|

市场调查报告书

商品编码

1685071

乳製品包装机市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Dairy Packaging Machine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

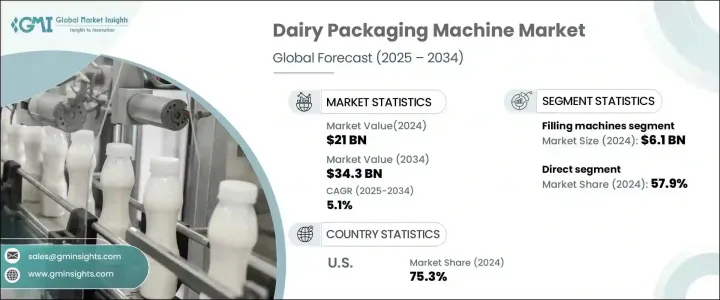

2024 年全球乳製品包装机市场价值为 210 亿美元,预计 2025 年至 2034 年期间的复合年增长率为 5.1%。全球人口的增加,加上可支配收入的增加,推动了全球乳製品消费的激增。牛奶、起司、优格和奶油等产品的需求正在增加,尤其是在新兴经济体中,城市化和饮食偏好的改变正在推动市场扩张。此外,消费者越来越重视食品的便利性、安全性和更长的保质期,迫使乳製品生产商投资先进的包装解决方案。

包装机在维持产品完整性、减少浪费和简化生产流程方面发挥关键作用。这些进步不仅满足了消费者的期望,而且还帮助製造商遵守严格的监管标准,为市场创造了巨大的成长机会。乳製品包装机械中自动化、物联网和永续发展技术的整合进一步提高了营运效率并解决了环境问题,为市场持续成长奠定了基础。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 210亿美元 |

| 预测值 | 343亿美元 |

| 复合年增长率 | 5.1% |

依类型,市场分为成型-填充-封口 (FFS) 机、码垛机、装盒机、灌装机、包装机、贴标机等。其中,灌装机成为 2024 年最高的收入来源,达到 61 亿美元,预计在预测期内的复合年增长率为 5.6%。灌装机是包装各种乳製品不可缺少的设备,包括液态奶、奶油、奶油和奶粉。它们能够处理各种产品黏度和包装形式,这对旨在满足日益增长的消费者需求的乳製品製造商来说是一项重要资产。

根据配销通路,市场分为直接分销和间接分销。直接细分市场在 2024 年占据了 57.9% 的市场份额,预计在预测期内的复合年增长率为 5.2%。直销因其提供客製化解决方案的效率以及促进製造商和买家之间的无缝沟通而占据市场主导地位。透过该管道,乳製品生产商能够获得符合特定营运需求和监管要求的客製化机械,为产业带来巨大的价值。

2024 年,美国乳製品包装机市场占据全球主导地位,占有 75.3% 的份额,预计在预测期内的复合年增长率为 4.9%。该国先进的乳製品行业受益于强大的供应链和大规模的生产设施,这些设施促进了创新包装技术的采用。对尖端乳製品加工和包装设备的大量投资进一步巩固了美国市场的领导地位,并强调了其对乳製品生产创新和效率的承诺。

目录

第 1 章:方法论与范围

- 市场范围和定义

- 基础估算与计算

- 预测计算

- 资料来源

- 基本的

- 次要

- 付费来源

- 公共资源

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 供应商概况

- 利润率分析

- 重要新闻及倡议

- 监管格局

- 衝击力

- 成长动力

- 全球对乳製品的需求不断增长

- 包装机械的技术进步

- 对永续和便捷包装的需求不断增长

- 产业陷阱与挑战

- 高资本投入

- 严格遵守法规

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第 5 章:乳製品包装机市场估计与预测:按类型,2021-2034 年

- 主要趋势

- 灌装机

- 成型-填充-封口 (FFS) 机

- 码高机

- 包装机

- 装盒机

- 贴标机

- 其他的

第 6 章:乳製品包装机市场估计与预测:依包装类型,2021-2034 年

- 主要趋势

- 灵活的

- 死板的

第 7 章:乳製品包装机市场估计与预测:按运营,2021-2034 年

- 主要趋势

- 自动的

- 半自动

第 8 章:乳製品包装机市场估计与预测:按应用,2021-2034 年

- 主要趋势

- 牛奶

- 新鲜乳製品

- 奶油和酪乳

- 奶粉

- 其他的

第 9 章:乳製品包装机市场估计与预测:按配销通路,2021-2034 年

- 主要趋势

- 直接的

- 间接

第 10 章:乳製品包装机市场估计与预测:按地区,2021-2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东及非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第 11 章:公司简介

- Alfa Laval

- Barry-Wehmiller

- Carpigiani

- DeLaval

- Feldmeier Equipment

- GEA

- IMA

- Krones

- Paul Mueller

- PFM

- Scherjon Dairy Equipment

- Sidel

- SPX Flow

- Technogel

- Tetra Pak

The Global Dairy Packaging Machine Market was valued at USD 21 billion in 2024 and is projected to grow at a CAGR of 5.1% from 2025 to 2034. The rising global population, coupled with increasing disposable incomes, is fueling a surge in dairy consumption worldwide. Products like milk, cheese, yogurt, and butter are witnessing heightened demand, especially in emerging economies where urbanization and changing dietary preferences are driving market expansion. Additionally, consumers are increasingly prioritizing convenience, safety, and longer shelf life in food products, compelling dairy producers to invest in advanced packaging solutions.

Packaging machines are playing a pivotal role in maintaining product integrity, reducing waste, and streamlining production processes. These advancements not only meet consumer expectations but also help manufacturers comply with stringent regulatory standards, creating significant growth opportunities in the market. The integration of automation, IoT, and sustainability-focused technologies in dairy packaging machinery is further elevating operational efficiency and addressing environmental concerns, positioning the market for sustained growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $21 Billion |

| Forecast Value | $34.3 Billion |

| CAGR | 5.1% |

The market is segmented by type into form-fill-seal (FFS) machines, palletizing machines, cartoning machines, filling machines, wrapping machines, labeling machines, and others. Among these, filling machines emerged as the highest revenue generator in 2024, reaching USD 6.1 billion, and are anticipated to grow at a CAGR of 5.6% during the forecast period. Filling machines are indispensable for packaging a variety of dairy products, including liquid milk, cream, butter, and powdered milk. Their ability to handle diverse product viscosities and packaging formats makes them a critical asset for dairy manufacturers aiming to meet the growing consumer demand.

By distribution channel, the market is divided into direct and indirect segments. The direct segment accounted for 57.9% of the market share in 2024 and is projected to grow at a CAGR of 5.2% during the forecast period. Direct sales dominate the market due to their efficiency in offering tailored solutions and facilitating seamless communication between manufacturers and buyers. This channel enables dairy producers to acquire custom-designed machinery that aligns with specific operational needs and regulatory requirements, delivering immense value to the industry.

The US dairy packaging machine market dominated the global landscape with a 75.3% share in 2024 and is expected to grow at a CAGR of 4.9% during the forecast period. The country's advanced dairy sector benefits from a robust supply chain and large-scale production facilities that promote the adoption of innovative packaging technologies. Significant investments in cutting-edge dairy processing and packaging equipment further solidify the US market's leadership and underscore its commitment to innovation and efficiency in dairy production.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rising global demand for dairy products

- 3.6.1.2 Technological advancements in packaging machinery

- 3.6.1.3 Growing demand for sustainable and convenient packaging

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High capital investment

- 3.6.2.2 Stringent regulatory compliance

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Dairy Packaging Machine Market Estimates & Forecast, By Type, 2021-2034 (USD Billion)

- 5.1 Key trends

- 5.2 Filling Machines

- 5.3 Form-Fill-Seal (FFS) Machines

- 5.4 Palletizing Machines

- 5.5 Wrapping Machines

- 5.6 Cartoning Machines

- 5.7 Labeling Machines

- 5.8 Others

Chapter 6 Dairy Packaging Machine Market Estimates & Forecast, By Packaging Type, 2021-2034 (USD Billion)

- 6.1 Key trends

- 6.2 Flexible

- 6.3 Rigid

Chapter 7 Dairy Packaging Machine Market Estimates & Forecast, By Operation, 2021-2034 (USD Billion)

- 7.1 Key trends

- 7.2 Automatic

- 7.3 Semi-automatic

Chapter 8 Dairy Packaging Machine Market Estimates & Forecast, By Application, 2021-2034 (USD Billion)

- 8.1 Key trends

- 8.2 Milk

- 8.3 Fresh Dairy Products

- 8.4 Butter & Buttermilk

- 8.5 Milk Powder

- 8.6 Others

Chapter 9 Dairy Packaging Machine Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Dairy Packaging Machine Market Estimates & Forecast, By Region, 2021-2034 (USD Billion)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Alfa Laval

- 11.2 Barry-Wehmiller

- 11.3 Carpigiani

- 11.4 DeLaval

- 11.5 Feldmeier Equipment

- 11.6 GEA

- 11.7 IMA

- 11.8 Krones

- 11.9 Paul Mueller

- 11.10 PFM

- 11.11 Scherjon Dairy Equipment

- 11.12 Sidel

- 11.13 SPX Flow

- 11.14 Technogel

- 11.15 Tetra Pak

全球乳製品包装市场规模、份额、趋势和成长分析报告(2026-2034年)全球乳製品包装市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析、未来预测(2026-2034)

全球乳製品包装市场规模、份额、趋势和成长分析报告(2026-2034年)全球乳製品包装市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析、未来预测(2026-2034) 乳製品包装市场规模、份额及成长分析(依材料、包装类型、产品类型及地区)-2025-2032 年产业预测

乳製品包装市场规模、份额及成长分析(依材料、包装类型、产品类型及地区)-2025-2032 年产业预测 2025 年至 2033 年乳製品包装市场报告(按包装材料、包装类型、产品类型、应用和地区)

2025 年至 2033 年乳製品包装市场报告(按包装材料、包装类型、产品类型、应用和地区) 乳製品包装市场机会、成长动力、产业趋势分析与预测 2025-2034

乳製品包装市场机会、成长动力、产业趋势分析与预测 2025-2034 乳製品包装:市场占有率分析、产业趋势、成长预测(2025-2030)拉丁美洲乳製品包装:市场占有率分析、行业趋势和成长预测(2025-2030 年)美国乳製品包装:市场占有率分析、产业趋势、产业趋势、成长预测(2025-2030)全球乳製品包装市场规模(按地区、范围和预测)

乳製品包装:市场占有率分析、产业趋势、成长预测(2025-2030)拉丁美洲乳製品包装:市场占有率分析、行业趋势和成长预测(2025-2030 年)美国乳製品包装:市场占有率分析、产业趋势、产业趋势、成长预测(2025-2030)全球乳製品包装市场规模(按地区、范围和预测)