|

市场调查报告书

商品编码

1876783

再生金属市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Recycled Metal Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

2024年全球再生金属市场价值为1,281亿美元,预计2034年将以5.4%的复合年增长率成长至2,171亿美元。

市场专注于收集、加工和再利用废弃金属,将其转化为新的原材料,从而减少对原生矿石的开采需求。从车辆、建筑、电子产品和包装等报废产品中回收的金属在环境永续性、节能减排和温室气体减排方面发挥着至关重要的作用。铝、钢、铜和锌可以重复回收而不损失质量,是循环经济的关键组成部分。包括人工智慧驱动的分类、机器人技术、基于感测器的分离以及低排放炉在内的技术进步,显着提高了回收效率。数位追踪和区块链应用正被日益广泛地采用,以确保回收金属的透明度、可追溯性和真实性,使製造商和消费者能够验证供应链的完整性和永续采购实践。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 1281亿美元 |

| 预测值 | 2171亿美元 |

| 复合年增长率 | 5.4% |

预计到2024年,机械加工环节的产值将达到769亿美元,该环节能够高效地对废金属进行破碎、切割和预处理,以便其再利用。热加工环节紧随其后,该环节擅长从成分复杂或受污染的废料中回收金属,透过在高温下熔化和分离,获得适用于工业用途的高纯度金属产品。

2024年,建筑和基础设施领域占据26.5%的市场份额,这主要得益于建筑和土木工程项目对钢铁和铝材的强劲需求。汽车和交通运输行业由于电动和轻型汽车的普及而快速增长。工业机械、电子产品、电气设备、包装和能源公用事业也高度依赖回收金属来实现经济高效且可持续的生产,其应用范围涵盖电路、线路以及可再生能源系统等各个领域。

受汽车和建筑业需求成长的推动,美国再生金属市场规模在2024年达到266亿美元。在北美,电动车、节能基础设施和永续製造实践的普及是推动市场成长的主要动力。加拿大正加大工业废弃物和废弃物回收的投资,以支持循环经济措施。

全球再生金属市场的主要企业包括:Metaloop GmbH、Redwood Materials Inc.、Kuusakoski Group、Steel Dynamics Inc.、Radius Recycling Inc.、Sims Metal Management Limited、Lohum Cleantech Pvt Ltd、Ace Green Recycling Inc.、Nucor Corporation、Europe Metalan Metal,clid、Ace Green。 Alliance、Hensel Recycling GmbH、Novelis Inc.、ScrapBees GmbH、Sortera Technologies Inc. 和 Triple M Metal LP。这些企业正采取多种策略来巩固自身市场地位,包括扩大加工能力、投资先进的分类和冶炼技术以及引入自动化以提高效率。此外,他们还透过建立策略合作伙伴关係和合资企业来增强供应链能力并确保原材料供应。许多企业正致力于数位化、基于区块链的可追溯性以及永续性认证,以吸引具有环保意识的客户。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 不断增长的工业和建筑活动

- 回收製程的技术进步

- 来自汽车和电子行业的需求不断增长

- 成长驱动因素

- 产业陷阱与挑战

- 废金属价格波动

- 缺乏高效率的收集和分类系统

- 市场机会

- 数位技术与自动化的融合

- 绿色产业对再生原料的需求不断成长

- 产品创新与再生金属製造

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 按金属类型

- 未来市场趋势

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 专利格局

- 贸易统计(HS编码)(註:仅提供重点国家的贸易统计资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依金属类型划分,2021-2034年

- 主要趋势

- 黑色金属

- 废钢

- 废铁

- 铸铁

- 有色金属

- 铝

- 原铝废料

- 再生铝合金

- 铜

- 铜线电缆

- 铜管

- 带领

- 电池引线

- 铅片

- 贵金属

- 黄金回收

- 银回收

- 铂族金属

- 特殊金属

- 钛

- 镍

- 稀土元素

- 铝

第六章:市场估算与预测:依废弃物来源划分,2021-2034年

- 主要趋势

- 工业废料(快速废料)

- 製造废弃物流

- 加工厂副产品

- 废弃废料(旧废料)

- 报废车辆

- 拆除的建筑物和基础设施

- 电子垃圾(电子废弃物)

- 家用电器和消费品

- 家庭废料(新废料)

- 钢铁厂回归

- 铸造厂回归

第七章:市场估算与预测:依加工方式划分,2021-2034年

- 主要趋势

- 机械加工

- 粉碎和尺寸缩减

- 磁选

- 密度分离

- 热处理

- 电弧炉(EAF)

- 感应炉

- 火法冶金加工

- 化学加工

- 湿式冶金萃取

- 电解精炼

- 溶剂萃取

- 先进的分选技术

- 人工智慧驱动的光学分选

- 基于感测器的分离

- 雷射诱导击穿光谱(LIBS)

第八章:市场估算与预测:依最终用途产业划分,2021-2034年

- 主要趋势

- 建筑与基础设施

- 结构钢应用

- 加固材料

- 政府基础建设项目

- 汽车与运输

- 车身及车架部件

- 引擎和传动系统部件

- 电动汽车零件

- 製造和工业机械

- 重型设备

- 工业工具及组件

- 电气与电子

- 电线和导线

- 电子元件

- 电池应用

- 包装及容器

- 食品饮料包装

- 工业包装

- 能源与公用事业

- 发电设备

- 再生能源基础设施

- 电网和输电系统

- 航太与国防

- 飞机部件

- 国防应用

- 消费品和家电

- 化工及加工工业

- 海洋与造船

- 其他的

第九章:市场估计与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第十章:公司简介

- Ace Green Recycling Inc.

- Asahi Holdings Inc.

- Batx Energies Private Limited

- Befesa SA

- 欧洲金属回收有限公司

- GFG Alliance

- Hensel Recycling GmbH

- Kuusakoski Group

- Lohum Cleantech Pvt Ltd

- Metaloop GmbH

- Nucor Corporation

- Novelis Inc

- Redwood Materials Inc.

- ScrapBees GmbH

- Radius Recycling Inc.

- Sims Metal Management Limited

- Sortera Technologies Inc

- Steel Dynamics Inc.

- Triple M Metal LP

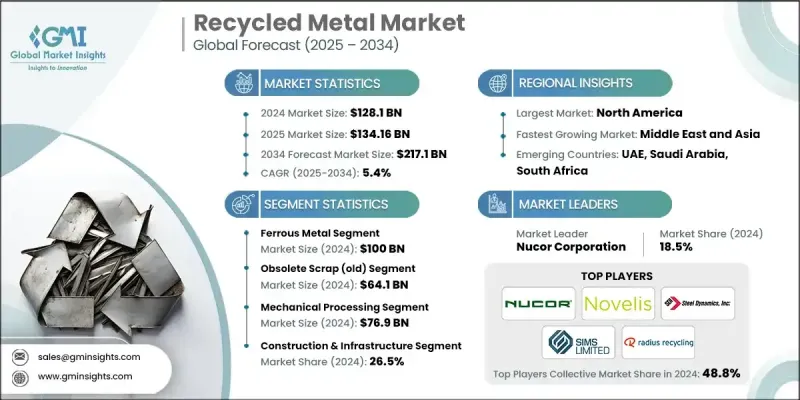

The Global Recycled Metal Market was valued at USD 128.1 billion in 2024 and is estimated to grow at a CAGR of 5.4% to reach USD 217.1 billion by 2034.

The market focuses on collecting, processing, and repurposing used metals into new raw materials, reducing the need for mining virgin ores. Metals recovered from end-of-life products such as vehicles, buildings, electronics, and packaging play a crucial role in environmental sustainability, energy conservation, and greenhouse gas reduction. Aluminium, steel, copper, and zinc can be recycled repeatedly without losing quality, making them key contributors to a circular economy. Technological advancements, including AI-driven sorting, robotics, sensor-based separation, and low-emission furnaces, have significantly enhanced recovery efficiency. Digital tracking and blockchain applications are increasingly being adopted to ensure transparency, traceability, and authenticity of recycled metals, enabling manufacturers and consumers to verify supply chain integrity and sustainable sourcing practices.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $128.1 Billion |

| Forecast Value | $217.1 Billion |

| CAGR | 5.4% |

The mechanical processing segment generated USD 76.9 billion in 2024, as it efficiently shreds, cuts, and prepares scrap metals for reuse. Thermal processing follows, excelling in recovering metals from complex or contaminated scrap by melting and separating them at high temperatures to achieve high-purity outputs suitable for industrial use.

The construction and infrastructure segment held a 26.5% share in 2024, driven by high demand for steel and aluminium in building and civil engineering projects. The automotive and transportation sector is experiencing rapid growth due to the adoption of electric and lightweight vehicles. Industrial machinery, electronics, electrical equipment, packaging, and energy utilities also rely heavily on recycled metals for cost-effective and sustainable production, ranging from circuits and wiring to renewable energy systems.

U.S. Recycled Metal Market reached USD 26.6 billion in 2024, driven by increasing demand from the automotive and construction sectors. In North America, the growth is fueled by the shift toward electric vehicles, energy-efficient infrastructure, and sustainable manufacturing practices. Canada is investing in recovery from industrial and obsolete scrap to support circular economy initiatives.

Key companies operating in the Global Recycled Metal Market include: Metaloop GmbH, Redwood Materials Inc., Kuusakoski Group, Steel Dynamics Inc., Radius Recycling Inc., Sims Metal Management Limited, Lohum Cleantech Pvt Ltd, Ace Green Recycling Inc., Nucor Corporation, European Metal Recycling Limited, Asahi Holdings Inc., Befesa S.A., Batx Energies Private Limited, GFG Alliance, Hensel Recycling GmbH, Novelis Inc., ScrapBees GmbH, Sortera Technologies Inc., Triple M Metal LP. Companies in the recycled metal market are employing several strategies to strengthen their position, including expanding processing capacities, investing in advanced sorting and smelting technologies, and integrating automation to improve efficiency. They are also forming strategic partnerships and joint ventures to enhance supply chain capabilities and secure raw material sources. Many players are focusing on digitalization, blockchain-based traceability, and sustainability certifications to appeal to environmentally conscious customers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Metal Type

- 2.2.2 Scrap Source

- 2.2.3 Processing Method

- 2.2.4 End use Industry

- 2.2.5 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing industrial and construction activities

- 3.2.1.2 Technological advancements in recycling processes

- 3.2.1.3 Increasing demand from automotive and electronics sectors

- 3.2.1 Growth drivers

- 3.3 Industry pitfalls and challenges

- 3.3.1 Fluctuating scrap metal prices

- 3.3.2 Lack of efficient collection and segregation systems

- 3.4 Market opportunities

- 3.4.1 Integration of digital technologies and automation

- 3.4.2 Rising demand for secondary raw materials in green industries

- 3.4.3 Product innovation and recycled metal-based manufacturing

- 3.5 Growth potential analysis

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 Middle East & Africa

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Price trends

- 3.10.1 By region

- 3.10.2 By metal type

- 3.11 Future market trends

- 3.12 Technology and innovation landscape

- 3.12.1 Current technological trends

- 3.12.2 Emerging technologies

- 3.13 Patent landscape

- 3.14 Trade statistics (HS code)( Note: the trade statistics will be provided for key countries only)

- 3.14.1 Major importing countries

- 3.14.2 Major exporting countries

- 3.15 Sustainability and environmental aspects

- 3.15.1 Sustainable practices

- 3.15.2 Waste reduction strategies

- 3.15.3 Energy efficiency in production

- 3.15.4 Eco-friendly initiatives

- 3.16 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Metal Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Ferrous metals

- 5.2.1 Steel scrap

- 5.2.2 Iron scrap

- 5.2.3 Cast iron

- 5.3 Non-ferrous metals

- 5.3.1 Aluminum

- 5.3.1.1 Primary aluminum scrap

- 5.3.1.2 Secondary aluminum alloys

- 5.3.2 Copper

- 5.3.2.1 Copper wire & cable

- 5.3.2.2 Copper tubing & pipe

- 5.3.3 Lead

- 5.3.3.1 Battery lead

- 5.3.3.2 Sheet lead

- 5.3.4 Precious metals

- 5.3.4.1 Gold recovery

- 5.3.4.2 Silver recovery

- 5.3.4.3 Platinum group metals

- 5.3.5 Specialty metals

- 5.3.5.1 Titanium

- 5.3.5.2 Nickel

- 5.3.5.3 Rare earth elements

- 5.3.1 Aluminum

Chapter 6 Market Estimates and Forecast, By Scrap Source, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Industrial scrap (Prompt scrap)

- 6.2.1 Manufacturing waste streams

- 6.2.2 Processing facility byproducts

- 6.3 Obsolete scrap (Old scrap)

- 6.3.1 End-of-life vehicles

- 6.3.2 Demolished buildings & infrastructure

- 6.3.3 Electronic waste (E-waste)

- 6.3.4 Appliances & consumer goods

- 6.4 Home scrap (New scrap)

- 6.4.1 Steel mill revert

- 6.4.2 Foundry returns

Chapter 7 Market Estimates and Forecast, By Processing Method, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Mechanical processing

- 7.2.1 Shredding & size reduction

- 7.2.2 Magnetic separation

- 7.2.3 Density separation

- 7.3 Thermal processing

- 7.3.1 Electric arc furnace (EAF)

- 7.3.2 Induction furnace

- 7.3.3 Pyrometallurgical processing

- 7.4 Chemical processing

- 7.4.1 Hydrometallurgical extraction

- 7.4.2 Electrorefining

- 7.4.3 Solvent extraction

- 7.5 Advanced sorting technologies

- 7.5.1 AI-powered optical sorting

- 7.5.2 Sensor-based separation

- 7.5.3 Laser-induced breakdown spectroscopy (LIBS)

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Construction & infrastructure

- 8.2.1 Structural steel applications

- 8.2.2 Reinforcement materials

- 8.2.3 Government infrastructure projects

- 8.3 Automotive & transportation

- 8.3.1 Body & frame components

- 8.3.2 Engine & drivetrain parts

- 8.3.3 Electric vehicle components

- 8.4 Manufacturing & industrial machinery

- 8.4.1 Heavy equipment

- 8.4.2 Industrial tools & components

- 8.5 Electrical & electronics

- 8.5.1 Wiring & conductors

- 8.5.2 Electronic components

- 8.5.3 Battery applications

- 8.6 Packaging & containers

- 8.6.1 Food & beverage packaging

- 8.6.2 Industrial packaging

- 8.7 Energy & utilities

- 8.7.1 Power generation equipment

- 8.7.2 Renewable energy infrastructure

- 8.7.3 Grid & transmission systems

- 8.8 Aerospace & defense

- 8.8.1 Aircraft components

- 8.8.2 Defense applications

- 8.9 Consumer products & appliances

- 8.10 Chemical & process industries

- 8.11 Marine & shipbuilding

- 8.12 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Ace Green Recycling Inc.

- 10.2 Asahi Holdings Inc.

- 10.3 Batx Energies Private Limited

- 10.4 Befesa S.A.

- 10.5 European Metal Recycling Limited

- 10.6 GFG Alliance

- 10.7 Hensel Recycling GmbH

- 10.8 Kuusakoski Group

- 10.9 Lohum Cleantech Pvt Ltd

- 10.10 Metaloop GmbH

- 10.11 Nucor Corporation

- 10.12 Novelis Inc

- 10.13 Redwood Materials Inc.

- 10.14 ScrapBees GmbH

- 10.15 Radius Recycling Inc.

- 10.16 Sims Metal Management Limited

- 10.17 Sortera Technologies Inc

- 10.18 Steel Dynamics Inc.

- 10.19 Triple M Metal LP

再生铅市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

再生铅市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 金属回收市场-2025-2030年预测

金属回收市场-2025-2030年预测 再生金属市场规模、份额、成长分析(按金属类型、来源、最终用户、地区划分)-2025-2032年产业预测

再生金属市场规模、份额、成长分析(按金属类型、来源、最终用户、地区划分)-2025-2032年产业预测 金属回收市场(按金属类型、最终用途产业、产品形式和收集来源)—2025-2032 年全球预测

金属回收市场(按金属类型、最终用途产业、产品形式和收集来源)—2025-2032 年全球预测 2025年金属回收全球市场报告2025年金属回收设备全球市场报告2025年非铁金属回收全球市场报告

2025年金属回收全球市场报告2025年金属回收设备全球市场报告2025年非铁金属回收全球市场报告 2025 年至 2033 年金属回收市场规模、份额、趋势及预测(依金属类型、最终用途产业及地区划分)

2025 年至 2033 年金属回收市场规模、份额、趋势及预测(依金属类型、最终用途产业及地区划分) 再生钢市场-全球产业规模、份额、趋势、机会及预测(细分、按废料类型、按应用、按加工方法、按最终用户、按地区及竞争情况,2020-2030 年预测)2025年全球再生金属市场报告

再生钢市场-全球产业规模、份额、趋势、机会及预测(细分、按废料类型、按应用、按加工方法、按最终用户、按地区及竞争情况,2020-2030 年预测)2025年全球再生金属市场报告