|

市场调查报告书

商品编码

1666540

汽车数据线市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测Automotive Data Cables Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

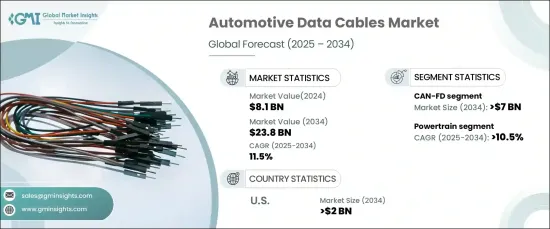

2024 年全球汽车数据线市场价值为 81 亿美元,预计 2025 年至 2034 年期间将以 11.5% 的复合年增长率快速增长。这些技术进步导致对车辆高效资料传输和连接的需求不断增加。汽车产业对感测器、摄影机和资讯娱乐系统等电子元件的依赖日益增加,极大地促进了对高品质汽车资料线的需求。此外,在政府支持措施的支持下,车对车(V2V)和车对基础设施(V2I)技术的扩展正在加速电子系统的开发和应用,进一步推动市场向前发展。

随着基础设施不断改善,特别是对智慧城市和互联交通的关注,对汽车资料线的需求日益加剧。主要製造商在全球扩大生产设施进一步支持了这一成长。透过优化生产流程和缩短交货时间,公司能够更好地满足符合当地偏好和监管标准的车辆日益增长的区域需求。这些努力不仅加强了产业的供应链,也促进了电子元件的创新,从而推动了汽车产业对资料线的需求。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 81亿美元 |

| 预测值 | 238亿美元 |

| 复合年增长率 | 11.5% |

CAN-FD(控制器资料网路灵活资料速率)部门预计到 2034 年将产生 70 亿美元的收入。汽车製造商正在大力投资增强 CAN-FD 技术,以支援汽车和工业领域日益复杂的应用。 CAN-FD 解决方案的持续开发对于满足现代车辆的需求至关重要,因为现代车辆需要更快、更可靠的资料传输以实现最佳性能。

此外,动力总成领域也将经历显着成长,预计到 2034 年复合年增长率将达到 10.5%。随着汽车製造商采用先进的电子设备和车载电脑网路来满足现代动力系统的高资料要求,该领域对汽车资料线的需求持续上升。动力系统日益复杂,再加上尖端电气技术的集成,为强大的资料线提供了机会,可实现车辆功能的无缝资料交换,支援车辆的整体性能和效率。

预计到 2034 年,美国汽车资料线市场规模将达到资料亿美元。美国的原始设备製造商 (OEM) 专注于改进车辆设计以纳入更多的电子系统,导致资料线的需求激增。先进电子设备与动力传动技术整合进一步推动了这一趋势,以电子控制取代了传统的机械系统,从而提高了车辆的效率和性能。

目录

第 1 章:方法论与范围

- 市场定义

- 基础估算与计算

- 预测计算

- 资料来源

- 基本的

- 次要

- 有薪资的

- 民众

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 监管格局

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- PESTEL 分析

第四章:竞争格局

- 介绍

- 战略仪表板

- 创新与永续发展格局

第 5 章:市场规模与预测:按电缆,2021 – 2034 年

- 主要趋势

- 控制器区域网路 (CAN)

- 控制器区域网路灵活资料速率 (CAN-FD)

- FlexRay

- 乙太网路

- 低电压差分讯号 (LVDS)/高速资料 (HSD)

- 同轴电缆

第六章:市场规模及预测:依车型,2021 – 2034 年

- 主要趋势

- 搭乘用车

- 商用车

第 7 章:市场规模与预测:按应用,2021 – 2034 年

- 主要趋势

- 动力传动系统

- 车身控制与舒适度

- 资讯娱乐与通信

- 安全性与 ADAS

第 8 章:市场规模与预测:按地区,2021 – 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 西班牙

- 义大利

- 俄罗斯

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- 澳新银行

- 中东和非洲

- 南非

- 海湾合作委员会

- 土耳其

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

第九章:公司简介

- ACOME

- Amphenol

- Aptiv

- Belden

- Champlain

- Coficab

- Condumex

- Coroplast

- Furukawa

- Gebauer

- HUBER+SUHNER

- ITC

- Lear

- Leoni

- Prysmian

- Salcavi

- Sumitomo

- Waytek

- Yazaki

The Global Automotive Data Cables Market, valued at USD 8.1 billion in 2024, is expected to grow rapidly at a CAGR of 11.5% between 2025 and 2034. This surge in demand is driven by the increasing integration of advanced electronic systems into modern vehicles, coupled with the implementation of stricter safety standards and regulations within the automotive sector. These technological advancements have led to the rising need for efficient data transfer and connectivity in vehicles. The automotive industry's growing reliance on electronic components, including sensors, cameras, and infotainment systems, has significantly contributed to the demand for high-quality automotive data cables. Moreover, the expansion of vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2I) technologies, backed by supportive government initiatives, is accelerating the development and adoption of electronic systems, further pushing the market forward.

As infrastructure continues to improve, especially with the focus on smart cities and connected transportation, the demand for automotive data cables is intensifying. This growth is further supported by key manufacturers expanding their production facilities globally. By optimizing production processes and reducing lead times, companies are better able to cater to the growing regional demand for vehicles that meet local preferences and regulatory standards. These efforts are not only strengthening the industry's supply chain but also fostering innovation in electronic components, boosting the demand for data cables in the automotive sector.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.1 Billion |

| Forecast Value | $23.8 Billion |

| CAGR | 11.5% |

The CAN-FD (Controller Area Network Flexible Data-rate) segment is expected to generate USD 7 billion in revenue by 2034. CAN-FD technology, known for its ability to facilitate rapid and efficient data transfer, has become essential for modern vehicles that require high-speed communication between systems. Automotive manufacturers are investing significantly in the enhancement of CAN-FD technology to support increasingly complex applications within both automotive and industrial sectors. This ongoing development of CAN-FD solutions is critical to meeting the demands of modern vehicles, which require faster, more reliable data transmission for optimal performance.

Additionally, the powertrain segment is set to experience significant growth, with a projected CAGR of 10.5% through 2034. The shift towards electric vehicles (EVs) is playing a major role in this growth. As automotive manufacturers adopt advanced electronics and onboard computer networks to meet the high data requirements of modern powertrains, the need for automotive data cables in this sector continues to rise. The increasing complexity of powertrain systems, coupled with the integration of cutting-edge electric technologies, presents an opportunity for robust data cables to enable seamless data exchange for vehicle functions, supporting overall vehicle performance and efficiency.

The U.S. automotive data cables market is projected to reach USD 2 billion by 2034. The rapid transition toward electric vehicles, driven by growing consumer interest and environmental considerations, has significantly increased the demand for sophisticated electronic components, including automotive data cables. Original equipment manufacturers (OEMs) in the U.S. are focused on advancing vehicle designs to incorporate more electronic systems, creating a surge in demand for data cables. This trend is further fueled by the integration of advanced electronics in powertrain technologies, replacing traditional mechanical systems with electronic controls, thus enhancing vehicle efficiency and performance.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Cable, 2021 – 2034 (USD Million)

- 5.1 Key trends

- 5.2 Controller Area Network (CAN)

- 5.3 Controller Area Network Flexible Data-Rate (CAN-FD)

- 5.4 FlexRay

- 5.5 Ethernet

- 5.6 Low Voltage Differential Signaling (LVDS)/High Speed Data (HSD)

- 5.7 Coaxial Cables

Chapter 6 Market Size and Forecast, By Vehicle, 2021 – 2034 (USD Million)

- 6.1 Key trends

- 6.2 Passenger Vehicles

- 6.3 Commercial Vehicles

Chapter 7 Market Size and Forecast, By Application, 2021 – 2034 (USD Million)

- 7.1 Key trends

- 7.2 Powertrain

- 7.3 Body Control & Comfort

- 7.4 Infotainment & Communication

- 7.5 Safety & ADAS

Chapter 8 Market Size and Forecast, By Region, 2021 – 2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 South Korea

- 8.4.4 India

- 8.4.5 ANZ

- 8.5 Middle East & Africa

- 8.5.1 South Africa

- 8.5.2 GCC

- 8.5.3 Turkey

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Mexico

- 8.6.3 Argentina

Chapter 9 Company Profiles

- 9.1 ACOME

- 9.2 Amphenol

- 9.3 Aptiv

- 9.4 Belden

- 9.5 Champlain

- 9.6 Coficab

- 9.7 Condumex

- 9.8 Coroplast

- 9.9 Furukawa

- 9.10 Gebauer

- 9.11 HUBER+SUHNER

- 9.12 ITC

- 9.13 Lear

- 9.14 Leoni

- 9.15 Prysmian

- 9.16 Salcavi

- 9.17 Sumitomo

- 9.18 Waytek

- 9.19 Yazaki