|

市场调查报告书

商品编码

1951128

全球防务海上搜索与导航雷达市场(2026-2036)Global Defense Surface Search / Navigation Radars Market 2026-2036 |

||||||

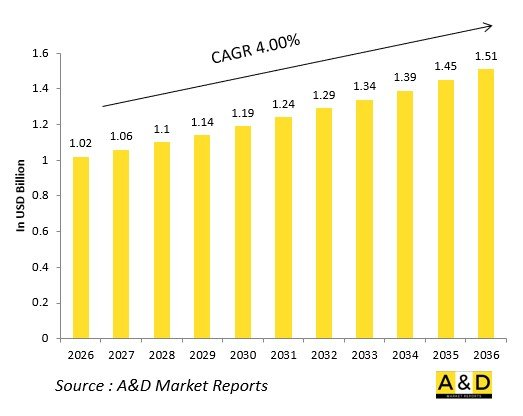

全球防务海上搜寻与导航雷达市场预计在2026年达到10.2亿美元,预计到2036年将达到15.1亿美元,2026年至2036年的复合年增长率(CAGR)为4.00%。

引言

由于海上竞争加剧和非对称威胁,对精确海上态势感知的需求日益增长,全球防务海上搜索/导航雷达市场预计将蓬勃发展。 这些雷达结合了X波段的精度和S波段的抗干扰能力,能够在各种天气条件下运行,尤其擅长在嘈杂的沿海环境中探测水面舰艇、低空飞行器和潜望镜。产业领导者正在开发采用数位波束成形和主动相控阵雷达(AESA)技术的双用途平台,用于防撞、目标分类以及与作战管理系统的整合。

舰队现代化推动了雷达的发展,老旧的机械扫描雷达正被紧凑型、低特征的雷达阵列所取代,这些雷达阵列适用于护卫舰、轻型护卫舰和无人水面舰艇。反无人机和小艇拦截以及与卫星和声吶网路的互通性也是推动雷达需求成长的因素。频段拥塞和电子战威胁等挑战正在推动认知处理和波形适应性的创新。这一时代有望出现以软体为中心的雷达,这些雷达能够提高态势感知能力,减轻舰员的工作负荷,并支援在复杂水域执行多任务作战。

科技对防御性海上搜索/导航雷达的影响

技术突破正在将防御性海上搜索/导航雷达转变为实现海上优势的多功能工具。氮化镓 (GaN) 发射机提高了对隐蔽小型舰艇和无人机 (UAV) 的分辨率和探测范围,而主动电子扫描阵列 (AESA) 则实现了瞬时多波束控制,从而能够同时进行搜索和追踪。利用人工智慧演算法的数位讯号处理技术能够有效滤除表面噪声,即使在波涛汹涌的海面上也能自动侦测到半潜式舰艇和快速攻击艇。

量子启发式感测器和高光谱融合技术正在改进潜望镜和潜水员的侦测,这对于港口防御至关重要。软体定义无线电技术能够实现动态跳频,从而避免干扰并提高在电子战场景中的韧性。 5G 骨干网路和扩增实境 (AR) 介面的整合简化了导航流程,并最大限度地减少了高威胁环境下的人为错误。 这些进步减少了老旧舰艇改造所需的系统尺寸,促进了无人舰艇的自主运行,并重新定义了海上监视,使其从被动监视转变为符合网络中心战战略的预测性威胁消除。

国防海上搜索和导航雷达市场的主要驱动因素

国防海上搜索和导航雷达市场受到强劲驱动因素的推动。不断升级的海上领土争端正在加速近岸平台的升级,优先考虑能够抵抗欺骗和多路径干扰的雷达。全球海军扩张计画要求为轻型护卫舰和巡逻艇配备紧凑型、高解析度系统,并与飞弹导引和电子战设备无缝整合。

与自主系统和人工智慧分析技术的协同作用正在推动能够即时识别威胁的自适应雷达的应用。 受沿海国家打击走私、海盗和非法捕捞活动的推动,出口市场蓬勃发展,这促使市场青睐价格适中且性能卓越的商用现货(COTS)加固型设计。永续发展目标则推动低功耗、模组化架构的发展,从而延长使用寿命并简化维护。

地缘政治联盟促进共同采购,进而降低原物料短缺造成的供应风险。旨在提高频谱效率和网路安全的法规增强了系统抵御混合威胁的能力。这些因素强调了机动性、精确性和网路整合性,以保护关键海上航道。

本报告分析了全球国防海上搜索和导航雷达市场,提供了影响该市场的技术资讯、未来十年的预测以及区域趋势。

目录

国防海上搜索与导航雷达市场报告定义

国防海上搜索与导航雷达市场细分

依地区

依平台

依功能

依科技

未来十年国防海上搜索与导航雷达市场分析

国防海上搜索与导航雷达市场技术

全球国防海上搜索与导航雷达市场预测

区域国防海上搜索与导航雷达市场趋势及预测

北美

驱动因素、限制因素及挑战

PEST分析

市场预测与情境分析

主要公司

供应商层级概览

公司标竿分析

欧洲

中东

亚太地区

南美洲

国防海上搜索/导航雷达市场国家分析

美国

国防项目

最新资讯

专利

当前市场技术成熟度

市场预测与情境分析

加拿大

义大利

法国

德国

荷兰

比利时

西班牙

瑞典

希腊

澳洲

南非

印度

中国

俄罗斯

韩国

日本

马来西亚

新加坡

巴西

国防海上搜索/导航雷达市场机会矩阵

国防海上搜索/导航雷达市场报告专家意见

结论

关于航空与国防市场报告

The Global Defense Surface Search / Navigation Radars market is estimated at USD 1.02 billion in 2026, projected to grow to USD 1.51 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 4.00% over the forecast period 2026-2036.

Introduction:

The global Defense Surface Search / Navigation Radars market is set for dynamic expansion, propelled by the need for precise maritime domain awareness amid rising naval confrontations and asymmetric threats. These radars excel in detecting surface vessels, low-flying aircraft, and periscopes in cluttered coastal environments, combining X-band precision with S-band resilience for all-weather operations. Industry leaders advance dual-use platforms with digital beamforming and AESA technology, enabling collision avoidance, target classification, and integration into combat management systems.

Growth stems from fleet modernizations replacing aging mechanical scanners with compact, low-signature arrays suited for frigates, corvettes, and unmanned surface vessels. Emphasis on anti-drone and small boat interdiction drives demand, alongside interoperability with satellite and sonar networks. Challenges like spectrum congestion and electronic warfare threats spur innovations in cognitive processing and waveform agility. This era promises software-centric radars that enhance situational awareness, reduce crew burden, and support multi-mission profiles in contested waters.

Technology Impact in Defense Surface Search / Navigation Radars

Technological breakthroughs are transforming Defense Surface Search / Navigation Radars into versatile enablers of maritime superiority. Gallium nitride (GaN) transmitters boost resolution and range against stealthy small craft and UAVs, while active electronically scanned arrays (AESA) deliver instantaneous multi-beam operation for simultaneous search and track. Digital signal processing with AI algorithms excels in sea clutter rejection, automating detection of semi-submersibles and fast attack craft in high-sea states.

Quantum-inspired sensors and hyperspectral fusion improve periscope and swimmer detection, critical for harbor protection. Software-defined radios enable dynamic frequency hopping to evade jamming, fostering resilience in electronic warfare scenarios. Integration with 5G backbones and augmented reality interfaces streamlines navigation, minimizing human error during high-threat transits. These advancements shrink system footprints for retrofits on legacy hulls, promote unmanned vessel autonomy, and align with network-centric warfare, redefining surface surveillance from reactive monitoring to predictive threat neutralization.

Key Drivers in Defense Surface Search / Navigation Radars

Robust drivers underpin the Defense Surface Search / Navigation Radars market. Escalating maritime territorial disputes accelerate upgrades for littoral-capable platforms, prioritizing radars resilient to spoofing and multipath interference. Naval expansion programs worldwide demand compact, high-resolution systems for corvettes and patrol vessels, integrating seamlessly with missile cueing and electronic warfare suites.

Technological synergies with autonomous systems and AI-driven analytics propel adoption of adaptive radars that classify threats in real-time. Export markets flourish as coastal nations counter smuggling, piracy, and illegal fishing, favoring affordable yet capable COTS-enhanced designs. Sustainability goals favor low-power, modular architectures that extend service life and ease maintenance.

Geopolitical alliances foster joint procurement, mitigating supply risks from raw material shortages. Regulatory pushes for spectrum efficiency and cybersecurity harden systems against hybrid threats. Together, these forces emphasize agility, precision, and networked integration to safeguard vital sea lanes.

Regional Trends in Defense Surface Search / Navigation Radars

Regional variations define Defense Surface Search / Navigation Radars trends. Asia-Pacific leads with intense focus on archipelagic defense, advancing compact X-band arrays for island chain patrols and anti-access strategies. Europe emphasizes NATO-standard interoperability, upgrading frigates with dual-band systems for Baltic and Mediterranean operations against sub-surface intruders.

North America pioneers GaN-AESA innovations for carrier escorts and Arctic transits, exporting to allies facing hybrid maritime challenges. The Middle East prioritizes mobile coastal radars for oil platform security and strait surveillance amid proxy conflicts. In Africa and Latin America, emphasis shifts to rugged, low-maintenance solutions for anti-piracy and EEZ enforcement, often via technology transfers.

Pan-regional collaborations address chokepoint vulnerabilities, with trends converging on multi-static networks blending radar with passive acoustics. Climate-resilient designs adapt to extreme weather, ensuring persistent vigilance across diverse theaters.

Key Defense Surface Search / Navigation Radars Programs

Signature Defense Surface Search / Navigation Radars programs highlight maritime innovation. Naval flagships include multi-function AESA suites for destroyers, fusing surface search with fire control for over-the-horizon targeting. Coastal defense initiatives deploy truck-mounted S/X-band systems for rapid perimeter surveillance and drone mitigation.

Unmanned programs integrate low-profile radars into USVs for swarm denial and persistent monitoring. International consortia drive modular upgrade paths for legacy fleets, incorporating cognitive features for clutter adaptation. Airborne maritime patrol variants evolve with podded navigation aids for P-8 successors.

These efforts prioritize open architectures for sensor fusion, jamming-resistant waveforms, and human-machine teaming. Focused on export variants and collaborative testing, they bolster blue-water and green-water capabilities, ensuring dominance in contested littorals.

Table of Contents

Defense Surface Search / Navigation Radars Market - Table of Contents

Defense Surface Search / Navigation Radars Market Report Definition

Defense Surface Search / Navigation Radars Market Segmentation

By Region

By Platform

By Function

By Technology

Defense Surface Search / Navigation Radars Market Analysis for next 10 Years

The 10-year Defense Surface Search / Navigation Radars Market analysis would give a detailed overview of Defense Surface Search / Navigation Radars Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Surface Search / Navigation Radars Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Surface Search / Navigation Radars Market Forecast

The 10-year Defense Surface Search / Navigation Radars Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Surface Search / Navigation Radars Market Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense Surface Search / Navigation Radars Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Surface Search / Navigation Radars Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Surface Search / Navigation Radars Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Function, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Platform, 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Function, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Platform, 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Region, 2026-2036

List of Figures

- Figure 1: Global Defense Surface Search / Navigation Radars Market Forecast, 2026-2036

- Figure 2: Global Defense Surface Search / Navigation Radars Market Forecast, By Function, 2026-2036

- Figure 3: Global Defense Surface Search / Navigation Radars Market Forecast, By Platform, 2026-2036

- Figure 4: Global Defense Surface Search / Navigation Radars Market Forecast, By Region, 2026-2036

- Figure 5: North America, Defense Surface Search / Navigation Radars Market, Forecast, 2026-2036

- Figure 6: Europe, Defense Surface Search / Navigation Radars Market, Forecast, 2026-2036

- Figure 7: Middle East, Defense Surface Search / Navigation Radars Market, Forecast, 2026-2036

- Figure 8: APAC, Defense Surface Search / Navigation Radars Market, Forecast, 2026-2036

- Figure 9: South America, Defense Surface Search / Navigation Radars Market, Forecast, 2026-2036

- Figure 10: United States, Defense Surface Search / Navigation Radars Market, Technology Maturation, 2026-2036

- Figure 11: United States, Defense Surface Search / Navigation Radars Market, Forecast, 2026-2036

- Figure 12: Canada, Defense Surface Search / Navigation Radars Market, Technology Maturation, 2026-2036

- Figure 13: Canada, Defense Surface Search / Navigation Radars Market, Forecast, 2026-2036

- Figure 14: Italy, Defense Surface Search / Navigation Radars Market, Technology Maturation, 2026-2036

- Figure 15: Italy, Defense Surface Search / Navigation Radars Market, Market Forecast, 2026-2036

- Figure 16: France, Defense Surface Search / Navigation Radars Market, Technology Maturation, 2026-2036

- Figure 17: France, Defense Surface Search / Navigation Radars Market, Market Forecast, 2026-2036

- Figure 18: Germany, Defense Surface Search / Navigation Radars Market, Technology Maturation, 2026-2036

- Figure 19: Germany, Defense Surface Search / Navigation Radars Market, Market Forecast, 2026-2036

- Figure 20: Netherlands, Defense Surface Search / Navigation Radars Market, Technology Maturation, 2026-2036

- Figure 21: Netherlands, Defense Surface Search / Navigation Radars Market, Market Forecast, 2026-2036

- Figure 22: Belgium, Defense Surface Search / Navigation Radars Market, Technology Maturation, 2026-2036

- Figure 23: Belgium, Defense Surface Search / Navigation Radars Market, Market Forecast, 2026-2036

- Figure 24: Spain, Defense Surface Search / Navigation Radars Market, Technology Maturation, 2026-2036

- Figure 25: Spain, Defense Surface Search / Navigation Radars Market, Market Forecast, 2026-2036

- Figure 26: Sweden, Defense Surface Search / Navigation Radars Market, Technology Maturation, 2026-2036

- Figure 27: Sweden, Defense Surface Search / Navigation Radars Market, Forecast, 2026-2036

- Figure 28: Brazil, Defense Surface Search / Navigation Radars Market, Technology Maturation, 2026-2036

- Figure 29: Brazil, Defense Surface Search / Navigation Radars Market, Market Forecast, 2026-2036

- Figure 30: Australia, Defense Surface Search / Navigation Radars Market, Technology Maturation, 2026-2036

- Figure 31: Australia, Defense Surface Search / Navigation Radars Market, Market Forecast, 2026-2036

- Figure 32: India, Defense Surface Search / Navigation Radars Market, Technology Maturation, 2026-2036

- Figure 33: India, Defense Surface Search / Navigation Radars Market, Market Forecast, 2026-2036

- Figure 34: China, Defense Surface Search / Navigation Radars Market, Technology Maturation, 2026-2036

- Figure 35: China, Defense Surface Search / Navigation Radars Market, Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Defense Surface Search / Navigation Radars Market, Technology Maturation, 2026-2036

- Figure 37: Saudi Arabia, Defense Surface Search / Navigation Radars Market, Market Forecast, 2026-2036

- Figure 38: South Korea, Defense Surface Search / Navigation Radars Market, Technology Maturation, 2026-2036

- Figure 39: South Korea, Defense Surface Search / Navigation Radars Market, Market Forecast, 2026-2036

- Figure 40: Japan, Defense Surface Search / Navigation Radars Market, Technology Maturation, 2026-2036

- Figure 41: Japan, Defense Surface Search / Navigation Radars Market, Market Forecast, 2026-2036

- Figure 42: Malaysia, Defense Surface Search / Navigation Radars Market, Technology Maturation, 2026-2036

- Figure 43: Malaysia, Defense Surface Search / Navigation Radars Market, Market Forecast, 2026-2036

- Figure 44: Singapore, Defense Surface Search / Navigation Radars Market, Technology Maturation, 2026-2036

- Figure 45: Singapore, Defense Surface Search / Navigation Radars Market, Market Forecast, 2026-2036

- Figure 46: United Kingdom, Defense Surface Search / Navigation Radars Market, Technology Maturation, 2026-2036

- Figure 47: United Kingdom, Defense Surface Search / Navigation Radars Market, Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Defense Surface Search / Navigation Radars Market, By Function (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Defense Surface Search / Navigation Radars Market, By Function (CAGR), 2026-2036

- Figure 50: Opportunity Analysis, Defense Surface Search / Navigation Radars Market, By (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Defense Surface Search / Navigation Radars Market, By Platform(CAGR), 2026-2036

- Figure 52: Opportunity Analysis, Defense Surface Search / Navigation Radars Market, By Region (Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Defense Surface Search / Navigation Radars Market, By Region (CAGR), 2026-2036

- Figure 54: Scenario Analysis, Defense Surface Search / Navigation Radars Market, Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Defense Surface Search / Navigation Radars Market, Global Market, 2026-2036

- Figure 56: Scenario 1, Defense Surface Search / Navigation Radars Market, Total Market, 2026-2036

- Figure 57: Scenario 1, Defense Surface Search / Navigation Radars Market, By Function, 2026-2036

- Figure 58: Scenario 1, Defense Surface Search / Navigation Radars Market, By Platform, 2026-2036

- Figure 59: Scenario 1, Defense Surface Search / Navigation Radars Market, By Region, 2026-2036

- Figure 60: Scenario 2, Defense Surface Search / Navigation Radars Market, Total Market, 2026-2036

- Figure 61: Scenario 2, Defense Surface Search / Navigation Radars Market, By Function, 2026-2036

- Figure 62: Scenario 2, Defense Surface Search / Navigation Radars Market, By Platform, 2026-2036

- Figure 63: Scenario 2, Defense Surface Search / Navigation Radars Market, By Region, 2026-2036

- Figure 64: Company Benchmark, Defense Surface Search / Navigation Radars Market, 2026-2036

全球国防资料链路终端(Link-16)市场(2026-2036 年)全球国防机载製氧系统(OBOGS)市场:2026-2036年

全球国防资料链路终端(Link-16)市场(2026-2036 年)全球国防机载製氧系统(OBOGS)市场:2026-2036年 2026年全球人工智慧负责人面试支援工具市场报告

2026年全球人工智慧负责人面试支援工具市场报告 手提式清洗机市场按产品类型、技术、操作类型、容量、分销管道和最终用途划分 - 全球预测 2026-2032全球国防复合材料市场:2026-2036无人机农业配送市场(按无人机类型、营运模式、有效载荷容量、应用和最终用户)—2025-2030 年全球预测

手提式清洗机市场按产品类型、技术、操作类型、容量、分销管道和最终用途划分 - 全球预测 2026-2032全球国防复合材料市场:2026-2036无人机农业配送市场(按无人机类型、营运模式、有效载荷容量、应用和最终用户)—2025-2030 年全球预测 军事数据链接的全球市场:平台·用途·零组件·频宽·频率·链接类型·销售据点·军事规格·各地区 (~2032年)

军事数据链接的全球市场:平台·用途·零组件·频宽·频率·链接类型·销售据点·军事规格·各地区 (~2032年) 卫星模拟器市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测

卫星模拟器市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测 航空航天:订阅竞争和市场情报

航空航天:订阅竞争和市场情报 Market Forecast:年度订阅服务

Market Forecast:年度订阅服务