|

市场调查报告书

商品编码

1666978

车载网路市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Vehicle Networking Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

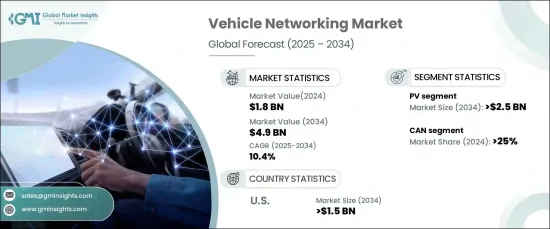

全球车辆网路市场在 2024 年的估值为 18 亿美元,预计在 2025 年至 2034 年期间将以 10.4% 的强劲复合年增长率增长。这些尖端技术实现了车辆和基础设施之间的无缝即时通信,提高了安全性、效率和整体驾驶体验。自动驾驶汽车的扩张进一步刺激了对先进网路解决方案的需求。高效的车对车 (V2V) 和车对基础设施 (V2I) 通讯对于自动驾驶汽车的顺利运行至关重要,使其成为未来汽车行业的关键组成部分。

此外,对车辆诊断和预测性维护的日益重视正在成为主要的市场驱动力。有了先进的网路技术,现在可以持续监控车辆性能,从而提前发现潜在问题。这种早期检测不仅可以确保更好的可靠性,而且还有助于降低维护成本和车辆停机时间,使个人消费者和车队营运商都受益。此外,即时防撞和紧急煞车等安全功能的进步也推动了对可靠、高性能车辆网路系统的需求。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 18亿美元 |

| 预测值 | 49亿美元 |

| 复合年增长率 | 10.4% |

就车辆类型而言,市场分为乘用车 (PV)、轻型商用车 (LCV)、重型商用车 (HCV) 和自动导引车 (AGV)。 2024 年,光伏市场占据了 50% 的主导份额,预计到 2034 年将达到 25 亿美元。 这种主导地位很大程度上是由于消费者对先进车载技术的需求不断增长,包括资讯娱乐系统、即时导航和增强的安全功能,这些功能越来越多地被纳入乘用车中。

在连接方面,车辆网路市场分为 LIN、CAN、RF、乙太网路、FlexRay 和 MOST。 CAN(控制器区域网路)领域由于其可靠性、稳健性和成本效益,在 2024 年占据了 25% 的份额。它广泛用于引擎控制和煞车等关键汽车系统中的即时资料传输,即使在电磁干扰严重的恶劣环境中也能提供出色的性能。

美国车联网市场在2024年处于领先地位,占全球90%的份额。由于美国成熟的汽车产业以及自动驾驶、电动车和 5G 连接等突破性技术的快速应用,美国市场规模预计到 2034 年将达到 15 亿美元。这些创新在很大程度上依赖先进的车联网解决方案,推动美国市场实现大幅成长。随着消费者期望的提高和技术的不断发展,车载网路市场将实现显着扩张,提供增强车辆连接性和性能的创新解决方案。

目录

第 1 章:方法论与范围

- 研究设计

- 研究方法

- 资料收集方法

- 基础估计和计算

- 基准年计算

- 市场估计的主要趋势

- 预测模型

- 初步研究与验证

- 主要来源

- 资料探勘来源

- 市场定义

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 供应商概况

- 技术提供者

- 服务提供者

- 经销商

- 最终用途

- 利润率分析

- 定价分析

- 成本明细

- 技术与创新格局

- 重要新闻及倡议

- 监管格局

- 衝击力

- 成长动力

- 政府专注于减少碳排放

- 电动车销量不断成长

- 政府支持汽车零件产业

- 市场参与者的策略性倡议

- 产业陷阱与挑战

- 电动车中半导体的消耗不断增加

- 发展中国家和欠发达国家缺乏自主行动基础设施

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:依车型,2021 - 2034 年

- 主要趋势

- 光电

- 轻型商用车

- 丙型肝炎病毒

- 自动导引车

第六章:市场估计与预测:依连结性,2021 - 2034 年

- 主要趋势

- CAN(控制器区域网路)

- LIN(本地互连网路)

- RF(射频)

- FlexRay

- 乙太网路

- MOST(媒体导向系统传输)

第 7 章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 动力传动系统

- 安全

- 车身电子

- 机壳

- 资讯娱乐

第 8 章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 西班牙

- 义大利

- 俄罗斯

- 北欧

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳新银行

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东及非洲

- 阿联酋

- 南非

- 沙乌地阿拉伯

第九章:公司简介

- Acome

- Analog Devices

- Bosch

- Broadcom

- Continental

- Intel

- Harman

- Marvell Semiconductor

- Microchip Technology

- NXP Semiconductors

- ON Semiconductor

- Qualcomm

- Renesas

- Sierra Wireless

- Spiarent

- Communications

- STMicroelectronics NV

- Texas Instrumental

- Toshiba

- Xilinx

The Global Vehicle Networking Market, with a valuation of USD 1.8 billion in 2024, is expected to grow at a robust CAGR of 10.4% from 2025 to 2034. This growth is primarily driven by the accelerating adoption of connected car technologies, fueled by the integration of the Internet of Things (IoT) and 5G networks. These cutting-edge technologies enable seamless real-time communication between vehicles and infrastructure, enhancing safety, efficiency, and the overall driving experience. The expansion of autonomous vehicles has further spurred demand for advanced networking solutions. Efficient vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2I) communication are vital for the smooth functioning of self-driving cars, making them a critical component in the future of the automotive industry.

Furthermore, the increasing emphasis on vehicle diagnostics and predictive maintenance is becoming a major market driver. With advanced networking technologies in place, continuous monitoring of vehicle performance is now possible, allowing for early detection of potential issues. This early detection not only ensures better reliability but also helps to reduce maintenance costs and vehicle downtime, benefiting both individual consumers and fleet operators. In addition, advancements in safety features, such as real-time collision avoidance and emergency braking, are pushing the need for reliable, high-performance vehicle networking systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Billion |

| Forecast Value | $4.9 Billion |

| CAGR | 10.4% |

In terms of vehicle types, the market is segmented into Passenger Vehicles (PV), Light Commercial Vehicles (LCV), Heavy Commercial Vehicles (HCV), and Autonomous Guided Vehicles (AGV). The PV segment held a dominant 50% share in 2024 and is forecast to reach USD 2.5 billion by 2034. This dominance is largely due to the growing consumer demand for advanced in-car technologies, including infotainment systems, real-time navigation, and enhanced safety features that are increasingly being incorporated into passenger vehicles.

On the connectivity front, the vehicle networking market is categorized into LIN, CAN, RF, Ethernet, FlexRay, and MOST. The CAN (Controller Area Network) segment held a 25% share in 2024 thanks to its reliability, robustness, and cost-effectiveness. It's widely used for real-time data transmission in critical automotive systems like engine control and braking, providing exceptional performance even in harsh environments with high electromagnetic interference.

The U.S. vehicle networking market was the leader in 2024, accounting for 90% of the global share. The market in the U.S. is expected to reach USD 1.5 billion by 2034, driven by the country's well-established automotive sector and rapid adoption of groundbreaking technologies such as autonomous driving, electric vehicles, and 5G connectivity. These innovations rely heavily on advanced vehicle networking solutions, propelling the U.S. market toward substantial growth. As consumer expectations rise and technology continues to evolve, the vehicle networking market is poised for remarkable expansion, delivering innovative solutions that enhance vehicle connectivity and performance.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Technology providers

- 3.2.2 Service providers

- 3.2.3 Distributors

- 3.2.4 End use

- 3.3 Profit margin analysis

- 3.4 Pricing analysis of

- 3.5 Cost breakdown

- 3.6 Technology & innovation landscape

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Government focus on reducing carbon emissions

- 3.9.1.2 Growing sales of electric vehicles

- 3.9.1.3 Government support for automotive components industry

- 3.9.1.4 Strategic initiatives by market players

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Increasing consumption of semiconductors in electric vehicles

- 3.9.2.2 Lack of autonomous mobility infrastructure in developing and underdeveloped countries

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 PV

- 5.3 LCV

- 5.4 HCV

- 5.5 AGV

Chapter 6 Market Estimates & Forecast, By Connectivity, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 CAN (Controller Area Network)

- 6.3 LIN (Local Interconnect Network)

- 6.4 RF (Radio Frequency)

- 6.5 FlexRay

- 6.6 Ethernet

- 6.7 MOST (Media Oriented Systems Transport)

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Powertrain

- 7.3 Safety

- 7.4 Body electronics

- 7.5 Chassis

- 7.6 Infotainment

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.3.7 Nordics

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 ANZ

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 South Africa

- 8.6.3 Saudi Arabia

Chapter 9 Company Profiles

- 9.1 Acome

- 9.2 Analog Devices

- 9.3 Bosch

- 9.4 Broadcom

- 9.5 Continental

- 9.6 Intel

- 9.7 Harman

- 9.8 Marvell Semiconductor

- 9.9 Microchip Technology

- 9.10 NXP Semiconductors

- 9.11 ON Semiconductor

- 9.12 Qualcomm

- 9.13 Renesas

- 9.14 Sierra Wireless

- 9.15 Spiarent

- 9.16 Communications

- 9.17 STMicroelectronics NV

- 9.18 Texas Instrumental

- 9.19 Toshiba

- 9.20 Xilinx

CAN总线显示器市场按车辆类型、显示技术、连接类型、分销管道和应用划分-全球预测,2026-2032年CAN汇流排介面模组市场按类型、资料速率、组件、应用和最终用户划分,全球预测,2026-2032年

CAN总线显示器市场按车辆类型、显示技术、连接类型、分销管道和应用划分-全球预测,2026-2032年CAN汇流排介面模组市场按类型、资料速率、组件、应用和最终用户划分,全球预测,2026-2032年 汽车网路存取设备市场 - 全球产业规模、份额、趋势、机会及预测(按车辆类型、需求类别、相容性、地区和竞争格局划分,2021-2031年)USB乙太网路桥接器市场按速度、介面、晶片组供应商、通路和最终用户划分-全球预测,2026-2032年低空通讯网路市场:按平台、应用、通讯技术、组件和最终用户分類的全球预测(2026-2032年)汽车乙太网路桥接IC市场:依资料速率、拓朴结构、车辆类型、车道数和应用划分-2026年至2032年全球预测

汽车网路存取设备市场 - 全球产业规模、份额、趋势、机会及预测(按车辆类型、需求类别、相容性、地区和竞争格局划分,2021-2031年)USB乙太网路桥接器市场按速度、介面、晶片组供应商、通路和最终用户划分-全球预测,2026-2032年低空通讯网路市场:按平台、应用、通讯技术、组件和最终用户分類的全球预测(2026-2032年)汽车乙太网路桥接IC市场:依资料速率、拓朴结构、车辆类型、车道数和应用划分-2026年至2032年全球预测 车载网路半导体市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)新一代车载网路市场(按网路技术、连接性、车辆类型、应用和最终用户划分)—全球预测 2025-2032

车载网路半导体市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)新一代车载网路市场(按网路技术、连接性、车辆类型、应用和最终用户划分)—全球预测 2025-2032 汽车用RF SoC·模组(2025年)

汽车用RF SoC·模组(2025年) 车载网路市场(按组件、按通讯协议、按网路类型、按应用、按国家和地区)-2025 年至 2032 年全球产业分析、市场规模、市场份额及预测

车载网路市场(按组件、按通讯协议、按网路类型、按应用、按国家和地区)-2025 年至 2032 年全球产业分析、市场规模、市场份额及预测