|

市场调查报告书

商品编码

1666545

超薄玻璃市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Ultra-Thin Glass Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

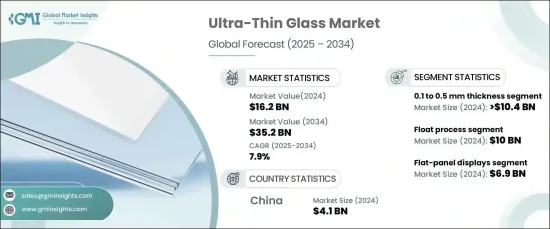

2024 年全球超薄玻璃市场规模将达到 162 亿美元,预计 2025-2034 年期间复合年增长率将达到 7.9%。这一成长是由消费性电子、汽车和能源领域不断增长的需求推动的,这些领域中轻质、灵活和耐用的材料至关重要。

0.1 至 0.5 毫米厚度部分占据市场主导地位,2024 年的市场规模为 104 亿美元,预计在 2025-2034 年期间将保持 7.7% 的复合年增长率的稳定增长。此厚度范围内的超薄玻璃因其独特的强度、柔韧性和透明度组合而广泛采用。这些特性使其非常适合需要精确度的应用,例如柔性显示器、穿戴式装置和轻量面板。在汽车和能源领域,超薄玻璃越来越多地用于减轻重量、提高燃油效率和增强能源解决方案,例如太阳能电池板。此外,对永续和高性能材料的需求不断增长,推动了其应用,而环保生产方法的进步为市场创造了新的机会。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 162亿美元 |

| 预测值 | 352亿美元 |

| 复合年增长率 | 7.9% |

浮法製程是超薄玻璃的主要生产方法,2024 年的价值为 100 亿美元,预计在 2025 年至 2034 年期间的复合年增长率为 7.8%。 该工艺可确保生产高品质、均匀且厚度精确的玻璃板,非常适合一致性和性能至关重要的应用。浮法製程支援薄型、轻型玻璃的开发,这种玻璃越来越多地应用于需要先进材料的行业,例如消费性电子、汽车和可再生能源。该工艺能够满足对耐用、高清晰度玻璃的需求,从而推动其在市场上持续保持重要地位。

中国引领全球超薄玻璃市场,2024 年贡献 41 亿美元,预计 2025 年至 2034 年的复合年增长率为 8.8%。中国在生产技术方面的进步和对永续性的重视进一步加速了市场的成长。作为全球製造业中心,中国完全有能力满足柔性显示器、轻量化组件和节能应用领域对超薄玻璃日益增长的需求。

整体而言,在技术进步、轻质材料需求不断增长以及全球各行业对节能和永续解决方案的强力推动下,超薄玻璃市场将大幅扩张。

目录

第 1 章:方法论与范围

- 市场范围和定义

- 基础估算与计算

- 预测计算

- 资料来源

- 基本的

- 次要

- 付费来源

- 公共资源

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 供应商概况

- 利润率分析

- 重要新闻及倡议

- 监管格局

- 衝击力

- 成长动力

- 消费性电子产品需求不断成长

- 太阳能板渗透率不断提高

- 由于其灵活性和强度,在医疗设备和感测器中的应用日益广泛

- 产业陷阱与挑战

- 製造流程复杂,原物料价格波动

- 来自塑胶和陶瓷等替代材料的竞争

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第 5 章:市场估计与预测:按厚度,2021-2034 年

- 主要趋势

- 小于0.1毫米

- 0.1 至 0.5 毫米

- 0.5 至 1.2 毫米

第 6 章:市场估计与预测:按生产工艺,2021-2034 年

- 主要趋势

- 下拉工艺

- 溢流熔合工艺

- 浮法工艺

第 7 章:市场估计与预测:按应用,2021 年至 2034 年

- 主要趋势

- 半导体基板

- 平面显示器

- 触控设备

- 其他的

第 8 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中东及非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- AGC Inc.

- Central Glass Co. Ltd.

- Changzhou Almaden Co. Ltd.

- Corning Inc.

- CSG Holdings Co. Ltd.

- Emerge Glass

- Luoyang Glass Co. Ltd.

- Nippon Sheet Glass Co., Ltd.

- Noval Glass Co. Ltd.

- Schott AG

- Taiwan Glass Ind

- Xinyi Glass Holdings Ltd.

The Global Ultra-Thin Glass Market reached USD 16.2 billion in 2024 and is projected to grow at a robust CAGR of 7.9% during 2025-2034. This growth is driven by rising demand across consumer electronics, automotive, and energy sectors, where lightweight, flexible, and durable materials are essential.

The 0.1 to 0.5 mm thickness segment dominated the market, accounting for USD 10.4 billion in 2024, and is expected to maintain steady growth at a 7.7% CAGR during 2025-2034. Ultra-thin glass in this thickness range is witnessing high adoption due to its unique combination of strength, flexibility, and transparency. These properties make it highly suitable for applications requiring precision, such as flexible displays, wearable devices, and lightweight panels. In the automotive and energy sectors, ultra-thin glass is increasingly used to reduce weight, improve fuel efficiency, and enhance energy solutions, such as solar panels. Additionally, the growing demand for sustainable and high-performance materials is boosting its adoption, while advancements in eco-friendly production methods are creating new opportunities in the market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $16.2 Billion |

| Forecast Value | $35.2 Billion |

| CAGR | 7.9% |

The float process, a key production method for ultra-thin glass, was valued at USD 10 billion in 2024 and is anticipated to grow at a CAGR of 7.8% throughout 2025- 2034. This process ensures the production of high-quality, uniform glass sheets with precise thickness, making it ideal for applications where consistency and performance are critical. The float process supports the development of thin, lightweight glass, which is increasingly used in industries requiring advanced materials, such as consumer electronics, automotive, and renewable energy. The process's ability to meet the demand for durable, high-clarity glass drives its continued significance in the market.

China leads the global ultra-thin glass market, contributing USD 4.1 billion in 2024, with a projected CAGR of 8.8% from 2025 to 2034. The country's market dominance is fueled by its strong consumer electronics sector, growing automotive industry, and increasing investment in renewable energy solutions. China's advancements in production technologies and focus on sustainability are further accelerating the market growth. As a global manufacturing hub, China is well-positioned to meet the rising demand for ultra-thin glass in flexible displays, lightweight components, and energy-efficient applications.

Overall, the ultra-thin glass market is set for significant expansion, driven by technological advancements, increasing demand for lightweight materials, and a strong push for energy-efficient and sustainable solutions across industries worldwide.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing demand for consumer electronics

- 3.6.1.2 Growing penetration in solar panels

- 3.6.1.3 Rising use in medical devices and sensors due to its flexibility and strength

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Complex manufacturing process and fluctuating raw material prices

- 3.6.2.2 Competition from alternative materials such as plastics and ceramics

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Thickness, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Less than 0.1 mm

- 5.3 0.1 to 0.5 mm

- 5.4 0.5 to 1.2 mm

Chapter 6 Market Estimates & Forecast, By Production Process, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Downdraw process

- 6.3 Overflow- fusion process

- 6.4 Float process

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Semiconductors substrate

- 7.3 Flat-panel displays

- 7.4 Touch-control devices

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AGC Inc.

- 9.2 Central Glass Co. Ltd.

- 9.3 Changzhou Almaden Co. Ltd.

- 9.4 Corning Inc.

- 9.5 CSG Holdings Co. Ltd.

- 9.6 Emerge Glass

- 9.7 Luoyang Glass Co. Ltd.

- 9.8 Nippon Sheet Glass Co., Ltd.

- 9.9 Noval Glass Co. Ltd.

- 9.10 Schott AG

- 9.11 Taiwan Glass Ind

- 9.12 Xinyi Glass Holdings Ltd.

超薄玻璃市场:按材料、厚度、製造流程、应用和最终用户划分-2026-2032年全球市场预测

超薄玻璃市场:按材料、厚度、製造流程、应用和最终用户划分-2026-2032年全球市场预测 超薄玻璃:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

超薄玻璃:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 超薄玻璃市场规模、份额和成长分析(按厚度、製造流程、应用、终端用户产业和地区划分)-2026-2033年产业预测

超薄玻璃市场规模、份额和成长分析(按厚度、製造流程、应用、终端用户产业和地区划分)-2026-2033年产业预测 全球超薄透明玻璃市场

全球超薄透明玻璃市场 全球超薄玻璃市场规模(按厚度范围、应用、最终用户产业、区域范围和预测)

全球超薄玻璃市场规模(按厚度范围、应用、最终用户产业、区域范围和预测) 2032年超薄玻璃市场预测:全球厚度、製造流程、应用、最终用户和地区分析

2032年超薄玻璃市场预测:全球厚度、製造流程、应用、最终用户和地区分析 超薄玻璃市场规模、份额、趋势分析报告:按应用、地区、细分市场、预测,2025-2030 年

超薄玻璃市场规模、份额、趋势分析报告:按应用、地区、细分市场、预测,2025-2030 年 超薄玻璃市场,按製造流程、按应用、按最终用户、按国家和地区划分 - 2024-2032 年行业分析、市场规模、市场份额和预测

超薄玻璃市场,按製造流程、按应用、按最终用户、按国家和地区划分 - 2024-2032 年行业分析、市场规模、市场份额和预测