|

市场调查报告书

商品编码

1683411

超薄玻璃:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Ultra-thin Glass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

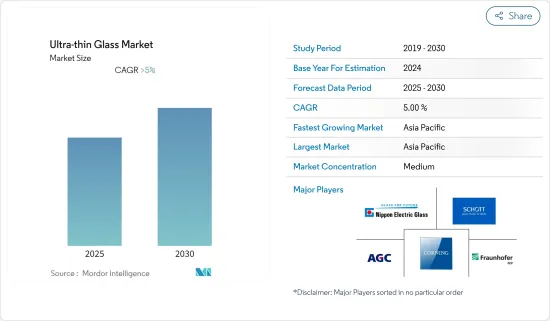

预计预测期内超薄玻璃市场复合年增长率将超过 5%。

主要亮点

- 预计预测期内超薄玻璃在电子产业的广泛应用将占据市场主导地位。它的柔韧性、弹性和出色的抗刮性等特性使其适合用于智慧型装置。

- 正在进行的使用超薄玻璃作为太阳能计划专用镜子的研究预计将在预测期内为市场成长提供各种机会。

- 由于家电行业规模庞大,而家电行业是超薄玻璃的主要应用领域,因此亚太地区预计将成为超薄玻璃的最大市场。

超薄玻璃市场趋势

消费性电子产品需求不断成长

- 超薄玻璃在消费性电子领域的广泛应用,正刺激市场区隔的需求。由于重量轻、平整度高、柔韧性好、表面品质好等特性,这些玻璃适用于个人电脑 (PC)、电子阅读器、智慧型手机和其他电子设备。

- 预计 2020 年全球消费性电子领域收益将达到 4,260 亿美元,到 2024年终将达到约 5,650 亿美元。

- 2019年桌上型电脑、笔记型电脑及平板电脑的总销量分别约为8,840万台、1.66亿台和1.368亿台。预计2020年全球销售给终端用户的智慧型手机数量将达到15.6亿支。随着对电子设备的需求不断增加,预计未来几年这些电子产品的生产和销售将进一步增加。

- 预计所有上述因素都将在预测期内推动超薄玻璃市场的发展。

亚太地区占市场主导地位

- 由于中国、印度、日本和韩国等国家的超薄玻璃消费量不断增加,亚太地区是全球最大且成长最快的超薄玻璃市场。

- 预计到 2020 年该地区的消费电子产品总合收入将达到 2,270 亿美元,到 2024年终预计将成长到 2,627 亿美元。

- 2019年全球售出的智慧型手机为15亿部,其中仅在中国就售出了4.2亿部以上。

- 由于该地区的一些新兴国家对智慧型设备的需求很高,因此该地区未来市场成长潜力巨大。

- 2019年,中国、印度等主要国家的汽车产销量均大幅下滑,预计对市场成长将产生轻微影响。

- 因此,基于上述因素,预计预测期内亚太地区对超薄玻璃的需求将会成长。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 家电需求不断成长

- 其他驱动因素

- 限制因素

- 原料高成本

- 其他阻碍因素

- 产业价值链分析

- 波特五力分析

- 新进入者的威胁

- 买家的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争程度

第五章 市场区隔

- 按应用

- 半导体基板

- 触控萤幕

- 指纹感应器

- 汽车嵌装玻璃

- 其他用途

- 按最终用户产业

- 消费性电子产品

- 车

- 生物技术

- 其他最终用户产业

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争格局

- 併购、合资、合作、协议

- 市场占有率分析

- 主要企业策略

- 公司简介

- AGC Glass Europe

- Central Glass Co. Ltd

- Changzhou Almaden Co. Ltd

- Corning Incorporated

- CSG Holding Co. Ltd

- Emerge Glass

- Fraunhofer FEP

- Nippon Electric Glass Co. Ltd

- Nitto Boseki Co., Ltd

- Novalglass

- Schott AG

- Taiwan Glass Industry Corporation

第七章 市场机会与未来趋势

- 为太阳能计划开发高性能玻璃

- 其他机会

简介目录

Product Code: 68544

The Ultra-thin Glass Market is expected to register a CAGR of greater than 5% during the forecast period.

Key Highlights

- Extensive applications of ultra-thin glasses in the electronics industry are anticipated to govern the market during the forecast timeline. Its properties like flexibility, elasticity, and superior scratch resistance ability make them suitable for use in smart devices.

- On-going research is being done to use ultra-thin glasses as special mirrors for solar energy projects are expected to offer various opportunities for the growth of the market over the forecast period.

- The Asia-Pacific region is expected to be the largest market for the ultra-thin glass market because of the gigantic consumer electronics industry of the region where these glasses find their major application.

Ultra-Thin Glass Market Trends

Growing Demand from Consumer Electronics

- The extensive use of ultra-thin glass in the consumer electronics segment has surged the demand of the market studied. Its properties such as lightweight, perfect flatness, flexibility, good surface quality, etc. make these glasses suitable for Personal Computers (PCs), e-readers, smartphones, and other electronic gadgets.

- Global revenue from the consumer electronics segment is projected to be USD 426 billion in 2020 and is estimated to reach around USD 565 billion by the end of 2024.

- The total number of sales of desktop PCs, laptops, and tablets in 2019 was about 88.4 million, 166 million and 136.8 million units respectively. The number of smartphones sold to end users globally in 2020 is anticipated to be 1.560 billion units. With the increasing demand for electronics, the production and sales of these electronic goods are expected to further increase over the coming years.

- All the aforementioned factors are expected to drive the ultra-thin glass market during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region accounts for the largest and fastest-growing market in the ultra-thin glass market globally owing to the increasing consumption from countries such as China, India, Japan, and South Korea.

- The region is projected to amass a total of USD 227 billion from its consumer electronics segment by 2020 and is forecasted to grow up to USD 262.7 billion by the end of 2024.

- China alone accounts for the sale of more than 420 million units of smartphones sold out of 1.5 billion units sold globally in 2019.

- The region holds great potential for the future growth of the market studied as some emerging countries from the region have a high demand for smart devices.

- The automotive production and sales in major countries such as China and India have witnessed huge downfall in 2019 and this is expected to slightly affect the growth of the market.

- Hence, from the above mentioned factors, the demand for ultra-thin glass in Asia-Pacific region is expected to grow over the forecast period.

Ultra-Thin Glass Industry Overview

The Ultra-Thin Glass Market is partially fragmented. Some of the players in the market include Nippon Electric Glass Co. Ltd, Schott AG, AGC Glass Europe, Corning Incorporated, and Fraunhofer FEP.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from Consumer Electronics

- 4.1.2 Other Drivers

- 4.2 Restraints

- 4.2.1 High Cost of Raw Materials

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porters Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Semiconductor Substrate

- 5.1.2 Touch Panel Displays

- 5.1.3 Fingerprint Sensors

- 5.1.4 Automotive Glazing

- 5.1.5 Other Applications

- 5.2 End-user Industry

- 5.2.1 Consumer Electronics

- 5.2.2 Automotive

- 5.2.3 Biotechnology

- 5.2.4 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AGC Glass Europe

- 6.4.2 Central Glass Co. Ltd

- 6.4.3 Changzhou Almaden Co. Ltd

- 6.4.4 Corning Incorporated

- 6.4.5 CSG Holding Co. Ltd

- 6.4.6 Emerge Glass

- 6.4.7 Fraunhofer FEP

- 6.4.8 Nippon Electric Glass Co. Ltd

- 6.4.9 Nitto Boseki Co., Ltd

- 6.4.10 Novalglass

- 6.4.11 Schott AG

- 6.4.12 Taiwan Glass Industry Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Advanced Glass for Solar Energy Projects

- 7.2 Other Opportunities

02-2729-4219

+886-2-2729-4219

超薄玻璃市场规模、份额和成长分析(按厚度、製造流程、应用、终端用户产业和地区划分)-2026-2033年产业预测

超薄玻璃市场规模、份额和成长分析(按厚度、製造流程、应用、终端用户产业和地区划分)-2026-2033年产业预测 超薄玻璃市场(按材料类型、厚度、製程、应用和最终用户)—2025-2032 年全球预测

超薄玻璃市场(按材料类型、厚度、製程、应用和最终用户)—2025-2032 年全球预测 全球超薄透明玻璃市场

全球超薄透明玻璃市场 全球超薄玻璃市场规模(按厚度范围、应用、最终用户产业、区域范围和预测)

全球超薄玻璃市场规模(按厚度范围、应用、最终用户产业、区域范围和预测) 2032年超薄玻璃市场预测:全球厚度、製造流程、应用、最终用户和地区分析

2032年超薄玻璃市场预测:全球厚度、製造流程、应用、最终用户和地区分析 2025-2033年超薄玻璃市场报告(依厚度类型、製造流程、应用、最终用途产业和地区)

2025-2033年超薄玻璃市场报告(依厚度类型、製造流程、应用、最终用途产业和地区) 超薄玻璃市场规模、份额、趋势分析报告:按应用、地区、细分市场、预测,2025-2030 年

超薄玻璃市场规模、份额、趋势分析报告:按应用、地区、细分市场、预测,2025-2030 年 超薄玻璃市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

超薄玻璃市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 超薄玻璃市场,按製造流程、按应用、按最终用户、按国家和地区划分 - 2024-2032 年行业分析、市场规模、市场份额和预测

超薄玻璃市场,按製造流程、按应用、按最终用户、按国家和地区划分 - 2024-2032 年行业分析、市场规模、市场份额和预测