|

市场调查报告书

商品编码

1936048

全球防务可变排气喷嘴市场:2026-2036Global Defense Variable Exhaust Nozzles Market 2026-2036 |

||||||

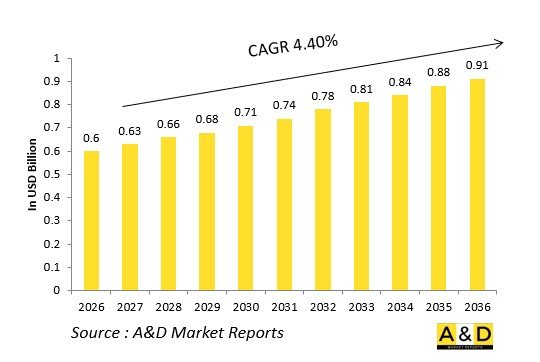

据估计,全球国防可变排气喷嘴市场在2026年的价值为6亿美元,预计到2036年将达到9.1亿美元,2026年至2036年的复合年增长率为4.40%。

引言

全球防务可变排气喷嘴市场透过液压或电动致动器驱动的瓣片来调节排气面积和方向,从而提高战术飞机的性能。 收敛-发散喉道加速加力燃烧室气流,而铰接式襟翼则为失速后机动和短距起飞提供推力向量控制。

市场动态反映了第六代战斗机的需求。冷却蒙皮和V形结构使喷嘴能够在加力燃烧室最大膨胀期间平衡红外线抑制。核心技术包括重迭式花瓣密封、蒸发冷却以及用于全权限数位引擎控制系统(FADEC)连锁调度的无缝干/湿过渡。低可观测性锯齿设计与飞机蒙皮融合。

争夺空中优势的地缘政治竞争推动了研发,优先考虑模组化作动器以实现机队的快速升级。开放式架构允许在不改变核心设计的情况下进行隐身改装。供应链着重于耐火高温合金和陶瓷基复合材料。在竞争方面,普惠公司、罗尔斯·罗伊斯公司和通用电气公司正在率先开发3D列印连桿。

技术对国防可变排气喷嘴市场的影响

采用独立上下驱动机构的二维喷嘴可实现无俯仰配平阻力的俯仰向量控制,从而实现无炮管设计。冷却式花瓣蒙皮采用薄膜冷却孔控制涡轮气流,在维持隐身外形的同时,还能承受加力燃烧室火焰稳定器的衝击。

电动致动器取代了液压系统,显着降低了脆弱性,同时实现了在整个马赫数范围内精确的喉部调节。形状记忆合金在加热时会收缩,从而实现自驱动扩散。等离子致动器消除了机械间隙,并降低了雷达反射截面。

从喷嘴蒙皮展开的自适应V形结构可混合旁通空气,在不损失推力的情况下抑制喷射引擎的红外线特征。数位孪生技术优化了花瓣轨迹,以减少热颤振。单晶花瓣前缘可在持续加压过程中抵抗氧化。

FADEC融合技术可同步控制喷嘴面积和进气口倾角,防止引擎在突然减速时启动失败。 3D列印的晶格结构在保持刚性的同时减轻了致动器重量。这些创新实现了更长的超音速巡航航程、更精确的推力向量角和无尾稳定性。

国防领域可变排气喷嘴市场的主要驱动因素

第六代隐形飞机需要与飞机无缝融合且能实现推力向量控制的低可观测性喷嘴。超音速巡航要求精确控制喉部,以防止过度膨胀激波的产生。

维护成本方面,电动致动器更受青睐,因为它能最大限度地减少液压洩漏。出口市场需要适用于各种加力燃烧循环的模组化喷嘴片。航空母舰作战优先考虑弹射起飞期间可靠的喷嘴分离。

预算压力促使人们选择3D列印喷嘴,因为它可以降低模具成本。 为了增强供应链韧性,钛短缺问题正透过合金替代来解决。互通性使得联军可以使用通用作动器。

失速后机动性需要独立于控制面的俯仰控制。这些要求使得可变尾喷管成为提高机动性的关键。

国防可变尾喷管市场区域趋势

北美率先在下一代战斗机 (NGAD) 中采用二维/轴对称混合式可变尾喷管,并强调电动动作。

欧洲正在为其颱风和阵风战斗机升级冷却式V形喷管,以实现分散部署。

亚太地区的自主研发正在加速。印度的AMCA和中国的歼-35均设计用于舰载发射。

中东正在研发用于昼夜拦截的烟雾混合喷嘴。

俄罗斯正在研发高温花瓣喷嘴,以提升苏-57的超机动性。

韩国正在整合KF-21的出口版本。

等离子驱动设计正逐渐成为主流。亚太地区正在扩大其製造占有率。

(196字)

主要国防可变尾喷管市场项目

F-22的2D喷嘴采用液压蚌壳结构,可实现±20°的俯仰角向量推力控制。

新一代战斗机(NGAD)的自适应喷嘴计画与第三代引擎核心有所不同。

改良型的EJ200引擎将配备可移动的级联式推力叶片,用于超音速巡航。

印度的AMCA战斗机将配备国产的二维向量推力系统,用于航空母舰作战。

WS-15 J-20引擎的喷嘴采用可伸缩的V形结构,以减少尾焰。

阵风M88战斗机的喷嘴整合了斯奈克玛核心,用于滑跃起飞/拦阻起飞(STOBAR)作业。

苏-57战斗机的三维推力向量系统使其能够进行普加乔夫眼镜蛇机动。

T-50战斗机的全权限数位引擎控制系统(FADEC)驱动的脚蹬作动机构可在失速后保持姿态角。

目录

国防可变排气喷嘴市场 - 目录

国防可变排气喷嘴市场报告定义

国防可变排气喷嘴市场区隔

依平台

依喷嘴型

依驱动方式

未来十年国防可变排气喷嘴市场分析

本章将详细分析未来十年国防可变排气喷嘴市场的成长、趋势变化、技术应用概况以及整体市场吸引力。

国防可变排气喷嘴市场技术概况

本部分讨论了预计将影响该市场的十大技术,以及这些技术可能对整体市场产生的影响。

全球国防可变排气喷嘴市场预测

以上各部分详细涵盖了该市场未来十年的国防可变排气喷嘴市场预测。

区域国防可变排气喷嘴市场趋势及预测

本部分涵盖了区域反无人机市场的趋势、驱动因素、限制因素、挑战以及政治、经济、社会和技术因素。此外,还提供了详细的区域市场预测和情境分析。最终的区域分析包括主要公司概况、供应商状况和公司基准分析。目前市场规模是基于一切照旧情境估算的。

北美

驱动因素、限制因素与挑战

PEST分析

市场预测与情境分析

主要公司

供应商层级结构

公司标竿分析

欧洲

中东

亚太地区

南美洲

国防可变排气喷嘴市场国家分析

本章涵盖该市场的主要国防项目以及最新的市场动态和专利申请资讯。此外,本章也提供未来十年各国的市场预测和情境分析。

美国

国防项目

最新消息

专利

当前市场技术成熟度

市场预测与情境分析

加拿大

义大利

法国

德国

荷兰

比利时

西班牙

瑞典

希腊

澳洲

南非

印度

中国

俄罗斯

南非

韩国

日本

马来西亚

新加坡

巴西

国防可变排气喷嘴市场机会矩阵

机会矩阵帮助读者了解该市场中高机会细分领域。

关于国防可变排气喷嘴市场报告的专家意见

本报告总结了我们专家对此市场分析潜力的意见。

结论

关于航空与国防市场报告

The Global Defense Variable Exhaust Nozzles Market is estimated at USD 0.6 billion in 2026, projected to grow to USD 0.91 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 4.40% over the forecast period 2026-2036.

Introduction

The global Defense Variable Exhaust Nozzles market enhances tactical aircraft performance, modulating exhaust area and direction via hydraulic or electric actuators translating petal segments. Convergent-divergent throats accelerate post-combustor flow, while articulated flaps vector thrust for post-stall maneuvers and short takeoffs.

Market dynamics reflect sixth-generation requirements, where nozzles balance peak afterburner expansion with infrared suppression through cooled skins and chevrons. Core technologies include petal overlap seals, transpirational cooling, and FADEC-linked scheduling for seamless dry-to-wet transitions. Emphasis on low-observable serrations integrates with aircraft skins.

Geopolitical air dominance competitions drive development, prioritizing modular actuators for rapid fleet upgrades. Open architectures enable stealth retrofits without core redesigns. Supply chains focus on refractory superalloys and ceramic matrix composites. Competition features Pratt & Whitney, Rolls-Royce, and GE pioneering 3D-printed linkages.

Technology Impact in Defense Variable Exhaust Nozzles Market

2D nozzles with independent upper/lower actuators deliver pitch vectoring without pitch trim drag, enabling canardless designs. Cooled petal skins employ film cooling holes metering turbine air to withstand afterburner flameholders, preserving stealth shaping.

Electric actuators replace hydraulics, slashing vulnerability while enabling precise throat modulation across Mach regimes. Shape memory alloys contract under heat for self-actuating divergence. Plasma actuators eliminate mechanical gaps, reducing radar cross-section.

Adaptive chevrons deploy from nozzle skins, mixing bypass air to suppress jet plume infrared without thrust loss. Digital twins optimize petal trajectories against thermal flutter. Single-crystal petal leading edges resist oxidation during sustained reheat.

FADEC fusion schedules nozzle area with inlet ramps, preventing engine unstart during rapid decelerations. 3D-printed lattice structures lighten actuators while maintaining rigidity. These innovations extend super cruise envelopes, boost thrust vector angles, and enable tail-less stability.

Key Drivers in Defense Variable Exhaust Nozzles Market

Sixth-generation stealth mandates low-observable nozzles blending with fuselages while vectoring thrust. Super cruise requirements demand precise throat control preventing overexpansion shock trains.

Sustainment economics favor electric actuation minimizing hydraulic leaks. Export markets require modular petals compatible with diverse afterburner cycles. Carrier ops prioritize reliable divergence for catapult strokes.

Budget pressures favor 3D-printed nozzles slashing tooling costs. Supply chain resilience counters titanium shortages via alloy substitution. Interoperability enables common actuators across coalitions.

Post-stall maneuverability drives pitch authority independent of control surfaces. These imperatives position variable nozzles as agility enablers.

Regional Trends in Defense Variable Exhaust Nozzles Market

North America pioneers 2D/axisymmetric hybrids for NGAD, emphasizing electric actuation.

Europe upgrades Typhoon/Rafale with cooled chevrons for dispersed basing.

Asia-Pacific accelerates indigenous development-India's AMCA, China's J-35-tailored to carrier catapults.

Middle East pursues smoke-mixing nozzles for day intercepts.

Russia advances high-temperature petals for Su-57 super maneuverability.

South Korea integrates with KF-21 export packages.

Trends favor plasma-actuated designs; Asia-Pacific gains manufacturing share.

(196 words)

Key Defense Variable Exhaust Nozzles Market Programs

F-22's 2D nozzles vector thrust +-20° pitch via hydraulic clamshells.

NGAD adaptive nozzles schedule divergence with third-stream cores.

EJ200 upgrades deploy translating cascade petals for super cruise.

India's AMCA equips indigenous 2D vectoring for carrier ops.

WS-15 J-20 nozzles feature retractable chevrons for plume reduction.

Rafale M88 nozzle integrates with Snecma core for STOBAR.

Su-57 3D thrust vectoring enables Pugachev Cobra.

T-50 FADEC-driven petal actuation sustains post-stall angles.

Table of Contents

Defense Variable Exhaust Nozzles Market - Table of Contents

Defense Variable Exhaust Nozzles Market Report Definition

Defense Variable Exhaust Nozzles Market Segmentation

By Platform

By Nozzle Type

By Actuation

Defense Variable Exhaust Nozzles Market Analysis for next 10 Years

The 10-year Defense Variable Exhaust Nozzles market analysis would give a detailed overview of Defense Variable Exhaust Nozzles market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Variable Exhaust Nozzles Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Variable Exhaust Nozzles Market Forecast

The 10-year Defense Variable Exhaust Nozzles market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Variable Exhaust Nozzles Market Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense Variable Exhaust Nozzles Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Variable Exhaust Nozzles Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Variable Exhaust Nozzles Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Platform, 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Nozzle Type, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Region, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Platform, 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Nozzle Type, 2026-2036

List of Figures

- Figure 1: Global Variable Exhaust Nozzles Market Forecast, 2026-2036

- Figure 2: Global Variable Exhaust Nozzles Market Forecast, By Region, 2026-2036

- Figure 3: Global Variable Exhaust Nozzles Market Forecast, By Platform, 2026-2036

- Figure 4: Global Variable Exhaust Nozzles Market Forecast, By Nozzle Type, 2026-2036

- Figure 5: North America, Variable Exhaust Nozzles Market , Forecast, 2026-2036

- Figure 6: Europe, Variable Exhaust Nozzles Market , Forecast, 2026-2036

- Figure 7: Middle East, Variable Exhaust Nozzles Market , Forecast, 2026-2036

- Figure 8: APAC, Variable Exhaust Nozzles Market , Forecast, 2026-2036

- Figure 9: South America, Variable Exhaust Nozzles Market , Forecast, 2026-2036

- Figure 10: United States, Variable Exhaust Nozzles Market , Technology Maturation, 2026-2036

- Figure 11: United States, Variable Exhaust Nozzles Market , Forecast, 2026-2036

- Figure 12: Canada, Variable Exhaust Nozzles Market , Technology Maturation, 2026-2036

- Figure 13: Canada, Variable Exhaust Nozzles Market , Forecast, 2026-2036

- Figure 14: Italy, Variable Exhaust Nozzles Market , Technology Maturation, 2026-2036

- Figure 15: Italy, Variable Exhaust Nozzles Market , Market Forecast, 2026-2036

- Figure 16: France, Variable Exhaust Nozzles Market , Technology Maturation, 2026-2036

- Figure 17: France, Variable Exhaust Nozzles Market , Market Forecast, 2026-2036

- Figure 18: Germany, Variable Exhaust Nozzles Market , Technology Maturation, 2026-2036

- Figure 19: Germany, Variable Exhaust Nozzles Market , Market Forecast, 2026-2036

- Figure 20: Netherlands, Variable Exhaust Nozzles Market , Technology Maturation, 2026-2036

- Figure 21: Netherlands, Variable Exhaust Nozzles Market , Market Forecast, 2026-2036

- Figure 22: Belgium, Variable Exhaust Nozzles Market , Technology Maturation, 2026-2036

- Figure 23: Belgium, Variable Exhaust Nozzles Market , Market Forecast, 2026-2036

- Figure 24: Spain, Variable Exhaust Nozzles Market , Technology Maturation, 2026-2036

- Figure 25: Spain, Variable Exhaust Nozzles Market , Market Forecast, 2026-2036

- Figure 26: Sweden, Variable Exhaust Nozzles Market , Technology Maturation, 2026-2036

- Figure 27: Sweden, Variable Exhaust Nozzles Market , Market Forecast, 2026-2036

- Figure 28: Brazil, Variable Exhaust Nozzles Market , Technology Maturation, 2026-2036

- Figure 29: Brazil, Variable Exhaust Nozzles Market , Market Forecast, 2026-2036

- Figure 30: Australia, Variable Exhaust Nozzles Market , Technology Maturation, 2026-2036

- Figure 31: Australia, Variable Exhaust Nozzles Market , Market Forecast, 2026-2036

- Figure 32: India, Variable Exhaust Nozzles Market , Technology Maturation, 2026-2036

- Figure 33: India, Variable Exhaust Nozzles Market , Market Forecast, 2026-2036

- Figure 34: China, Variable Exhaust Nozzles Market , Technology Maturation, 2026-2036

- Figure 35: China, Variable Exhaust Nozzles Market , Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Variable Exhaust Nozzles Market , Technology Maturation, 2026-2036

- Figure 37: Saudi Arabia, Variable Exhaust Nozzles Market , Market Forecast, 2026-2036

- Figure 38: South Korea, Variable Exhaust Nozzles Market , Technology Maturation, 2026-2036

- Figure 39: South Korea, Variable Exhaust Nozzles Market , Market Forecast, 2026-2036

- Figure 40: Japan, Variable Exhaust Nozzles Market , Technology Maturation, 2026-2036

- Figure 41: Japan, Variable Exhaust Nozzles Market , Market Forecast, 2026-2036

- Figure 42: Malaysia, Variable Exhaust Nozzles Market , Technology Maturation, 2026-2036

- Figure 43: Malaysia, Variable Exhaust Nozzles Market , Market Forecast, 2026-2036

- Figure 44: Singapore, Variable Exhaust Nozzles Market , Technology Maturation, 2026-2036

- Figure 45: Singapore, Variable Exhaust Nozzles Market , Market Forecast, 2026-2036

- Figure 46: United Kingdom, Variable Exhaust Nozzles Market , Technology Maturation, 2026-2036

- Figure 47: United Kingdom, Variable Exhaust Nozzles Market , Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Variable Exhaust Nozzles Market , By Region (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Variable Exhaust Nozzles Market , By Region (CAGR), 2026-2036

- Figure 50: Opportunity Analysis, Variable Exhaust Nozzles Market , By (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Variable Exhaust Nozzles Market , By Platform(CAGR), 2026-2036

- Figure 52: Opportunity Analysis, Variable Exhaust Nozzles Market , By Nozzle Type (Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Variable Exhaust Nozzles Market , By Nozzle Type (CAGR), 2026-2036

- Figure 54: Scenario Analysis, Variable Exhaust Nozzles Market , Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Variable Exhaust Nozzles Market , Global Market, 2026-2036

- Figure 56: Scenario 1, Variable Exhaust Nozzles Market , Total Market, 2026-2036

- Figure 57: Scenario 1, Variable Exhaust Nozzles Market , By Region, 2026-2036

- Figure 58: Scenario 1, Variable Exhaust Nozzles Market , By Platform, 2026-2036

- Figure 59: Scenario 1, Variable Exhaust Nozzles Market , By Nozzle Type, 2026-2036

- Figure 60: Scenario 2, Variable Exhaust Nozzles Market , Total Market, 2026-2036

- Figure 61: Scenario 2, Variable Exhaust Nozzles Market , By Region, 2026-2036

- Figure 62: Scenario 2, Variable Exhaust Nozzles Market , By Platform, 2026-2036

- Figure 63: Scenario 2, Variable Exhaust Nozzles Market , By Nozzle Type, 2026-2036

- Figure 64: Company Benchmark, Variable Exhaust Nozzles Market , 2026-2036