|

市场调查报告书

商品编码

1665028

汽车整合电源模组市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Automotive Integrated Power Module Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

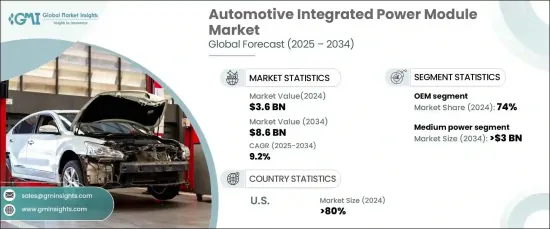

2024 年全球汽车整合电源模组市场价值 36 亿美元,预计将经历显着增长,预计 2025 年至 2034 年的复合年增长率为 9.2%。随着电动车需求的不断增长,汽车整合电源模组在管理车辆电池、电动马达和其他重要部件之间的电力转换方面发挥着至关重要的作用,确保车辆的最佳性能。

市场按功率位准分类,包括低功率、中功率和高功率部分。 2024 年,中等功率模组占据了 40% 的市场份额,预计到 2034 年将达到 30 亿美元。透过增强电源转换、马达控制和电池管理,中等功率模组优化了能源效率,提高了车辆性能和燃油经济性。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 36亿美元 |

| 预测值 | 86亿美元 |

| 复合年增长率 | 9.2% |

就销售通路而言,市场分为两个主要类别: OEM (原始设备製造商)和售后市场。到 2024 年, OEM部门将占据市场主导地位,占有 74% 的份额。更高效、更具成本效益的半导体材料的开发,具有更高的热导率、更高的效率和更快的开关速度,正在推动OEM 的采用。这些创新越来越多地融入电动和混合动力汽车的动力系统中,帮助汽车製造商提高汽车性能并最大限度地提高能源效率。

2024 年,美国汽车整合电源模组市场将占据 80% 的主导份额,这一趋势反映了美国混合动力和电动车产量的快速成长。随着主要汽车製造商大力投资电动车和混合动力车的生产,对高性能电力电子设备的需求日益增加。此外,政府旨在扩大电动车基础设施的倡议,例如增加充电站数量和向电动车购买者提供奖励,进一步推动了市场成长并加速了电动车的普及。

这个不断成长的市场证明了汽车整合功率模组在汽车产业发展中发挥的关键作用,推动了技术创新和更高的能源效率。随着对电动和混合动力汽车的需求不断增长,汽车整合电源模组市场将蓬勃发展,有助于开发更环保、更有效率的交通解决方案。

目录

第 1 章:方法论与范围

- 研究设计

- 研究方法

- 资料收集方法

- 基础估算与计算

- 基准年计算

- 市场估计的主要趋势

- 预测模型

- 初步研究和验证

- 主要来源

- 资料探勘来源

- 市场范围和定义

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 原物料供应商

- 组件提供者

- 生产

- 经销商

- 最终用途

- 供应商概况

- 利润率分析

- 技术与创新格局

- 专利分析

- 重要新闻及倡议

- 监管格局

- 案例研究

- 衝击力

- 成长动力

- 电动和混合动力车的普及率不断提高

- 电力电子技术进步

- 对能源效率和性能的需求

- 监理推动燃油效率和减排

- 产业陷阱与挑战

- 整合式电源模组成本较高

- 设计与製造的复杂性

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:按功率,2021 - 2034 年

- 主要趋势

- 低功耗

- 中等功率

- 高功率

第 6 章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 动力传动系统

- 电池管理系统

- 热管理系统

- 充电系统

- 其他的

第七章:市场估计与预测:依车型,2021 - 2034 年

- 主要趋势

- 搭乘用车

- 掀背车

- 轿车

- 越野车

- 商用车

- 轻型商用车 (LCV)

- 重型商用车 (HCV)

第 8 章:市场估计与预测:按销售管道,2021 - 2034 年

- 主要趋势

- OEM

- 售后市场

第 9 章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东及非洲

- 阿联酋

- 南非

- 沙乌地阿拉伯

第十章:公司简介

- Analog Devices

- Autotalks Ltd

- Denso

- Dialog

- Fuji

- Infineon

- Littelfuse

- Maxim

- Mitsubishi

- NXP Semiconductors

- ON Semiconductor

- Renesas

- Rohm

- Semikron

- STMicroelectronics

- Texas

- Toshiba

- Vishay

- Wolfspeed

The Global Automotive Integrated Power Module Market was valued at USD 3.6 billion in 2024 and is expected to experience significant growth, with a projected CAGR of 9.2% from 2025 to 2034. This surge in market expansion is largely driven by the increasing shift toward electric vehicles (EVs), as stricter emissions regulations and government incentives continue to promote eco-friendly transportation solutions. As the demand for EVs rises, automotive integrated power modules play a crucial role in managing the power conversion between the vehicle's battery, electric motor, and other vital components, ensuring optimal vehicle performance.

The market is categorized by power levels, including low power, medium power, and high power segments. In 2024, the medium power segment accounted for 40% of the market share and is expected to reach USD 3 billion by 2034. These modules are especially important for hybrid electric vehicles (HEVs), where they balance the energy flow between the internal combustion engine (ICE) and the electric motor. By enhancing power conversion, motor control, and battery management, medium power modules optimize energy efficiency, improving both vehicle performance and fuel economy.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.6 Billion |

| Forecast Value | $8.6 Billion |

| CAGR | 9.2% |

In terms of sales channels, the market is divided into two key categories: OEM (Original Equipment Manufacturer) and aftermarket. The OEM segment dominated the market with a substantial 74% share in 2024. This growth is fueled by ongoing advancements in power semiconductor technologies. The development of more efficient, cost-effective semiconductor materials offering higher thermal conductivity, improved efficiency, and faster switching speeds is driving OEM adoption. These innovations are increasingly incorporated into the powertrains of electric and hybrid vehicles, helping automakers enhance vehicle performance and maximize energy efficiency.

The U.S. automotive integrated power module market held a dominant 80% share in 2024, a trend that reflects the nation's rapid growth in the production of hybrid and electric vehicles. With major automakers heavily investing in EV and HEV production, there is an escalating demand for high-performance power electronics. Additionally, government initiatives aimed at expanding EV infrastructure, such as increasing the number of charging stations and offering incentives to electric vehicle buyers, are further fueling market growth and accelerating the adoption of electric vehicles.

This growing market demonstrates the crucial role that automotive integrated power modules play in the evolution of the automotive industry, driving both technological innovation and greater energy efficiency. As the demand for electric and hybrid vehicles continues to rise, the market for automotive integrated power modules is set to thrive, contributing to the development of greener, more efficient transportation solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material providers

- 3.1.2 Component providers

- 3.1.3 Manufacture

- 3.1.4 Distributors

- 3.1.5 End Use

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Case study

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Growing adoption of electric and hybrid vehicles

- 3.9.1.2 Technological advancements in power electronics

- 3.9.1.3 Demand for energy efficiency and performance

- 3.9.1.4 Regulatory push for fuel efficiency and emissions reduction

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High cost of integrated power module

- 3.9.2.2 Complexity in design and manufacturing

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Power, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Low power

- 5.3 Medium power

- 5.4 High power

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Powertrain system

- 6.3 Battery management system

- 6.4 Thermal management system

- 6.5 Charging system

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger vehicle

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial Vehicle

- 7.3.1 Light Commercial Vehicles (LCVs)

- 7.3.2 Heavy Commercial Vehicles (HCVs)

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Analog Devices

- 10.2 Autotalks Ltd

- 10.3 Denso

- 10.4 Dialog

- 10.5 Fuji

- 10.6 Infineon

- 10.7 Littelfuse

- 10.8 Maxim

- 10.9 Mitsubishi

- 10.10 NXP Semiconductors

- 10.11 ON Semiconductor

- 10.12 Renesas

- 10.13 Rohm

- 10.14 Semikron

- 10.15 STMicroelectronics

- 10.16 Texas

- 10.17 Toshiba

- 10.18 Vishay

- 10.19 Wolfspeed

2026-2030年全球汽车配电市场

2026-2030年全球汽车配电市场 汽车48伏特电子接线盒及配电中心市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

汽车48伏特电子接线盒及配电中心市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 汽车配电模组市场:材料类型、销售管道、车辆类型、产品类型和额定电流划分 - 全球预测 2025-2032

汽车配电模组市场:材料类型、销售管道、车辆类型、产品类型和额定电流划分 - 全球预测 2025-2032 48v低压电电力供给网路(PDN)架构和供应链全景(2025年)汽车配电模组市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

48v低压电电力供给网路(PDN)架构和供应链全景(2025年)汽车配电模组市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 全球汽车配电模组市场规模(按组件类型、车辆类型、电压类型、地区、范围和预测)全球汽车配电块市场规模(按类型、组件、车辆类型、地区、范围和预测)

全球汽车配电模组市场规模(按组件类型、车辆类型、电压类型、地区、范围和预测)全球汽车配电块市场规模(按类型、组件、车辆类型、地区、范围和预测) 2023-2030年全球汽车配电模组市场规模研究与预测(以组件类型依车辆类型依电压类型及区域分析)

2023-2030年全球汽车配电模组市场规模研究与预测(以组件类型依车辆类型依电压类型及区域分析)