|

市场调查报告书

商品编码

1936050

全球国防附件齿轮箱 (AMAD) 市场 (2026-2036)Global Defense Accessory Gearboxes (AMAD) Market 2026-2036 |

||||||

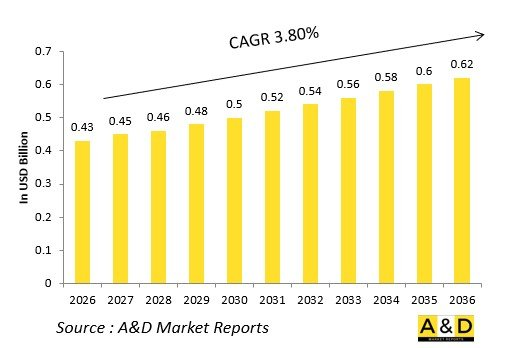

全球国防附件齿轮箱 (AMAD) 市场预计在 2026 年达到 4.3 亿美元,预计到 2036 年将达到 6.2 亿美元,2026 年至 2036 年的复合年增长率 (CAGR) 为 3.80%。

引言

全球国防附件齿轮箱 (AMAD) 市场透过将引擎转子连接到发电机、燃油泵和整合驱动发电机 (IDG) 来驱动关键子系统。行星齿轮系将高速旋转轴的转速降低到辅助轮毂转速,从而在战斗机动过程中实现可靠的电力和液压动力输出。

市场正朝着 "更电气化" 的架构发展,其中自适应动力装置(AMAD)整合了变频发电机和电启动/发电机,并取消了固定速度驱动装置。核心技术包括喷油润滑锥齿轮、防熔化涂层和状态监测晶片检测器。模组化设计有助于在前沿部署期间快速更换零件。

地缘政治对出动次数的需求正在推动研发,优先考虑与无人集群相容的自适应循环核心和齿轮箱。开放式架构使得整个引擎系列能够采用相同的技术。供应链专注于高强度合金和精密滚齿加工。通用电气、赛峰集团和柯林斯宇航公司正在竞相开发混合动力版本。

该市场透过机械可靠性来维持作战能力。

国防附件变速箱 (AMAD) 的技术影响

整合式启动/发电机 (ISG) AMAD 透过行星齿轮耦合高扭力电机,实现引擎从启动到怠速的无缝过渡,无需单独的启动机。模组化附件垫支援现场重新配置(更换发电机),无需拆卸齿轮箱。

基于状态的维护整合了振动感知器和油泥检测器,可将健康数据传输到引擎全权限数位引擎控制系统 (FADEC),以实现预测性更换。碳复合材料外壳显着减轻了重量,同时在低于 20g 的瞬态条件下保持了刚性。带有陶瓷滚子的圆锥滚子轴承即使在润滑油受到污染的情况下也能延长使用寿命。

变速恆频发电机取代了液压蓄压器,电子矩阵转换器稳定了功率输出。静电喷雾润滑均匀地涂覆齿轮,使其耐磨性提高一倍。数位孪生技术模拟了战斗损伤造成的负载应变下的齿轮嚙合情况。

混合动力架构将辅助负载分配给机翼安装的发电机。这使得 "动力输出" AMAD得以实现,从而释放了紧急驱动装置。 3D列印的螺旋齿轮具有最佳化的齿形,可降低噪音。这些创新提高了可靠性,同时实现了分散式推进概念。

国防辅助组件变速箱 (AMAD) 的关键驱动因素

"更电气化" 的飞机架构需要透过紧凑型行星齿轮系驱动的高功率整合驱动发电机。第六代无人平台需要无启动器的AMAD来实现自主发射。

维修经济性强调模组化设计,以最大限度地减少维修车间的引擎拆卸和安装。出口补偿推动了锥齿轮组的许可生产。远征作战优先考虑能够承受沙尘吸入的封闭式齿轮箱。

预算压力促使军方采用经加固的商用衍生型AMAD。供应链韧性透过陶瓷替代轴承解决了轴承短缺问题。互通性标准使得联盟各引擎可使用通用轴承座。

定向能武器需要由主轴驱动的兆瓦级发电机。这些要求使得AMAD成为一种动力装置。

本报告分析了全球国防附件齿轮箱(AMAD)市场,提供了影响该市场的技术资讯、未来10年的预测以及区域趋势。

目录

国防附件变速箱 (AMAD) 市场报告定义

国防附件变速箱 (AMAD) 市场细分

依平台

依应用

依产地

未来十年国防附件齿轮箱 (AMAD) 市场分析

国防附件变速箱 (AMAD) 市场技术

全球国防附件变速箱 (AMAD) 市场预测

区域国防附件变速箱 (AMAD) 市场趋势及预测

北美

驱动因素、限制因素与挑战

PEST 分析

市场预测及情境分析

主要公司

供应商层级概览

公司标竿分析

欧洲

中东

亚太地区

南美洲

国防附件变速箱 (AMAD) 市场国家分析

美国

国防项目

最新资讯

专利

当前市场技术成熟度

市场预测及情境分析

加拿大

义大利

法国

德国

荷兰

比利时

西班牙

瑞典

希腊

澳洲

南非

印度

中国

俄罗斯

韩国

日本

马来西亚

新加坡

巴西

国防附件变速箱 (AMAD) 市场机会矩阵

专家对国防配件齿轮箱 (AMAD) 市场的看法

结论

关于航空与国防市场报告

The Global Defense Accessory Gearboxes (AMAD) Market is estimated at USD 0.43 billion in 2026, projected to grow to USD 0.62 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 3.80% over the forecast period 2026-2036.

Introduction

The global Defense Accessory Gearboxes (AMAD) market powers critical subsystems by coupling engine rotors to generators, fuel pumps, and integrated drive generators. Epicyclic gear trains step down high-speed spool rotation to accessory pad speeds, enabling reliable electricity and hydraulics under combat maneuvers.

Market evolution tracks more-electric architectures, where AMADs integrate variable frequency generators and electric starter/generators, eliminating constant-speed drives. Core technologies include spray-lubricated bevel gears, anti-fretting coatings, and condition monitoring chip detectors. Emphasis on modularity supports rapid swaps during forward deployments.

Geopolitical demands for sortie generation drive development, prioritizing gearboxes compatible with adaptive cycle cores and unmanned swarms. Open architectures enable technology insertion across engine families. Supply chains focus on high-strength alloys and precision hobbing. Competition features GE, Safran, and Collins Aerospace pioneering hybrid electric variants.

This market sustains mission capability through mechanical reliability.

Technology Impact in Defense Accessory Gearboxes (AMAD)

Integrated starter/generator (ISG) AMADs eliminate separate starters, using high-torque electric motors coupled through planetary gears for seamless engine cranking to idle transitions. Modular accessory pads allow field reconfiguration-generator swaps without gearbox removal.

Condition-based maintenance embeds vibration sensors and oil debris detectors, streaming health data via engine FADEC for predictive swaps. Carbon composite housings slash weight while maintaining rigidity under 20g transients. Tapered roller bearings with ceramic rollers extend lives under contaminated lubes.

Variable speed constant frequency generators replace hydraulic accumulators, stabilizing output through electronic matrix converters. Spray lubrication with electrostatically charged mists coats gears uniformly, doubling scuff resistance. Digital twins simulate gear mesh under distorted loads from battle damage.

Hybrid electric architectures offload accessories to wing-mounted generators, enabling "power-off-take" AMADs focused solely on emergency drives. 3D-printed helical gears optimize tooth geometry for noise reduction. These innovations boost reliability while enabling distributed propulsion concepts.

Key Drivers in Defense Accessory Gearboxes (AMAD)

More-electric aircraft architectures demand high-output integrated drive generators powered through compact epicyclic trains. Sixth-generation unmanned platforms require starterless AMADs for autonomous launches.

Sustainment economics favor modular designs minimizing engine removals during depot visits. Export offsets spur licensed production of bevel gear sets. Expeditionary ops prioritize sealed gearboxes tolerant of sand ingestion.

Budget pressures favor commercial derivative AMADs with military hardening. Supply chain resilience counters bearing shortages via ceramic substitution. Interoperability standards enable common pads across coalition engines.

Directed-energy weapons need megawatt-class generators driving off main spools. These imperatives position AMADs as electrical powerplants.

Regional Trends in Defense Accessory Gearboxes (AMAD)

North America dominates with F-35 sustainment driving ISG integration for STOVL variants.

Europe upgrades Rafale/Typhoon with modular generator pads for dispersed basing.

Asia-Pacific accelerates indigenous development-India's Tejas, China's J-20-for domestic engine families.

Middle East pursues desert-hardened sealed designs.

Russia advances high-g tolerant gearboxes for Su-57 agility.

South Korea integrates with KF-21 export packages.

Trends favor electric hybrids; Asia-Pacific gains manufacturing share.

Key Defense Accessory Gearboxes (AMAD) Programs

F135 AMAD powers integrated generator/starter with planetary coupling for lift fan operations.

NGAD hybrid electric AMAD incorporates wing-buried generators offloading main spool.

EJ200 upgrades deliver variable frequency power through compact epicyclic trains.

India's Kaveri derivative equips indigenous starter/generator pad.

F119 gearbox drives high-fault-tolerant electrical systems for stealth missions.

Rafale M88 AMAD integrates emergency hydraulic pumps.

Su-57 AL-41F1 gearbox handles 3D thrust vectoring accessory loads.

T-7A trainer validates high-cycle composite housings.

Table of Contents

Defense Accessory Gearboxes Market - Table of Contents

Defense Accessory Gearboxes Market Report Definition

Defense Accessory Gearboxes Market Segmentation

By Platform

By Application

By Source

Defense Accessory Gearboxes Market Analysis for next 10 Years

The 10-year Defense Accessory Gearboxes market analysis would give a detailed overview of Defense Accessory Gearboxes market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Accessory Gearboxes Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Accessory Gearboxes Market Forecast

The 10-year Defense Accessory Gearboxes market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Accessory Gearboxes Market Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense Accessory Gearboxes Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Accessory Gearboxes Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Accessory Gearboxes Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Application, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Platform, 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Source, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Application, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Platform, 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Source, 2026-2036

List of Figures

- Figure 1: Global Defense Accessory Gearboxes Market Forecast, 2026-2036

- Figure 2: Global Defense Accessory Gearboxes Market Forecast, By Application, 2026-2036

- Figure 3: Global Defense Accessory Gearboxes Market Forecast, By Platform, 2026-2036

- Figure 4: Global Defense Accessory Gearboxes Market Forecast, By Source, 2026-2036

- Figure 5: North America, Defense Accessory Gearboxes Market , Forecast, 2026-2036

- Figure 6: Europe, Defense Accessory Gearboxes Market , Forecast, 2026-2036

- Figure 7: Middle East, Defense Accessory Gearboxes Market , Forecast, 2026-2036

- Figure 8: APAC, Defense Accessory Gearboxes Market , Forecast, 2026-2036

- Figure 9: South America, Defense Accessory Gearboxes Market , Forecast, 2026-2036

- Figure 10: United States, Defense Accessory Gearboxes Market , Technology Maturation, 2026-2036

- Figure 11: United States, Defense Accessory Gearboxes Market , Forecast, 2026-2036

- Figure 12: Canada, Defense Accessory Gearboxes Market , Technology Maturation, 2026-2036

- Figure 13: Canada, Defense Accessory Gearboxes Market , Forecast, 2026-2036

- Figure 14: Italy, Defense Accessory Gearboxes Market , Technology Maturation, 2026-2036

- Figure 15: Italy, Defense Accessory Gearboxes Market , Market Forecast, 2026-2036

- Figure 16: France, Defense Accessory Gearboxes Market , Technology Maturation, 2026-2036

- Figure 17: France, Defense Accessory Gearboxes Market , Market Forecast, 2026-2036

- Figure 18: Germany, Defense Accessory Gearboxes Market , Technology Maturation, 2026-2036

- Figure 19: Germany, Defense Accessory Gearboxes Market , Market Forecast, 2026-2036

- Figure 20: Netherlands, Defense Accessory Gearboxes Market , Technology Maturation, 2026-2036

- Figure 21: Netherlands, Defense Accessory Gearboxes Market , Market Forecast, 2026-2036

- Figure 22: Belgium, Defense Accessory Gearboxes Market , Technology Maturation, 2026-2036

- Figure 23: Belgium, Defense Accessory Gearboxes Market , Market Forecast, 2026-2036

- Figure 24: Spain, Defense Accessory Gearboxes Market , Technology Maturation, 2026-2036

- Figure 25: Spain, Defense Accessory Gearboxes Market , Market Forecast, 2026-2036

- Figure 26: Sweden, Defense Accessory Gearboxes Market , Technology Maturation, 2026-2036

- Figure 27: Sweden, Defense Accessory Gearboxes Market , Market Forecast, 2026-2036

- Figure 28: Brazil, Defense Accessory Gearboxes Market , Technology Maturation, 2026-2036

- Figure 29: Brazil, Defense Accessory Gearboxes Market , Market Forecast, 2026-2036

- Figure 30: Australia, Defense Accessory Gearboxes Market , Technology Maturation, 2026-2036

- Figure 31: Australia, Defense Accessory Gearboxes Market , Market Forecast, 2026-2036

- Figure 32: India, Defense Accessory Gearboxes Market , Technology Maturation, 2026-2036

- Figure 33: India, Defense Accessory Gearboxes Market , Market Forecast, 2026-2036

- Figure 34: China, Defense Accessory Gearboxes Market , Technology Maturation, 2026-2036

- Figure 35: China, Defense Accessory Gearboxes Market , Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Defense Accessory Gearboxes Market , Technology Maturation, 2026-2036

- Figure 37: Saudi Arabia, Defense Accessory Gearboxes Market , Market Forecast, 2026-2036

- Figure 38: South Korea, Defense Accessory Gearboxes Market , Technology Maturation, 2026-2036

- Figure 39: South Korea, Defense Accessory Gearboxes Market , Market Forecast, 2026-2036

- Figure 40: Japan, Defense Accessory Gearboxes Market , Technology Maturation, 2026-2036

- Figure 41: Japan, Defense Accessory Gearboxes Market , Market Forecast, 2026-2036

- Figure 42: Malaysia, Defense Accessory Gearboxes Market , Technology Maturation, 2026-2036

- Figure 43: Malaysia, Defense Accessory Gearboxes Market , Market Forecast, 2026-2036

- Figure 44: Singapore, Defense Accessory Gearboxes Market , Technology Maturation, 2026-2036

- Figure 45: Singapore, Defense Accessory Gearboxes Market , Market Forecast, 2026-2036

- Figure 46: United Kingdom, Defense Accessory Gearboxes Market , Technology Maturation, 2026-2036

- Figure 47: United Kingdom, Defense Accessory Gearboxes Market , Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Defense Accessory Gearboxes Market , By Application (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Defense Accessory Gearboxes Market , By Application (CAGR), 2026-2036

- Figure 50: Opportunity Analysis, Defense Accessory Gearboxes Market , By (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Defense Accessory Gearboxes Market , By Platform(CAGR), 2026-2036

- Figure 52: Opportunity Analysis, Defense Accessory Gearboxes Market , By Source (Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Defense Accessory Gearboxes Market , By Source (CAGR), 2026-2036

- Figure 54: Scenario Analysis, Defense Accessory Gearboxes Market , Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Defense Accessory Gearboxes Market , Global Market, 2026-2036

- Figure 56: Scenario 1, Defense Accessory Gearboxes Market , Total Market, 2026-2036

- Figure 57: Scenario 1, Defense Accessory Gearboxes Market , By Application, 2026-2036

- Figure 58: Scenario 1, Defense Accessory Gearboxes Market , By Platform, 2026-2036

- Figure 59: Scenario 1, Defense Accessory Gearboxes Market , By Source, 2026-2036

- Figure 60: Scenario 2, Defense Accessory Gearboxes Market , Total Market, 2026-2036

- Figure 61: Scenario 2, Defense Accessory Gearboxes Market , By Application, 2026-2036

- Figure 62: Scenario 2, Defense Accessory Gearboxes Market , By Platform, 2026-2036

- Figure 63: Scenario 2, Defense Accessory Gearboxes Market , By Source, 2026-2036

- Figure 64: Company Benchmark, Defense Accessory Gearboxes Market , 2026-2036