|

市场调查报告书

商品编码

1666634

血管移植市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测Vascular Graft Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

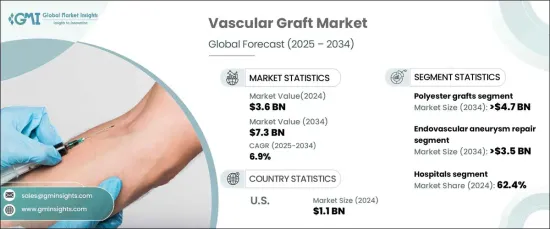

2024 年全球血管移植市场价值为 36 亿美元,将实现令人瞩目的成长,预计 2025 年至 2034 年的复合年增长率为 6.9%。此外,血管移植技术的进步和向微创手术的转变正在改变医疗格局、改善患者的治疗效果并使手术解决方案更容易获得且更有效。

随着世界各地的医疗保健系统努力应对人口老化和相关慢性病的增加,对血管移植的需求持续激增。生物工程和合成移植材料的创新正在解决生物相容性、耐用性和易用性等关键挑战。混合移植物结合了多种材料的优势,也因其提高手术成功率的能力而受到关注。随着对个人化医疗的更加重视,製造商投资于研发,以创造适合不同医疗需求的下一代移植物,确保市场保持活力和竞争力。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 36亿美元 |

| 预测值 | 73亿美元 |

| 复合年增长率 | 6.9% |

根据原料,市场分为聚酯移植物、膨体聚四氟乙烯 (EPTFE) 移植物、生物合成移植物和聚氨酯移植物。聚酯移植物将占据主导地位,预计复合年增长率为 7.3%,到 2034 年其市场价值将达到 47 亿美元。它们在修復大血管和解决复杂心血管问题方面的广泛应用凸显了它们在市场成长中的关键作用。

根据应用,血管移植用于血管内动脉瘤修復 (EVAR)、血液透析通路和周边血管修復等手术。其中,EVAR 预计将达到显着成长,预计复合年增长率为 7.7%,到 2034 年将达到 35 亿美元。 这种微创手术具有切口小、恢復期短的特点,与传统开放式手术相比越来越受到青睐。其併发症风险降低,使其成为老年和高风险患者的理想解决方案,大大促进了其在全球范围内的采用。

在北美,血管移植市场预计将从 2024 年的 11 亿美元开始,从 2025 年到 2034 年的复合年增长率为 6.1%。广泛采用尖端医疗技术和完善的医疗保健基础设施使北美成为全球血管移植市场创新和需求的主要驱动力。

目录

第 1 章:方法论与范围

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 全球慢性病数量不断增加

- 发展中经济体末期肾病患者数量不断增加

- 已开发国家的技术进步

- 器官移植数量增加

- 产业陷阱与挑战

- 开发中国家缺乏技术人才

- 成长动力

- 成长潜力分析

- 监管格局

- 技术格局

- 差距分析

- 定价分析

- 波特的分析

- PESTEL 分析

- 未来市场趋势

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第 5 章:市场估计与预测:按原料,2021 – 2034 年

- 主要趋势

- 聚酯接枝物

- EPTFE 移植物

- 生物合成移植物

- 聚氨酯接枝物

第 6 章:市场估计与预测:按应用,2021 年至 2034 年

- 主要趋势

- 血管内动脉瘤修復

- 腹主动脉瘤修復

- 胸主动脉瘤修復

- 血液透析通路

- 周围血管修復

第 7 章:市场估计与预测:依最终用途,2021 年至 2034 年

- 主要趋势

- 医院

- 门诊手术中心

- 其他最终用途

第 8 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- Abbott

- ARTIVION

- B. Braun

- BD (Becton, Dickinson & Company)

- Cook Medical

- Cordis

- Endologix

- GETINGE

- LeMaitre

- Medtronic

- MERIT MEDICAL

- MicroPort

- TERUMO

- Vascular Graft Solutions

- GORE

The Global Vascular Graft Market, valued at USD 3.6 billion in 2024, is set to witness impressive growth, with a projected CAGR of 6.9% from 2025 to 2034. This robust expansion is driven by multiple factors, including the escalating prevalence of cardiovascular diseases, rising occurrences of end-stage renal disease (ESRD), and increasing surgical interventions. Furthermore, technological advancements in vascular grafts and the shift toward minimally invasive procedures are transforming the landscape, enhancing patient outcomes, and making surgical solutions more accessible and effective.

As healthcare systems worldwide grapple with aging populations and the associated rise in chronic conditions, the demand for vascular grafts continues to surge. Innovations in bioengineered and synthetic graft materials are addressing critical challenges such as biocompatibility, durability, and ease of use. Hybrid grafts, which combine the strengths of multiple materials, are also gaining traction for their ability to improve surgical success rates. With a greater emphasis on personalized healthcare, manufacturers invest in research and development to create next-generation grafts tailored to diverse medical needs, ensuring the market remains dynamic and competitive.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.6 Billion |

| Forecast Value | $7.3 Billion |

| CAGR | 6.9% |

The market is segmented by raw material into polyester grafts, expanded polytetrafluoroethylene (EPTFE) grafts, biosynthetic grafts, and polyurethane grafts. Polyester grafts are positioned to dominate, with an anticipated CAGR of 7.3%, driving their market value to USD 4.7 billion by 2034. These grafts, often constructed from materials like Dacron, are lauded for their strength and longevity, particularly in high-pressure vascular environments. Their widespread application in repairing large vessels and addressing complex cardiovascular challenges highlights their critical role in the market's growth.

By application, vascular grafts are utilized in procedures such as endovascular aneurysm repair (EVAR), hemodialysis access, and peripheral vascular repair. Among these, EVAR is poised for remarkable growth, with a projected CAGR of 7.7%, reaching USD 3.5 billion by 2034. This minimally invasive approach, characterized by smaller incisions and shorter recovery periods, is increasingly favored over traditional open surgeries. Its reduced risk of complications makes it an ideal solution for elderly and high-risk patients, significantly boosting its adoption globally.

In North America, the vascular graft market is projected to grow at a CAGR of 6.1% from 2025 to 2034, starting at USD 1.1 billion in 2024. The region remains a leader in embracing advanced surgical technologies, including EVAR, which often necessitates specialized grafts like stent grafts. The widespread adoption of cutting-edge medical techniques and a well-established healthcare infrastructure position North America as a key driver of innovation and demand within the global vascular graft market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing number of chronic diseases worldwide

- 3.2.1.2 Growing number of end-stage renal disorders in developing economies

- 3.2.1.3 Technological advancements in developed countries

- 3.2.1.4 Rise in organ transplantation

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of skilled personnel in developing countries

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Gap analysis

- 3.7 Pricing analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Raw Material, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Polyester grafts

- 5.3 EPTFE grafts

- 5.4 Biosynthetic grafts

- 5.5 Polyurethane grafts

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Endovascular aneurysm repair

- 6.2.1 Abdominal aortic aneurysm repair

- 6.2.2 Thoracic aortic aneurysm repair

- 6.3 Hemodialysis access

- 6.4 Peripheral vascular repair

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other End Use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott

- 9.2 ARTIVION

- 9.3 B. Braun

- 9.4 BD (Becton, Dickinson & Company)

- 9.5 Cook Medical

- 9.6 Cordis

- 9.7 Endologix

- 9.8 GETINGE

- 9.9 LeMaitre

- 9.10 Medtronic

- 9.11 MERIT MEDICAL

- 9.12 MicroPort

- 9.13 TERUMO

- 9.14 Vascular Graft Solutions

- 9.15 GORE

血管假体市场按产品类型、血管直径、适应症、最终用户和分销管道划分 - 全球预测 2025-2032

血管假体市场按产品类型、血管直径、适应症、最终用户和分销管道划分 - 全球预测 2025-2032 血管移植市场:2025-2030 年预测

血管移植市场:2025-2030 年预测 全球血管移植市场

全球血管移植市场 血管移植市场报告(按产品、原料(聚四氟乙烯、聚酯、聚氨酯、生物合成材料)、应用、最终用户(医院、门诊手术中心)和地区)2025 年至 2033 年血液透析血管移植市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

血管移植市场报告(按产品、原料(聚四氟乙烯、聚酯、聚氨酯、生物合成材料)、应用、最终用户(医院、门诊手术中心)和地区)2025 年至 2033 年血液透析血管移植市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 人造血管市场-全球产业规模、份额、趋势、机会及预测(按应用、按聚合物、按地区及竞争细分,2020-2030 年)血管移植市场-全球产业规模、份额、趋势、机会和预测(按产品、应用、地区和竞争细分,2020-2030 年)2021-2029年全球血管移植市场

人造血管市场-全球产业规模、份额、趋势、机会及预测(按应用、按聚合物、按地区及竞争细分,2020-2030 年)血管移植市场-全球产业规模、份额、趋势、机会和预测(按产品、应用、地区和竞争细分,2020-2030 年)2021-2029年全球血管移植市场 血管移植市场报告:2031 年趋势、预测与竞争分析

血管移植市场报告:2031 年趋势、预测与竞争分析 2025年全球血管人工移植市场报告

2025年全球血管人工移植市场报告