|

市场调查报告书

商品编码

1665328

播种机及撒播机市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Seed Drill and Broadcast Seeder Machinery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

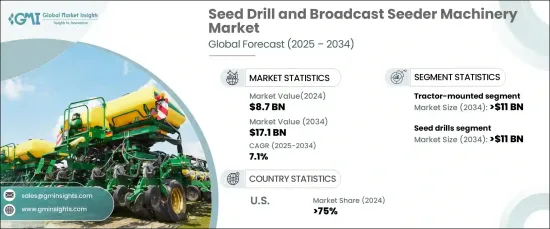

2024 年全球播种机和撒播机机械市场规模将达到 87 亿美元,预计 2025 年至 2034 年期间将以 7.1% 的强劲复合年增长率增长。条播机和撒播机是满足这一需求的重要工具,它们透过提高种植效率、降低成本、优化作物产量来满足不断增长的粮食需求,从而显着提高粮食安全。

2024 年,播种机占据市场主导地位,占有 65% 以上的份额。预计到 2034 年,该领域的规模将达到 110 亿美元。变数播种、GPS 导航和即时资料系统等功能正在推动种子放置的改进,根据土壤条件优化播种率,并最终提高作物产量。人工智慧感测器进一步增强了深度控制、间距和养分分布,提供更智慧、更精确的种植解决方案。此外,智慧连接可以实现即时监控、田间测绘和数据驱动的决策,从而创造更有效率、更永续的农业方法。随着永续发展的推动力不断加大,对先进、资源高效的播种机的需求持续上升。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 87亿美元 |

| 预测值 | 171亿美元 |

| 复合年增长率 | 7.1% |

市场还根据推进类型进行细分,选项包括拖拉机安装、手动/手动操作和自走式系统。其中,拖拉机搭载市场预计到 2034 年将创造 110 亿美元。这些拖拉机安装的系统非常适合免耕和少耕等保护性农业实践,有助于保持土壤健康并减少侵蚀。该领域的创新重点是轻质材料、节能设计以及与电动和混合动力拖拉机的兼容性,符合监管标准并促进永续农业技术。

在美国,播种机和撒播机械市场在 2024 年占据了 75% 的主导份额。新型电动和氢动力模型融合了人工智慧(AI)、电脑视觉和精密 GPS,正在推动种植过程的重大改进。这些先进的机器能够在播种过程中进行即时调整,优化种植效率。机器学习技术正在进一步增强对不同现场条件的适应性,解决劳动力短缺问题,降低营运成本并提高生产力。对尖端农业设备的持续投资正在推动市场成长并激发该领域的创新。

报告内容

第 1 章:方法论与范围

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 供应商概况

- 设备製造商

- 经销商

- 技术提供者

- 系统整合商

- 最终用户

- 利润率分析

- 技术差异化

- GPS 和 GNSS 导航系统

- 变数播种 (VRS)

- 自主播种机

- 即时资料监控

- 其他的

- 成本明细分析

- 製造成本

- 原料

- 劳动成本

- 研发费用

- 行销和分销成本

- 售后服务费用

- 其他的

- 製造成本

- 重要新闻和倡议

- 专利分析

- 监管格局

- 衝击力

- 成长动力

- 全球粮食安全需求

- 精准农业技术的应用日益广泛

- 农业设备经济效率的需求日益增长

- 对永续农业的偏好正在改变

- 产业陷阱与挑战

- 土壤相容性限制

- 初期投资成本高

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第 5 章:市场估计与预测:按设备,2021 - 2034 年

- 主要趋势

- 播种机

- 单碟

- 双碟

- 空气种子

- 肥料种子

- 广播播种机

- 挂载广播

- 拖曳式

- 自走式

第 6 章:市场估计与预测:按推进方式,2021 - 2034 年

- 主要趋势

- 手动/手操

- 拖拉机悬挂

- 自走式

第 7 章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 谷物

- 豆类

- 油籽

- 草类

- 覆盖作物

第 8 章:市场估计与预测:按最终用途,2021 - 2034 年

- 主要趋势

- 个体农户

- 农业承包商

- 政府/研究机构

第 9 章:市场估计与预测:按销售管道,2021 - 2034 年

- 主要趋势

- 在线的

- 离线

第 10 章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 西班牙

- 义大利

- 俄罗斯

- 北欧

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳新银行

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东及非洲

- 阿联酋

- 南非

- 沙乌地阿拉伯

第 11 章:公司简介

- AGCO

- Amazonen Werke

- Bourgault Industries

- BUPL (FieldKing)

- Claas

- CNH Industrial

- Great Plains

- Horsch

- John Deere

- Kubota

- Kuhn

- Kverneland Group

- Landforce

- Lemken

- Mahindra & Mahindra

- Morris Equipment

- National Agro Industries

- Pottinger

- Tume

- Väderstad

- Yanmar

- Zoomlion

The Global Seed Drill And Broadcast Seeder Machinery Market reached USD 8.7 billion in 2024 and is projected to grow at a robust CAGR of 7.1% from 2025 to 2034. The increasing global population, expected to hit 9.7 billion by 2050, is fueling the demand for greater agricultural productivity. Seed drills and broadcast seeders are essential tools in meeting this demand, significantly enhancing food security by improving planting efficiency, lowering costs, and optimizing crop yields to satisfy growing food requirements.

In 2024, seed drills dominated the market, capturing over 65% of the share. This segment is anticipated to reach USD 11 billion by 2034. The rapid advancements in precision agriculture technologies are revolutionizing the seed drill market. Features like variable rate seeding, GPS guidance, and real-time data systems are driving improvements in seed placement, optimizing seeding rates according to soil conditions, and ultimately boosting crop yields. AI-powered sensors further enhance depth control, spacing, and nutrient distribution, offering smarter, more precise planting solutions. Additionally, smart connectivity enables real-time monitoring, field mapping, and data-driven decision-making, creating a more efficient and sustainable farming approach. As the push for sustainability continues to intensify, the demand for advanced, resource-efficient seed drills remains on the rise.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.7 billion |

| Forecast Value | $17.1 billion |

| CAGR | 7.1% |

The market is also segmented by propulsion type, with options including tractor-mounted, manual/hand-operated, and self-propelled systems. Among these, the tractor-mounted segment is expected to generate USD 11 billion by 2034. Manufacturers are prioritizing sustainability by developing seed drills that feature reduced carbon footprints, improved fuel efficiency, and minimized soil impact. These tractor-mounted systems are well-suited for conservation agriculture practices such as no-till and reduced-till farming, helping to preserve soil health and reduce erosion. Innovations in this space focus on lightweight materials, energy-efficient designs, and compatibility with electric and hybrid tractors, aligning with regulatory standards and promoting sustainable farming techniques.

In the U.S., the seed drill and broadcast seeder machinery market held a dominant 75% share in 2024. The country is witnessing a surge in the adoption of autonomous and robotic seed drill technologies. New electric and hydrogen-powered models, integrated with artificial intelligence (AI), computer vision, and precision GPS, are driving significant improvements in the planting process. These advanced machines enable real-time adjustments during seeding, optimizing planting efficiency. Machine learning technologies are further enhancing adaptability to diverse field conditions, addressing labor shortages, reducing operational costs, and increasing productivity. Continued investments in cutting-edge agricultural equipment are fueling market growth and spurring innovation in the sector.

Report Content

Chapter 1 Methodology and Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Equipment manufacturers

- 3.2.2 Distributors

- 3.2.3 Technology providers

- 3.2.4 System integrators

- 3.2.5 End users

- 3.3 Profit margin analysis

- 3.4 Technology differentiators

- 3.4.1 GPS and GNSS guidance systems

- 3.4.2 Variable rate seeding (VRS)

- 3.4.3 Autonomous seeding machines

- 3.4.4 Real-time data monitoring

- 3.4.5 Others

- 3.5 Cost breakdown analysis

- 3.5.1 Manufacturing costs

- 3.5.1.1 Raw materials

- 3.5.1.2 Labor costs

- 3.5.2 R & D costs

- 3.5.3 Marketing and distribution costs

- 3.5.4 After-sales service costs

- 3.5.5 Others

- 3.5.1 Manufacturing costs

- 3.6 Key news and initiatives

- 3.7 Patent analysis

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Global demand for food security

- 3.9.1.2 Increasing adoption of precision agriculture technologies

- 3.9.1.3 Growing demand for economic efficiency for agriculture equipment

- 3.9.1.4 Changing preferences towards sustainable agriculture

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Soil compatibility constraints

- 3.9.2.2 High initial investment costs

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Equipment, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Seed drills

- 5.2.1 Single-disc

- 5.2.2 Double-disc

- 5.2.3 Air seed

- 5.2.4 Fertilizer seed

- 5.3 Broadcast seeders

- 5.3.1 Mounted-broadcast

- 5.3.2 Tow-behind

- 5.3.3 Self-propelled

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Manual/hand operated

- 6.3 Tractor-mounted

- 6.4 Self-propelled

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Cereals

- 7.3 Legumes

- 7.4 Oil seeds

- 7.5 Grasses

- 7.6 Cover crops

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Individual farmers

- 8.3 Agricultural contractors

- 8.4 Government/research institutes

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Online

- 9.3 Offline

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 AGCO

- 11.2 Amazonen Werke

- 11.3 Bourgault Industries

- 11.4 BUPL (FieldKing)

- 11.5 Claas

- 11.6 CNH Industrial

- 11.7 Great Plains

- 11.8 Horsch

- 11.9 John Deere

- 11.10 Kubota

- 11.11 Kuhn

- 11.12 Kverneland Group

- 11.13 Landforce

- 11.14 Lemken

- 11.15 Mahindra & Mahindra

- 11.16 Morris Equipment

- 11.17 National Agro Industries

- 11.18 Pottinger

- 11.19 Tume

- 11.20 Väderstad

- 11.21 Yanmar

- 11.22 Zoomlion

种植工具市场:依产品类型、动力来源、材料、应用、通路和最终用户划分-全球预测,2026-2032年自走式蔬菜移植市场:按类型、引擎功率、种植行数、价格范围、通路、最终用户和应用划分-2026-2032年全球预测蔬菜移植市场:按类型、操作方式、动力来源、应用和最终用户划分,全球预测,2026-2032年农业植物保护无人机市场:按无人机类型、组件、作物类型、应用、最终用户划分,全球预测(2026-2032)

种植工具市场:依产品类型、动力来源、材料、应用、通路和最终用户划分-全球预测,2026-2032年自走式蔬菜移植市场:按类型、引擎功率、种植行数、价格范围、通路、最终用户和应用划分-2026-2032年全球预测蔬菜移植市场:按类型、操作方式、动力来源、应用和最终用户划分,全球预测,2026-2032年农业植物保护无人机市场:按无人机类型、组件、作物类型、应用、最终用户划分,全球预测(2026-2032) 2026年全球播种机市场报告2026年全球施肥机械市场报告2026年全球肥料施用与植物保护设备市场报告

2026年全球播种机市场报告2026年全球施肥机械市场报告2026年全球肥料施用与植物保护设备市场报告 种植设备市场规模、份额和成长分析(按设备类型、动力来源、行类型、最终用途、分销通路和地区划分)-2026-2033年产业预测蔬菜种植机器人市场(依动力源、商业农场、自主机器人、露天农场、播种和机械臂)——2026-2032年全球预测

种植设备市场规模、份额和成长分析(按设备类型、动力来源、行类型、最终用途、分销通路和地区划分)-2026-2033年产业预测蔬菜种植机器人市场(依动力源、商业农场、自主机器人、露天农场、播种和机械臂)——2026-2032年全球预测 水稻插秧机市场:依产品类型(骑乘式插秧机、步行式插秧机)、驱动方式(自走式、手排式)、容量(4行以下、4-8行)、导航系统与应用领域划分-全球预测至2035年

水稻插秧机市场:依产品类型(骑乘式插秧机、步行式插秧机)、驱动方式(自走式、手排式)、容量(4行以下、4-8行)、导航系统与应用领域划分-全球预测至2035年