|

市场调查报告书

商品编码

1684684

船用感测器市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测Marine Transducers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

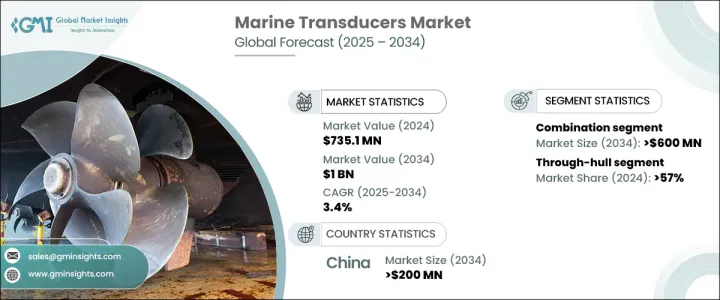

2024 年全球船用感测器市场价值为 7.351 亿美元,预计 2025 年至 2034 年期间的复合年增长率为 3.4%。这一成长主要得益于声纳和成像技术的快速进步,这不断提高水下可视化的精度、清晰度和有效性。 CHIRP 和侧扫声纳等尖端创新正在彻底改变水下成像,使导航、捕鱼和海洋研究更加准确和高效。

随着对高解析度声纳系统的需求不断增加,依赖船用感测器的行业正在采用复杂的解决方案来改善其营运。商业捕鱼、海军防御和海洋研究对即时资料的需求日益增长,进一步推动了市场扩张。此外,人工智慧和机器学习与声纳技术的结合正在提高检测能力,而无线连接和智慧功能则使船用感测器更加用户友好。这些因素共同促进了先进船用感测器的广泛应用,巩固了其在现代船用应用中的作用。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 7.351亿美元 |

| 预测值 | 10亿美元 |

| 复合年增长率 | 3.4% |

市场按类型细分,主要类别包括温度感测器、深度感测器、速度感测器和组合感测器。 2024 年,组合感测器将占据 60% 的市场份额,引领市场。预计到 2034 年,该领域将创造 6 亿美元的收入,这要归功于其将深度测量、鱼类检测和水下成像整合到单一设备中的多功能性。将多种功能整合到一个换能器中的能力显着降低了成本和空间要求,使其非常适合小型船舶和商业捕鱼应用。军事和研究领域对组合换能器的需求也在增加,因为效率和空间最佳化至关重要。

根据安装方法,市场分为船体安装式、船内安装式和船尾安装式感测器。 2024 年,船体感测器凭藉其出色的耐用性和在恶劣海洋环境中高效运作的能力,占据 57% 的份额。这些安装在水面下的感测器能够提供高度精确的深度和温度读数,在严苛的条件下其表现优于其他替代方案。它们在商业捕鱼、海上勘探和海军应用中的广泛应用继续增强了它们的需求。製造商也正在开发先进的材料和涂层以增强使用寿命和性能,使贯穿船体的感测器成为专业和工业应用的首选。

中国仍然是船用感测器市场的主导力量,到 2024 年将占全球销售额的 45%。到 2034 年,中国市场预计将创下 2 亿美元的产值。作为船舶电子和船舶製造领域的全球领导者,中国不断推动船舶感测器製造领域的创新和效率。该国完善的海军基础设施、不断扩张的航运业以及不断增加的海洋研发投资是推动成长的关键因素。政府支持的现代化渔船队和加强海上安全的措施进一步支持了市场扩张。凭藉强劲的国内需求和蓬勃发展的出口市场,中国预计在未来十年继续保持船用感测器生产的领先地位。

目录

第 1 章:方法论与范围

- 研究设计

- 研究方法

- 资料收集方法

- 基础估计和计算

- 基准年计算

- 市场估计的主要趋势

- 预测模型

- 初步研究与验证

- 主要来源

- 资料探勘来源

- 市场定义

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 供应商概况

- 利润率分析

- 定价分析

- 专利格局

- 成本明细

- 技术与创新格局

- 重要新闻及倡议

- 监管格局

- 衝击力

- 成长动力

- 声纳和成像技术的进步

- 休閒划船和钓鱼活动的成长

- 物联网和人工智慧船舶设备的采用日益广泛

- 扩大商业和国防海洋应用

- 产业陷阱与挑战

- 先进感测器和安装成本高

- 小型和非商用船舶的采用有限

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第 5 章:市场估计与预测:按类型,2021 - 2034 年

- 主要趋势

- 深度感测器

- 速度感测器

- 温度感测器

- 组合感测器

第 6 章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 商业运输

- 休閒划船

- 渔业

- 海军防御

- 海上能源勘探

- 海洋学研究

第 7 章:市场估计与预测:按安装量,2021 - 2032 年

- 主要趋势

- 贯穿船体

- 船体内

- 横樑安装

第 8 章:市场估计与预测:按技术,2021 - 2032 年

- 主要趋势

- 单光束

- 多光束

- 侧扫声纳

- 其他的

第 9 章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 西班牙

- 义大利

- 俄罗斯

- 北欧

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳新银行

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东及非洲

- 阿联酋

- 南非

- 沙乌地阿拉伯

第十章:公司简介

- Airmar

- Benthos

- BioSonics

- EdgeTech

- eSonar

- Furuno

- Garmin

- Hydroacoustic

- Johnson Outdoors

- Kongsberg

- Marport

- Navico

- Phoenix

- SAIYANG

- SEIWA

- Simrad

- Sonotronics

- Teledyne Technologies

- Tritech

- Wesmar

The Global Marine Transducers Market was valued at USD 735.1 million in 2024 and is expected to experience a CAGR of 3.4% between 2025 and 2034. This growth is primarily fueled by rapid advancements in sonar and imaging technologies, which continue to enhance the precision, clarity, and effectiveness of underwater visualizations. Cutting-edge innovations, such as CHIRP and side-scan sonars, are revolutionizing underwater imaging, making navigation, fishing, and marine research more accurate and efficient.

As demand for high-resolution sonar systems increases, industries that rely on marine transducers are adopting sophisticated solutions to improve their operations. The growing need for real-time data in commercial fishing, naval defense, and oceanographic research is further driving market expansion. Additionally, the integration of AI and machine learning into sonar technologies is improving detection capabilities, while wireless connectivity and smart features are making marine transducers more user-friendly. These factors collectively contribute to the increasing adoption of advanced marine transducers, solidifying their role in modern marine applications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $735.1 Million |

| Forecast Value | $1 Billion |

| CAGR | 3.4% |

The market is segmented by type, with key categories including temperature transducers, depth transducers, speed transducers, and combination transducers. In 2024, combination transducers led the market with a commanding 60% share. This segment is anticipated to generate USD 600 million by 2034, thanks to its multifunctional capabilities that integrate depth measurement, fish detection, and underwater imaging into a single device. The ability to consolidate multiple functionalities into one transducer significantly reduces costs and space requirements, making them highly preferred for smaller vessels and commercial fishing applications. The demand for combination transducers is also increasing in military and research sectors, where efficiency and space optimization are critical.

By installation method, the market is categorized into through-hull, in-hull, and transom-mount transducers. In 2024, through-hull transducers dominated with a 57% share due to their exceptional durability and ability to function efficiently in harsh marine environments. These transducers, installed beneath the water surface, provide highly accurate readings for depth and temperature, outperforming alternative options in challenging conditions. Their widespread use in commercial fishing, offshore exploration, and naval applications continues to bolster their demand. Manufacturers are also developing advanced materials and coatings to enhance longevity and performance, making through-hull transducers a preferred choice for professional and industrial applications.

China remains a dominant force in the marine transducers market, accounting for 45% of global sales in 2024. By 2034, the country's market is projected to generate USD 200 million. As a global leader in marine electronics and shipbuilding, China continues to drive innovation and efficiency in marine transducer manufacturing. The nation's well-developed naval infrastructure, expanding shipping industry, and increasing investments in marine research and development are key factors fueling growth. Government-backed initiatives to modernize fishing fleets and enhance maritime security further support market expansion. With strong domestic demand and a thriving export market, China is poised to remain at the forefront of marine transducer production in the coming decade.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.2 Pricing analysis

- 3.3 Patent landscape

- 3.4 Cost breakdown

- 3.5 Technology & innovation landscape

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Advancements in sonar and imaging technologies

- 3.8.1.2 Growth in recreational boating and fishing activities

- 3.8.1.3 Increasing adoption of IoT and AI-enabled marine devices

- 3.8.1.4 Expansion of commercial and defense marine applications

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High cost of advanced transducers and installation

- 3.8.2.2 Limited adoption in small and non-commercial vessels

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Depth transducers

- 5.3 Speed transducers

- 5.4 Temperature transducers

- 5.5 Combination transducers

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Commercial shipping

- 6.3 Recreational boating

- 6.4 Fisheries

- 6.5 Naval defense

- 6.6 Offshore energy exploration

- 6.7 Oceanographic research

Chapter 7 Market Estimates & Forecast, By Installation, 2021 - 2032 ($Bn, Units)

- 7.1 Key trends

- 7.2 Through-hull

- 7.3 In-hull

- 7.4 Transom-mount

Chapter 8 Market Estimates & Forecast, By Technology, 2021 - 2032 ($Bn, Units)

- 8.1 Key trends

- 8.2 Single beam

- 8.3 Multi-beam

- 8.4 Side-scan sonar

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Airmar

- 10.2 Benthos

- 10.3 BioSonics

- 10.4 EdgeTech

- 10.5 eSonar

- 10.6 Furuno

- 10.7 Garmin

- 10.8 Hydroacoustic

- 10.9 Johnson Outdoors

- 10.10 Kongsberg

- 10.11 Marport

- 10.12 Navico

- 10.13 Phoenix

- 10.14 SAIYANG

- 10.15 SEIWA

- 10.16 Simrad

- 10.17 Sonotronics

- 10.18 Teledyne Technologies

- 10.19 Tritech

- 10.20 Wesmar

电阻式真空感测器市场:依产品类型、应用、终端用户产业及通路划分,全球预测,2026-2032年

电阻式真空感测器市场:依产品类型、应用、终端用户产业及通路划分,全球预测,2026-2032年 全球封闭回路型电流感测器市场规模、份额、趋势和成长分析报告(2026-2034)全球开放回路感测器市场规模、份额、趋势和成长分析报告:2026-2034年超音波振动感测器市场按类型、频率范围、额定功率、应用、终端用户产业和销售管道,全球预测(2026-2032年)超音波换能器市场-2026-2031年预测

全球封闭回路型电流感测器市场规模、份额、趋势和成长分析报告(2026-2034)全球开放回路感测器市场规模、份额、趋势和成长分析报告:2026-2034年超音波振动感测器市场按类型、频率范围、额定功率、应用、终端用户产业和销售管道,全球预测(2026-2032年)超音波换能器市场-2026-2031年预测 开放回路电流感测器市场规模、份额、成长分析(按产品类型、应用、最终用户和地区划分)-2026-2033年产业预测感测器市场-2025-2030年预测

开放回路电流感测器市场规模、份额、成长分析(按产品类型、应用、最终用户和地区划分)-2026-2033年产业预测感测器市场-2025-2030年预测 全球封闭回路型系统市场:未来预测(至2032年)-按类型、组件、技术、应用、最终用户和地区进行分析

全球封闭回路型系统市场:未来预测(至2032年)-按类型、组件、技术、应用、最终用户和地区进行分析 全球封闭式冷却器市场

全球封闭式冷却器市场 工业开环电流感测器市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

工业开环电流感测器市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测