|

市场调查报告书

商品编码

1665099

正庚烷市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测n-Heptane Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

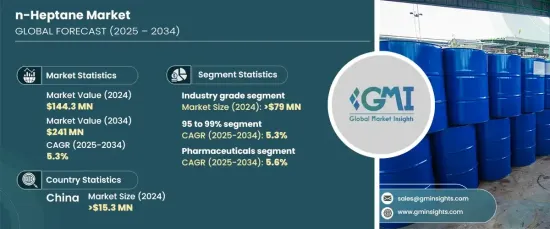

2024 年全球正庚烷市场价值达到 1.443 亿美元,预计 2025 年至 2034 年期间将实现强劲增长,复合年增长率为 5.3%。这一增长得益于工业需求的不断增长、应用范围的不断扩大以及汽车、製药和化学品等各个领域的重大发展。正庚烷用途广泛,在化学过程和燃料测试中被广泛用作溶剂,这使其成为众多行业中不可或缺的材料。随着主要经济体的需求不断增长,市场有望稳步扩张,特别是在工业基础设施强大的国家。此外,对研究和产品创新的日益关注将有助于市场的发展。随着产业寻求高效、高性能材料,正庚烷的应用将持续发展,进一步推动市场成长。

2024 年,工业级细分市场引领正庚烷市场,估值达到 7,900 万美元,预计到 2034 年复合年增长率为 5.1%。工业级正庚烷常用于黏合剂、涂料和燃料测试,可为非关键应用提供可靠的性能。此外,它在化学合成和橡胶製造方面发挥关键作用,尤其是在工业框架完善的地区。它在这些领域的广泛应用有助于保持其在市场上的强势地位。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 1.443亿美元 |

| 预测值 | 2.41亿美元 |

| 复合年增长率 | 5.3% |

2024 年,纯度为 95% 至 99% 的市场占据主导地位,创造了 7,210 万美元的收入,预计到 2034 年的复合年增长率为 5.3%。它广泛用于实验室的分析目的和化学合成,这些场合高精度是至关重要的。此外,它在燃料性能测试和药物配方中的作用凸显了其在需要高精度和卓越品质的领域中的重要作用。

中国已成为亚太正庚烷市场的重要参与者,到 2024 年贡献 1,530 万美元,预测期内预期成长率为 6.3%。中国强劲的化学工业和汽车工业是需求激增的驱动力。中国快速扩张的工业基础,加上都市化和基础设施的改善,巩固了在全球正庚烷市场的地位。随着黏合剂、涂料、医药等领域的应用不断增加,中国的市场潜力持续成长。

在工业扩张、产品进步和各类应用对高品质溶剂的需求不断增长的推动下,正庚烷市场可望大幅成长。随着产业不断优先考虑性能,正庚烷在製造和研究过程中的重要性将不断提高,巩固其在全球市场的地位。

目录

第 1 章:方法论与范围

- 市场范围和定义

- 基础估算与计算

- 预测计算

- 资料来源

- 基本的

- 次要

- 付费来源

- 公共资源

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 供应商概况

- 利润率分析

- 重要新闻及倡议

- 监管格局

- 衝击力

- 成长动力

- 实验室和工业应用对高纯度溶剂的需求不断增加

- 不断增长的能源需求推动石化测试

- 扩大製药和黏合剂製造业

- 产业陷阱与挑战

- 限制使用挥发性有机化合物 (VOC) 的严格环境法规

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:依等级,2021-2034 年

- 主要趋势

- 工业级

- 医药级

第 6 章:市场估计与预测:按纯度,2021-2034 年

- 主要趋势

- <95%

- 95 至 99%

- ≥99%

第 7 章:市场估计与预测:按应用,2021 年至 2034 年

- 主要趋势

- 药品

- 油漆和涂料

- 电子产品

- 黏合剂和密封剂

- 塑胶和聚合物

- 化学合成

- 其他的

第 8 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中东及非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- Chevron Phillips Chemical

- Chuzhou Runda Solvents

- DHC Solvent Chemie

- Gadiv Petrochemical Industries

- Haltermann Carless Deutschland

- Hanwha Total Petrochemical

- Henan Haofei Chemical

- Liaoning Yufeng Chemical

- Mehta Petro-Refineries

- Royal Dutch Shell

- Sankyo Chemical

- Shenyang Huifeng Petrochemical

- SK Global Chemical

The Global N-Heptane Market reached a valuation of USD 144.3 million in 2024, and it is expected to experience robust growth with a CAGR of 5.3% from 2025 to 2034. This growth is being fueled by rising industrial demand, an expanding range of applications, and significant developments in various sectors, including automotive, pharmaceuticals, and chemicals. N-heptane's versatility and wide adoption as a solvent in chemical processes and fuel testing make it indispensable across numerous industries. With its growing demand in key economies, the market is positioned for steady expansion, particularly in countries with strong industrial infrastructures. Furthermore, the increasing focus on research and product innovations will contribute to the market development. As industries seek efficient and high-performance materials, n-heptane's applications will continue to evolve, further driving market growth.

In 2024, the industry-grade segment led the n-heptane market, reaching a valuation of USD 79 million, and it is expected to grow at a CAGR of 5.1% through 2034. This segment's dominance is attributed to its cost-effectiveness and suitability for a range of industrial processes. Often utilized in adhesives, coatings, and fuel testing, the industry-grade n-heptane offers reliable performance for non-critical applications. Additionally, it plays a key role in chemical synthesis and rubber manufacturing, especially in regions with a well-established industrial framework. Its broad usage across these sectors helps maintain its strong position in the market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $144.3 Million |

| Forecast Value | $241 Million |

| CAGR | 5.3% |

The 95% to 99% purity segment dominated the market in 2024, generating USD 72.1 million in revenue, with a projected CAGR of 5.3% through 2034. N-heptane within this purity range is highly sought after due to its ability to meet the rigorous demands of industries requiring precise formulations. It is widely used in laboratories for analytical purposes and chemical synthesis, where high accuracy is paramount. Furthermore, its role in fuel performance testing and pharmaceutical formulations highlights its essential use in sectors that require high precision and exceptional quality.

China has emerged as a key player in the Asia-Pacific n-heptane market, contributing USD 15.3 million in 2024, with an expected growth rate of 6.3% during the forecast period. The country's robust chemical and automotive industries are the driving force behind this surge in demand. China's rapidly expanding industrial base, coupled with urbanization and improved infrastructure, strengthens its position in the global n-heptane market. With increasing applications in sectors like adhesives, coatings, and pharmaceuticals, China's market potential continues to grow.

The n-heptane market is poised for substantial growth, driven by industrial expansion, product advancements, and the increasing demand for high-quality solvents in various applications. As industries continue to prioritize performance, n-heptane's significance in manufacturing and research processes will continue to rise, solidifying its place in the global marketplace.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing demand for high-purity solvents in laboratories and industrial applications

- 3.6.1.2 Rising energy demands fueling petrochemical testing

- 3.6.1.3 Expansion of the pharmaceutical and adhesive manufacturing industries

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Stringent environmental regulations restricting the use of volatile organic compounds (VOCs)

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Grade, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Industry grade

- 5.3 Pharmaceutical grade

Chapter 6 Market Estimates & Forecast, By Purity, 2021-2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 <95%

- 6.3 95 to 99%

- 6.4 ≥99%

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Pharmaceuticals

- 7.3 Paints & coatings

- 7.4 Electronics

- 7.5 Adhesives & sealants

- 7.6 Plastic & polymers

- 7.7 Chemical synthesis

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Chevron Phillips Chemical

- 9.2 Chuzhou Runda Solvents

- 9.3 DHC Solvent Chemie

- 9.4 Gadiv Petrochemical Industries

- 9.5 Haltermann Carless Deutschland

- 9.6 Hanwha Total Petrochemical

- 9.7 Henan Haofei Chemical

- 9.8 Liaoning Yufeng Chemical

- 9.9 Mehta Petro-Refineries

- 9.10 Royal Dutch Shell

- 9.11 Sankyo Chemical

- 9.12 Shenyang Huifeng Petrochemical

- 9.13 SK Global Chemical

脂肪族烃溶剂和稀释剂市场-全球产业规模、份额、趋势、机会和预测,按类型、应用、地区和竞争格局划分,2020-2030年预测

脂肪族烃溶剂和稀释剂市场-全球产业规模、份额、趋势、机会和预测,按类型、应用、地区和竞争格局划分,2020-2030年预测 涂料稀释剂市场报告:趋势、预测和竞争分析(至 2031 年)

涂料稀释剂市场报告:趋势、预测和竞争分析(至 2031 年) 脂肪族烃溶剂和稀释剂:市场占有率分析、产业趋势和统计、成长预测(2025-2030 年)半导体薄板市场报告:2030 年趋势、预测与竞争分析

脂肪族烃溶剂和稀释剂:市场占有率分析、产业趋势和统计、成长预测(2025-2030 年)半导体薄板市场报告:2030 年趋势、预测与竞争分析 全球正庚烷市场-全球产业分析、规模、占有率、成长、趋势、预测(2031)- 依产品类型、依应用、依地区

全球正庚烷市场-全球产业分析、规模、占有率、成长、趋势、预测(2031)- 依产品类型、依应用、依地区 正庚烷的全球市场分析:工厂产能、产量、运营效率、需求/供应、最终用户行业、销售渠道、区域需求 (2015-2035)

正庚烷的全球市场分析:工厂产能、产量、运营效率、需求/供应、最终用户行业、销售渠道、区域需求 (2015-2035)