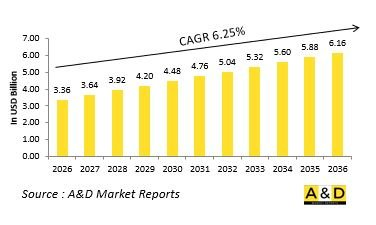

2026 年全球航空航太和国防工业铜需求预计为 33.6 亿美元,预计从 2026 年到 2036 年将以 6.25% 的复合年增长率增长,到 2036 年将达到 61.6 亿美元。

全球航空航太与国防工业铜需求概述

铜是航空航太和国防应用中的关键材料,因其优异的导电性和导热性、耐腐蚀性和机械强度而备受重视。 铜的应用范围十分广泛,涵盖飞机布线、配电系统、航空电子设备、雷达系统和通讯网路。在国防系统中,铜对于可靠的电子设备、感测器和飞弹系统至关重要,这些系统容不得任何故障。现代军事平台日益复杂的,包括无人机、电子战系统和卫星技术,正在推动对铜的需求。此外,在航空航太领域,铜对于商用和军用飞机的推进系统、能源管理和热控系统都至关重要。业界朝着更轻量化、更耐用和更高性能的方向发展,确保铜在提升运作效率和系统可靠性方面继续发挥核心作用。由于地缘政治因素会影响采购和提炼,供应链的稳定性是关键考虑因素。为了在控製成本和实现永续性的同时满足不断增长的需求,回收和替代采购策略变得越来越重要。总而言之,铜独特的性能、多功能性以及在关键任务系统中发挥的关键作用,使其成为现代航空航天和国防工业不可或缺的一部分,直接影响创新、系统性能和战略规划。

航空航太和国防工业中影响全球铜需求的技术因素

航空航太和国防系统的技术进步显着影响铜的需求,因为现代平台需要高性能的电气、热学和通讯组件。诸如电力推进、混合动力飞机系统、大容量储能和先进航空电子设备等新兴技术,正在提高对铜的数量和品质要求。电子战和雷达系统依靠铜来实现高效的信号传输和散热,而卫星通讯和天基感测器则依靠可靠的铜导体来不间断运作。积层製造和精密加工技术使得铜能够被加工成复杂的组件,从而在保持导电性和热性能的同时,提高了设计的灵活性。将铜整合到紧凑型电子设备和小型化系统中,符合飞机和国防平台朝向更轻、更有效率方向发展的趋势。材料科学的创新,包括铜合金和涂层,正在提高铜的耐腐蚀性、耐久性和在恶劣环境下的性能。国防电子设备的网路安全和可靠性也推动了对高品质铜组件的需求,以防止故障发生。随着新型推进、能源和感测器技术的不断发展,它们越来越依赖铜作为基础材料,而这些技术趋势正是航空航太和国防领域铜需求的关键驱动因素。

航空航太和国防工业铜需求的关键驱动因素

全球航空航太和国防领域的铜需求受多种因素驱动。随着包括无人机平台、雷达网路和通讯系统在内的飞机和国防系统日益复杂,高品质铜对于确保其可靠性能至关重要。电动和混合动力推进技术的日益普及,以及先进储能和电源管理解决方案的应用,进一步增加了对铜的需求。多个地区的国防现代化计划和采购项目,重点在于机队升级、整合先进电子设备和增强系统韧性,这些都进一步推动了铜的消耗。感测器系统、航空电子设备和卫星通讯技术的进步需要高精度铜组件。在关键系统中,可靠性、耐久性和热管理使得铜在风险较高的运作环境中至关重要。 供应链的考量,包括原物料采购和品质保证,都会影响采购和策略库存规划。此外,环境法规和永续发展措施推动了铜的回收和再利用,间接影响市场动态。营运需求、技术进步和战略国防优先事项的交汇,正在支撑铜需求的持续成长,巩固其作为航空航太和国防领域关键全球材料的地位。

航空航太与国防工业铜需求的区域趋势

航空航太和国防工业对铜的区域需求因工业基础、国防优先事项和技术应用而异。北美拥有强大的研发基础设施,强调高性能铜在先进飞机、无人系统和太空防御技术的应用。欧洲通常专注于将铜整合到多用途飞机、雷达网路和联合防御项目中,力求在性能和永续性之间取得平衡。亚太地区由于军事现代化项目的扩展、民用航空活动的增加以及本土航空航天技术的开发,正经历着快速增长。 中东国家优先将铜用于高科技国防系统,例如飞弹、监视平台和战略飞机,通常透过国际合作采购零件。非洲和南美市场呈现选择性成长,专注于在航空、海军和通讯系统中实现成本效益高的部署,同时逐步引入先进材料。电气化、小型化和网路化国防系统的趋势正在推动所有地区铜用量的成长。回收利用计画和安全的采购实践影响着区域策略,确保铜供应与长期营运和工业目标保持一致。工业能力、技术应用和战略重点的区域差异塑造了铜需求,同时也反映了全球航空航太和国防能力的进步。

航空航太和国防工业的主要铜需求项目:

美国国防后勤局 (DLA) 拨款 100 万美元用于铜业先进铸造技术开发。国防后勤局 (DLA) 为美国国防部的全球后勤需求提供支持,并为各军事司令部和联合作战司令部提供支援。 其使命是为全球美军提供经济高效、可靠的后勤保障,确保其在和平时期和战时都能保持战备状态。

目录

航空航太与国防市场铜零件 - 目录

航空航太与国防市场报告中铜部件的定义

航空航太与国防市场细分

按部件

按工艺

按地区

按合金

航空航太与国防市场铜零件未来十年分析

本章详细概述了航空航太与国防市场铜零件的市场成长、趋势变化、技术应用概况以及整体市场吸引力,并进行了未来十年的市场分析。

门禁控制市场技术概况

本部分讨论了预计将影响该市场的十大技术,以及这些技术可能对整体市场产生的影响。

全球门禁管制市场预测

以上各部分详细阐述了该市场未来十年的预测。

区域门禁管制市场趋势及预测

本部分涵盖区域门禁管制市场的趋势、驱动因素、限制因素、挑战以及政治、经济、社会和技术因素。此外,还提供了详细的区域市场预测和情境分析。最终的区域分析包括主要公司概况、供应商格局和公司基准分析。目前市场规模是基于 "一切照旧" 情境估算的。

北美

驱动因素、限制因素与挑战

PEST分析

市场预测与情境分析

主要公司

供应商层级结构

公司标竿分析

欧洲

中东

亚太地区

南美洲

门禁控制市场国家分析

本章涵盖该市场的主要国防项目以及最新的市场新闻和专利申请。此外,本章也提供未来十年各国的市场预测和情境分析。

美国

国防项目

最新消息

专利

当前市场技术成熟度

市场预测与情境分析

加拿大

义大利

法国

德国

荷兰

比利时

西班牙

瑞典

德国

澳洲

南非

印度

中国

俄罗斯

南非

韩国

日本

马来西亚

新加坡

巴西

门禁市场机会矩阵

机会矩阵帮助读者了解该市场中高机会细分领域。

专家对门禁市场报告的意见

本报告总结了我们专家对此市场分析潜力的意见。

结论

关于航空与国防市场报告

The Global Copper demand in Aerospace & Defense Industry market is estimated at USD 3.36 billion in 2026, projected to grow to USD 6.16 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 6.25% over the forecast period 2026-2036.

Introduction to Global Copper Demand in Aerospace & Defense Industry

Copper is a critical material in aerospace and defense applications, valued for its excellent electrical and thermal conductivity, corrosion resistance, and mechanical strength. Its widespread use spans aircraft wiring, power distribution systems, avionics, radar systems, and communication networks. In defense systems, copper is essential for high-reliability electronics, sensors, and missile systems where operational failure is not an option. The increasing complexity of modern military platforms, including unmanned aerial vehicles, electronic warfare systems, and satellite technologies, has intensified copper requirements. Additionally, the aerospace sector relies on copper for propulsion systems, energy management, and thermal control in both commercial and military aircraft. Industrial focus on lightweight, durable, and high-performance materials ensures that copper remains central to achieving operational efficiency and system reliability. Supply chain stability is a major consideration due to geopolitical factors affecting sourcing and refining. Recycling and alternative sourcing strategies are gaining importance to meet rising demand while managing cost and sustainability. Overall, copper's unique properties, versatility, and critical role in mission-critical systems make it indispensable for modern aerospace and defense industries, directly influencing technological innovation, system performance, and strategic planning.

Technology Impact in Global Copper Demand in Aerospace & Defense Industry

Technological advancements in aerospace and defense systems have significantly influenced the demand for copper, as modern platforms require high-performance electrical, thermal, and communication components. Emerging technologies such as electric propulsion, hybrid aircraft systems, high-capacity energy storage, and advanced avionics increase the volume and quality requirements for copper. Electronic warfare and radar systems rely on copper for efficient signal transmission and heat dissipation, while satellite communications and space-based sensors depend on reliable copper conductors for uninterrupted operations. Additive manufacturing and precision machining allow copper to be formed into complex components, enhancing design flexibility while maintaining conductivity and thermal performance. Integration of copper in compact electronics and miniaturized systems supports the trend toward lighter, more efficient aircraft and defense platforms. Materials science innovations, including copper alloys and coatings, improve corrosion resistance, durability, and performance under extreme conditions. Cybersecurity and reliability considerations in defense electronics further necessitate high-quality copper components to prevent failures. As new propulsion, energy, and sensor technologies evolve, the reliance on copper as a foundational material grows, making technological trends a central driver of its demand across aerospace and defense sectors.

Key Drivers in Copper Demand in Aerospace & Defense Industry

Several factors drive global copper demand in aerospace and defense sectors. The growing sophistication of aircraft and defense systems, including unmanned aerial platforms, radar networks, and communication systems, necessitates high-quality copper for reliable performance. Increasing adoption of electric and hybrid propulsion technologies, along with advanced energy storage and power management solutions, amplifies material requirements. Defense modernization initiatives and procurement programs in multiple regions focus on upgrading fleets, integrating advanced electronics, and enhancing system resilience, further boosting copper consumption. Technological progress in sensor systems, avionics, and satellite communications requires high-precision copper components. Reliability, durability, and thermal management in critical systems make copper indispensable in high-stakes operational environments. Supply chain considerations, including raw material sourcing and quality assurance, influence procurement and strategic inventory planning. Additionally, environmental regulations and sustainability initiatives encourage recycling and reuse of copper, indirectly affecting market dynamics. The intersection of operational necessity, technological evolution, and strategic defense priorities collectively underpins sustained growth in copper demand, reinforcing its status as a core material in aerospace and defense applications globally.

Regional Trends in Copper Demand in Aerospace & Defense Industry

Regional demand for copper in aerospace and defense varies according to industrial capabilities, defense priorities, and technological adoption. North America emphasizes high-performance copper for advanced aircraft, unmanned systems, and space-based defense technologies, driven by robust research and development infrastructure. Europe focuses on integrating copper in multi-role aircraft, radar networks, and collaborative defense programs, often balancing performance with sustainability considerations. Asia-Pacific demonstrates rapid growth due to expanding military modernization programs, increasing commercial aviation activity, and development of indigenous aerospace technologies. Middle Eastern nations prioritize copper for high-tech defense systems, including missiles, surveillance platforms, and strategic aircraft, often sourcing components through international partnerships. African and South American markets show selective growth, focusing on cost-efficient deployment in air, naval, and communication systems while gradually adopting advanced materials. Across all regions, trends in electrification, miniaturization, and networked defense systems drive higher copper utilization. Recycling initiatives and secure sourcing practices influence regional strategies, ensuring that copper availability aligns with long-term operational and industrial goals. Variations in regional industrial capacity, technological adoption, and strategic priorities shape copper demand while reflecting global advancements in aerospace and defense capabilities.

Key Copper demand in Aerospace & Defense Industry Program:

U.S. Defense Logistics Agency Allocates $1 Million to Copper Industry for Advanced Casting Technology. The Defense Logistics Agency supports the global logistics requirements of the U.S. Department of Defense, serving the Military Departments and Unified Combatant Commands. Its mission is to deliver cost-effective, reliable logistics support to U.S. Armed Forces worldwide, ensuring continuous readiness during both peacetime and conflict.

Table of Contents

Copper Component In The Aerospace And Defense Market - Table of Contents

Copper Component In The Aerospace And Defense Market Report Definition

Copper Component In The Aerospace And Defense Market Segmentation

By Component

By Process

By Region

By Alloy

Copper Component In The Aerospace And Defense Market Analysis for next 10 Years

The 10-year Copper Component In The Aerospace And Defense market analysis would give a detailed overview of Copper Component In The Aerospace And Defense market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Access Control Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Access Control Market Forecast

The 10-year access control market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Access Control Market Trends & Forecast

The regional access control market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Access Control Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Access Control Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Access Control Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Component, 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Alloy, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Region, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Component, 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Alloy, 2026-2036

List of Figures

- Figure 1: Global Copper Demand A&D Market Forecast, 2026-2036

- Figure 2: Global Copper Demand A&D Market Forecast, By Region, 2026-2036

- Figure 3: Global Copper Demand A&D Market Forecast, By Component, 2026-2036

- Figure 4: Global Copper Demand A&D Market Forecast, By Alloy, 2026-2036

- Figure 5: North America, Copper Demand A&D Market, Market Forecast, 2026-2036

- Figure 6: Europe, Copper Demand A&D Market, Market Forecast, 2026-2036

- Figure 7: Middle East, Copper Demand A&D Market, Market Forecast, 2026-2036

- Figure 8: APAC, Copper Demand A&D Market, Market Forecast, 2026-2036

- Figure 9: South America, Copper Demand A&D Market, Market Forecast, 2026-2036

- Figure 10: United States, Copper Demand A&D Market, Technology Maturation, 2026-2036

- Figure 11: United States, Copper Demand A&D Market, Market Forecast, 2026-2036

- Figure 12: Canada, Copper Demand A&D Market, Technology Maturation, 2026-2036

- Figure 13: Canada, Copper Demand A&D Market, Market Forecast, 2026-2036

- Figure 14: Italy, Copper Demand A&D Market, Technology Maturation, 2026-2036

- Figure 15: Italy, Copper Demand A&D Market, Market Forecast, 2026-2036

- Figure 16: France, Copper Demand A&D Market, Technology Maturation, 2026-2036

- Figure 17: France, Copper Demand A&D Market, Market Forecast, 2026-2036

- Figure 18: Germany, Copper Demand A&D Market, Technology Maturation, 2026-2036

- Figure 19: Germany, Copper Demand A&D Market, Market Forecast, 2026-2036

- Figure 20: Netherlands, Copper Demand A&D Market, Technology Maturation, 2026-2036

- Figure 21: Netherlands, Copper Demand A&D Market, Market Forecast, 2026-2036

- Figure 22: Belgium, Copper Demand A&D Market, Technology Maturation, 2026-2036

- Figure 23: Belgium, Copper Demand A&D Market, Market Forecast, 2026-2036

- Figure 24: Spain, Copper Demand A&D Market, Technology Maturation, 2026-2036

- Figure 25: Spain, Copper Demand A&D Market, Market Forecast, 2026-2036

- Figure 26: Sweden, Copper Demand A&D Market, Technology Maturation, 2026-2036

- Figure 27: Sweden, Copper Demand A&D Market, Market Forecast, 2026-2036

- Figure 28: Brazil, Copper Demand A&D Market, Technology Maturation, 2026-2036

- Figure 29: Brazil, Copper Demand A&D Market, Market Forecast, 2026-2036

- Figure 30: Australia, Copper Demand A&D Market, Technology Maturation, 2026-2036

- Figure 31: Australia, Copper Demand A&D Market, Market Forecast, 2026-2036

- Figure 32: India, Copper Demand A&D Market, Technology Maturation, 2026-2036

- Figure 33: India, Copper Demand A&D Market, Market Forecast, 2026-2036

- Figure 34: China, Copper Demand A&D Market, Technology Maturation, 2026-2036

- Figure 35: China, Copper Demand A&D Market, Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Copper Demand A&D Market, Technology Maturation, 2026-2036

- Figure 37: Saudi Arabia, Copper Demand A&D Market, Market Forecast, 2026-2036

- Figure 38: South Korea, Copper Demand A&D Market, Technology Maturation, 2026-2036

- Figure 39: South Korea, Copper Demand A&D Market, Market Forecast, 2026-2036

- Figure 40: Japan, Copper Demand A&D Market, Technology Maturation, 2026-2036

- Figure 41: Japan, Copper Demand A&D Market, Market Forecast, 2026-2036

- Figure 42: Malaysia, Copper Demand A&D Market, Technology Maturation, 2026-2036

- Figure 43: Malaysia, Copper Demand A&D Market, Market Forecast, 2026-2036

- Figure 44: Singapore, Copper Demand A&D Market, Technology Maturation, 2026-2036

- Figure 45: Singapore, Copper Demand A&D Market, Market Forecast, 2026-2036

- Figure 46: United Kingdom, Copper Demand A&D Market, Technology Maturation, 2026-2036

- Figure 47: United Kingdom, Copper Demand A&D Market, Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Copper Demand A&D Market, By Region (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Copper Demand A&D Market, By Region (CAGR), 2026-2036

- Figure 50: Opportunity Analysis, Copper Demand A&D Market, By Component (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Copper Demand A&D Market, By Component (CAGR), 2026-2036

- Figure 52: Opportunity Analysis, Copper Demand A&D Market, By Alloy (Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Copper Demand A&D Market, By Alloy (CAGR), 2026-2036

- Figure 54: Scenario Analysis, Copper Demand A&D Market, Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Copper Demand A&D Market, Global Market, 2026-2036

- Figure 56: Scenario 1, Copper Demand A&D Market, Total Market, 2026-2036

- Figure 57: Scenario 1, Copper Demand A&D Market, By Region, 2026-2036

- Figure 58: Scenario 1, Copper Demand A&D Market, By Component, 2026-2036

- Figure 59: Scenario 1, Copper Demand A&D Market, By Alloy, 2026-2036

- Figure 60: Scenario 2, Copper Demand A&D Market, Total Market, 2026-2036

- Figure 61: Scenario 2, Copper Demand A&D Market, By Region, 2026-2036

- Figure 62: Scenario 2, Copper Demand A&D Market, By Component, 2026-2036

- Figure 63: Scenario 2, Copper Demand A&D Market, By Alloy, 2026-2036

- Figure 64: Company Benchmark, Copper Demand A&D Market, 2026-2036

2026年全球铜磷合金市场研究报告

2026年全球铜磷合金市场研究报告 数控车床主轴市场:依主轴类型、轴配置、转速范围、轴承类型、安装方向、最终用户划分,全球预测,2026-2032年

数控车床主轴市场:依主轴类型、轴配置、转速范围、轴承类型、安装方向、最终用户划分,全球预测,2026-2032年 无机铜化学品市场规模、份额和成长分析:按产品类型、配方类型、最终用途产业、销售管道和地区划分-2026-2033年产业预测

无机铜化学品市场规模、份额和成长分析:按产品类型、配方类型、最终用途产业、销售管道和地区划分-2026-2033年产业预测 钴铜产品市场规模、份额和成长分析:按产品类型、形态、最终用途产业、电池应用、地区和产业预测,2026-2033年

钴铜产品市场规模、份额和成长分析:按产品类型、形态、最终用途产业、电池应用、地区和产业预测,2026-2033年 铜金属市场分析及预测(至2035年):依类型、产品、应用、形态、材质、最终用户、技术、功能、安装类型及设备划分

铜金属市场分析及预测(至2035年):依类型、产品、应用、形态、材质、最终用户、技术、功能、安装类型及设备划分 铜:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)

铜:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年) 2026年全球铜市场报告

2026年全球铜市场报告 铜板市场-全球产业规模、份额、趋势、机会和预测:按应用、销售管道、地区和竞争格局划分,2021-2031年

铜板市场-全球产业规模、份额、趋势、机会和预测:按应用、销售管道、地区和竞争格局划分,2021-2031年 2026-2030年全球铜市场全球银涂层铜粉市场(按粒径、颗粒形状、製造流程、包装类型、应用和最终用途行业划分)预测(2026-2032年)

2026-2030年全球铜市场全球银涂层铜粉市场(按粒径、颗粒形状、製造流程、包装类型、应用和最终用途行业划分)预测(2026-2032年)