|

市场调查报告书

商品编码

1664845

冷冻食品加工机械市场机会、成长动力、产业趋势分析及 2024 - 2032 年预测Frozen Food Processing Machinery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2024 - 2032 |

||||||

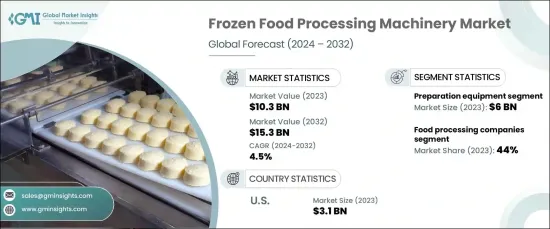

2023 年全球冷冻食品加工机械市场价值为 103 亿美元,预计 2024 年至 2032 年期间将以 4.5% 的强劲复合年增长率成长。速冻和低温方法等冷冻技术的创新在透过保存质地和营养成分来维持食品品质方面发挥关键作用。这对于满足日益增长的冷冻水果、蔬菜和海鲜的需求至关重要。

快餐店(QSR)的扩张和线上食品配送产业的蓬勃发展正在推动冷冻食品产业的成长。这些行业严重依赖冷冻产品,因此需要先进的加工机械来满足高需求。此外,全球超市和大卖场的激增也加速了零售业对冷冻食品的依赖。零售商正在加大对最先进设备的投资,以满足不断变化的消费者偏好并确保产品品质。

| 市场范围 | |

|---|---|

| 起始年份 | 2023 |

| 预测年份 | 2024-2032 |

| 起始值 | 103亿美元 |

| 预测值 | 153亿美元 |

| 复合年增长率 | 4.5% |

儘管取得了重大进步,但小型製造商(尤其是新兴市场的製造商)仍面临明显的障碍。现代设备的高昂前期成本加上预算限制,往往会限制他们使用尖端机械的机会。供应链中断进一步使关键零件和包装材料的供应变得复杂,从而导致生产延迟。这些挑战对于努力在这个充满活力的市场中竞争的小型企业构成了巨大的障碍。

就机械类型而言,製备设备在 2023 年占据市场主导地位,创造了 60 亿美元的收入。预计 2024 年至 2032 年期间,该领域将以约 4.7% 的复合年增长率稳步增长。这些机器确保尺寸和形状的一致性,这对于保持产品品质和优化冷冻过程至关重要。

2023 年,食品加工公司占据了约 44% 的市场份额,预计这一趋势将以类似的成长轨迹持续到 2032 年。因此,对高性能机械的投资激增,使公司能够满足日益增长的消费者期望。

美国仍然是冷冻食品加工机械市场的主导者,2023 年市场价值为 31 亿美元。这些进步正在提高生产效率、改善产品品质并满足美国食品加工行业日益增长的需求。

目录

第 1 章:方法论与范围

- 市场范围和定义

- 基础估算与计算

- 预测计算

- 资料来源

- 基本的

- 次要

- 付费来源

- 公共资源

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 供应商概况

- 利润率分析

- 重要新闻及倡议

- 监管格局

- 衝击力

- 成长动力

- 冷冻食品需求不断成长

- 技术进步

- 产业陷阱与挑战

- 高资本投入

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第 5 章:市场估计与预测:按机械类型,2021-2032 年

- 主要趋势

- 製备设备

- 切刀

- 搅拌机

- 切片机

- 磨床

- 其他(削皮器等)

- 冷冻设备

- 速冻机

- 螺旋速冻机

- 平板冷冻机

- 个体速冻(IQF)设备

- 其他(隧道冷冻机等)

- 包装设备

- 包装机

- 装袋机

- 装盒机

- 其他(真空包装机等)

- 其他(仓储设备、传送带等)

第六章:市场估计与预测:依技术,2021-2032 年

- 主要趋势

- 机械冷冻

- 低温冷冻

第 7 章:市场估计与预测:按营运模式,2021 年至 2032 年

- 主要趋势

- 半自动

- 自动的

第 8 章:市场估计与预测:按应用,2021 年至 2032 年

- 主要趋势

- 水果和蔬菜

- 乳製品

- 肉类、家禽和海鲜

- 即食食品

- 烘焙产品

- 小吃

- 其他(汤、酱汁等)

第 9 章:市场估计与预测:按最终用途,2021-2032 年

- 主要趋势

- 食品加工公司

- 餐厅及餐饮服务

- 零售和超市

- 其他(配送中心等)

第 10 章:市场估计与预测:按地区,2021-2032 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中东及非洲

- 阿联酋

- 沙乌地阿拉伯

- 南非

第 11 章:公司简介

- Air Products and Chemicals, Inc.

- Alfa Laval AB

- Bühler Group

- GEA Group AG

- Griffith Foods Inc.

- Hoshizaki Corporation

- Intralox

- JBT Corporation

- Marel

- OctoFrost Group

- SPX FLOW, Inc.

- Starfrost (UK) Ltd.

- Tetra Pak International SA

- The Middleby Corporation

The Global Frozen Food Processing Machinery Market was valued at USD 10.3 billion in 2023 and is projected to grow at a robust CAGR of 4.5% from 2024 to 2032. Driving this growth are advancements in automation, artificial intelligence (AI), and machine learning, which are revolutionizing food processing machinery by enhancing efficiency and cutting costs. Innovations in freezing technologies, such as quick freezing and cryogenic methods, are playing a pivotal role in maintaining food quality by preserving texture and nutrients. This is crucial for meeting the rising demand for frozen fruits, vegetables, and seafood.

The expansion of quick-service restaurants (QSRs) and the booming online food delivery sector are fueling the frozen food industry's growth. These sectors rely heavily on frozen products, spurring the need for advanced processing machinery to meet high demand. Additionally, the global proliferation of supermarkets and hypermarkets is accelerating the retail sector's reliance on frozen foods. Retailers are increasingly investing in state-of-the-art equipment to cater to evolving consumer preferences and ensure product quality.

| Market Scope | |

|---|---|

| Start Year | 2023 |

| Forecast Year | 2024-2032 |

| Start Value | $10.3 Billion |

| Forecast Value | $15.3 Billion |

| CAGR | 4.5% |

Despite significant advancements, smaller manufacturers, especially in emerging markets, face notable obstacles. High upfront costs for modern equipment, coupled with budget constraints, often limit their access to cutting-edge machinery. Supply chain disruptions further complicate the availability of critical components and packaging materials, leading to production delays. These challenges pose substantial barriers for smaller players striving to compete in this dynamic market.

In terms of machinery type, preparation equipment dominated the market in 2023, generating USD 6 billion in revenue. This segment is anticipated to grow at a steady CAGR of approximately 4.7% from 2024 to 2032. Preparation equipment-comprising tools for slicing, cutting, blending, and grinding-plays a critical role in frozen food production. These machines ensure consistency in size and shape, which is essential for maintaining product quality and optimizing freezing processes.

Food processing companies accounted for approximately 44% of the market share in 2023, and this trend is expected to continue with a similar growth trajectory through 2032. The rising demand for convenience foods with extended shelf lives has led to increased production among these companies. Consequently, investments in high-performance machinery have surged, enabling companies to meet growing consumer expectations.

The United States remains a dominant player in the frozen food processing machinery market, valued at USD 3.1 billion in 2023. The market is forecasted to expand at a CAGR of 4.9% from 2024 to 2032, driven by continuous innovation in freezing technologies. These advancements are enhancing production efficiency, improving product quality, and supporting the growing needs of the US food processing industry.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2032

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rising demand for frozen foods

- 3.6.1.2 Technological advancements

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High capital investment

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Machinery Type, 2021-2032 (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Preparation equipment

- 5.2.1 Cutters

- 5.2.2 Blenders

- 5.2.3 Slicers

- 5.2.4 Grinders

- 5.2.5 Others (Peelers, Etc)

- 5.3 Freezing Equipment

- 5.3.1 Blast freezers

- 5.3.2 Spiral freezers

- 5.3.3 Plate freezers

- 5.3.4 Individual Quick Freezing (IQF) Equipment

- 5.3.5 Others (Tunnel Freezers, Etc)

- 5.4 Packaging equipment

- 5.4.1 Wrapping machines

- 5.4.2 Bagging machines

- 5.4.3 Cartoning machines

- 5.4.4 Others (Vacuum Packaging Machines, Etc)

- 5.5 Others (Storage Equipment, Conveyors, Etc)

Chapter 6 Market Estimates & Forecast, By Technology, 2021-2032 (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Mechanical freezing

- 6.3 Cryogenic freezing

Chapter 7 Market Estimates & Forecast, By Mode of Operation, 2021-2032 (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Semi-Automatic

- 7.3 Automatic

Chapter 8 Market Estimates & Forecast, By Application, 2021-2032 (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Fruits & vegetables

- 8.3 Dairy products

- 8.4 Meat, poultry, & seafood

- 8.5 Ready-to-Eat (RTE) meals

- 8.6 Bakery products

- 8.7 Snacks

- 8.8 Others (Soups, Sauces, Etc)

Chapter 9 Market Estimates & Forecast, By End Use, 2021-2032 (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Food processing companies

- 9.3 Restaurants and foodservice

- 9.4 Retail & supermarkets

- 9.5 Others (Distribution Centers, Etc)

Chapter 10 Market Estimates & Forecast, By Region, 2021-2032 (USD Million) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Air Products and Chemicals, Inc.

- 11.2 Alfa Laval AB

- 11.3 Bühler Group

- 11.4 GEA Group AG

- 11.5 Griffith Foods Inc.

- 11.6 Hoshizaki Corporation

- 11.7 Intralox

- 11.8 JBT Corporation

- 11.9 Marel

- 11.10 OctoFrost Group

- 11.11 SPX FLOW, Inc.

- 11.12 Starfrost (UK) Ltd.

- 11.13 Tetra Pak International S.A.

- 11.14 The Middleby Corporation