|

市场调查报告书

商品编码

1666688

汽车机器人市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Automotive Robotics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

2024 年全球汽车机器人市场价值为 97 亿美元,预计 2025 年至 2034 年期间的复合年增长率为 15.4%。机器人技术融入工业领域可确保更高的一致性、减少错误并提高生产力,自动化在组装、焊接和材料处理等关键操作中变得至关重要。

推动汽车机器人需求的主要因素之一是需要提高製造精度和效率。现代汽车设计,尤其是电动或混合动力车型的设计,要求更高的精度。机器人在执行焊接、喷漆和组装等任务方面发挥着至关重要的作用,这些任务的精确度都超越了手工劳动。重复任务的自动化减少了生产时间,提高了产量并维持了高品质标准。此外,工业 4.0 技术实现的机器人与物联网和智慧製造的整合优化了生产流程并降低了营运成本。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 97亿美元 |

| 预测值 | 384亿美元 |

| 复合年增长率 | 15.4% |

汽车机器人市场分为三个主要部分:硬体、软体和服务。其中,硬体部分占有最大份额,到 2024 年约占市场的 64%。随着对更先进、轻量化和精密硬体的需求不断增加,製造商不断投资尖端技术,以满足汽车生产的复杂需求。

就机器人类型而言,关节型机器人因其多功能性和精确度而占据市场主导地位。它们在执行焊接、喷漆和材料处理等任务时特别有效。关节机器人具有多轴运动和即时调整等先进功能,在汽车製造业中广泛使用。它们的灵活性使其能够满足大规模生产和客製化製造的需求,使其成为汽车产业自动化策略的重要组成部分。

在北美,美国汽车机器人市场规模预计到 2034 年将超过 99 亿美元。对灵活自动化系统的关注,包括人工智慧和协作机器人(cobots)的集成,预计将在塑造市场的未来方面发挥关键作用。

目录

第 1 章:方法论与范围

- 市场范围和定义

- 基础估算与计算

- 预测计算

- 资料来源

- 基本的

- 次要

- 付费来源

- 公共资源

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 供应商概况

- 利润率分析

- 重要新闻及倡议

- 监管格局

- 衝击力

- 成长动力

- 自动化需求增加

- 电动和自动驾驶汽车需求激增

- 关注安全和工人福祉

- 协作机器人的兴起

- 机器人技术不断进步

- 产业陷阱与挑战

- 初期投资高

- 机器人操作熟练劳动力短缺

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第 5 章:市场估计与预测:按组件,2021 年至 2034 年

- 主要趋势

- 硬体

- 控制器

- 机械手臂

- 末端执行器

- 感应器

- 视觉感测器

- 力/扭力感测器

- 其他的

- 其他的

- 软体

- 服务

第 6 章:市场估计与预测:按机器人类型,2021 年至 2034 年

- 主要趋势

- 关节型机器人

- 4 轴机器人

- 6 轴机器人

- 其他的

- Scara 机器人

- 笛卡儿机器人

- 圆柱形机器人

- 其他的

第 7 章:市场估计与预测:按应用,2021 年至 2034 年

- 主要趋势

- 物料处理

- 焊接

- 点焊

- 电弧焊

- 组装/拆卸

- 检查

- 切割和加工

- 物流和仓库自动化

- 其他的

第 8 章:市场估计与预测:依酬载容量,2021 年至 2034 年

- 主要趋势

- 最多 16 公斤

- 16–60公斤

- 60–225公斤

- 超过 225 公斤

第 9 章:市场估计与预测:按部署类型,2021 年至 2034 年

- 主要趋势

- 固定机器人

- 移动机器人

- 自动导引车 (AGV)

- 自主移动机器人 (AMR)

第 10 章:市场估计与预测:按技术,2021 年至 2034 年

- 主要趋势

- 机器学习和人工智慧

- 3D 视觉系统

- 物联网集成

- 云机器人

第 11 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 拉丁美洲其他地区

- 中东及非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

- MEA 其他地区

第 12 章:公司简介

- ABB

- Comau SpA

- Denso Wave

- Dürr AG

- Fanuc Corporation

- Harmonic Drive System

- Kawasaki Heavy Industries

- KUKA Robotics

- Nachi-Fujikoshi Corp

- Omron Corporation

- Panasonic Welding Systems Co. Ltd.

- Reis Gmbh & Co.

- Rockwell Automation

- Seiko Epson Corporation

- Stäubli

- Universal Robots

- Yamaha Robotics

- Yaskawa Electric Corporation

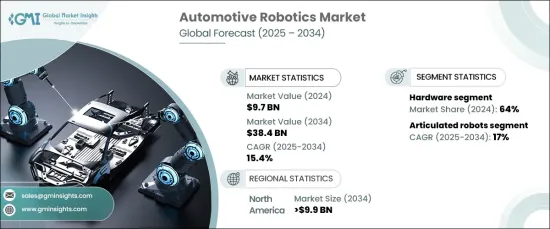

The Global Automotive Robotics Market, valued at USD 9.7 billion in 2024, is expected to expand at a CAGR of 15.4% from 2025 to 2034. This surge is driven by the increasing reliance on automation to streamline automotive manufacturing, improve efficiency, and enhance production quality. The integration of robotics into the industry ensures greater consistency, reduces errors, and boosts productivity, with automation becoming essential in key operations such as assembly, welding, and material handling.

One of the primary factors fueling the demand for automotive robotics is the need for improved manufacturing precision and efficiency. Modern vehicle designs, especially those involving electric or hybrid models, demand a higher level of accuracy. Robots are critical in performing tasks like welding, painting, and assembly, all with a level of precision that surpasses manual labor. The automation of repetitive tasks reduces production times, increases throughput, and maintains high-quality standards. Additionally, the integration of robotics with IoT and smart manufacturing, enabled by Industry 4.0 technologies, optimizes production workflows and lowers operational costs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.7 Billion |

| Forecast Value | $38.4 Billion |

| CAGR | 15.4% |

The automotive robotics market is divided into three key segments: hardware, software, and services. Among these, the hardware segment holds the largest share, accounting for approximately 64% of the market in 2024. This segment includes components like robotic arms, sensors, actuators, and controllers, which are crucial for enhancing the accuracy, speed, and durability of robotic systems. As the demand for more advanced, lightweight, and precise hardware increases, manufacturers continue to invest in cutting-edge technology to meet the complex demands of automotive production.

When it comes to robot types, articulated robots dominate the market due to their versatility and precision. They are particularly effective in performing tasks such as welding, painting, and material handling. The advanced capabilities of articulated robots, including multi-axis movement and real-time adjustments, contribute to their widespread use in automotive manufacturing. Their flexibility allows them to cater to both mass production and customized manufacturing needs, making them an essential part of the automotive sector's automation strategy.

In North America, the U.S. automotive robotics market is expected to exceed USD 9.9 billion by 2034. The country's growth in this sector is driven by advanced manufacturing technologies, the adoption of smart factories, and the rise of electric vehicles (EVs). The focus on flexible automation systems, including the integration of AI and collaborative robots (cobots), is expected to play a key role in shaping the market's future.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.7 Growth drivers

- 3.7.1 Increased demand for automation

- 3.7.2 Surge in demand for electric and autonomous vehicles

- 3.7.3 Focus on safety and worker well-being

- 3.7.4 Rise of collaborative robots (cobots)

- 3.7.5 Ongoing technological advancements in robotics

- 3.8 Industry pitfalls & challenges

- 3.8.1 High Initial Investment

- 3.8.2 Skilled labor shortages for robotics operation

- 3.9 Growth potential analysis

- 3.10 Porter’s analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021-2034 (USD billion)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Controller

- 5.2.2 Robot arm

- 5.2.3 End-effector

- 5.2.4 Sensors

- 5.2.4.1 Vision sensors

- 5.2.4.2 Force/torque sensors

- 5.2.4.3 Others

- 5.2.5 Others

- 5.3 Software

- 5.4 Service

Chapter 6 Market Estimates & Forecast, By Robot Type, 2021-2034 (USD billion)

- 6.1 Key trends

- 6.2 Articulated robots

- 6.2.1 4-axis robots

- 6.2.2 6-axis robots

- 6.2.3 Others

- 6.3 Scara robots

- 6.4 Cartesian robots

- 6.5 Cylindrical robots

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD billion)

- 7.1 Key trends

- 7.2 Material handling

- 7.3 Welding

- 7.3.1 Spot welding

- 7.3.2 Arc welding

- 7.4 Assembly/disassembly

- 7.5 Inspection

- 7.6 Cutting and processing

- 7.7 Logistics and warehouse automation

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By Payload Capacity, 2021-2034 (USD billion)

- 8.1 Key trends

- 8.2 Up to 16 kg

- 8.3 16–60 kg

- 8.4 60–225 kg

- 8.5 More than 225 kg

Chapter 9 Market Estimates & Forecast, By Deployment Type, 2021-2034 (USD billion)

- 9.1 Key trends

- 9.2 Fixed robots

- 9.3 Mobile robots

- 9.3.1 Automated Guided Vehicles (AGVs)

- 9.3.2 Autonomous Mobile Robots (AMRs)

Chapter 10 Market Estimates & Forecast, By Technology, 2021-2034 (USD billion)

- 10.1 Key trends

- 10.2 Machine learning and artificial intelligence

- 10.3 3D vision systems

- 10.4 IoT integration

- 10.5 Cloud robotics

Chapter 11 Market Estimates & Forecast, By Region, 2021-2034 (USD billion)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Rest of Latin America

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

- 11.6.4 Rest of MEA

Chapter 12 Company Profiles

- 12.1 ABB

- 12.2 Comau SpA

- 12.3 Denso Wave

- 12.4 Dürr AG

- 12.5 Fanuc Corporation

- 12.6 Harmonic Drive System

- 12.7 Kawasaki Heavy Industries

- 12.8 KUKA Robotics

- 12.9 Nachi-Fujikoshi Corp

- 12.10 Omron Corporation

- 12.11 Panasonic Welding Systems Co. Ltd.

- 12.12 Reis Gmbh & Co.

- 12.13 Rockwell Automation

- 12.14 Seiko Epson Corporation

- 12.15 Stäubli

- 12.16 Universal Robots

- 12.17 Yamaha Robotics

- 12.18 Yaskawa Electric Corporation

汽车机器人市场-全球产业规模、份额、趋势、机会及预测(依产品类型、组件、应用、地区及竞争格局划分,2021-2031年)

汽车机器人市场-全球产业规模、份额、趋势、机会及预测(依产品类型、组件、应用、地区及竞争格局划分,2021-2031年) 汽车喷涂机器人系统市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)汽车雷射焊接系统市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)汽车超音波焊接设备市场机会、成长动力、产业趋势分析及2025-2034年预测

汽车喷涂机器人系统市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)汽车雷射焊接系统市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)汽车超音波焊接设备市场机会、成长动力、产业趋势分析及2025-2034年预测 汽车和机器人工学的VLA大规模模式的应用(2025年)

汽车和机器人工学的VLA大规模模式的应用(2025年) 汽车机器人:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)

汽车机器人:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年) 汽车製造市场中的下一代机器人——全球和区域分析:重点关注应用、机器人类型和国家分析——分析与预测,2025-2034

汽车製造市场中的下一代机器人——全球和区域分析:重点关注应用、机器人类型和国家分析——分析与预测,2025-2034 汽车机器人市场报告(按产品类型、组件类型、应用、最终用户和地区)2025 年至 2033 年

汽车机器人市场报告(按产品类型、组件类型、应用、最终用户和地区)2025 年至 2033 年 汽车机器人市场规模、份额、成长分析(按类型、组件、应用和地区)—2025 年至 2032 年产业预测

汽车机器人市场规模、份额、成长分析(按类型、组件、应用和地区)—2025 年至 2032 年产业预测 2032 年汽车机器人市场预测:按产品类型、组件、部署类型、技术、应用、最终用户和地区进行的全球分析

2032 年汽车机器人市场预测:按产品类型、组件、部署类型、技术、应用、最终用户和地区进行的全球分析