|

市场调查报告书

商品编码

1665232

石油和天然气云端运算市场机会、成长动力、产业趋势分析和 2025 - 2034 年预测Cloud Computing in Oil and Gas Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

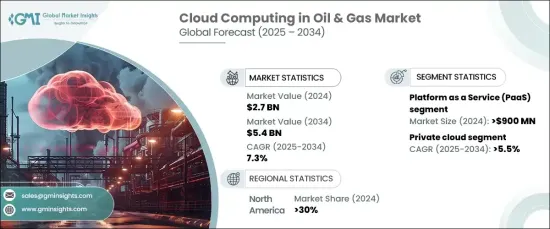

2024资料全球石油和天然气云端运算市场价值为 27 亿美元,预计 2025 年至 2034 年期间将以 7.3% 的复合年增长率强劲增长。随着石油和天然气公司努力实现营运现代化,整合云端技术可以提供更大的灵活性,从而能够更快地响应市场波动并实现更有效率的资源管理。

2024 年,市场将分为几种主要服务产品:基础设施即服务 (IaaS)、平台即服务 (PaaS) 和软体即服务 (SaaS)。其中,PaaS领域占据了相当大的市场份额,价值达9亿美元。由于其能够简化应用程式开发和管理,消除维护底层基础设施的复杂性,因此该领域正在迅速扩张。透过采用 PaaS 解决方案,石油和天然气公司可以简化开发流程、缩短产品上市时间并根据需求轻鬆扩展资源。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 27亿美元 |

| 预测值 | 54亿美元 |

| 复合年增长率 | 7.3% |

石油和天然气领域的云端运算也按部署模式细分,包括公有、私有和混合云端解决方案。预计资料2025 年到 2034 年,私有云领域将以 5.5% 的复合年增长率稳步增长。透过私有云部署,石油和天然气公司可以更好地控制资料隐私,同时受益于云端技术的可扩展性和灵活性。在遵守严格监管标准不容商榷的行业中,这一点尤其重要。

在美国,石油和天然气云端运算市场在 2024 年占据了 30% 的份额。作为数位转型策略的一部分,美国主要的石油和天然气公司正在大力投资云端基础设施。此外,该地区强大的监管框架和对先进资料分析解决方案日益增长的需求,正在加速云端运算在从勘探到分销等广泛的石油和天然气业务中的整合。

目录

第 1 章:方法论与范围

- 研究设计

- 研究方法

- 资料收集方法

- 基础估算与计算

- 基准年计算

- 市场估计的主要趋势

- 预测模型

- 初步研究和验证

- 主要来源

- 资料探勘来源

- 市场范围和定义

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 供应商概况

- 软体供应商

- 服务提供者

- 石油和天然气营运商

- 经销商

- 最终用户

- 利润率分析

- 技术与创新格局

- 专利分析

- 监管格局

- 使用案例

- 使用案例1

- 好处

- 投资报酬率

- 使用案例2

- 好处

- 投资报酬率

- 使用案例1

- 案例研究

- 案例研究 1

- 消费者姓名

- 挑战

- 解决方案

- 影响

- 案例研究 2

- 消费者姓名

- 挑战

- 解决方案

- 影响

- 案例研究 1

- 衝击力

- 成长动力

- 对即时资料分析和监控的需求日益增加

- 透过资料洞察提高永续性并减少对环境的影响

- 透过基于云端的解决方案提高营运效率

- 石油和天然气产业越来越关注数位转型倡议

- 产业陷阱与挑战

- 与遗留系统的整合挑战

- 对资料隐私和网路安全威胁的担忧

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:按服务,2021 - 2034 年

- 主要趋势

- 基础设施即服务 (IaaS)

- 平台即服务 (PaaS)

- 软体即服务 (SaaS)

第六章:市场估计与预测:依部署模式,2021 - 2034 年

- 主要趋势

- 公共云端

- 私有云端

- 混合云端

第 7 章:市场估计与预测:按运营,2021 - 2034 年

- 主要趋势

- 上游

- 中游

- 下游

第 8 章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 资料储存和管理

- 资产管理

- 协作和沟通工具

- 远端监控

- 模拟与建模

- 其他的

第 9 章:市场估计与预测:按最终用途,2021 - 2034 年

- 主要趋势

- 国家石油公司 (NOC)

- 独立石油公司 (IOC)

第 10 章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东及非洲

- 阿联酋

- 南非

- 沙乌地阿拉伯

第 11 章:公司简介

- ABB

- Accenture

- Amazon Web Services (AWS)

- AVEVA

- Baker Hughes

- Cisco

- Dassault Systèmes

- General Electric

- Halliburton

- Honeywell

- IBM

- Intel

- Microsoft

- Oracle

- Rockwell Automation

- SAP

- Schlumberger

- Siemens Energy

- Tata Consultancy Services (TCS)

- Yokogawa

The Global Cloud Computing In Oil And Gas Market was valued at USD 2.7 billion in 2024 and is expected to experience robust growth at a CAGR of 7.3% from 2025 to 2034. This growth is fueled by the increasing need for operational agility, optimized workflows, and enhanced data access. As oil and gas companies strive to modernize their operations, integrating cloud technologies offers increased flexibility, enabling faster responses to market fluctuations and more efficient resource management.

In 2024, the market was divided into several key service offerings: Infrastructure as a Service (IaaS), Platform as a Service (PaaS), and Software as a Service (SaaS). Among these, the PaaS segment commanded a substantial market share, valued at USD 900 million. This segment is expanding rapidly due to its ability to simplify application development and management, eliminating the complexities of maintaining underlying infrastructure. By adopting PaaS solutions, oil and gas companies can streamline development, reduce time to market, and easily scale their resources according to demand.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.7 Billion |

| Forecast Value | $5.4 Billion |

| CAGR | 7.3% |

Cloud computing in the oil and gas sector is also segmented by deployment mode, including public, private, and hybrid cloud solutions. The private cloud segment is expected to grow steadily at a CAGR of 5.5% from 2025 to 2034. This growth is driven by the rising adoption of private cloud solutions, which offer enhanced security features crucial for companies handling sensitive data. With private cloud deployments, oil and gas firms can enjoy greater control over data privacy while benefiting from the scalability and flexibility of cloud technologies. This is particularly important in an industry where compliance with stringent regulatory standards is non-negotiable.

In the U.S., the cloud computing market for oil and gas captured a 30% share in 2024. The widespread adoption of cloud technologies across the region is significantly boosting operational efficiency and reducing costs. Major oil and gas companies in the U.S. are investing heavily in cloud infrastructure as part of their digital transformation strategies. Furthermore, the region's strong regulatory framework and increasing demand for advanced data analytics solutions are accelerating the integration of cloud computing across a wide range of oil and gas operations, from exploration to distribution.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Software providers

- 3.2.2 Service providers

- 3.2.3 Oil & gas operators

- 3.2.4 Distributors

- 3.2.5 End users

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Regulatory landscape

- 3.7 Used cases

- 3.7.1 Used case 1

- 3.7.1.1 Benefits

- 3.7.1.2 ROI

- 3.7.2 Used case 2

- 3.7.2.1 Benefits

- 3.7.2.2 ROI

- 3.7.1 Used case 1

- 3.8 Case study

- 3.8.1 Case study 1

- 3.8.1.1 Consumer name

- 3.8.1.2 Challenge

- 3.8.1.3 Solution

- 3.8.1.4 Impact

- 3.8.2 Case study 2

- 3.8.2.1 Consumer name

- 3.8.2.2 Challenge

- 3.8.2.3 Solution

- 3.8.2.4 Impact

- 3.8.1 Case study 1

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing demand for real-time data analytics and monitoring

- 3.9.1.2 Shift towards improving sustainability and reducing environmental impact through data insights

- 3.9.1.3 Enhanced operational efficiency through cloud-based solutions

- 3.9.1.4 Growing focus on digital transformation initiatives in the oil and gas sector

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Integration challenges with legacy systems

- 3.9.2.2 Concerns regarding data privacy and cybersecurity threats

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Service, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Infrastructure as a Service (IaaS)

- 5.3 Platform as a Service (PaaS)

- 5.4 Software as a Service (SaaS)

Chapter 6 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Public cloud

- 6.3 Private cloud

- 6.4 Hybrid cloud

Chapter 7 Market Estimates & Forecast, By Operation, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Upstream

- 7.3 Midstream

- 7.4 Downstream

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Data storage and management

- 8.3 Asset management

- 8.4 Collaboration and communication tools

- 8.5 Remote monitoring and control

- 8.6 Simulation and modeling

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 National Oil Companies (NOCs)

- 9.3 Independent Oil Companies (IOCs)

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 ABB

- 11.2 Accenture

- 11.3 Amazon Web Services (AWS)

- 11.4 AVEVA

- 11.5 Baker Hughes

- 11.6 Cisco

- 11.7 Dassault Systèmes

- 11.8 General Electric

- 11.9 Halliburton

- 11.10 Honeywell

- 11.11 IBM

- 11.12 Intel

- 11.13 Microsoft

- 11.14 Oracle

- 11.15 Rockwell Automation

- 11.16 SAP

- 11.17 Schlumberger

- 11.18 Siemens Energy

- 11.19 Tata Consultancy Services (TCS)

- 11.20 Yokogawa

油气资料管理软体市场分析及预测(至2035年):依类型、产品类型、服务、技术、元件、应用、部署模式、最终使用者、功能及解决方案划分石油和天然气数据业务市场分析及预测(至2035年):按类型、产品、服务、技术、组件、应用、部署模式、最终用户、解决方案和阶段划分

油气资料管理软体市场分析及预测(至2035年):依类型、产品类型、服务、技术、元件、应用、部署模式、最终使用者、功能及解决方案划分石油和天然气数据业务市场分析及预测(至2035年):按类型、产品、服务、技术、组件、应用、部署模式、最终用户、解决方案和阶段划分 2026年全球油气资料管理市场报告

2026年全球油气资料管理市场报告 石油和天然气资料管理市场规模、份额和成长分析(按组件、资料类型、技术、部署类型、组织规模、应用和地区划分)—2026-2033年产业预测

石油和天然气资料管理市场规模、份额和成长分析(按组件、资料类型、技术、部署类型、组织规模、应用和地区划分)—2026-2033年产业预测 石油和天然气数据货币化市场-全球产业规模、份额、趋势、机会和预测,按方法、按部署模式、按应用、按地区和竞争进行细分,2020-2030 年预测石油和天然气移动市场-全球产业规模、份额、趋势、机会和预测(按组件、按部署、按应用、按地区、按竞争)2020-2030F

石油和天然气数据货币化市场-全球产业规模、份额、趋势、机会和预测,按方法、按部署模式、按应用、按地区和竞争进行细分,2020-2030 年预测石油和天然气移动市场-全球产业规模、份额、趋势、机会和预测(按组件、按部署、按应用、按地区、按竞争)2020-2030F 石油和天然气资料管理市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

石油和天然气资料管理市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 全球石油、天然气和交通市场

全球石油、天然气和交通市场