|

市场调查报告书

商品编码

1716692

陆域风能市场机会、成长动力、产业趋势分析及2025-2034年预测Onshore Wind Energy Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

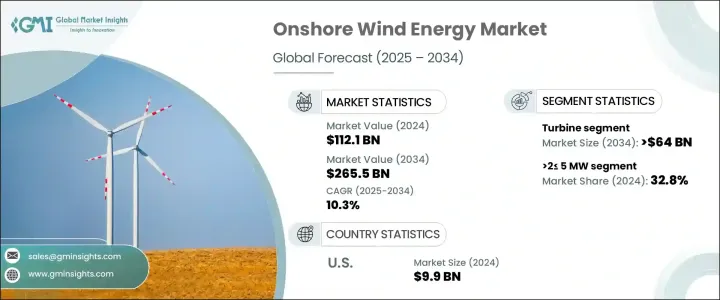

2024 年全球陆上风能市场价值为 1,121 亿美元,预估 2025 年至 2034 年期间的复合年增长率为 10.3%。这一成长主要得益于对清洁再生能源的需求激增,以及政府支持的旨在减少碳排放和支持永续发展目标的措施。世界各国都在加强摆脱化石燃料,而陆上风能是最具成本效益和可扩展性的解决方案之一。随着全球各经济体在实现再生能源目标方面面临越来越大的压力,陆上风电项目在有利的监管框架、不断下降的技术成本以及现代风力涡轮机效率提高的推动下,正在获得发展动力。

政策制定者正在引入简化的许可流程、提供税收抵免并部署激励计划以促进风能发展,为市场参与者扩大投资组合创造非常有利的环境。此外,涡轮机设计和控制系统的技术创新显着提高了容量係数并降低了平准化能源成本 (LCOE),使陆上风电专案更具经济可行性。随着气候目标的收紧和能源需求的飙升,尤其是在新兴经济体,全球市场预计将在未来十年内见证产能的大幅增加。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 1121亿美元 |

| 预测值 | 2655亿美元 |

| 复合年增长率 | 10.3% |

联邦和州级激励措施的稳步实施、强有力的政府授权以及积极的可再生能源目标,正在成为陆上风能市场的强劲增长催化剂。快速的城市化、工业扩张以及不断增加的能源消耗(尤其是在发展中地区)进一步加速了陆上风电项目的部署。巴西、墨西哥和阿根廷等国家正在成为有前景的市场,它们不仅拥有丰富的风能资源,而且还提供积极的政府支持和有吸引力的投资框架。这些国家正在经历越来越多的项目公告和外国投资,旨在扩大其风能基础设施。电网基础设施现代化的平行投资有助于风电更好地融入国家能源系统,提高风力发电的可靠性和效率。

陆上风能市场分为涡轮机、支撑结构、电力基础设施等,其中涡轮机占据主导地位。预计到 2034 年,光是涡轮机领域就将创造 640 亿美元的收入,这得益于对符合严格的再生能源要求的高容量、高效涡轮机的需求不断增长。涡轮机技术的进步,包括更高的塔架、更长的叶片和复杂的电网整合能力,实现了更高的能量输出和对不同风况的更强的适应性,使陆上风电装置对投资者和公用事业公司都更具吸引力。

就涡轮机额定功率而言,2 MW 至 5 MW 的系统在 2024 年占据了 32.8% 的市场份额,这得益于它们在容量、成本和电网相容性之间的最佳平衡。这些涡轮机特别适合需要中等输出且有空间或技术限制的项目。增强的控制系统和先进的软体整合也提高了涡轮机的性能,提高了能量产量,并最大限度地减少了停机时间。

在联邦政府的长期激励措施和风电技术成本效益的提高的支持下,北美将在 2024 年占据全球陆上风能市场的 8.6% 份额。随着政策的持续支持和技术的改进,北美仍然是推动未来市场成长的关键地区。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统

- 监管格局

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 战略仪表板

- 创新与技术格局

第五章:市场规模及预测:依组件划分,2021 年至 2034 年

- 主要趋势

- 涡轮

- 塔

- 刀片

- 其他的

- 支撑结构

- 下部结构钢

- 基础

- 其他的

- 电力基础设施

- 电线电缆

- 变电站

- 其他的

- 其他的

第六章:市场规模及预测:以涡轮机额定功率,2021 年至 2034 年

- 主要趋势

- ≤2兆瓦

- >2≤5兆瓦

- >5≤8兆瓦

- >8≤10兆瓦

- >10≤12兆瓦

- > 12 兆瓦

第七章:市场规模及预测:依地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 荷兰

- 瑞典

- 法国

- 英国

- 芬兰

- 波兰

- 西班牙

- 义大利

- 奥地利

- 爱尔兰

- 比利时

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 世界其他地区

第八章:公司简介

- CRRC

- CSSC Haizhuang Wind Power

- Envision Group

- Goldwind

- GE Vernova

- Iberdrola

- Nordex

- Siemens Gamesa Renewable Energy

- United Power

- Vestas

- Windey Energy Technology Group

The Global Onshore Wind Energy Market was valued at USD 112.1 billion in 2024 and is projected to grow at a CAGR of 10.3% between 2025 and 2034. This growth is largely fueled by a surge in demand for clean, renewable energy sources, combined with government-backed initiatives aimed at reducing carbon emissions and supporting sustainable development goals. Countries worldwide are ramping up efforts to transition away from fossil fuels, and onshore wind energy stands out as one of the most cost-effective and scalable solutions. As economies worldwide face increasing pressure to meet their renewable energy targets, onshore wind projects are gaining momentum, driven by favorable regulatory frameworks, declining technology costs, and improved efficiency of modern wind turbines.

Policymakers are introducing streamlined permitting processes, offering tax credits, and deploying incentive programs to foster wind energy development, creating a highly conducive environment for market players to expand their portfolios. In addition, technological innovations in turbine design and control systems are significantly improving capacity factors and reducing the levelized cost of energy (LCOE), making onshore wind projects more financially viable. As climate goals tighten and energy demand soars, particularly across emerging economies, the global market is on track to witness substantial capacity additions over the next decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $112.1 Billion |

| Forecast Value | $265.5 Billion |

| CAGR | 10.3% |

The steady implementation of federal and state-level incentives, robust government mandates, and aggressive renewable energy targets are acting as strong growth catalysts for the onshore wind energy market. Rapid urbanization, industrial expansion, and increasing energy consumption, especially in developing regions, are further accelerating the deployment of onshore wind projects. Countries such as Brazil, Mexico, and Argentina are emerging as promising markets, offering not only abundant wind resources but also proactive government support and attractive investment frameworks. These countries are witnessing a growing number of project announcements and foreign investments aimed at expanding their wind energy infrastructure. Parallel investments in modernizing grid infrastructure are facilitating better integration of wind power into national energy systems, enhancing the reliability and efficiency of wind-generated electricity.

The onshore wind energy market is segmented into turbines, support structures, electrical infrastructure, and others, with turbines dominating as the leading component. The turbine segment alone is anticipated to generate USD 64 billion by 2034, propelled by the increasing demand for high-capacity, efficient turbines that align with stringent renewable energy mandates. Advancements in turbine technology, including taller towers, longer blades, and sophisticated grid integration capabilities, are enabling higher energy outputs and greater adaptability to diverse wind conditions, making onshore wind installations more attractive for investors and utilities alike.

In terms of turbine rating, systems ranging from 2 MW to 5 MW held 32.8% of the market share in 2024, owing to their optimal balance between capacity, cost, and grid compatibility. These turbines are particularly favored for projects requiring moderate output with spatial or technical constraints. Enhanced control systems and advanced software integrations are also boosting turbine performance, improving energy yields, and minimizing downtime.

North America accounted for 8.6% of the global onshore wind energy market share in 2024, backed by long-term federal incentives and advancements in wind power technology cost-effectiveness. With continuous policy support and technology improvements, North America remains a pivotal region driving future market growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research Design

- 1.2 Base estimates & calculations

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market Definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Component, 2021 – 2034 (USD Million)

- 5.1 Key trends

- 5.2 Turbine

- 5.2.1 Tower

- 5.2.2 Blades

- 5.2.3 Others

- 5.3 Support structure

- 5.3.1 Substructure steel

- 5.3.2 Foundation

- 5.3.3 Others

- 5.4 Electrical infrastructure

- 5.4.1 Wires & Cables

- 5.4.2 Substation

- 5.4.3 Others

- 5.5 Others

Chapter 6 Market Size and Forecast, By Turbine Rating, 2021 – 2034 (USD Million & MW)

- 6.1 Key trends

- 6.2 ≤ 2 MW

- 6.3 >2≤ 5 MW

- 6.4 >5≤ 8 MW

- 6.5 >8≤10 MW

- 6.6 >10≤ 12 MW

- 6.7 > 12 MW

Chapter 7 Market Size and Forecast, By Region, 2021 – 2034 (USD Million & MW)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 Netherlands

- 7.3.3 Sweden

- 7.3.4 France

- 7.3.5 UK

- 7.3.6 Finland

- 7.3.7 Poland

- 7.3.8 Spain

- 7.3.9 Italy

- 7.3.10 Austria

- 7.3.11 Ireland

- 7.3.12 Belgium

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.5 Rest of World

Chapter 8 Company Profiles

- 8.1 CRRC

- 8.2 CSSC Haizhuang Wind Power

- 8.3 Envision Group

- 8.4 Goldwind

- 8.5 GE Vernova

- 8.6 Iberdrola

- 8.7 Nordex

- 8.8 Siemens Gamesa Renewable Energy

- 8.9 United Power

- 8.10 Vestas

- 8.11 Windey Energy Technology Group