|

市场调查报告书

商品编码

1913396

高纯度氧化铝市场:市场机会、成长驱动因素、产业趋势分析及预测(2026-2035)High Purity Alumina Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

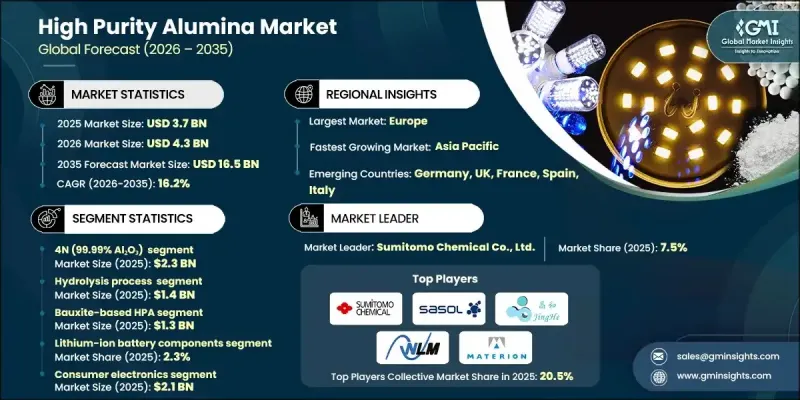

全球高纯度氧化铝市场预计到 2025 年将价值 37 亿美元,到 2035 年达到 165 亿美元,年复合成长率为 16.2%。

市场成长的驱动力在于对满足高端工业应用严苛的品质、可靠性和性能要求的先进材料的需求不断增长。高纯度氧化铝由杂质含量极低的氧化铝製成,具有优异的热稳定性、高耐化学性和卓越的电绝缘性能。这些特性使其成为对精度和耐久性要求极高的应用领域的关键材料。各製造领域对高性能材料的持续依赖支撑着市场的稳定扩张。生产技术的显着进步也推动了市场的发展势头,现代化的精炼和提纯方法确保了材料品质的稳定性。製造商越来越能够根据特定应用的需求对材料性能进行微调,同时提高能源效率并减少排放。这种发展反映了整个工业界向永续製造实践和优化生产流程转变的趋势,使高纯度氧化铝成为下一代技术的关键材料。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 初始市场规模 | 37亿美元 |

| 市场规模预测 | 165亿美元 |

| 复合年增长率 | 16.2% |

预计到2025年,水解製程市场规模将达到14亿美元。与盐酸浸出法一样,水解製程正逐渐成为一种经济高效且扩充性生产的方法,能够提供稳定的纯度水准。它兼具大规模生产和严格品管的优势,使其非常适合满足日益增长的工业需求。

预计到2025年,锂离子电池组件市占率将达到2.3%。对高纯度氧化铝的需求持续向对材料一致性和可靠性要求极高的应用领域转移。在製造公差日益严格的背景下,尤其是在高温和精密加工环境下,对高热稳定性、光学透明度和低污染要求的应用领域仍将保持强劲需求。

预计到2025年,北美高纯度氧化铝市场规模将达5.253亿美元。该地区的成长主要得益于先进电子、航太、国防和储能产业的强劲需求。持续加大研发投入、创新以及提高生产标准,进一步推动了全部区域高纯度氧化铝的应用和消费。

目录

第一章:分析方法和范围

第二章执行摘要

第三章业界考察

- 产业生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 对先进电子设备的需求不断增长

- 电动车生态系统的快速成长

- LED和照明技术拓展

- 产业潜在风险与挑战

- 生产成本高且能源需求旺盛

- 来自低成本区域生产商的竞争压力

- 市场机会

- 扩大下一代电池的应用

- 5G及未来6G基础设施的扩展

- 在航太和国防领域的应用日益广泛

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 按纯度等级

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利状态

- 贸易统计资料(HS编码)(註:贸易统计仅涵盖主要国家)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续努力

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 考虑到碳足迹

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要企业的竞争分析

- 竞争定位矩阵

- 主要趋势

- 企业合併(M&A)

- 商业伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 依纯度等级分類的市场估算与预测(2022-2035 年)

- 3N(99.9% AL2O3)

- 4N(99.99% AL2O3)

- 5N(99.999% AL2O3)

- 6N(99.9999% AL2O3)

- UHPA - 超高纯度氧化铝(纯度超过 99.9999%)

第六章 依製造技术分類的市场估算与预测(2022-2035 年)

- 水解法

- 盐酸(HCl)浸出法

- 醇盐法

- 热解

- 三层电解精炼

- 分馏结晶

- 真空蒸馏

- 其他的

第七章 市场估算与预测:依原料划分(2022-2035 年)

- 矾土基高纯度空气

- 高岭土基HPA

- 铝金属基高纯度铝

- 高铝黏土基HPA

第八章 按应用领域分類的市场估算与预测(2022-2035 年)

- LED基板和照明

- 蓝宝石基板生产

- 半导体製造

- 锂离子电池零件

- 5G和电信基础设施

- 医疗和生物医学应用

- 量子运算组件

- 航太与国防陶瓷

- 电力电子和高频装置

- 技术陶瓷和先进陶瓷

- 电子显示器、光电子学

- 其他的

第九章 依最终用途产业分類的市场估算与预测(2022-2035 年)

- 家用电子电器

- 车

- 航太与国防

- 医疗和医疗设备

- 电讯

- 能源与电力

- 工业/製造业

- 其他的

第十章 各地区市场估计与预测(2022-2035 年)

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第十一章 公司简介

- Alcoa Corporation

- Altech Chemicals Limited

- Baikowski

- Caplinq Corporation

- Emerging sustainable HPA producers

- Hebei Pengda Advanced Materials Technology

- Materion Corporation

- Nippon Light Metal Holdings Co., Ltd.

- Norsk Hydro ASA

- Orbite Technologies Inc.

- PSB Industries SA

- Sumitomo Chemical Co., Ltd.

- Sasol Limited

- Xuancheng Jingrui New Materials Co., Ltd.

The Global High Purity Alumina Market was valued at USD 3.7 billion in 2025 and is estimated to grow at a CAGR of 16.2% to reach USD 16.5 billion by 2035.

Market growth is driven by rising demand for advanced materials that meet strict quality, reliability, and performance requirements across high-end industrial applications. High purity alumina, derived from aluminum oxide with minimal impurity content, offers excellent thermal stability, strong chemical resistance, and superior electrical insulation properties. These characteristics make it a critical material for applications where precision and durability are essential. Continued reliance on high-performance materials across manufacturing sectors has supported consistent market expansion. Significant improvements in production technologies have also contributed to market momentum, as modernized refining and purification methods now deliver more uniform material quality. Manufacturers are increasingly able to fine-tune material characteristics to meet application-specific requirements while improving energy efficiency and lowering emissions. This evolution reflects the broader industrial shift toward sustainable manufacturing practices and optimized production processes, positioning high purity alumina as a key material in next-generation technologies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.7 Billion |

| Forecast Value | $16.5 Billion |

| CAGR | 16.2% |

The hydrolysis process segment reached USD 1.4 billion in 2025. Alongside HCl leaching, hydrolysis has gained prominence as a cost-effective and scalable production method capable of delivering consistent purity levels. Its ability to balance large-scale output with strict quality control has made it well-suited to meet growing industrial demand.

The lithium-ion battery components segment held 2.3% share in 2025. Demand for high purity alumina continues to shift toward applications that require exceptional material consistency and reliability. Usage remains strong across sectors that depend on high thermal stability, optical clarity, and minimal contamination, particularly as manufacturing tolerances become increasingly stringent in high-temperature and precision-driven environments.

North America High Purity Alumina Market generated USD 525.3 million in 2025. Growth in this region is supported by strong demand from advanced electronics, aerospace, defense, and energy storage industries. Continued investment in research, innovation, and high manufacturing standards is further accelerating adoption and consumption across the region.

Key companies operating in the Global High Purity Alumina Market include Alcoa Corporation, Baikowski, Norsk Hydro ASA, Materion Corporation, Nippon Light Metal Holdings Co., Ltd., Sumitomo Chemical Co., Ltd., Sasol Limited, Altech Chemicals Limited, Orbite Technologies Inc., PSB Industries SA, Caplinq Corporation, Hebei Pengda Advanced Materials Technology, Xuancheng Jingrui New Materials Co., Ltd., and emerging sustainable HPA producers. Companies in the Global High Purity Alumina Market are strengthening their market position through technology advancement, capacity expansion, and product specialization. Many players are investing in process innovation to achieve higher purity levels while reducing production costs and environmental impact. Strategic focus on application-specific grades allows suppliers to meet evolving customer requirements in electronics, energy storage, and advanced manufacturing. Geographic expansion and localized production are being used to improve supply reliability and reduce logistics risks.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Purity Grade

- 2.2.2 Production Technology

- 2.2.3 Raw Material

- 2.2.4 Application

- 2.2.5 End Use Industry

- 2.2.6 Regional

- 2.3 TAM Analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for advanced electronics

- 3.2.1.2 Rapid growth in electric vehicle ecosystems

- 3.2.1.3 Expansion of LED and lighting technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs and energy requirements

- 3.2.2.2 Competitive pressure from low-cost regional producers

- 3.2.3 Market opportunities

- 3.2.3.1 Growing adoption in next-generation batteries

- 3.2.3.2 Expansion of 5G and future 6G infrastructure

- 3.2.3.3 Increasing use in aerospace and defence applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By purity grade

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Purity Grade, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 3N (99.9% AL2O3)

- 5.3 4N (99.99% AL2O3)

- 5.4 5N(99.999% AL2O3)

- 5.5 6N (99.9999% AL2O3)

- 5.6 UHPA - ultra high purity alumina (>99.9999%)

Chapter 6 Market Estimates and Forecast, By Production Technology, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Hydrolysis process

- 6.3 HCL (hydrochloric acid) leaching

- 6.4 Alkoxide process

- 6.5 Thermal decomposition

- 6.6 Three-layer electrolytic refining

- 6.7 Fractional crystallization

- 6.8 Vacuum distillation

- 6.9 Others

Chapter 7 Market Estimates and Forecast, By Raw Material, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Bauxite-based HPA

- 7.3 Kaolin-based HPA

- 7.4 Aluminum metal-based HPA

- 7.5 High-alumina clay-based HPA

Chapter 8 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Led substrates and lighting

- 8.3 Sapphire substrate production

- 8.4 Semiconductor manufacturing

- 8.5 Lithium-ion battery components

- 8.6 5g and telecommunications infrastructure

- 8.7 Medical and biomedical applications

- 8.8 Quantum computing components

- 8.9 Aerospace and defense ceramics

- 8.10 Power electronics and RF devices

- 8.11 Technical ceramics and advanced ceramics

- 8.12 Electronic displays and optoelectronics

- 8.13 Others

Chapter 9 Market Estimates and Forecast, By End Use Industry, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Consumer electronics

- 9.3 Automotive

- 9.4 Aerospace and defense

- 9.5 Healthcare and medical devices

- 9.6 Telecommunications

- 9.7 Energy and power

- 9.8 Industrial manufacturing

- 9.9 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Alcoa Corporation

- 11.2 Altech Chemicals Limited

- 11.3 Baikowski

- 11.4 Caplinq Corporation

- 11.5 Emerging sustainable HPA producers

- 11.6 Hebei Pengda Advanced Materials Technology

- 11.7 Materion Corporation

- 11.8 Nippon Light Metal Holdings Co., Ltd.

- 11.9 Norsk Hydro ASA

- 11.10 Orbite Technologies Inc.

- 11.11 PSB Industries SA

- 11.12 Sumitomo Chemical Co., Ltd.

- 11.13 Sasol Limited

- 11.14 Xuancheng Jingrui New Materials Co., Ltd.

奈米涂层半导体散热器市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、材质、装置、製程及最终用户划分

奈米涂层半导体散热器市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、材质、装置、製程及最终用户划分 全球高纯度氧化铝市场规模、份额、趋势及成长分析报告(2026-2034年)

全球高纯度氧化铝市场规模、份额、趋势及成长分析报告(2026-2034年) 2026年全球高纯度氧化铝市场报告

2026年全球高纯度氧化铝市场报告 高纯度氧化铝(HPA):市占率分析、产业趋势与统计、成长预测(2026-2031)

高纯度氧化铝(HPA):市占率分析、产业趋势与统计、成长预测(2026-2031) 高纯度氧化铝市场规模、份额及成长分析(依产品类型、技术、应用、最终用户及地区划分)-2026-2033年产业预测

高纯度氧化铝市场规模、份额及成长分析(依产品类型、技术、应用、最终用户及地区划分)-2026-2033年产业预测 高纯度氧化铝市场按应用、纯度等级、技术和地区划分

高纯度氧化铝市场按应用、纯度等级、技术和地区划分 高纯度氧化铝市场按产品类型、形式、生产技术、应用和最终用户划分-2025-2030 年全球预测

高纯度氧化铝市场按产品类型、形式、生产技术、应用和最终用户划分-2025-2030 年全球预测 高纯度氧化铝市场规模、份额、趋势及预测(按纯度等级、生产方法、应用和地区),2025 年至 2033 年

高纯度氧化铝市场规模、份额、趋势及预测(按纯度等级、生产方法、应用和地区),2025 年至 2033 年 全球高纯度紫杉叶素市场:市场占有率和排名、总销售量和需求预测(2025-2031)2026-2032年高纯度氧化铝市场(按等级、技术、应用和地区)

全球高纯度紫杉叶素市场:市场占有率和排名、总销售量和需求预测(2025-2031)2026-2032年高纯度氧化铝市场(按等级、技术、应用和地区)