|

市场调查报告书

商品编码

1936038

全球防空反导(AMD)市场(2026-2036)Global Air and Missile Defense Market 2026-2036 |

||||||

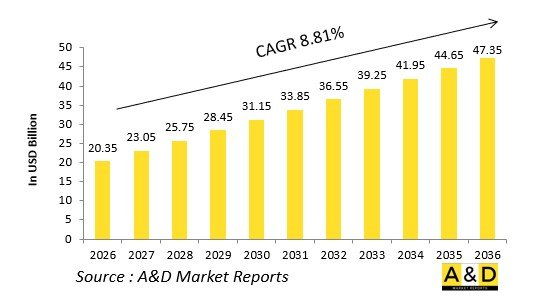

据估计,全球防空反导(AMD)市场在2026年的价值为203.5亿美元,预计到2036年将达到473.5亿美元,2026年至2036年的复合年增长率(CAGR)为8.81%。

引言

全球防空反导(AMD)市场是应对各种空中威胁(从短程火箭到洲际弹道飞弹)的战略威慑基础。整合架构将感测器、发射器和作战指挥系统分层部署,以侦测、追踪和消除入侵,从而保护民众、基础设施和部署部队。

市场动态反映了飞弹的扩散和高超音速技术的创新,推动了对可扩展和网路化防御系统的需求。核心要素包括地基拦截器、舰载垂直发射系统、空中预警和太空队列。製造商正在透过开放式系统设计进行创新,以实现快速升级,确保系统在技术变革浪潮中保持长久的使用寿命。

地缘政治竞争正在加速投资,各国正在加强多层防御以应对饱和攻击。互通性标准促进了联盟的形成,而军民两用技术则模糊了军用和民用之间的界线。在供应链中,弹性半导体和效应器推进系统是优先考虑的。竞争的焦点在于现有企业与利用人工智慧进行威胁识别的敏捷新进入者之间的较量。

防空反导(AMD)的发展与资讯优势密不可分,它融合了物理破坏和定向能攻击。这一市场代表高风险工程,在争夺激烈的空域,精准的时机把握能够避免灾难。

防空反导(AMD)的关键驱动因素

飞弹威胁的扩散正在推动防空反导(AMD)市场的发展。同侪竞争暴露了传统防御体系的脆弱性,促使人们建构多层防御体係以保护人员和资产。

战略威慑理念要求建立强大的防空反导态势,将联盟战区防御和国土防御结合。现代化势在必行的是为现有平台加装即插即用的感测器,以应对饱和攻击战术。

都市化进程的加速增加了附带风险,推动了低可观测性拦截器和精确导引武器的发展。随着中等强国获取包含训练和维护在内的多层次系统以威慑邻国,出口动力日益增强。

技术融合(人工智慧、太空和网路)凸显了对综合空中态势感知的需求,促进了反导系统与进攻性火力的整合。预算调整优先考虑高效发射器而非大规模部队。

永续性推动了定向能武器采用固态电源,从而减少了其后勤保障需求。联盟范围内的监理协调简化了联合研发流程。

从印太地区的紧张局势到欧洲週边地区的地缘政治热点,局势依然紧迫。两用技术创新正在吸引私人投资,并加速电磁轨道炮等进攻性武器的研发。

这些因素使反导系统成为可信力量投射的基石。

防空与飞弹防御(AMD)区域趋势

区域需求正在塑造防空与飞弹防御(AMD)市场。印太地区的紧张局势推动了海上防空与飞弹防御的发展,宙斯盾舰艇和岛基雷达正在应对高超音速飞弹的攻击。

在欧洲,北约框架内的防务整合正在推进,重点发展移动式防空系统和北极週边一体化防空体系。

在中东,各国正在部署密集的点基防空系统以应对集中的火箭弹袭击,并高度重视配备本地製造补偿装置的快速反应发射器。

本报告对全球防空与飞弹防御(AMD)市场进行了考察和分析,提供了影响该市场的技术资讯、未来十年的预测以及区域趋势。

目录

防空反导 (AMD) 市场报告定义

防空反导 (AMD) 市场区隔

依地区

依类型

依最终使用者

未来十年防空反导 (AMD) 市场分析

防空反导 (AMD) 市场技术

全球防空反导 (AMD) 市场预测

区域防空反导 (AMD) 市场趋势及预测

北美

驱动因素、限制因素与挑战

PEST 分析

市场预测及情境分析

主要公司

供应商等级

公司基准分析

欧洲

中东

亚太地区

南美洲

防空与飞弹防御 (AMD) 市场趋势与预测

美国

国防项目

最新消息

专利

该市场的当前技术成熟度

市场预测与情境分析

加拿大

义大利

法国

德国

荷兰

比利时

西班牙

瑞典

希腊

澳洲

南非

印度

中国

俄罗斯

韩国

日本

马来西亚

新加坡

巴西

防空反导(AMD)市场机会矩阵

防空反导(AMD)市场专家意见

结论

关于航空和国防市场报告

The Global Air and Missile Defense Market is estimated at USD 20.35 billion in 2026, projected to grow to USD 47.35 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 8.81% over the forecast period 2026-2036.

Introduction

The global Air and Missile Defense (AMD) market forms the backbone of strategic deterrence, countering diverse aerial threats from short-range rockets to intercontinental ballistic missiles. Integrated architectures layer sensors, launchers, and battle managers to detect, track, and neutralize incursions, protecting populations, infrastructure, and deployed forces.

Market dynamics reflect escalating missile proliferation and hypersonic innovations, driving demand for scalable, networked defenses. Core elements encompass ground-based interceptors, naval vertical launch systems, airborne early warning, and space-based cueing. Manufacturers innovate with open-system designs for rapid upgrades, ensuring longevity amid technological leaps.

Geopolitical rivalries amplify investments, as nations fortify layered shields against saturation attacks. Interoperability standards enable allied coalitions, while dual-use technologies blur civilian-military lines. Supply chains prioritize resilient semiconductors and propulsion for effectors. Competitive arenas pit incumbents against agile disruptors leveraging AI for threat discrimination.

AMD evolution intertwines with information dominance, fusing kinetic kills with directed energy. This market epitomizes high-stakes engineering, where precision timing averts catastrophe in contested skies.

Technology Impact in Air and Missile Defense

Technological breakthroughs propel Air and Missile Defense (AMD) into a new era of precision and adaptability. Hypersonic glide vehicle interceptors demand solid-state radars with gallium nitride amplifiers, extending detection envelopes against maneuvering targets. AI-driven fusion centers process petabytes from multi-spectral sensors, enabling autonomous salvo management and decoy rejection.

Directed-energy weapons-lasers and microwaves-offer speed-of-light engagements with deep magazines, ideal for drone swarms and cruise missiles. Quantum sensors enhance precision tracking in cluttered environments, while space-based infrared detectors provide persistent global cueing.

Network-centric architectures link terrestrial, naval, airborne, and orbital nodes via secure 5G meshes, creating kill webs that distribute intercepts dynamically. Modular open-system approaches accelerate effector swaps, from hit-to-kill vehicles to net-centric warheads.

Cyber-hardened command systems resist jamming, incorporating blockchain for tamper-proof data sharing. Hypersonic boost-glide countermeasures evolve with scramjet-powered interceptors. Digital engineering twins simulate mega-engagements, slashing development cycles.

These advancements compress decision loops, boost kill probabilities, and expand battlespace awareness, redefining AMD as proactive offense in defensive guise.

Key Drivers in Air and Missile Defense

Proliferating missile threats ignite the Air and Missile Defense (AMD) market. Advanced ballistic and hypersonic arsenals from peer competitors expose gaps in legacy shields, spurring layered architectures for population and asset protection.

Strategic deterrence doctrines mandate robust AMD postures, integrating theater and homeland defense amid alliance commitments. Modernization imperatives retrofit platforms with plug-and-play sensors, countering saturation tactics.

Urbanization heightens collateral stakes, driving low-observable interceptors and precision effectors. Export dynamics flourish as middle powers acquire tiered systems to deter neighbors, bundled with training and sustainment.

Technological convergence-AI, space, cyber-amplifies needs for integrated air pictures, fusing AMD with offensive fires. Budget realignments prioritize high-leverage effectors over massed forces.

Sustainability pushes solid-state power for directed energy, reducing logistics footprints. Regulatory harmonization across coalitions streamlines co-development.

Geopolitical hotspots sustain urgency, from Indo-Pacific tensions to European flanks. Dual-use innovations attract commercial investment, accelerating effectors like railguns.

These drivers cement AMD as cornerstone of credible power projection.

Regional Trends in Air and Missile Defense

Regional imperatives sculpt the Air and Missile Defense (AMD) market. Indo-Pacific tensions propel sea-based AMD, with Aegis-like ships and island-chain radars countering hypersonic salvos.

Europe unifies defenses via NATO frameworks, emphasizing mobile batteries and integrated air defense for high-north flanks.

Middle East deploys dense point defenses against rocket barrages, favoring quick-reaction launchers with local production offsets.

North America pioneers space-layering and directed energy, leveraging vast test ranges for hypersonic validations.

Russia bolsters S-500 equivalents for multi-layered shields against stealth incursions.

South Asia invests in ballistic missile defenses tied to nuclear postures, blending imports with indigenous radars.

Latin America focuses tiered systems for narco-drone threats, prioritizing cost-effective maritime patrols.

Africa adopts man-portable air defense integrated with counter-UAS for peacekeeping.

Global trends favor cloud-based command for coalition ops, with supply chains diversifying to Asia for effectors. Export controls shape tech flows, while alliances drive co-production.

Key Air and Missile Defense Programs

Iconic programs define Air and Missile Defense (AMD) trajectories. Ground-based midcourse systems intercept ICBMs in exo-atmosphere, leveraging boost-phase cueing from satellites.

Naval ballistic missile defense evolves Aegis baselines with hypersonic upgrades, deploying from destroyers in distributed fleets.

Patriot successors introduce modular radars and gallium nitride seekers for cruise missile barrages.

European Sky Shield initiatives harmonize short-range batteries across borders, incorporating drones as forward sensors.

Indo-Pacific allies develop common missile architectures for archipelago defense.

Directed-energy roadmaps mature shipboard lasers for drone interdiction, scaling to boost-phase kills.

Space-based intercept layers prototype hit-to-kill vehicles launched from orbit.

Mobile tactical AMD outfits Stryker brigades with counter-UAS effectors.

Export programs like Iron Dome variants adapt for urban rocket defense, with tech transfers.

Hypersonic defense testbeds validate scramjet interceptors against glide vehicles.

These efforts forge resilient webs, blending kinetic, electronic, and energetic means for all-domain protection.

Table of Contents

Air and Missile Defense Market - Table of Contents Air and Missile Defense Market Report Definition

Air and Missile Defense Market Segmentation

By Region

By Type

By End User

Air and Missile Defense Market Analysis for next 10 Years

The 10-year air and missile defense market analysis would give a detailed overview of air and missile defense market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Air and Missile Defense Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Air and Missile Defense Market Forecast

The 10-year air and missile defense market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Air and Missile Defense Market Trends & Forecast

The regional air and missile defense market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Air and Missile Defense Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Air and Missile Defense Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Air and Missile Defense Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Platform, 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Type, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Region, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Platform, 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Type, 2026-2036

List of Figures

- Figure 1: Global Air and Missile Defense Market Forecast, 2026-2036

- Figure 2: Global Air and Missile Defense Market Forecast, By Region, 2026-2036

- Figure 3: Global Air and Missile Defense Market Forecast, By Platform, 2026-2036

- Figure 4: Global Air and Missile Defense Market Forecast, By Type, 2026-2036

- Figure 5: North America, Air and Missile Defense Market, Forecast, 2026-2036

- Figure 6: Europe, Air and Missile Defense Market, Forecast, 2026-2036

- Figure 7: Middle East, Air and Missile Defense Market, Forecast, 2026-2036

- Figure 8: APAC, Air and Missile Defense Market, Forecast, 2026-2036

- Figure 9: South America, Air and Missile Defense Market, Forecast, 2026-2036

- Figure 10: United States, Air and Missile Defense Market, Technology Maturation, 2026-2036

- Figure 11: United States, Air and Missile Defense Market, Forecast, 2026-2036

- Figure 12: Canada, Air and Missile Defense Market, Technology Maturation, 2026-2036

- Figure 13: Canada, Air and Missile Defense Market, Forecast, 2026-2036

- Figure 14: Italy, Air and Missile Defense Market, Technology Maturation, 2026-2036

- Figure 15: Italy, Air and Missile Defense Market, Market Forecast, 2026-2036

- Figure 16: France, Air and Missile Defense Market, Technology Maturation, 2026-2036

- Figure 17: France, Air and Missile Defense Market, Market Forecast, 2026-2036

- Figure 18: Germany, Air and Missile Defense Market, Technology Maturation, 2026-2036

- Figure 19: Germany, Air and Missile Defense Market, Market Forecast, 2026-2036

- Figure 20: Netherlands, Air and Missile Defense Market, Technology Maturation, 2026-2036

- Figure 21: Netherlands, Air and Missile Defense Market, Market Forecast, 2026-2036

- Figure 22: Belgium, Air and Missile Defense Market, Technology Maturation, 2026-2036

- Figure 23: Belgium, Air and Missile Defense Market, Market Forecast, 2026-2036

- Figure 24: Spain, Air and Missile Defense Market, Technology Maturation, 2026-2036

- Figure 25: Spain, Air and Missile Defense Market, Market Forecast, 2026-2036

- Figure 26: Sweden, Air and Missile Defense Market, Technology Maturation, 2026-2036

- Figure 27: Sweden, Air and Missile Defense Market, Market Forecast, 2026-2036

- Figure 28: Brazil, Air and Missile Defense Market, Technology Maturation, 2026-2036

- Figure 29: Brazil, Air and Missile Defense Market, Market Forecast, 2026-2036

- Figure 30: Australia, Air and Missile Defense Market, Technology Maturation, 2026-2036

- Figure 31: Australia, Air and Missile Defense Market, Market Forecast, 2026-2036

- Figure 32: India, Air and Missile Defense Market, Technology Maturation, 2026-2036

- Figure 33: India, Air and Missile Defense Market, Market Forecast, 2026-2036

- Figure 34: China, Air and Missile Defense Market, Technology Maturation, 2026-2036

- Figure 35: China, Air and Missile Defense Market, Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Air and Missile Defense Market, Technology Maturation, 2026-2036

- Figure 37: Saudi Arabia, Air and Missile Defense Market, Market Forecast, 2026-2036

- Figure 38: South Korea, Air and Missile Defense Market, Technology Maturation, 2026-2036

- Figure 39: South Korea, Air and Missile Defense Market, Market Forecast, 2026-2036

- Figure 40: Japan, Air and Missile Defense Market, Technology Maturation, 2026-2036

- Figure 41: Japan, Air and Missile Defense Market, Market Forecast, 2026-2036

- Figure 42: Malaysia, Air and Missile Defense Market, Technology Maturation, 2026-2036

- Figure 43: Malaysia, Air and Missile Defense Market, Market Forecast, 2026-2036

- Figure 44: Singapore, Air and Missile Defense Market, Technology Maturation, 2026-2036

- Figure 45: Singapore, Air and Missile Defense Market, Market Forecast, 2026-2036

- Figure 46: United Kingdom, Air and Missile Defense Market, Technology Maturation, 2026-2036

- Figure 47: United Kingdom, Air and Missile Defense Market, Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Air and Missile Defense Market, By Region (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Air and Missile Defense Market, By Region (CAGR), 2026-2036

- Figure 50: Opportunity Analysis, Air and Missile Defense Market, By Platform (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Air and Missile Defense Market, By Platform (CAGR), 2026-2036

- Figure 52: Opportunity Analysis, Air and Missile Defense Market, By Type (Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Air and Missile Defense Market, By Type (CAGR), 2026-2036

- Figure 54: Scenario Analysis, Air and Missile Defense Market, Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Air and Missile Defense Market, Global Market, 2026-2036

- Figure 56: Scenario 1, Air and Missile Defense Market, Total Market, 2026-2036

- Figure 57: Scenario 1, Air and Missile Defense Market, By Region, 2026-2036

- Figure 58: Scenario 1, Air and Missile Defense Market, By Platform, 2026-2036

- Figure 59: Scenario 1, Air and Missile Defense Market, By Type, 2026-2036

- Figure 60: Scenario 2, Air and Missile Defense Market, Total Market, 2026-2036

- Figure 61: Scenario 2, Air and Missile Defense Market, By Region, 2026-2036

- Figure 62: Scenario 2, Air and Missile Defense Market, By Platform, 2026-2036

- Figure 63: Scenario 2, Air and Missile Defense Market, By Type, 2026-2036

- Figure 64: Company Benchmark, Air and Missile Defense Market, 2026-2036

防空作战市场:2026-2032年全球市场预测(依产品类型、交战范围、导引系统、平台类型、系统组件、应用和最终用户划分)

防空作战市场:2026-2032年全球市场预测(依产品类型、交战范围、导引系统、平台类型、系统组件、应用和最终用户划分) 全球防务一体化舰桥系统 (IBS) 市场 (2026-2036)

全球防务一体化舰桥系统 (IBS) 市场 (2026-2036) 飞弹防御系统市场-全球产业规模、份额、趋势、机会和预测,按射程、威胁类型、领域、地区和竞争格局划分,2020-2030年预测

飞弹防御系统市场-全球产业规模、份额、趋势、机会和预测,按射程、威胁类型、领域、地区和竞争格局划分,2020-2030年预测 全球综合防空反导市场(依系统、组件、范围、最终用户和地区划分)-预测至2030年战域防卫系统的全球市场(2025年~2035年)

全球综合防空反导市场(依系统、组件、范围、最终用户和地区划分)-预测至2030年战域防卫系统的全球市场(2025年~2035年) 世界及美国的整合型防空飞弹防御市场:预测(2024年~2030年)

世界及美国的整合型防空飞弹防御市场:预测(2024年~2030年) 防空作战市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测

防空作战市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测 飞弹及飞弹防御系统 (MMDS) 的全球市场:2024-2034年

飞弹及飞弹防御系统 (MMDS) 的全球市场:2024-2034年 亚太飞弹追踪系统市场:按应用、按平台、按国家:分析与预测(2023-2033)

亚太飞弹追踪系统市场:按应用、按平台、按国家:分析与预测(2023-2033)