|

市场调查报告书

商品编码

1664898

公用事业併网光伏逆变器市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测Utility On Grid PV Inverter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

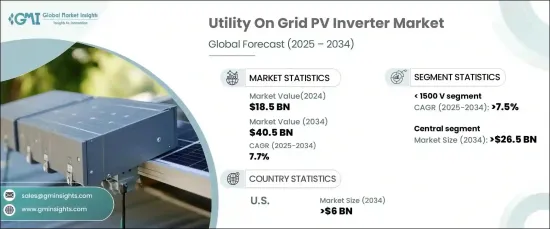

全球公用事业併网光伏逆变器市场预计将经历显着增长,到 2024 年达到 185 亿美元的价值,预计 2025 年至 2034 年的复合年增长率为 7.7%。这些逆变器旨在处理从数百千瓦到几兆瓦的高功率输出,提供效率、可靠性和无缝电网合规性。

市场按产品类型细分,其中中央逆变器占据领先地位。预计到 2034 年,中央逆变器将产生 265 亿美元的收入,它因能够管理高功率需求而特别受欢迎,使其成为公用事业规模太阳能专案的理想选择。这些逆变器以其成本效益和易于维护而闻名,这对于大规模安装至关重要。此外,中央逆变器配备了无功功率控制、电压调节和频率响应等先进功能,所有这些功能都确保符合电网标准并有助于整体电网稳定性。这些功能使中央逆变器成为市场成长的主要驱动力。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 185亿美元 |

| 预测值 | 405亿美元 |

| 复合年增长率 | 7.7% |

就标称输出电压而言,到 2034 年,输出低于 1500V 的逆变器预计以 7.5% 的复合年增长率增长。对于能够支援更高功率输出的逆变器的需求不断增加,特别是在大型公用事业规模的应用中,将进一步加速其采用。此外,各个地区不断升级电网基础设施以支援更高电压的太阳能连接,这将推动对这些逆变器的需求。

预计到 2034 年,美国公用事业併网光伏逆变器市场将创收 60 亿美元。这些政策正在刺激对太阳能技术的投资并推动公用事业併网光伏逆变器的采用。此外,美国正在向更加分散和有弹性的能源电网转变,同时太阳能技术成本下降,这进一步支持了该市场的成长。

目录

第 1 章:方法论与范围

- 研究设计

- 基础估算与计算

- 预测模型

- 初步研究与验证

- 主要来源

- 资料探勘来源

- 市场定义

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统

- 监管格局

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- PESTEL 分析

第四章:竞争格局

- 介绍

- 战略仪表板

- 创新与技术格局

第 5 章:市场规模及预测:依产品,2021 – 2034 年

- 主要趋势

- 细绳

- 中央

第 6 章:市场规模及预测:依标称输出电压,2021 – 2034 年

- 主要趋势

- < 1500 伏

- ≥1500V

第 7 章:市场规模与预测:按地区,2021 – 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 义大利

- 波兰

- 荷兰

- 奥地利

- 英国

- 法国

- 亚太地区

- 中国

- 澳洲

- 印度

- 日本

- 韩国

- 中东和非洲

- 以色列

- 沙乌地阿拉伯

- 阿联酋

- 南非

- 拉丁美洲

- 巴西

- 墨西哥

- 智利

第八章:公司简介

- Canadian Solar

- Delta Electronics

- Eaton

- Enphase Energy

- Fimer Group

- GoodWe

- Schneider Electric

- SMA Solar Technology

- Sungrow Power Supply

- Solis Inverters

- SolarEdge Technologies

- V-Guard Industries

The Global Utility On Grid PV Inverter Market is expected to experience significant growth, reaching a value of USD 18.5 billion in 2024 and a projected CAGR of 7.7% from 2025 to 2034. PV inverters play a crucial role in large-scale solar energy systems by converting direct current (DC) from photovoltaic (PV) panels into alternating current (AC), which is synchronized with the utility grid. These inverters are built to handle high power outputs, ranging from hundreds of kilowatts to several megawatts, offering efficiency, reliability, and seamless grid compliance.

The market is segmented by product type, with central inverters leading the way. Expected to generate USD 26.5 billion by 2034, central inverters are particularly sought after for their ability to manage high power demands, making them ideal for utility-scale solar projects. These inverters are known for their cost-efficiency and easy maintenance, which are essential for large-scale installations. Furthermore, central inverters come equipped with advanced features like reactive power control, voltage regulation, and frequency response, all of which ensure compliance with grid standards and contribute to overall grid stability. These capabilities have made central inverters a key driver of growth in the market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $18.5 Billion |

| Forecast Value | $40.5 Billion |

| CAGR | 7.7% |

In terms of nominal output voltage, inverters with outputs below 1500V are expected to grow at a CAGR of 7.5% through 2034. This growth is fueled by the demand for greater efficiency and the need to reduce electrical losses during long-distance power transmission. The increasing requirement for inverters capable of supporting higher power outputs, especially in large utility-scale applications, will further accelerate adoption. Additionally, the ongoing upgrade of grid infrastructure in various regions to support higher-voltage solar connections will drive demand for these inverters.

The U.S. utility on-grid PV inverter market is projected to generate USD 6 billion by 2034. The market's growth is primarily driven by robust government support for renewable energy, with initiatives like the Investment Tax Credit (ITC) and renewable energy standards. These policies are stimulating investment in solar technology and boosting the adoption of utility on-grid PV inverters. Additionally, the U.S. is experiencing a shift toward a more decentralized and resilient energy grid, alongside falling costs for solar technology, which further supports the growth of this market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Product, 2021 – 2034 (USD Billion & MW)

- 5.1 Key trends

- 5.2 String

- 5.3 Central

Chapter 6 Market Size and Forecast, By Nominal Output Voltage, 2021 – 2034 (USD Billion & MW)

- 6.1 Key trends

- 6.2 < 1500 V

- 6.3 ≥ 1500 V

Chapter 7 Market Size and Forecast, By Region, 2021 – 2034 (USD Billion & MW)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 Italy

- 7.3.3 Poland

- 7.3.4 Netherlands

- 7.3.5 Austria

- 7.3.6 UK

- 7.3.7 France

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 India

- 7.4.4 Japan

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Israel

- 7.5.2 Saudi Arabia

- 7.5.3 UAE

- 7.5.4 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Mexico

- 7.6.3 Chile

Chapter 8 Company Profiles

- 8.1 Canadian Solar

- 8.2 Delta Electronics

- 8.3 Eaton

- 8.4 Enphase Energy

- 8.5 Fimer Group

- 8.6 GoodWe

- 8.7 Schneider Electric

- 8.8 SMA Solar Technology

- 8.9 Sungrow Power Supply

- 8.10 Solis Inverters

- 8.11 SolarEdge Technologies

- 8.12 V-Guard Industries

高频太阳能逆变器市场-全球产业规模、份额、趋势、机会和预测,按产品类型、应用、功率等级、配销通路、地区和竞争进行细分,2020-2030 年预测

高频太阳能逆变器市场-全球产业规模、份额、趋势、机会和预测,按产品类型、应用、功率等级、配销通路、地区和竞争进行细分,2020-2030 年预测 2024-2035年全球太阳能光电逆变器产业

2024-2035年全球太阳能光电逆变器产业 併网光电逆变器市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

併网光电逆变器市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 光伏逆变器市场(按产品、组件、类型、相位、输出功率、销售管道和应用)—2025-2030 年全球预测

光伏逆变器市场(按产品、组件、类型、相位、输出功率、销售管道和应用)—2025-2030 年全球预测 太阳能逆变器:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

太阳能逆变器:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年) 2025年全球住宅太阳能逆变器市场报告2025年全球太阳能逆变器市场报告

2025年全球住宅太阳能逆变器市场报告2025年全球太阳能逆变器市场报告 光伏逆变器市场(按产品、最终用途和地区划分)全球商业和工业光伏逆变器市场研究报告 - 行业分析、规模、份额、成长、趋势和预测 2025 年至 2033 年全球太阳能微型逆变器市场研究报告 - 产业分析、规模、份额、成长、趋势和预测 2025 年至 2033 年

光伏逆变器市场(按产品、最终用途和地区划分)全球商业和工业光伏逆变器市场研究报告 - 行业分析、规模、份额、成长、趋势和预测 2025 年至 2033 年全球太阳能微型逆变器市场研究报告 - 产业分析、规模、份额、成长、趋势和预测 2025 年至 2033 年